admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

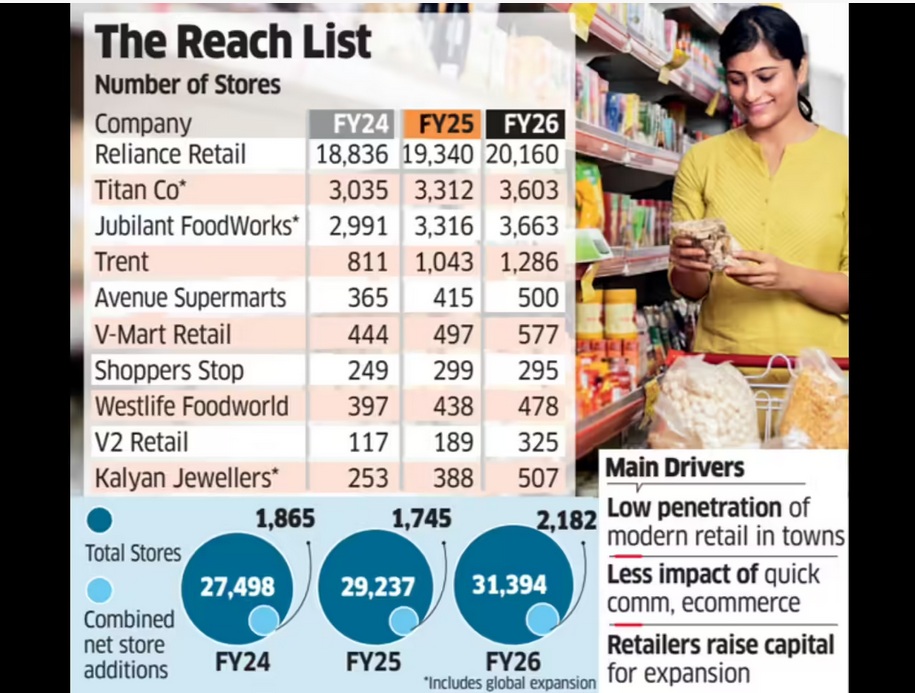

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

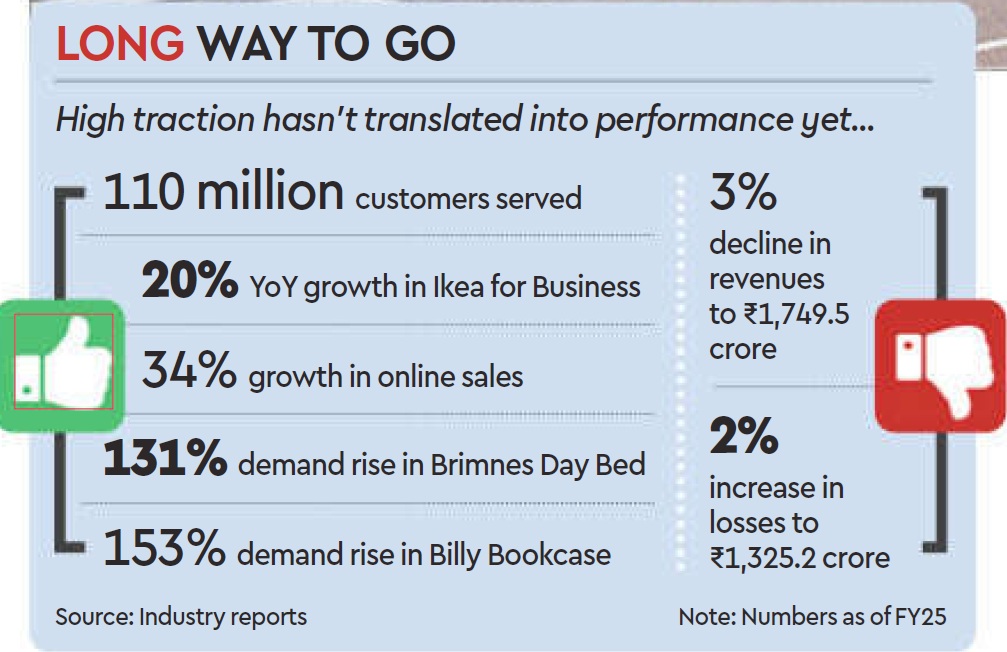

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

July 28, 2024

Writankar Mukherjee, Economic Times

Kolkata, 28 July 2024

Top retail chains such as Reliance Retail, Shoppers Stop and Spencer’s Retail are facing a prolonged slowdown in consumption, pushing them to exit unprofitable markets, raise debt and control costs.

