admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

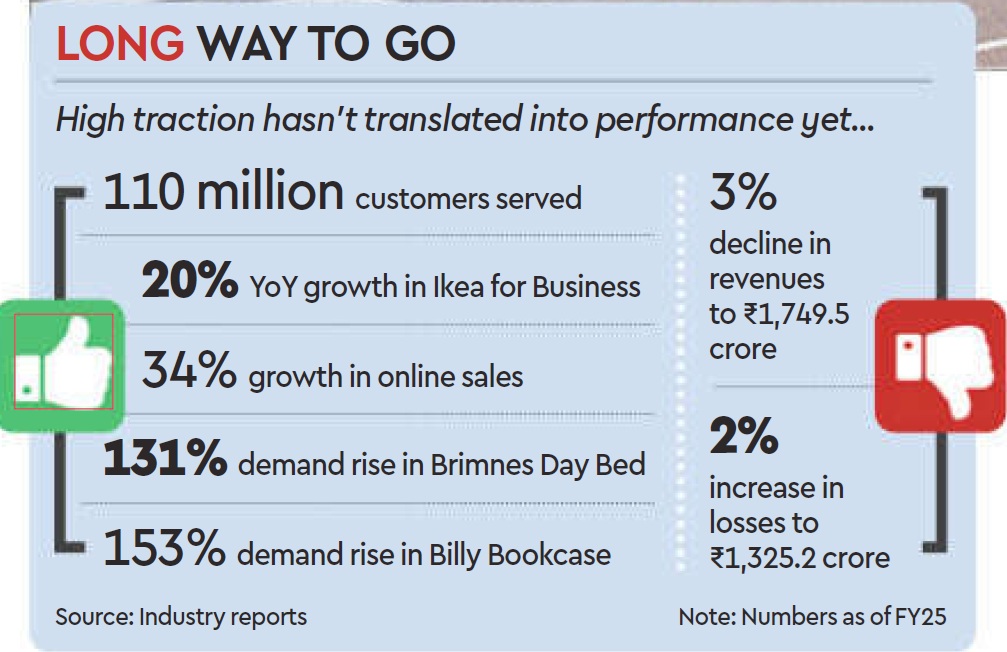

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

July 10, 2025

Alka Jain, Outlook Business

10 July 2025

Just when Blinkit, Instamart and Zepto were slowing down in their quick commerce game, Amazon’s entry may spur them towards a more aggressive race. The ecommerce giant has begun offering deliveries in as little as ten minutes in Delhi after Bengaluru, under the name ‘Amazon Now’.

“We are excited with the initial customer response and positive feedback, especially from Prime members. Based on this, we are now expanding the service over the next few months addressing immediate customer needs while maintaining Amazon’s standards for safety, quality and reliability,” the company said in an official statement.

Till now, the company was moving at its own pace with the idea that Indian consumers would wait a day or two for their deliveries. But the game has changed now—convenience is king here. Online shoppers want everything from milk to mobile chargers within a few minutes at their doorsteps.

And the big three of the quick commerce market—Blinkit, Instamart, Zepto—have cracked the consumer code perfectly. This trend has nudged Amazon and Flipkart to enter the 10-minute delivery segment. It started as an experiment in the larger ecommerce sector but has now become a necessity for online retailers.

Kathryn McLay, chief executive of Walmart International—an American multinational retail corporation—revealed that quick commerce now accounts for 20% of India’s ecommerce market and is growing at a rate of 50% annually. According to a Morgan Stanley report, the market is expected to reach $57bn by 2030.

Hence, Amazon could not afford to stay on the sidelines. The company has already pumped $11bn into Indian market since 2013 and recently announced another $233mn to upgrade its infrastructure and speed up deliveries. In addition, it has also opened five fulfilment centres across the country.

Despite continued investment, there are doubts if Amazon can disrupt the quick commerce game. Industry experts state that the ecommerce major’s late entry could upend the fragile unit economics of the space. It can even reignite discount wars and increase burn rate (a company spending its cash reserve while going through loss) for the incumbents, once the ecommerce giants begin to exert pressure and begin to capture market share.

Open Market, Thin Margins

Given the growth momentum and market size, quick commerce start-up Kiko.live cofounder Alok Chawla believes that there is definitely headroom to accommodate another player in the quick commerce market. However, margins may remain negative for a couple of years due to high business and delivery costs.

