admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

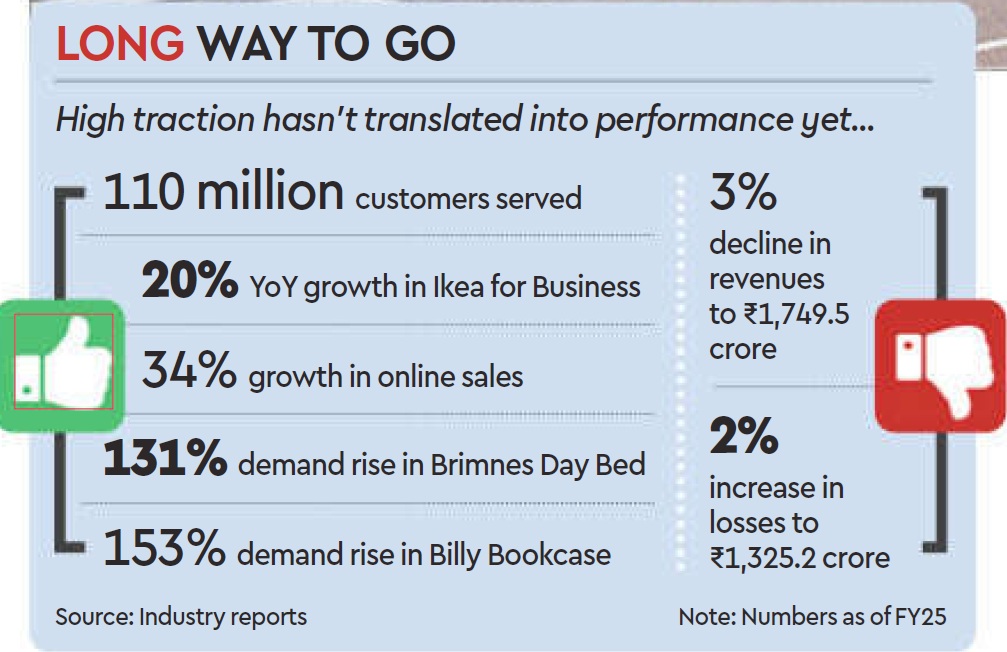

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

November 13, 2025

Saumyangi Yadav,Entrepreneur

Nov 13, 2025

India’s consumer landscape is undergoing a decisive shift in 2025. While D2C brands that once thrived on digital-only distribution are now aggressively building an offline footprint, legacy FMCG majors are simultaneously acquiring digital-first brands to strengthen their portfolios and tap into new consumer behaviours.

As analysts suggest, these trends signal a maturing phase for India’s D2C ecosystem, one that blends physical retail and strategic consolidation.

Offline Push Accelerates

According to a recent CBRE report, ‘India’s D2C Revolution: The New Retail Order’, D2C brands leased nearly 5.95 lakh sq ft of retail space between January and June 2025, accounting for 18 per cent of all retail leasing during this period, up sharply from 8 per cent in the first half of 2024. Fashion and apparel dominated the expansion, contributing close to 60 per cent of D2C leasing, followed by homeware and furnishings and jewellery at about 12 per cent each, while health and personal care brands accounted for roughly six per cent. The shift is equally visible in the choice of retail formats: 46 per cent of D2C leasing went to high streets, 40 per cent to malls, and the remaining to standalone stores, reflecting the category’s growing focus on visibility, trial and experiential discovery.

Experts suggest that it represents a strategic pivot to blended engagement.

As Devangshu Dutta, CEO of Third Eyesight, notes, “India’s D2C surge is powered by digital-first consumers, tremendous improvement in seamless logistics, and low-cost market entry, supported subsequently by substantial amounts of investor capital chasing those startups that stand out from the competition. Yet, lasting success demands a more holistic view: the divide between online and offline is a business construct, not a consumer reality. The larger chunk of retail sales still happens through physical channels and, for brands that want to be mainstream, an omnichannel presence is absolutely essential.”

