admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

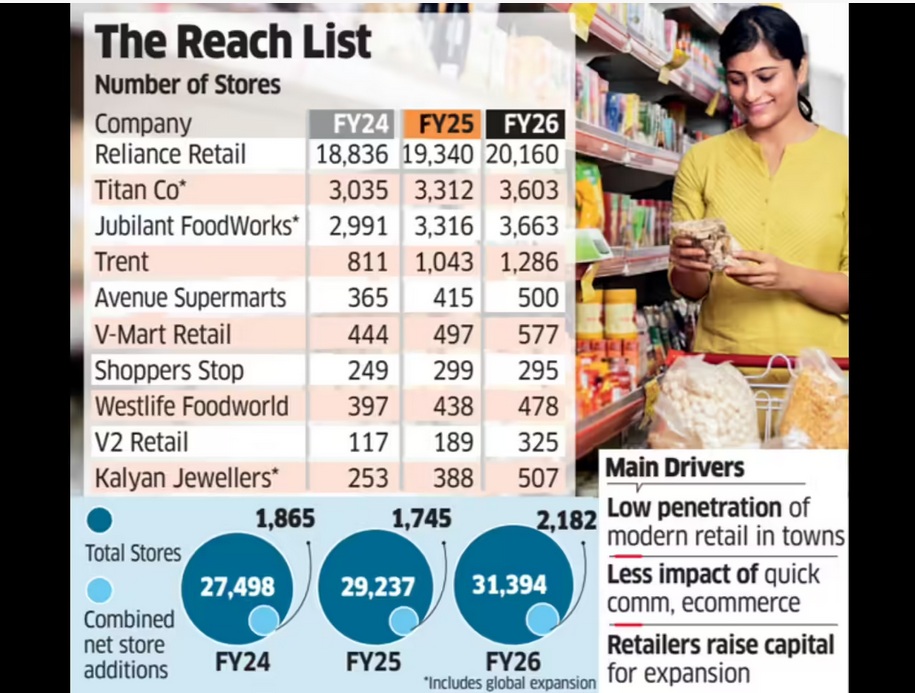

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

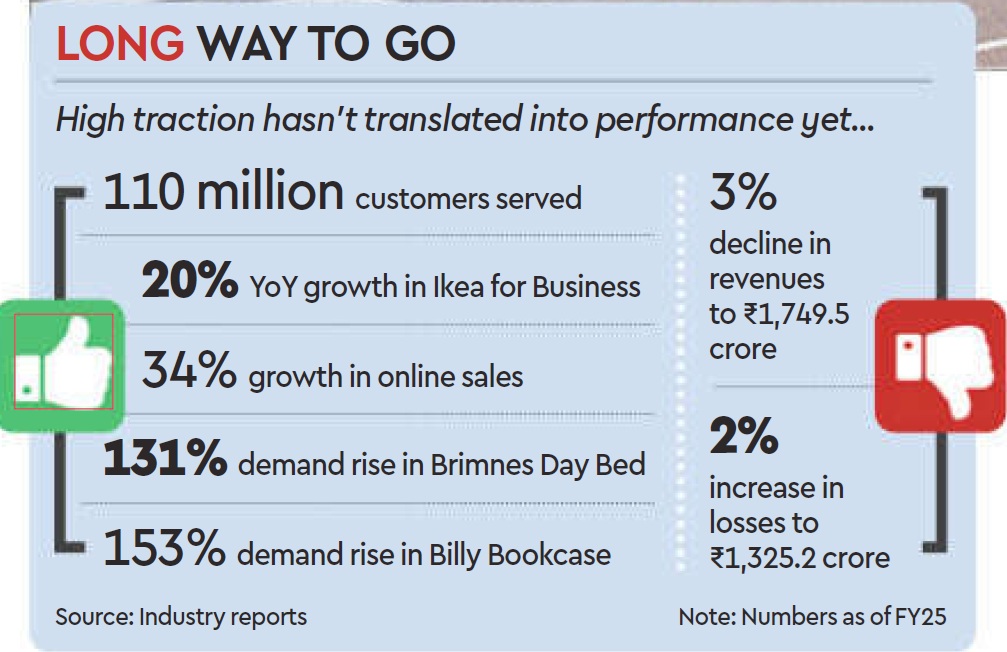

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

January 28, 2026

What does it actually take to build a fashion brand in India?