As per data, the average order value of ₹350–₹400 yields a gross margin of approximately 20% but high fulfilment and delivery costs (₹50–₹60 per order) significantly reduce overall profitability, often cancelling out most of the gains.

“Indian customers will not be willing to pay high shipping charges for convenience. But the market will continue to grow due to cart subsidies and shipping discounts. On top of this, profitability also remains quite some time away,” he says.

Even a survey by Grant Thornton Bharat, a professional services firm, shows that 81% of Indian quick commerce users cite discounts and offers as one of the main reasons they shop on platforms like Blinkit and Instamart.

But the fact is Amazon has extremely deep pockets, which means, the trio will once again have to get into aggressive discounting to protect their turf, said Chawla, indicating the possibility of higher cash burn quarters ahead.

In February, reports revealed that Indian quick commerce companies, including new entrants, were burning cash to the tune of ₹1,300–₹1,500 crore on a monthly basis. But a few months later, Aadit Palicha, chief executive of Zepto, a fast-growing 10-minute delivery platform, claimed that the company had slashed its operating cash burn by 50% in the previous quarter.

Still, the path to profitability remains shaky. Though Amazon can get an advantage of its existing huge customer base that is habitual of making online purchases including those in similar categories.

The real challenge lies beneath the surface because ecommerce and quick commerce operate on fundamentally different engines.

E-Comm vs Q-Comm: A Different Game

It may seem like a simple extension of what Amazon already does: deliver products. But in practice, the logistics, timelines and cost structures behind traditional ecommerce and quick commerce are different, said Somdutta Singh, founder and chief executive of Assiduus Global, a cross-border ecommerce accelerator that helps brands scale on global marketplaces through end-to-end solutions.

She explains the difference using a hypothetical situation: let’s say you order a phone case in Mumbai, which is picked from a nearby fulfilment centre. It will be added to a pre-routed delivery run with 30-50 other stops. This batching on the basis of route optimisation, keeps last-mile costs low, somewhere around ₹40–₹80.

But if you order the same item in a smaller town like Alleppey, it may first travel mid-mile from a hub in Cochin, then be handed off to a local partner like India Post. This increases the delivery time but keeps costs manageable through scale and planned routing.

This setup suits well in ecommerce business, which is built for reach and variety, not for speed. However, quick commerce runs on a completely different playbook because speed becomes priority here.

For instance, you order a pack of chips and a cold drink via Zepto in Andheri. These items are already stocked in a dark store within one to two kilometers of your home. The moment you place the order; someone picks it off the shelf. A rider is dispatched almost immediately and heads directly to your address.

There is no mid-mile movement, no routing logic and no batching. Each trip is a solo run. Delivery often happens within 10 to 15 minutes. This kind of speed relies on a dense network of local stores and a steady flow of short-range riders. But it also means higher costs.

“With no bundling of orders and lower average cart sizes, usually ₹250 to ₹300, the delivery cost per order can shoot up to ₹60 to ₹120. That is a heavy operational burden. Unlike traditional ecommerce, where cost efficiency scales with distance and order volume, quick commerce is constrained by geography and time pressure,” she explains.

So, it becomes more than just a category expansion for e-commerce platforms like Amazon and Flipkart. It marks a pivot in their “logistics thinking” and signals a broader shift in entry strategies. What once worked must now be retooled for hyperlocal and real-time operations.

Speed over Scale Not Easy

There are multiple challenges ahead for Amazon to make its presence felt and stay competitive in the quick commerce space. Firstly, it must build an operations and logistics layer that enables sub-15-minute deliveries, along with a technology stack to support it, according to Mit Desai, practice member at Praxis Global Alliance, a management consulting firm.

Second, it needs to build a dark store network to succeed in the space which is crucial to meet the 10-15 minutes delivery promise. Experts believe that a hybrid model will be the most successful in India—a mix of micro warehouses, partner stores and dark stores.

Desai states that Amazon’s existing capabilities can give it a base to build on, but it would also have to account for complexities and differences that come with the quick commerce business.

“For Amazon, the challenge will be operations. Can they build 700+ dark stores? Can they go hyperlocal? Can they navigate the chaos of Gurugram rain, Bengaluru traffic or the lanes of Dadar?” wonders Madhav Kasturia, founder and chief executive of Zippee, a quick commerce fulfilment start-up focused on hyperlocal deliveries and dark store management.

