admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

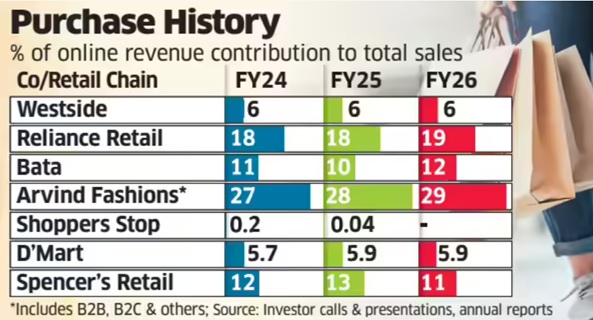

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

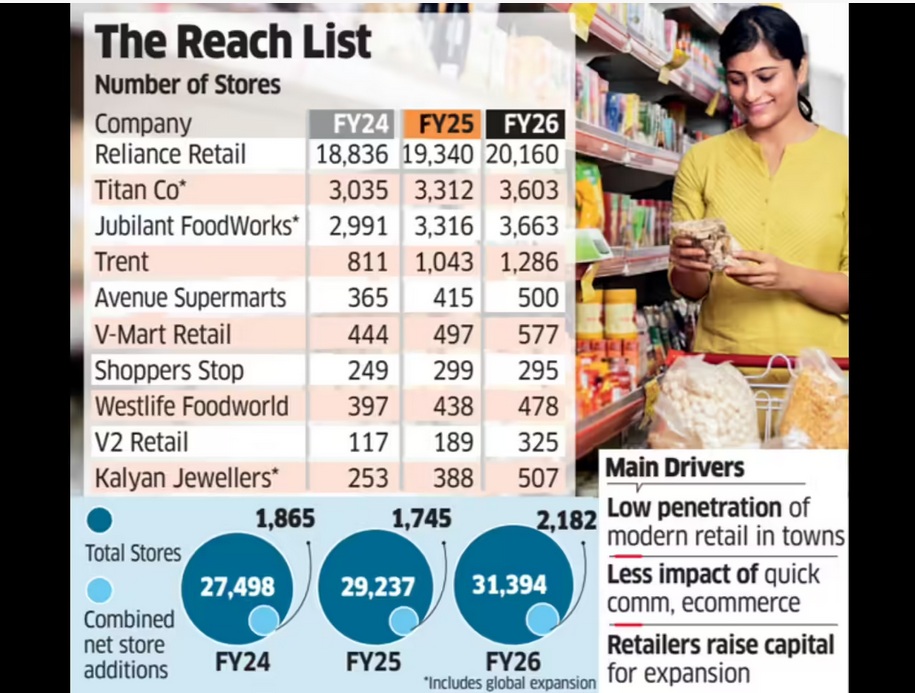

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

August 21, 2025

Praveen Paramasivam, Reuters

August 21, 2025

Summary

India's luxury beauty market to quintuple by 2035

Domestic brands account for less than a tenth of sales

Global brands modify offerings for IndiaIndia’s luxury beauty market is expected to quintuple to $4 billion by 2035 from $800 million in 2023, driven by its young, affluent, social-media savvy shoppers with rising disposable incomes, consulting firm Kearney and luxury beauty distributor LUXASIA said in a report.

Luxury beauty makes up just 4% of the $21-billion beauty and personal care market, compared with 8% to 24% across top Southeast Asian countries and 25% to 48% in developed markets including China and the United States.

That means there is plenty of room for growth.

“India is the last bastion of growth for premium beauty,” said Sameer Jindal, managing director for investment bank Houlihan Lokey’s corporate finance business in India.

“The Indian consumer is willing to experiment and try out new things.”

U.S. beauty giant Estee Lauder home to the brands Clinique and MAC, expects a strong runway for expansion and long-term growth in India, even as it grapples with soft sales in the Americas and Asia-Pacific.

“India today, within the Estee Lauder network, is looked at as one of the priority emerging markets,” said country general manager Rohan Vaziralli, highlighting plans to initially target 60 million women in the nation of more than 1.4 billion.

Homemaker R. Priyanka, based in the southern city of Chennai, said she was thrilled to have better access to Estee Lauder’s Jo Malone London fragrance in India, as a benefit of the companies’ efforts.

“It is easier than asking someone (abroad) to get it for you every time,” she added.

While global beauty brands might have to modify some of their products for India, which bakes in sultry temperatures in summer and oppressive humidity at other times, they face little competition from homegrown brands.

Kearney and LUXASIA identified only Forest Essentials and Kama Ayurveda as their major rivals, underscoring how domestic brands make up less than a tenth of luxury beauty sales.

In the more established markets of China, Japan and South Korea by comparison, domestic brands account for a 40% share.

“There is, of course, a premium perception gap between globally established brands and Indian brands,” said Devangshu Dutta, founder of retail consultancy Third Eyesight.

Global beauty giants’ huge marketing budgets also give them an edge over domestic brands, other industry watchers said.

