admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

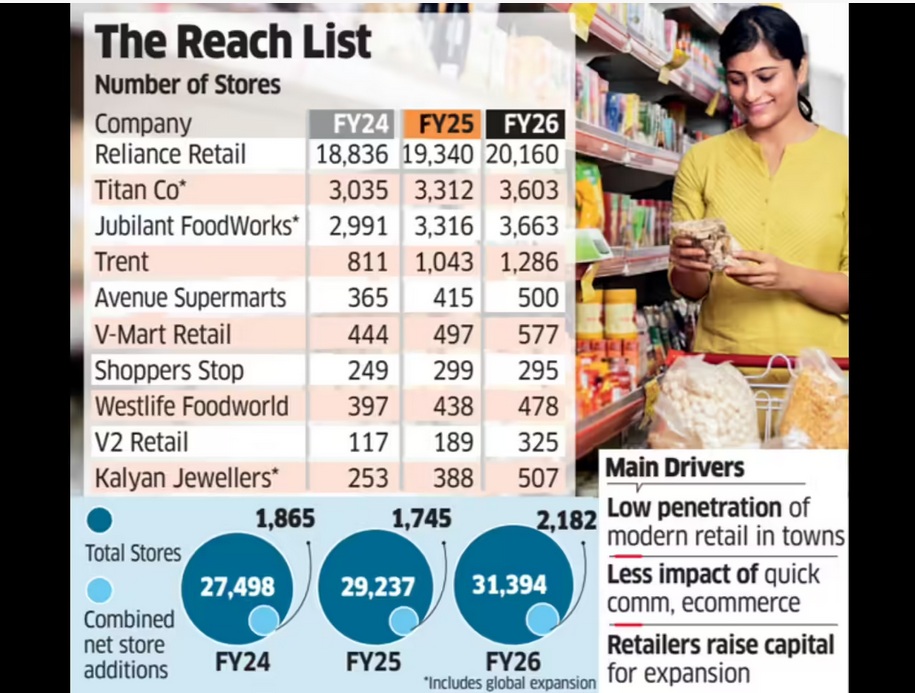

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

July 28, 2024

Writankar Mukherjee, Economic Times

Kolkata, 28 July 2024

Top retail chains such as Reliance Retail, Shoppers Stop and Spencer’s Retail are facing a prolonged slowdown in consumption, pushing them to exit unprofitable markets, raise debt and control costs.

India’s largest retailer Reliance Retail shuttered 249 stores in the three months ended June. The company is also going slow on expansion, opening 331 new stores in the quarter compared to 470-800 stores opened every quarter in FY22, FY23 and FY24. The closures mean the retail business of Reliance Industries made 82 net new store additions last quarter–the lowest in 15 quarters.

Spencer’s Retail has decided to completely exit North and South India markets by closing 49 stores in the National Capital Region (NCR), Andhra Pradesh and Telangana. The step will erase Rs 490 crore of annual revenue, but the company is hopeful it will improve profitability.

Shoppers Stop chief executive officer Kavindra Mishra told investors last week that it may have to defer a few store openings this fiscal due to regulatory and other issues. The company will also borrow Rs 100 crore for expansion with demand remaining soft.

Meanwhile, V-Mart Retail has closed 22 stores in the first six months of 2024, as per its latest investor presentation.

“Pruning underperforming locations is a natural reaction during times of demand stress,” said Devangshu Dutta, CEO of retail sector consulting firm Third Eyesight.

Pure Economics

“Demand forecasting can never be perfect due to a lag between demand assessment and supply. Retailers now try to do away with underperforming stores at the bottom of the pile quickly. Earlier there were prestige issues in shutting down stores, but now it’s acceptable industry practice and pure economics,” said Third Eyesight’s Dutta.

Analysts say most retailers expanded rapidly after the pandemic, banking on pent-up demand and revenge shopping at the time. With demand turning sluggish, the industry is now being forced to take various steps to sustain operations. At Reliance Retail, net profit rose by a modest 4.6% from a year earlier in the June quarter to Rs 2,549 crore while revenue grew 6.6% to Rs 66,260 crore. It was the slowest pace of revenue growth and came after a 9.8% increase in Q4FY24. Net profit and revenue from operations fell sequentially in the June quarter.

Spencer’s Retail CEO Anuj Singh told analysts on Thursday the 49 stores it is closing make up nearly 22% of revenue, but also Rs 56 crore of losses at the regional Ebitda level in North and South India. “They were a drag on the balance sheet. We will now focus on Uttar Pradesh and the East where there is a sizable consumption opportunity with a 250 million population,” he added.