Another challenge can be repeat, loyal customers. As of now, customers check prices across platforms, and order where prices are the lowest. So, Amazon will have to spend heavily on discounts to gain market share. Chawla says retention will remain a problem because Zepto’s growth has also slowed down after a reduction in discounting burn.

However, Singh highlights that Amazon may not roll out everything in one shot. “We will likely see small-scale pilots, co-branded dark stores, local partnerships, new rider networks, tested in top cities before any nationwide push. They will also reveal whether it is viable to retrofit scale-driven e-commerce infrastructure into something that runs well in a hyperlocal loop,” she added.

Profitability Remains a Concern

While the quick commerce space is becoming increasingly dynamic with new entrants, the core question remains: is it a sustainable business model? The path to profitability is still fraught with operational complexity, margin constraints and uncertainty in consumer behaviour.

“Margins in quick commerce were never pretty to begin with,” says Kasturia. Yet he remains optimistic about the market because India’s grocery market is still largely untapped online.

As per data, India’s grocery and essentials market is over $600bn, of which online commerce is just three to four percent. Even quick commerce is sitting at ₹7,000–₹9,000 crore gross merchandise value today. So, the market isn’t crowded. It’s just early.

“We are barely scratching the surface,” he says, arguing that whoever wins customer behaviour, will lead the game. For example, in tier 1 cities, users no longer compare prices—they compare time.

For Amazon, this is both an opportunity and a constraint. Experts believe that the ecommerce giant can stand out by focusing on trust, hygiene and reliability—areas where existing players sometimes falter.

Kasturia says that the platform should not even chase everything, rather focus on profitable categories like fruits, dairy and personal care. “Build strong private labels. Nail density before geography and don’t discount blindly,” he adds.

The key is to build for reorders, not virality. That’s when customer acquisition cost (CAC) drops, margins compound and a player stops bleeding money per order. And to reduce the cost of dark stores, Chawla suggests an alternative route.

“Riding to neighbourhood stores for long-tail stock keeping unit can cut real estate and wastage costs,” he says, adding that it can decentralise inventory without owning all of it.

To follow this playbook, Devangshu Dutta, founder of Third Eyesight, a management consulting and services firm, says that every player needs to invest hundreds of crores before the model begins to show surplus cash. It will demand multiple, interlocked shifts—in pricing strategy, tech backbone, category mix, and even brand positioning.

Amazon’s entry doesn’t merely add another contender in the 10-minute delivery race—it rewrites the playbook for every player. The real question now is: can the frontrunners hold their turf, or will Amazon’s scale and deep pockets tip the balance of power?

admin

December 31, 2024

Jasodhara Banerjee, Forbes India

31 December 2024

Once, there was alabaster. Then, there was porcelain. And now there is glass. And no, we are not talking about the different kinds material to make fine, delicate objet d’art, but the quality and texture of facial skin—smooth, flawless and luminescent—that humans aspire to.

While a Google search for the term ‘glass skin’ will churn out hundreds of results that describe not just what the term means—tracing it to Korean skin care routines and products—but also detail the meticulous steps, varying between five and 11, that will apparently make you look like your favourite K-pop singer or K-drama actor. Like all things K (read: Korean), be it television and OTT serials, or food and clothes, K-beauty seems to have taken the Indian market by storm. A search for ‘Korean brands’ on online platforms such as Nykaa and Tira Beauty brings up more than a thousand products, ranging from ₹75 for a facial sheet mask to ₹17,900 for 60 ml of face cream. Clearly, there is something for everybody.

Fuelling this surge has been a plethora of factors, including the rise of online marketplaces that have made Indian and foreign skin care and beauty products more accessible than before, the thriving ecosystem of influencers and content creators that has revolutionised the marketing of these products, and, of course, consumer demand for products that claim to have the goodness of natural ingredients backed by the surety of science. And, surprising as it may seem, the Covid-19 pandemic and accompanying lockdowns also seem to have played a role in this.

Case in point is Amorepacific Corporation, a Seoul-headquartered beauty and cosmetics company that operates in more than 50 countries, and has a portfolio of more than 30 brands, such as Sulwhasoo, Laneige, Mamonde, Etude House and Innisfree. It is one of the largest cosmetics companies, not just in South Korea, but in the world.