This panel (“Beyond the Noise- How D2c Fashion Brands Are Reinventing Retail”) at the 25th Edition of India Fashion Forum focussed on some real answers, in a refreshing, down-to-earth conversation moderated by Devangshu Dutta (Founder, Third Eyesight), with the founders of DeMoza (Agnes Raja George), The Mom Store (Surbhi Bhatia), Miraggio (Mohit Jain), BeyondBound (Tejasvi Madan), and Bari (Sameer Khan Lodhi).

No fluff, no “disrupting the industry” talk. Just founders being honest about what’s worked, what hasn’t, and what they’d do differently. A few things that struck a chord:

• Every single brand started because the founder couldn’t find something they personally wanted: inclusive activewear, affordable handbags that didn’t look cheap, good maternity wear. Sometimes the simplest observation is the best business idea.

• Inventory management came up often. One founder took their inventory cycle from 6 months down to 4. Another re-shuffles stock every 15 days based on what’s selling where. Unglamorous? Yes, but this is what actually keeps a business alive.

• The marketing conversation highlighted a move away from traditional advertising toward things that actually make people feel something. One founder talked about turning a farmhouse into a full “apricot colour” experience for customers. Another shoots content with real customers, not influencers.

• And the most memorable line of the whole discussion came from the most experienced founder in the room sharing a learning: “I won’t open stores fast.” No explanation needed, really.

Building a brand is exciting. Keeping it alive is the harder, quieter work. This panel was a good reminder of that. Worth a watch if you’re building something in this space.

admin

January 6, 2026

Saumyangi Yadav, Entrepreneur India

Jan 6, 2026

After years of rapid growth and a sharp reset, India’s direct-to-consumer (D2C) sector is expected to settle into a more balanced phase. The period of easy funding, aggressive customer acquisition and scale-at-all-costs expansion is clearly over, experts suggest. Now, what lies ahead in 2026 is a shift towards steadier growth driven by better execution, stronger retention and clearer brand positioning.

According to Bain and Flipkart, India’s e-retail market is projected to reach $170–190 billion in GMV by 2030, driven by a growing online shopper base and evolving commerce models. As adoption deepens across Tier-2 and Tier-3 cities, high-frequency categories such as grocery and lifestyle are expected to drive a larger share of growth, making repeat purchase and habit formation critical for D2C brands.

Against this backdrop, 2026 is shaping up as the year when D2C brands are judged less on ambition and more on outcomes.

A Post-Hype Phase of D2C

Industry observers say the D2C ecosystem has clearly moved beyond its hype-driven phase. Devangshu Dutta, Founder and Chief Executive of retail consultancy Third Eyesight, describes the current moment as one of structural correction rather than contraction.

“India’s D2C ecosystem is in a post-hype phase where growth may be slower but structurally healthier,” Dutta says, adding, “Earlier growth cycles prioritised visibility and sales at the expense of profitability and consistency. Now, success is being measured by repeat rates, contribution margins and the ability to fund growth internally.”

Tighter funding is also driving this shift. With D2C investments slowing and overall capital remaining cautious, brands are now being pushed to show predictability rather than promise. Tracxn data shows Indian D2C startups raised USD 757 million in 2024, significantly lower than previous years, while overall PE-VC investments in India remained flat at USD 33 billion in 2025, according to Venture Intelligence.

As a result, Dutta notes that many D2C companies are rationalising portfolios, tightening inventory cycles and optimising supply chains. Marketing strategies, too, are evolving, with greater emphasis on retention, community-building and owned channels instead of discount-led growth.

Uniqueness Will Define Winners

If capital discipline is one defining force, speed is another. Harish Bijoor, business and brand strategy expert, argues that D2C’s next phase will be shaped by how brands respond to a faster, more fragmented commerce environment.

“The e-commerce revolution led to a more refined orientation of D2C, and that has now given way to a q-commerce revolution that is even faster,” Bijoor says, adding, “The D2C revolution is going to be leveraged by speed. A whole host of players will invest time, energy and innovation into this.”

In Bijoor’s view, traditional e-commerce is now the slowest layer in a spectrum where quick commerce is the fastest, and D2C sits in between. In such a landscape, competing purely on price is no longer sustainable. He believes differentiation will increasingly come from uniqueness and premium positioning rather than ubiquity.