This also aligns with the broader market outlook. The India Brand Equity Foundation (IBEF), in its Indian FMCG Industry Analysis (October 2025), estimates the value of India’s D2C market at USD 80 billion in 2024, with expectations of crossing USD 100 billion in 2025. Much of this growth is being led by categories that combine frequent purchase cycles with strong digital discovery, beauty, personal care, and food and beverage segments where consumers are open to experimentation but demand authenticity, transparency, and a compelling product narrative.

“The Gen Z and millennial consumer cohorts value newness but also authenticity and unique product stories, which are best communicated in spaces that are controlled by the brand,” Dutta added, “In the launch and growth phases, this could be the brand’s digital presence including website and social media, but over time this can include pop-up stores, kiosks, shop-in-shops and even exclusive brand stores.”

CBRE’s data reflects this shift clearly, with D2C brands increasingly opting for flexible store formats and high-street locations to maximise traffic and visibility.

M&A Gains Momentum

Parallel to the offline push is a noticeable wave of consolidation. Large FMCG companies are accelerating acquisitions to capture emerging consumer niches and strengthen their digital-native capabilities.

In recent years, Hindustan Unilever has acquired Minimalist; Marico has bought Beardo, Just Herbs, True Elements, and Plix; ITC has taken over Yoga Bar; and Emami has secured full ownership of The Man Company. These deals, reported widely across business media in 2024 and 2025, point to the need for established companies to fast-track entry into high-growth, ingredient-forward, and youth-focused categories without the lead time of in-house incubation.

“Legacy FMCG companies are acquiring D2C brands to rapidly gain access to new consumer segments, product innovation, and digital-native capabilities, including direct engagement and insights. Such deals enable large companies to diversify portfolios, accelerate entry into trending segments by-passing the initial launch risks, and rejuvenate their brands with modern digital marketing expertise,” Dutta explained.

Challenges and Risks

But the acquisitions do not come without risk and challenges, analysts warned.

“However, integrating D2C operations also poses challenges, including cultural differences, the risk of stifling entrepreneurial agility, and the need to harmonise data and omnichannel strategies. The ability to nurture acquired brands without diluting their distinctive appeal will determine acquisition success,” Dutta added.

Yet even as the ecosystem expands, challenges remain. Offline stores add operational complexity, inventory planning, staffing, last-mile logistics, and real-time data integration. Still, the bottom line is that India’s D2C sector is moving into a hybrid era defined by tighter omnichannel integration, sharper product storytelling, and portfolio realignment through acquisitions.

(Published in Entrepreneur)

admin

November 4, 2025

Yash Bhatia, IMPACT

4 November 2025

It started with groceries. Quick commerce started delivering milk, bread, and eggs in 10–15 minutes, which seemed revolutionary enough in 2022. Then came the iPhone 14 launch, and suddenly, quick commerce wasn’t just about convenience; it was about spectacle. Overnight, India’s app-based delivery ecosystem became the stage for a new ritual: flagship products arriving at your doorstep faster than you can say ‘checkout.’

And now? Phones aren’t the limit. You can even order motorcycles online. Yes, motorcycles. Royal Enfield has partnered with Flipkart to list its entire 350cc portfolio, which will be delivered to five cities: Bengaluru, Gurugram, Kolkata, Lucknow, and Mumbai.

The lines between e-commerce and quick commerce are becoming increasingly blurred. Flipkart’s Flipkart Minutes and Amazon’s instant delivery options are proof that speed is no longer a differentiator; it’s table stakes. And as platforms race to expand, high-ticket items are joining the frenzy, from electronics and furniture to watches, fitness equipment, and premium kitchen appliances. For platforms, these products are goldmines of margin; the challenge lies in logistics and consumer trust.

According to a report by CareEdge Advisory, India had over 270 million online shoppers in 2024, making it the second-largest e-retail user base globally, while the e-commerce market grew 23.8% in 2024 over the year-ago period, it said. The report also added that Indians ordered Rs 64,000 crore of goods from quick-commerce platforms.

From the consumer standpoint, one of the challenges for consumers to buy high-ticket items from the quick commerce platforms is to get consumer trust, which used to be the case when e-commerce started its operations. Can quick commerce move to high-ticket items? Is quick commerce looking at these items as a branding exercise, or are they looking at them as a serious revenue stream channel?