“We are the number one beauty and personal care brand in South Korea and were the first Korean corporation to enter India with direct management, with our own subsidiary,” says Paul Lee, managing director and country head, Amorepacific India. “We started our business in India with Innisfree, which uses natural ingredients from Jeju Island in South Korea. We started with Innisfree because India had a huge demand for brands with natural products. Then we introduced Laneige and Sulwhasoo, which fall in the luxury skin care segment, and these were followed by Etude, which is a makeup brand.”

Amorepacific entered India sometime in 2012, taking tentative steps in a fledgling market with minimal investments and a retail store in Delhi’s Khan market. “At that time, the awareness of K-beauty was very small, and our momentum of growth started with the popularity of dedicated ecommerce players like Nykaa. In the last seven years, our annual growth has been 50 percent, our current growth is 60 percent year-on-year,” says Lee.

A potent potion for growth

Although industry players and experts feel there are multiple factors behind this growth, the popularity of Korean cultural elements is a significant one. “Korean beauty and personal care brands have multiple enabling factors. The global expansion of Korean beauty and personal care products has been on the back of a cultural export wave like any other earlier in history; in this case through the growing popularity of K-pop and K-dramas,” says Devangshu Dutta, founder, Third Eyesight and co-founder, PVC Partners. “In India, these brands initially had an influence in the Northeastern states, where customers are usually ahead on the fashion curve and also find resonance with the look of these brands.” He adds that factors such as the increasing number of Indian tourists to East Asian countries, and the growing presence of Korean and Japanese expatriates within India have also supported the growing footprint of these brands.

A spokesperson for Tira Beauty, which was launched in April 2023, agrees with Dutta, and attributes the demand for K-beauty products to the exposure that consumers have to K-dramas and K-pop. However, she adds that a significant factor is rooted in the products themselves. “These are the innovations that these brands are bringing to the table,” she explains. “The kind of formulations they offer are very well-suited for the Indian consumer. The ingredients are very efficacy oriented, and deliver a lot of quality, thus resolving a lot of concerns that consumers in India have.”

For instance, skin hydration is a core need of consumers, and a lot of Korean skin care products focus on hyaluronic acid as an ingredient. “Consumers who have sensitive skin or inflammation as a key concern get to use ingredients like centella asiatica, that a lot of Korean products use,” she says.

The spokesperson adds that the texture of the products is also a factor behind their popularity in India: “A lot of Korean sunscreens are light weight, a lot of their essences are suited for the Indian skin and the Indian weather. Both these factors are contributing to the rise we are witnessing in the space of K-beauty.”

Lee of Amorepacific highlights the use of unique ingredients such as fermented beans, ginseng and green tea that were never used before by American or European companies. There are also many options for consumers to choose from, depending on what is best suited for them. For instance, there is a product line with green tea for consumers with sensitive skin, and the same products are available for those with dry skin. “There are three key metrics that we have seen among Indian consumers: One is the demand for premium quality, two is the demand for glass skin, and the third is reliability.”

Lee also attributes market factors that have been instrumental in making Korean products more accessible to Indian consumers. “There has been a lot of change before Covid, and after Covid. From the macro perspective, the number of internet users with access to low-cost data plans has increased. During the Covid-19 pandemic, the number of new people watching OTT platforms such as Netflix also surged. From the Netflix perspective, I think India is one of the top three countries, where the number of subscribers is concerned.”

According to the Korea Trade-Investment Promotion Agency, the beauty market in India saw substantial growth following the Covid-19 pandemic and is projected to expand by 10 percent annually from 2022 to 2027, more than twice the global average growth rate for the beauty sector. According to market analyst Mordor Intelligence, the K-beauty market in India is expected to grow annually by 9.4 percent from 2021 to 2026.

Lee highlights the popularity of Korean OTT series such as Squid Games in making Indians familiar with Korean culture, and YouTube videos making a lot of people aware of K-beauty. “When we started operating in India, there were hardly two or three brands operating here, but currently there are more than 60 Korean brands in India. The influence of TV and music content has made people familiar with Korean culture, which is similar to Indian culture in being family-centric,” he adds.

Content creator Scherezade Shroff Talwar says, “The Hallyu [Korean] wave during the pandemic has definitely contributed to, what I would say, an over-consumption of Korean culture and I definitely contribute to it as well. K-beauty products have been around in India for a while, but with the increasing popularity of K-dramas and K-pop, people are seeing more such content across multiple platforms. This has contributed to the rising number of Korean brands in India, and the use of their products.” She recalls how, in November, she was in South Korea with her K-drama club, and the members had lists of the products that they wanted to buy there because they are not available in India.