WOOING INDIAN SHOPPERS

Estee Lauder is studying online sales patterns to identify the smaller cities to target, such as Siliguri in West Bengal state, partnering with designers such as Sabyasachi Mukherjee, and launching products such as kohl, an eyeliner Indians favour.

It has also invested in Forest Essentials, a brand with herbal ingredients, and in a programme offering funding to domestic beauty start-ups.

This year France’s L’Oreal said it was investing more in India and tapping into the “elevated beauty desires” of the nation’s young, digitally savvy, empowered women shoppers to drive growth. It declined further comment.

South Korea’s Amorepacific, known for brands such as Innisfree and Etude, is trying to leverage the Korean beauty craze in India with products geared to the market.

These include items for the popular “cleanser, serum, moisturiser, and sunscreen” beauty regimen, the country head, Paul Lee, said.

Japan’s Shiseido, with a history of more than 150 years, brought its NARS brand to Indian beauty retailer Nykaa’s website this year, and plans to step up growth of its brands in the subcontinent.

Global brands are very excited about India, where consumers are splurging more to stay on top of trends such as “cherry makeup”, Nykaa co-founder Adwaita Nayar said, referring to a look featuring flushed cheeks, glossy lips, and soft pink eyes.

Amazon, which has also been seeing a big boom in beauty demand in India, aims to identify emerging global trends and bring in more brands, said Siddharth Bhagat, director of beauty and fashion at the e-commerce company in India.

Retailer Shoppers Stop, which also pioneers foreign labels, plans to open 15 to 20 beauty stores in each of the next three years to boost its revenue from the segment to a quarter from less than a fifth now, its beauty business CEO Biju Kassim said.

Reporting by Praveen Paramasivam in Chennai; Editing by Dhanya Skariachan and Clarence Fernandez

(Published on Reuters)

admin

March 20, 2025

Sagar Malviya, Economic Times

Mumbai, 20 March 2025

Established beauty product makers such as Forest Essentials, Colorbar, Kama Ayurveda, Body Shop, VLCC Personal Care and Lotus Herbals saw a slowdown in sales growth in FY24, according to the latest Registrar of Companies filings. Consumers favoured new-age rivals such as Minimalist and Pilgrim, specialised derma brands, as well as global labels Shiseido, Innisfree and Eucerin.

Sales growth of established brands mostly in the natural skincare segment, more than halved to single digits during the previous financial year amid a broader economic slump.

In contrast, companies such as L’Oreal, Nykaa and Sephora continued to grow at 12-34% on a significantly bigger base, even as they lost pace.

Direct-to-consumer brand Pilgrim more than doubled its sales, Minimalist’s revenue increased 80% and Foxtale’s sales surged 500% on a lower base.

“With most consumers tightening their budget on discretionary spends in FY24, they seem to have opted for brands that give instant benefits compared to natural products, which take time to be effective,” said Devangshu Dutta, founder of retail consulting firm Third Eyesight.

Over the past few years, there has been a flurry of beauty product launches, which have depended on platforms such as Nykaa and Tira for sales.

In the past two years, Nykaa has launched more than 350 brands, or In the past two years, or nearly one new label every alternate day on average.

This includes international brands such as CeraVe, Uriage and Versed, as well as home-grown brands such as Foxtale and Hyphen.

Reliance Retail, which entered beauty retailing with Tira two years ago, now sells nearly 1,000 brands, including exclusive labels such as Akind, Augustinus Badee, Allies of Skin, Kundal and Patchology.

“10 years ago we were only competing against big guys,” Vincent Karney, global chief executive of Beiersdorf, maker of Eucerin, Nivea and La Prakrit, told ET last month. “Now we have those local brands, and we have to become a bit more agile.”

On Nykaa, Fenty Beauty by Rihanna is the highest-selling brand in lipcare while Eucerin has become its biggest premium dermo-cosmetic serum. South Korean beauty brands Axis-Y, Tirtir and Numbuzin grew over 60% in 2024, with sales of toners increasing 104%, serums 45%, moisturisers 52% and sunscreens 154% on the platform.

VLCC and Colorbar did not respond to ET queries, while Forest Essentials was not reachable.

In January, Mike Jatania, cofounder and executive chairman of The Body Shop and Aurea Group, told ET, “There would be continuation of new entrants. Inflation is still a global issue and we will see the pressure. Competitive environment will be a challenge… 70% of our stores are showing decent growth. We have closed some stores and opened a few also, that’s the nature of the business.”

Ingredients Matter

Warnery of Beiersdorf emphasised the need to stay focused on “big innovation, by being able to talk to GenZ, (a position) which might be filled in by those local brands coming with basic ingredients.”

The likes of Minimalist, Ordinary and Pilgrim disclose active ingredients at a granular level, specifying the exact percentage of acid used in the product to appeal to GenZ users (those born between 1997 and early 2010s), who are said to be far more conscious of what they use on their skin compared to millennials (those born during 1980s to mid-1990s) and Gen X (those born from about 1965 to 1980).