India’s largest retailer Reliance Retail shuttered 249 stores in the three months ended June. The company is also going slow on expansion, opening 331 new stores in the quarter compared to 470-800 stores opened every quarter in FY22, FY23 and FY24. The closures mean the retail business of Reliance Industries made 82 net new store additions last quarter–the lowest in 15 quarters.

Spencer’s Retail has decided to completely exit North and South India markets by closing 49 stores in the National Capital Region (NCR), Andhra Pradesh and Telangana. The step will erase Rs 490 crore of annual revenue, but the company is hopeful it will improve profitability.

Shoppers Stop chief executive officer Kavindra Mishra told investors last week that it may have to defer a few store openings this fiscal due to regulatory and other issues. The company will also borrow Rs 100 crore for expansion with demand remaining soft.

Meanwhile, V-Mart Retail has closed 22 stores in the first six months of 2024, as per its latest investor presentation.

“Pruning underperforming locations is a natural reaction during times of demand stress,” said Devangshu Dutta, CEO of retail sector consulting firm Third Eyesight.

Pure Economics

“Demand forecasting can never be perfect due to a lag between demand assessment and supply. Retailers now try to do away with underperforming stores at the bottom of the pile quickly. Earlier there were prestige issues in shutting down stores, but now it’s acceptable industry practice and pure economics,” said Third Eyesight’s Dutta.

Analysts say most retailers expanded rapidly after the pandemic, banking on pent-up demand and revenge shopping at the time. With demand turning sluggish, the industry is now being forced to take various steps to sustain operations. At Reliance Retail, net profit rose by a modest 4.6% from a year earlier in the June quarter to Rs 2,549 crore while revenue grew 6.6% to Rs 66,260 crore. It was the slowest pace of revenue growth and came after a 9.8% increase in Q4FY24. Net profit and revenue from operations fell sequentially in the June quarter.

Spencer’s Retail CEO Anuj Singh told analysts on Thursday the 49 stores it is closing make up nearly 22% of revenue, but also Rs 56 crore of losses at the regional Ebitda level in North and South India. “They were a drag on the balance sheet. We will now focus on Uttar Pradesh and the East where there is a sizable consumption opportunity with a 250 million population,” he added.

Singh said the store rationalisation exercise and about 35% headcount reduction at corporate offices will reduce overheads from 8% operating cost to 6.3% of total sales. “We now expect to achieve Ebitda breakeven by March 2025 which will give us the option to raise capital,” he said.

Mishra at Shoppers Stop said demand remained subdued last quarter due to fewer wedding dates, long election season with polling dates on weekend, heatwaves, and high level of cumulative inflation. All these factors combined hit growth and volume recovery, except in value fashion and beauty.

More stores shut than opened

In fact, the sustained demand slowdown saw chains like Pantaloons, Spencer’s Retail and Nature’s Basket close more stores than they opened last fiscal. Retailers like V-Mart Retail, W, Aurelia and Titan Eye+ had a higher rate of store closures than openings in the March quarter.

(Published in Economic Times)

admin

October 26, 2023

Sagar Malviya, Economic Times

26 October 2023

Surging demand for fitness wear and sports equipment for disciplines other than cricket and football helped Decathlon’s India unit expand sales 37% to Rs 3,955 crore in FY23. With more than 100 large, warehouse-like stores selling products catering to 85 sporting disciplines, the French company is bigger than Adidas, Nike and Asics all put together in India.

In FY22, sales were Rs 2,936 crore, according to its latest filings with the Registrar of Companies. The retailer, however, posted a net loss of Rs 18.6 crore during the year ended March 2023 compared to a net profit of Rs 36 crore a year ago.