Chirag Taneja, Founder & CEO, GoKwik – an e-commerce enablement platform, says what began as a branding exercise for D2C brands has now evolved into a credible revenue stream. “In the early days, high-ticket categories on D2C platforms saw limited traction,” he explains. “Trust was still being built, customers were unsure if their orders would even reach them. There were many friction points.”

But that’s no longer the case. According to GoKwik’s network data, high-ticket purchases (above ₹2,500) are no longer outliers, they’re becoming a consistent driver of topline revenue.

Interestingly, most of these premium purchases are powered by credit instruments from no-cost EMIs to instant credit options at checkout. “This reflects a clear shift in mindset,” says Taneja. “Consumers no longer view high-value spending as a financial strain. They see it as a set of manageable, bite-sized payments that help them aspire higher, quicker. It’s not just a financial enabler, it’s a psychological unlock that makes premium consumption feel accessible and routine,” he adds.

“With strong trust in delivery reliability, smooth returns, and credible brand backing, the ecosystem has bridged the gap that once kept premium shopping offline,” says Taneja.

Devangshu Dutta, Founder of a specialist consulting firm, Third Eyesight, thinks differently and points out that high-value items still make up a small slice of quick commerce sales. “The model thrives on simplicity, a limited product range on the platform’s end, and quick, low-friction decision-making on the consumer’s,” he explains.

That said, Dutta believes quick commerce can still play a strategic role for premium brands. “For high-value products, q-comm can be an excellent lever for driving velocity, testing market response, or amplifying brand visibility. But it should be viewed as one piece of the channel mix, not the primary sales driver.”

From the platform’s perspective, however, listing high-ticket products brings its own upside. “They create excitement, boost average transaction values, and improve realised margins,” Dutta notes. “Consumers are often drawn in by novelty, exclusivity, or status appeal, especially during big launches or limited-time promotions.”

Still, he adds a note of realism: “Premium and high-ticket purchases largely remain planned decisions. Most consumers continue to prefer established offline and e-commerce channels for such buys where trust in authenticity, return policies, and after-sales services still carry greater weight than instant gratification.”

Seshu Kumar Tirumala, Chief Buying and Merchandising Officer, BigBasket, says the company doesn’t look at electronics as a high-ticket item category but rather focuses on building a complete category experience for customers. “For example, if we list an Enfield bike, we’d also want to offer spare parts, servicing options, and extended warranties, because that’s how the category functions,” he explains.

Tirumala adds that BigBasket adopted the same approach when it ventured into mobiles and mobile accessories. “When we launched this category last year, it was a trial. Today, it’s a sizable part of our business,” he says. Currently, electronics and mobile accessories contribute 5–10% of BigBasket’s monthly sales, having grown 250–300% year-on-year since the first iPhone launch on the platform.

While the launch day drives the highest demand for flagship devices like the iPhone, Tirumala notes that the following one to two months see strong accessory sales, from AirPods and headphones to chargers and power banks. “On average, mobiles and accessories account for 7–8% of our total sales, peaking at 10% during the festive season. Overall, this category has grown from zero to 7–8% of our total business in just a year, and we expect it to reach around 25% next year,” he adds.

Currently, the platform offers select models from smartphone brands, including OnePlus, Realme, Redmi, Vivo, and Oppo.

The Bengaluru-based platform is now piloting the delivery of large home appliances across across select city areas in partnership with Croma. If successful, BigBasket plans to expand this model to other cities, further broadening its quick commerce offering beyond everyday essentials.

Taneja points out that the traditional e-commerce model, once driven by discounts and affordability, is now evolving toward experience and access. Over the next few years, two major shifts will shape this transformation: credit-first commerce, where EMIs become the default mode for premium purchases, and aspirational commerce, where consumers view e-commerce as the easiest path to lifestyle upgrades. Consequently, platforms will need to reposition themselves from being “where you save more” to “where you unlock more”, prioritising personalisation, trust, and a seamless shopping experience.

As quick commerce matures, it is no longer just about instant gratification; it’s becoming a bridge between aspiration and accessibility.

Platforms are proving that speed, trust, and seamless experience can coexist with high-value purchases.