According to a September report by market research firm Mintel, social media analysis in India reveals that there have been 6.2 million posts in the last two years discussing K-drama, K-pop, and K-beauty trends, predominantly among the 19 to 24 age group. This continued popularity in K-pop throughout the APAC region influences consumers’ interest in Korean skin care and beauty products, the report adds.

Lee says that Korean beauty companies have also been prompt to react to the demands in the market. For instance, Innisfree introduces new products every three months, and they are based on consumer feedback through social media and actual stores. Given the demand from Indian consumers, Amorepacific has also formed a task force at its headquarters which is dedicated to reviewing and studying the Indian market, with plans bring in more brands and businesses.

Data shows, adds Lee, that the import of Korean skin care products into India is increasing by 63 percent every year, going up four times compared to 2020. Amorepacific’s own research shows that 53 percent of Indian beauty consumers have already tried Korean products. “Fifteen percent of the entire skin care products market is now dominated by Korean products,” he claims.

Although Amorepacific decided to close all 23 of its exclusive stores in India because of the losses suffered during the pandemic, it decided to partner instead with local channels such as Nykaa, Tira Beauty and SS Beauty, and its products are today available across 400 counters in 45 cities. “Although our company is seeing 60 percent growth every year now, our retail area is doubling every year,” says Lee. “Our aim is to be available in 500 counters within a year.”

The availability and accessibility of Korean skin care and beauty products have also coincided with the rise of marketing products through influencers and content creators. The spokesperson for Tira Beauty says that influencers have played a massive role in the popularity of Korean products. “One of the reasons why K-beauty products do well across markets is because Gen-Z consumers tend to follow a lot of these influencers,” she explains. For instance, Tira launched the Beauty of Joseon sunscreen, and it went out of stock very quickly. “We experienced this because there was a lot of awareness due to influencer activations, and there’s a certain amount of virality these products enjoy even before they are launched.” She also gives the example of the brand Tirtir, which was launched on Tira Beauty in India in November. “The brand rolled out samples to influencers in India in July, and that helped propel demand to a great extent.”

According to business consulting firm Grand View Research, celebrity influencers have been beneficial to marketers due to their global reach, which often transcends cultural boundaries. Hence, the top strategy used by Korean cosmetics brands is to sell their products to Korean celebrities. Storytelling using Korean celebrities as brand ambassadors, and streaming advertisements and video tutorials all over the social media platform are some of the major strategies adopted by K-beauty brands.

Grand View Research gives the example of the lip layering bar of Laniege, which has emerged as a convenient tool for those who want to get the trendy gradient lip look with just a single application. Celebrities such as actors Song Hye Kyo and Lee Sung Kyung have used the product, enhancing its appeal and desirability among consumers.

Celebrities from different parts of the world promote K-beauty products, and this fosters a cross-cultural appeal and encourages individuals from diverse backgrounds to explore and adopt these products in their skin care routines. Following this global trend, in India, young celebrities have been roped in to appeal to Gen-Z consumers. For instance, actor Palak Tiwari became the first Indian brand ambassador for Etude, while actor Wamiqa Gabbi became first Indian brand ambassador for Innisfree, and Sara Tendulkar, daughter of cricketing legend Sachin Tendulkar, is the brand ambassador for Laneige.

Dutta of Third Eyesight says, “Influencers certainly have played a role in building the buzz around K-beauty and have formed a relatively cost-effective means to spread the message in the past. However, in recent years with a growing number of social influencers, there is more clutter as well on the channels.”

India not in the big league, but demanding

Although the rise of K-beauty products in India has been significant, the country remains a far smaller market for these brands compared to markets such as the US, Europe and China. According to Grand View Research, the global K-beauty products market size was valued at $91.99 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 9.3 percent from 2023 to 2030.

The consulting firm says the Korean cosmetics industry grew steadily during the Covid-19 pandemic, owing to an increase in awareness of the numerous benefits offered by the products. Moreover, due to a rise in popularity among consumers, major K-beauty companies are taking initiatives such as R&D, product launches, mergers and acquisitions to retain shares in the market and respond to changes in the marketplace by introducing a range of items.