Experts said a host of factors – from pricing products about 30-40% lower than competing products to selling everything from running shoes, athleisure wear to mountaineering equipment under its own brands – has worked in its favour. “They have an extremely powerful format across different sporting activities and have something for both active and casual wear shoppers. For them, the market is still under penetrated with the kind of comprehensive product range they sell for outdoor sports beyond shoes and clothing,” said Devangshu Dutta, founder of retail consulting firm Third Eyesight. “Even their front end staff seem to have a strong domain knowledge about products compared to rival brands.”

By selling only private labels, Decathlon, the world’s biggest sporting goods firm, controls almost every bit of operations, from pricing and design to distribution, and keeps costs and selling prices low.

Decathlon uses a combination of in-house manufacturing and outsourcing to stock its shelves. In fact, it sources nearly 15% of its global requirement from India across sporting goods. And nearly all of its cricket merchandise sold globally is designed and made in India.

(Published in Economic Times)

admin

August 28, 2023

Bindu D. Menon, Financial Express

August 28, 2023

Calvin Klein, Levi’s, Adidas and Lacoste are among the several players who are looking to tap the potential of Outlet malls, which are generally located on the peripheries of cities and major highways. These malls are fast replacing the old factory outlets of major brands, which were located in the cities in crowded places.

Real estate developers are also strategically choosing such locations to attract a wider customer base. Value-driven customers are thronging to such malls as it offers branded products at a discounted price ranging from 30-70%.

A few companies FE spoke to said Outlet malls are refined version of factory outlets and companies are able to generate revenue by liquidating stocks at a lower price.

Outlet Malls are a concept popular in the international market and are a huge hit among travellers. They are typically large group of shops outside city periphery that sell apparel, shoes and luggage at a discounted price. In the last decade, Outlet malls have sprung all over the country especially adjoining highways.

In New Delhi’s Jasola district, Pacific Premium, real estate firm has opened premium shopping space. Pacific Group operates around six malls spread across Delhi and Dehradun. Its new premium outlet mall is its largest to date and has four storeys and sizeable parking area.

The mall houses aspirational brands such as Birkenstock, Tommy Hilfiger, CalvinKlein, Levi’s, Adidas, Madame, Lacoste, Vero Moda and American Eagle among others. Other leading brands such as Nykaa and CaratLane, too have signed lease for occupying mall space.

Players like Village Groupe are developing mixed use development space in off location like Khapoli on Mumbai-Pune highway, Ludhiana and even Jaipur highway. A company disclosure says that it is developing over 500,000 sq feet mixed use space off-city limits.

“Outlet malls are a great opportunity for consumers who want to get the touch and feel experience. To that they offer brands at a discounted price is huge attraction for consumers,” said Susil S Dungarwal, promoter, Beyond Squarefeet Advisory, a mall management advisory firm.

Asked if online companies will pose a challenge to Outlet malls, Dungarwal says that there is no competition. “Outlet malls are an impulse destination. A consumer may be travelling along a highway, a good mall with discounted brands will be sure shot attraction,” he said adding growth in private vehicles has given a shot in the arm to Outlet malls.

“Till mid 1990s only 20% of vehicles on highways were private vehicles (cars and buses) and the rest were commercial vehicles (trucks and lorries). However, in 2023, almost 60% of the vehicles on highways are private vehicles,” he said.

Devangshu Dutta, Founder, Third Eyesight, said, “Outlet (discount) stores sit at the confluence of a mutual need. Branded chains with excess inventory to liquidate which they don’t want to carry at their primary stores, and consumers who want lower prices for their purchases”.

He points that outlet malls can offer brands some of the same advantages as regular malls, in terms of acting as footfall magnets, and offer shared services, but at lower costs due to a cheaper location.

“Rather than creating their own standalone outlet stores, brands can take up spaces in an outlet mall. The challenge of maintaining and managing footfall is shifted to the mall. However, as with regular malls, outlet malls need to be located well and need to be also managed well,” he added.

According to consultancy firm Anarock, top cities have over 51 million sq feet of mall stocks across the country with Delhi-NCR, Mumbai Metropolitan Region and Bengaluru accounting for 62% of the total stock.

(Published in Financial Express)