Shoppers Stop, which manages brands such as Estee Lauder, Shiseido, Bobbi Brown, Mac and Clinique in India, sees the overall beauty market driven by companies focusing on consumers across age groups, and not just younger ones. Both natural and dermatological products are expected to find takers.

“While most new age brands tap younger cohorts, their pocket size allows them to mostly buy affordable products and the more affluent consumers opt for established global brands that have proven themselves since decades,” said Biju Kassim, chief executive, beauty, at Shoppers Stop. “Beauty is still not a habit in India and with hundreds of brands being launched, the focus is to grow penetration. There is also a shift from care to cure, driven by derma-recommended products and brands disclosing active ingredients, but it is still a niche sub-segment.”

Dutta of Third Eyesight sees the current trend as temporary. “We expect growth of (established) companies to bounce back in the current fiscal, driven by a strong demand for beauty,” he said, pointing especially to online platforms. India’s beauty and personal care market is expected to reach $34 billion by 2028, up from $21 billion now, driven by an online surge and a growing preference for high quality, premium beauty products according to a report by Nykaa and consulting firm Redseer.

Nicolas Hieronimus, chief executive of cosmetics giant L’Oreal, last year said consumers in India are more demanding and are not just settling for very basic things like putting an ingredient in a product such as salicylic acid or collagen. “That’s where L’Oreal has the best cards to play, and that’s where we really thrive,” he had told ET.

Beiersdorf, Unilever, L’Oreal and Shiseido, among the world’s largest cosmetics companies, have all identified India as a key growth driver, citing the burgeoning population and growing affinity for beauty products.

(Published in Economic Times)

admin

July 28, 2024

Writankar Mukherjee, Economic Times

Kolkata, 28 July 2024

Top retail chains such as Reliance Retail, Shoppers Stop and Spencer’s Retail are facing a prolonged slowdown in consumption, pushing them to exit unprofitable markets, raise debt and control costs.

India’s largest retailer Reliance Retail shuttered 249 stores in the three months ended June. The company is also going slow on expansion, opening 331 new stores in the quarter compared to 470-800 stores opened every quarter in FY22, FY23 and FY24. The closures mean the retail business of Reliance Industries made 82 net new store additions last quarter–the lowest in 15 quarters.

Spencer’s Retail has decided to completely exit North and South India markets by closing 49 stores in the National Capital Region (NCR), Andhra Pradesh and Telangana. The step will erase Rs 490 crore of annual revenue, but the company is hopeful it will improve profitability.

Shoppers Stop chief executive officer Kavindra Mishra told investors last week that it may have to defer a few store openings this fiscal due to regulatory and other issues. The company will also borrow Rs 100 crore for expansion with demand remaining soft.

Meanwhile, V-Mart Retail has closed 22 stores in the first six months of 2024, as per its latest investor presentation.

“Pruning underperforming locations is a natural reaction during times of demand stress,” said Devangshu Dutta, CEO of retail sector consulting firm Third Eyesight.

Pure Economics

“Demand forecasting can never be perfect due to a lag between demand assessment and supply. Retailers now try to do away with underperforming stores at the bottom of the pile quickly. Earlier there were prestige issues in shutting down stores, but now it’s acceptable industry practice and pure economics,” said Third Eyesight’s Dutta.

Analysts say most retailers expanded rapidly after the pandemic, banking on pent-up demand and revenge shopping at the time. With demand turning sluggish, the industry is now being forced to take various steps to sustain operations. At Reliance Retail, net profit rose by a modest 4.6% from a year earlier in the June quarter to Rs 2,549 crore while revenue grew 6.6% to Rs 66,260 crore. It was the slowest pace of revenue growth and came after a 9.8% increase in Q4FY24. Net profit and revenue from operations fell sequentially in the June quarter.

Spencer’s Retail CEO Anuj Singh told analysts on Thursday the 49 stores it is closing make up nearly 22% of revenue, but also Rs 56 crore of losses at the regional Ebitda level in North and South India. “They were a drag on the balance sheet. We will now focus on Uttar Pradesh and the East where there is a sizable consumption opportunity with a 250 million population,” he added.

Singh said the store rationalisation exercise and about 35% headcount reduction at corporate offices will reduce overheads from 8% operating cost to 6.3% of total sales. “We now expect to achieve Ebitda breakeven by March 2025 which will give us the option to raise capital,” he said.

Mishra at Shoppers Stop said demand remained subdued last quarter due to fewer wedding dates, long election season with polling dates on weekend, heatwaves, and high level of cumulative inflation. All these factors combined hit growth and volume recovery, except in value fashion and beauty.

More stores shut than opened

In fact, the sustained demand slowdown saw chains like Pantaloons, Spencer’s Retail and Nature’s Basket close more stores than they opened last fiscal. Retailers like V-Mart Retail, W, Aurelia and Titan Eye+ had a higher rate of store closures than openings in the March quarter.

(Published in Economic Times)