“When you know that you get a particular great-tasting biryani at just one place with no branches, you will go to that place. That uniqueness is what will distinguish D2C commerce in the future,” he says.

Bijoor adds that many D2C brands have been trapped in price wars under the guise of differentiation. He also argued that brands that premiumise and resist excessive omnichannel dilution are more likely to build desirability and long-term value.

Consumers Move Beyond Metros

Structural shifts in demand are reshaping how and where D2C brands grow. India now has one of the world’s largest and most diverse online consumer bases, with growth increasingly driven by Tier-2, Tier-3 and smaller towns rather than metros alone. Internet adoption continues to deepen across rural and semi-urban India, expanding the addressable market well beyond early digital buyers.

This widening base is changing the nature of growth. Consumers are becoming more deliberate in how they spend, weighing value, quality and trust more carefully than before.

As Devangshu Dutta notes, Indian consumers have always been discerning, but rising living costs and economic uncertainty have made them even more thoughtful, pushing brands to earn repeat demand rather than rely on impulse or discount-led purchases.

“Value is not just about discounts,” he says. “It’s a balance of price, performance and trust. For D2C brands, repeat consumption has to be earned through consistent quality, transparent pricing and dependable service.”

High-frequency categories such as grocery, lifestyle and general merchandise are expected to drive much of this expansion. Bain estimates these segments will account for two out of every three e-retail dollars by 2030, reinforcing the importance of habit formation and retention-led models.

Quick Commerce Expands Discovery, Not Profitability

Quick commerce has emerged as a powerful but complex growth lever for D2C brands. The format now accounts for a significant share of India’s e-grocery demand and has scaled into a multi-billion-dollar market, becoming a key discovery channel for food and everyday consumption brands.

However, expansion beyond metros remains challenging. RedSeer data shows non-metro markets contribute just over 20 per cent of quick commerce GMV, even as platforms scale to over 150 cities, with breakeven economics in smaller towns requiring significantly higher throughput.

Praveen Govindu, partner at Deloitte India, cautions that while quick commerce has helped many D2C brands gain discovery, particularly in food and beverage, it is not a sustainable growth engine on its own.

“From a customer acquisition standpoint, quick commerce is not fundamentally different from traditional e-commerce,” Govindu says, adding, “It is an expensive channel, and competition will only intensify. Over the long term, brands cannot rely on burning capital there.”

Omnichannel Enters Its Toughest Phase Yet

As digital acquisition costs rise, India’s ad market is projected to grow nearly 8 per cent in 2025 to Rs 1.37 lakh crore, with digital accounting for almost half of the spends, brands are being pushed to diversify distribution. Yet omnichannel presence alone is no longer enough.

“Many brands talk about omnichannel, personalisation and seamless journeys, but in practice these efforts are still disjointed. In 2026, the focus will shift from intent to execution,” Govindu says.

RedSeer projects India’s retail market to cross USD 2 trillion by 2030, with nearly 90 per cent of consumption still happening offline. For D2C brands, this makes offline expansion unavoidable, but success will depend on consistent execution across pricing, inventory, service and communication.

Consumers, Govindu notes, do not consciously differentiate between online, offline or social platforms. “They simply want a consistent experience,” he says. “Even small inconsistencies can erode trust.”

AI-Led Discovery and Experience

Perhaps the most transformative force shaping 2026 will be the evolution of buying journeys themselves. Govindu sees the rise of AI-led and agentic commerce as a major inflection point.

“Conversational platforms and AI-driven assistants will increasingly influence discovery, purchase, fulfilment and post-sales experiences. What earlier happened across multiple touchpoints is now beginning to happen in one place,” he says.

This convergence amplifies the importance of content-led discovery, owned data and deep consumer understanding. Brands that can unify storytelling, commerce and service into a coherent narrative are more likely to build loyalty in an environment where switching costs are low and alternatives are abundant.

Whether growth comes through D2C websites, marketplaces, quick commerce or offline stores, experts agree that the real differentiator will be a brand’s ability to build durable consumer relationships. As investors shift focus from short-term metrics to long-term value creation like retention, margins and brand strength, the next phase of India’s D2C story is less about rapid expansion and more about refinement.