Grand View Research valued the US market, one of the largest for K-beauty products, at $20.2 billion in 2021 and expects it to grow at a CAGR of 8.8 percent between 2023 and 2030. Compared to this, Statista valued the India K-beauty market at $486 million in 2021, and expects it to grow to over $1.3 billion by 2032.

Lee of Amorepacific says the US remains the largest beauty market as a whole, followed by China, Japan, the UK, France and India. “One of the differentiating factors between the US and Indian consumers is that the premium market in India is very small, and it is still a mass-product driven market,” he says. “Secondly, ecommerce in India is still quite small. In South Korea and the US, ecommerce just in the beauty segment, is 30 to 40 percent, while in India it is 13 percent. India is traditionally an offline market.”

He adds that despite the growth, Indians remain sceptical about whether Korean products are suitable for Indian skins, and there is demand for products that are made only for Indians. “Localisation, therefore, has become important for the company. Although we conduct clinical trials in different geographies, we are starting to take more feedback from Indian consumers, and we are ready to develop products only for the Indian market. For instance, we have introduced the Innisfree kajal and the Innisfree hair massage oil, and have developed lip colours for the Indian market.”

Although the company did not divulge revenue figures, it is expecting to grow six times in the next six years in India, and plans to introduce at least five more brands within the next seven years in this market.

(Published in Forbes India)

admin

September 16, 2024

Sesa Sen, NDTV Profit

16 September 2024

As India’s economy grows and digital technologies reshape consumer behavior, the future of kirana stores—the quintessential neighbourhood grocery shops—hangs precariously in the balance.

These soap-to-staple sellers, once impervious to change, now confront an existential threat from quick commerce players like Blinkit, Instamart, Zepto, and from modern retailers such as DMart and Star Bazaar, raising a pivotal question: Can kiranas survive the pressure of change, or will they die a slow death?

The All India Consumer Products Distributors Federation, that represents four lakh packaged goods distributors and stockists, has recently raised alarms, urging Union Minister for Commerce and Industry Piyush Goyal to investigate the unchecked proliferation of quick commerce platforms and its potential ramifications for small traders.

Their concerns are not unfounded. Data suggests that the share of modern retail, including online commerce, which is currently below 10%, is set to cross 30% over the next 3-5 years. Much of this growth will come at the cost of traditional retail.

“Unless the government takes on an activist role to support the smallest of business owners, the shift toward large corporate formats is inevitable,” according to Devangshu Dutta, head of retail consultancy Third Eyesight.

Casualties Of The Boom

Madan Sachdev, a second-generation grocer operating Vandana Stores in eastern Delhi, has thrived in the recent years, adapting to the digital age by taking orders via WhatsApp and employing extra hands for home delivery.

Despite having weathered the storm of competition from giants like Amazon and BigBazaar, he now finds himself disheartened, as his monthly sales have halved to about Rs 30,000, all thanks to quick commerce.

Sachdev is worried about meeting expenses such as rent, his children’s education, and other household bills. He finds himself at a crossroads, uncertain about how to modernise his store or adopt new-age strategies in order to attract customers in an increasingly competitive market.

India’s $600 billion grocery market, a cornerstone for quick commerce, is largely dominated by more than 13 million local mom-and-pop stores.

Retailers like Sachdev are also seeing a steep decline in their profit margins from FMCG companies, which now hover around 10-12%, down from the 18-20% margins seen before the Covid-19 pandemic. The consumer goods companies are instead offering higher margins to quick commerce platforms so that they can afford the price tags.

Quick deliveries account for $5 billion, or 45%, of the country’s $11 billion online grocery market, according to Goldman Sachs. It is projected to capture 70% of the online grocery market, forecasted to grow to $60 billion by 2030, as consumers increasingly prioritise convenience and speed.

Many of the mom-and-pop shops are family-run and have been in business for generations. Yet they lack the resources to modernise and compete effectively with larger chains. Modern retail businesses, including quick commerce, begin with significantly more capital, thanks to funding from corporate investors, venture capital, private equity, and public markets.

“They can scale quickly and capture market share due to a superior product-service mix, larger infrastructure, and more robust business processes,” said Dutta.

Moreover, their ability to engage in price competition poses a challenge for small retailers and distributors, making it difficult for them to compete.