(Published in IMPACT)

Devangshu Dutta

January 5, 2010

If we were to look at phrases that have cropped up during the recent recessionary times in the consumer goods sector, “private label” has to be among those at the top of the list.

From clothing to cereals, toothpaste to televisions, there is hardly a category that has not seen retailers trying their hand at creating own labelled products.

The first motivation for most retailers to move into private label is margin. On first analysis, it appears that the branded suppliers are making tons of extra money by being out there in front of the consumer with a specific named product. The retailer finds that creating an alternative product under its own label allows it to capture extra gross margin. Typically the product category picked at the earliest stage of private label development would be one for which several generic or commodity suppliers are available.

At this early stage, the retailer is aiming for a relatively predictable, stable-demand and easily available product whose sales would be driven by the footfall that is already attracted into the store. A powerful bait to attract the customer is the visible reduction in price, as compared to a similar branded product. If the product can be compared like-for-like, customers would certainly convert to private label over time.

However, maintaining prices lower than brands can also be counter-productive. In many products, while customers might not be able to discern any qualitative difference, they may suspect that they are not getting a product comparable to one from a national or international brand. And while private label can drive off-take, the price differential can also erode gross margin which was the reason that the retailer may have got into private label in the first place. Over time, such a strategy can prove difficult to sustain, as costs of developing, sourcing and managing private label products move up.

The other strong reason a retailer chooses to have private label is to create a product offering that is differentiated from competitors who also offer brands that are similar or identical to the ones offered by the retailer. Department stores, supermarkets and hypermarkets around the world have all tried this approach – some have been more successful than others. The idea is to provide a customer strong reasons to visit their particular store, rather than any of the comparable competitors.

Of course, when differentiation is the operating factor, the products need more insight and development, and closer handling by the retailer at all stages. A price-driven private label line may be sourced from generic suppliers, but that approach isn’t good enough for a line driven by a differentiation strategy. In this case, costs of product development and management increase for the retailer. However, to compensate, the discount from a comparable national brand is not as high as generic nascent private label. In fact, some retailers have taken their private label to compete head on with national brands – they treat their private labels as respectfully as a national branded supplier would treat its brand.

So what does it take to go from a “copycat” to being a real brand?

Third Eyesight has evolved a Private Label Maturity Model (see the accompanying graphic) that can help retailers think through their approach to private label, whether their product offering is dominated by private label, or whether they have only just begun considering the possibility of including private label in their product range. The model sketches out a maturity path on five parameters that are affected by or influence the strength of a retailer’s private label offering:

In some cases, retailers may have multiple labels, some of which may be quite nascent while others might be highly evolved, clear and comparable to a national brand. This could be by default, because the labels have been launched at different times and have had more or less time to evolve. However, this can also be used as a conscious strategy to target various segments and competitive brands differently, depending on the strength of the competition and their relationship with the consumer.

The interesting thing is that size and scale do not offer any specific advantage to becoming a more sophisticated private label player. Some extremely large retailers continue to follow a discounted-price “me-too” private label strategy where even the packaging and colours of the product are copied from national brands, while much smaller players demonstrate capabilities to understand their specific consumers’ needs to design, source and promote proprietary products that compare with the best brands in the market.

For a moment, let’s also look at private labels from the suppliers’ point of view. As far as we can see, private label seems to be here to stay and grow. Suppliers can treat private labels as a threat, and figure out how to ensure that they retain a certain visibility and relationship with the consumer. On the other hand, interestingly, some suppliers are also looking at private label as an opportunity. They see the growth of private label as inevitable, and would much rather collaborate in the retailer’s private label development efforts. This way they can maintain some kind of influence on the product development, possibly avoid direct head-on conflict with their own star branded products and, if everything else fails, at least grab a share of the market that would have otherwise gone over to generic suppliers.

If you are retailer, I would suggest using the Private Label Maturity Model to clarify where you want to position yourself, and continue to use it as a guide as you develop and deliver your private label offering.

If you are a supplier concerned about private label, my suggestion would be to gauge how developed your customer is and is likely to become, and ensure that you are at least in step, if not a step ahead.

Of course, if you need support, we’ll only be too happy to help! (Contact Third Eyesight to discuss your private label needs.)