(Published in Entrepreneur India)

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

admin

December 15, 2025

By Saumyangi Yadav, Entrepreneur India

Dec 15, 2025

India’s D2C ecosystem has grown rapidly over the past five years, but scale remains elusive. While thousands of brands have launched and many have crossed early revenue milestones, only a small fraction manage to break past INR 100 crore in annual revenue. According to a new report by DSG Consumer Partners, based on a survey of over 100 Indian D2C founders and operators, the problem is not demand or product-market fit, it is how brands attempt to scale.

The report shows that around 60–65 per cent of Indian D2C brands remain stuck in the INR 1–50 crore revenue band, with very few reaching the INR 100 crore mark. This stage marks the point where early traction exists, but growth begins to strain unit economics, teams, and operating systems.

Insights from over 100 D2C founders reveal that India’s fastest-growing brands win on fundamentals rather than speed alone. Clear product-market fit, disciplined data tracking, strong unit economics, creative velocity, and an early focus on retention consistently separate scalable brands from those that plateau. Founders also admit that performance marketing mistakes, pricing missteps, and weak creative systems slow growth far more than budget constraints. In a booming D2C landscape, capability gaps in operations, brand-building, and supply-chain depth are widening the divide between breakout brands and those stuck in the performance plateau.

Industry observers argue that this is where many brands mistake rapid online growth for sustainable scale.

As Devangshu Dutta, Founder & CEO, Third Eyesight, explains, “Scaling up online can be very rapid, but is also capital-hungry in terms of CAC. Given the intense competition, the lack of customer stickiness and the power of platforms, there is a constant churn of marketing spend which is a huge bleed for growing brands.”

CAC Inflation is The Real Constraint

One of the clearest findings from the playbook is that acquisition efficiency, rising CAC and unstable ROAS, is the single biggest blocker to growth, cited by more founders than funding or category expansion. Moreover, over 70 per cent of brands rely on Meta as their primary acquisition channel, increasing vulnerability to auction pressure and platform-driven volatility.

Dutta links this directly to the limits of a digital-only mindset. “Limited offline expansion can trap brands in narrow urban digital markets, blocking broader scale,” he said.

This over-reliance on online performance marketing often leads to growth that looks strong on dashboards but weak on cash flow.

Highlighting their report, Pooja Shirali, Vice President, DSG Consumer Partners, said, “Across over 90 consumer brands we’ve partnered with at DSGCP, one truth is clear: brands that master Meta’s ecosystem don’t just grow, they change their entire trajectory through strategic clarity and disciplined execution. The real drivers of scale have less to do with viral moments, and everything to do with the long-term fundamentals that make milestones like the first INR 100 crore predictable, not accidental.”

Why Omnichannel is Unavoidable

The report suggests that brands that scale sustainably are those that reduce overdependence on paid digital acquisition and expand their distribution footprint. However, offline expansion brings its own complexity.

Dutta stresses that omnichannel is not an optional add-on, but a strategic shift. “D2C brands must adopt an omnichannel approach, blending online with offline retail for sustainable and scalable reach. Clearly the channels work very differently and management teams have to be prepared and capitalised for the long haul to tackle acquiring customers with channel-appropriate strategies,” he adds.

This aligns with the DSGCP report’s broader insight that scale breaks down when brands fail to adapt operating models as they grow.

Even within digital channels, performance weakens over time. The playbook finds that 62 per cent of founders report creative fatigue, where repeated creatives fail to sustain ROAS despite higher spends. At the same time, 55 per cent admit to under-investing in CRM and retention, with most brands reporting repeat purchase rates of just 10–30 per cent.

Both the data and expert opinion point to a common theme: brands that cross the INR 100 crore mark are structurally different. They obsess over unit economics, processes, and capital efficiency rather than topline growth alone.

As Dutta puts it, “Scalable brands that cross the growth hump have leadership obsessed with unit economics and omnichannel execution rather than chasing vanity metrics. Cash always was and is king, especially at early stages of growth.”

He adds that execution strength matters as much as strategy. “They are able to grow and steer teams that build and replicate processes fast rather than spending time, effort and money reinventing all the time, and do so without constant CXO intervention.”

As competition intensifies and capital becomes more selective, the next generation of INR 100 crore D2C brands is likely to be defined not by speed, but by the ability to compound cash flows, institutionalise processes, and scale distribution beyond digital platforms.

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

(Published in Entrepreneur India)