“This is something that has happened worldwide, in the largest markets, and I don’t think India will be an exception,” Dutta said, adding that it would be incomplete to single out a specific format of corporate business such as quick commerce as the sole villain in this situation.

“India is a tough, friction-laden environment at any given point in time, including government processes which don’t make it any easier,” he said.

Peer Pressure

Data from research firm Kantar shows that general trade, which comprises kirana and paan-beedi shops, have grown 4.2% on a 12-month basis in June, while quick commerce grew 29% during the same period.

Shoppers are becoming more omnichannel, rather than gravitating towards one particular channel, said Manoj Menon, director- commercial, Kantar Worldpanel, South Asia. “While the growth [for quick commerce and e-commerce] might appear to have declined compared to a year ago, a point to note is that the base for these channels has significantly grown. Therefore, achieving this level of growth is still commendable.”

Consumer goods companies such as Hindustan Unilever Ltd., Dabur India Ltd., Tata Consumer Products Ltd., etc., have acknowledged the salience of quick commerce to their packaged food, personal and homecare products. The platform currently comprises roughly 40% of their digital sales.

“We are working all the major players in the quick commerce space and devising product mix and portfolio. This is a very high growth channel for us,” according to Mohit Malhotra, chief executive officer, Dabur India.

Elara Capital analysts have pointed out that the share of quick commerce is expected to rise to60% in the near future with e-commerce and modern trade turning costlier for FMCG brands than quick commerce. “The larger brands tend to make better margins on quick-commerce platforms versus e-commerce due to lower discounts on the former,” it said in a report.

However, it is too premature to draw a parallel between kirana and quick commerce in terms of competition, given the significant size difference.

The average spend per consumer on FMCG in kirana stores stands at Rs. 21,285 annually while the same is Rs. 4,886 for quick commerce, according to Menon.

Rural Vs Urban Divide

Quick commerce is still an urban phenomenon. In contrast, in rural settings, where internet penetration is still catching up and access to large retail chains is limited, kirana stores continue to thrive.

According to Naveen Malpani, partner, Grant Thornton Bharat, while the growth of quick commerce is undeniable, this channel is not poised to replace traditional retail, which still has a wider reach in the country. “It will complement older models, filling a niche for immediate, smaller purchases. Also, a 10-20-minute delivery may not have a strong market pull in rural markets where distance and time are not much of a concern.”

Yet many others believe, even in these areas, the challenge is palpable.

The small businesses are beginning to feel the sting of same slow decline that once befell the ubiquitous telephone booths in the era of mobile phone, according to Sameer Gandotra, chief executive officer of Frendy, a start-up that is building ‘mini DMart’ in small towns where giants like Reliance and Tatas have yet to establish their presence.

As rural customers slowly start to embrace digital shopping and seek more variety, kirana stores must adapt or risk becoming obsolete, he said.

Besides, the popularity of quick commerce is set to challenge the dominance of incumbent e-commerce platforms, especially in categories such as beauty and personal care, packaged foods and apparel.

“Quick commerce is primarily operational in metros and tier 1 markets, which is impacting the sales of traditional companies in these areas. However, if quick-commerce players were to extend their operations to tier 2 and tier 3, it would even challenge companies such as DMart and Nykaa, and would pare sales and profitability,” noted analysts at Elara Securities.

Frendy’s Gandotra believes the journey for kirana stores is not a lost cause, but it requires strategic interventions. Many kirana store owners struggle to integrate point-of-sale systems, inventory management software, or even digital payment solutions. These stores need to embrace technology.

Another aspect is the need for policy support. Regulations to ensure fair competition can prevent monopolisation by large retailers. Additionally, subsidies, tax benefits, and grants for infrastructure improvements can help small businesses adapt to changing market dynamics. With renewed support, kirana stores can continue to be the backbone of Indian retail.

Nonetheless, there will be some who’ll be left behind during this shift. Analysts at Elara Capital warn that the swift rise of quick-commerce platforms, combined with aggressive discounting, could wipe off 25-30% of traditional grocery stores.

(Published on NDTV Profit)

admin

August 31, 2024

MG Arun, India Today

Aug 31, 2024

Nearly five years after the Centre brought in norms to rein in multinational e-commerce companies operating in India, Union commerce minister Piyush Goyal sparked fresh controversy by raising concerns over the rapid expansion of e-commerce. He also drew attention to the pricing strategies used by some e-commerce firms, questioning what he termed “predatory pricing”.

“Are we going to cause huge, social disruption with this massive growth of e-commerce? I don’t see it as a matter of pride that half our market may become part of the e-commerce network 10 years from now; it is a matter of concern,” Goyal said at an event in New Delhi last week.

His comments come at a time when the ecommerce business in India is growing exponentially. Estimated at $83 billion (around Rs 7 lakh crore) as of FY22, the market is expected to grow to $150 billion (Rs 12.6 lakh crore) by FY26. The growth will be due to multiple levers: a growing middle class, rising internet penetration, the proliferation of smartphones, convenience of online shopping and increasing digitisation of payments. The overall Indian retail market was pegged at $820 billion (Rs 69 lakh crore) in 2023, according to a report published by the Boston Consulting Group and the Retailers Association of India. E-commerce still comprises only about 7 per cent of that, as per Invest India.

The Indian e-commerce market is dominated by global giants, including Amazon and Walmart (which took over Flipkart in 2018). They, along with domestic players, offer huge discounted prices compared to retail prices, which drives online sales significantly. In FY23, Amazon Seller Services and Flipkart posted Rs 4,854 crore and Rs 4,891 crore losses, respectively. Goyal’s argument is that these losses are due to their predatory pricing.

“Is predatory pricing policy good for the country?” Goyal asked, while stressing the need for a balanced evaluation of e-commerce’s effects, particularly on traditional retailers such as restaurants, pharmacies and local stores. “I’m not wishing away ecommerce—it’s there to stay,” he said. Later, he said e-commerce uses technology that aids convenience. But there are 100 million small retailers whose livelihood depends on their businesses.

The Centre has specific laws that permit foreign direct investment (FDI) in e-commerce exclusively for business-to-business (B2B) transactions. However, according to Goyal, these laws have not been followed entirely in letter and spirit. Currently, India does not allow FDI in the inventory-based model of e-commerce, where e-commerce entities own and directly sell goods and services to consumers (B2C). FDI is permitted only in firms operating through a marketplace model, where an e-commerce entity provides a platform on a digital or electronic network to facilitate transactions between buyers and sellers (B2B).

The country’s laws also stipulate that in marketplace models, e-commerce entities cannot ‘directly or indirectly influence the sale price of goods or services’ and must maintain a ‘level playing field’. Entities in the marketplace model re allowed to transact with sellers registered on their platform on a B2B basis. However, each seller or its group company is not permitted to sell more than 25 per cent of the total sales of the marketplace model entity.

Goyal said certain structures have been created to suit large e-commerce players with “deep pockets”. Algorithms have been used to drive consumer choice and preference. For instance, several pharmacies have disappeared, he said, and a few large chains are dominating the retail space. He invoked the importance of platforms like the Open Network for Digital Commerce where small businesses can sell their products.

E-commerce firms counter the argument on predatory pricing. “It is the sellers’ discretion as to what price they should sell at,” says an industry source. The e-commerce player who provides the platform seldom has a role in it, he explains. “Sellers could be doing clearance sales or liquidation of old products at cheaper prices. Some sellers also source products at manufacturing cost and park it with e-commerce firms instead of involving warehousing agents. This helps cut their overhead costs and allows them to offer lower prices on the platform,” he adds.

Some experts are of the view that the government should not step in with controls and allow the market forces to play their role in determining prices. Price controls may lead to shortages, inferior product quality and the rise of illegal markets. Moreover, the Competition Commission of India (CCI), which is mandated to act against monopolies, may be given more teeth. It is ironical that, on the one hand, the Centre wants more FDI to flow in, but places more and more controls on foreign players on the other hand. At the core are the interests of small traders and retailers, a key section of the electorate.

Others argue that the government has a role to ensure that there is fair competition. “It is not just small retailers the government would be speaking for, but for large domestic players too,” says Devangshu Dutta, founder of consultancy firm Third Eyesight, emphasising that the government’s role should be to establish laws and practices that promote fairness.

According to him, it is no secret that e-commerce has grown through discounts. “For large e-commerce firms, market acquisition happens by acquiring a share of the consumer’s mind and through pricing. When a large sum is spent on advertisements, it is for acquiring the mind share of the consumer,” he says. “Pricing matters in a big way too. Whether you call it predatory pricing or market acquisition pricing depends on which side of the fence you are.”

(This article was originally published in the India Today edition dated September 9, 2024)