Singh said the store rationalisation exercise and about 35% headcount reduction at corporate offices will reduce overheads from 8% operating cost to 6.3% of total sales. “We now expect to achieve Ebitda breakeven by March 2025 which will give us the option to raise capital,” he said.

Mishra at Shoppers Stop said demand remained subdued last quarter due to fewer wedding dates, long election season with polling dates on weekend, heatwaves, and high level of cumulative inflation. All these factors combined hit growth and volume recovery, except in value fashion and beauty.

More stores shut than opened

In fact, the sustained demand slowdown saw chains like Pantaloons, Spencer’s Retail and Nature’s Basket close more stores than they opened last fiscal. Retailers like V-Mart Retail, W, Aurelia and Titan Eye+ had a higher rate of store closures than openings in the March quarter.

(Published in Economic Times)

admin

February 23, 2024

Kailash Babar & Sagar Malviya, Economic Times

Mumbai, 23 February 2024

Tata Group and Reliance Industries, two of India’s largest conglomerates, are vying for premium retail real estate in Mumbai as they extend their footprints, creating rivalry in a city starved of marquee properties. From Zara and Starbucks to Westside and Titan, the Tata Group occupies nearly 25 million square feet of retail space in India. That is still no match for Reliance Industries that control three times more at 73 million sq ft for more than 100 local and global brands.

But in Mumbai, they are evenly matched, having nearly 3 million sq ft of retail space each. That is a quarter of what is considered the most prime retail real estate in the country, and both the retail giants are looking for more.

“In a modern retail environment, most visible locations contain more successful or larger brands. It just so happens that many of those brands are owned by either Reliance or the Tatas,” said Devangshu Dutta, founder of Third Eyesight, a strategy consulting firm.

“Tatas have been in retail for longer but also slower to scale up compared to Reliance which had this stated ambition of being the most dominant and put the money behind it,” he said.

In a market where demand is much higher than supply, developers and landlords seek to separate the wheat from the chaff, experts said. Ultimately, success in Mumbai’s retail real estate scene hinges on a delicate equilibrium between accommodating industry leaders and fostering a vibrant, varied shopping environment, they said. “In the competitive landscape of retail real estate in Mumbai, commercial developers and mall owners often face the strategic challenge of accommodating prominent retail brands,” said Abhishek Sharma, director, retail, at commercial real estate consultants Knight Frank India.

“These big brands, with a significant market share of 40-45% in the Indian retail sector, can easily be termed as industry giants and possess the potential to command 45-50% of space in any mall,” he said. According to Sharma, there may be perceptions of preferential treatments, but the dynamics are complex, and developers must balance the demand from these major brands with the need for a diverse tenant mix.

Tata Group entered retail in the late 1980s, initially by opening Titan watch stores and a decade later by launching department store Westside. So far, it has about 4,600 stores, including brands such as Tanishq, Starbucks, Westside, Zudio, Zara and Croma.

While Reliance Retail started in 2006, it overcompensated for its late entry by aggressively opening stores across formats. Reliance has over 18,774 stores across supermarkets, electronics, jewellery, and apparel space. It has also either partnered or acquired over 80 global brands, from Gap and Superdry to Balenciaga and Jimmy Choo. A diverse portfolio of brands across various segments through strategic partnerships and collaborations helps an entity like Reliance to leverage synergies and enhance retail presence, especially in malls, experts said.

“The array of brands with Reliance bouquet allows it to enter early into the project and set the tone and positioning of the mall,” said a retail leasing expert who requested not to be identified.

“This positively helps the mall to set its own positioning and future tenant mix. It also helps Reliance place their brands in most relevant zones within the mall. This will emerge as a clear differentiator in a city like Mumbai where brands are already jostling for space, which is the costliest in the country,” the person added.

(Published in Economic Times)

admin

August 23, 2023

New Delhi, 23 August 2023

Bindu D. Menon, Financial Express

Tata Group’s Titan Company is not the only one to be bullish on the fine jewellery segment by recently raising its stake in CaratLane from 71.09% to 98.28% for a consideration of Rs 4,621 crore. Other corporate groups as well as private equity firms who have entered this segment are making investments and scaling up.

For instance, recently, Aditya Birla Group entered the gold jewellery market with the launch of Novel Jewels with an estimated investment of Rs 5,000 crore. It also plans to launch large-format jewellery formats and in-house brands.

“The younger generation’s changing style preferences and shopping habits have favoured the growth of jewellery chains and a shift in jewellery designs to lighter, more contemporary styles. This has also facilitated the delinking of the cost and the product price to some extent,” said Devangshu Dutta, Founder, Third Eyesight.

Analysts following the sector said that lighter weight jewellery have been a game changer for the industry. Moving away from the traditional 22 carats jewellery line, younger consumers are opting for 12, 14 and 18 carat jewellery in minimalist designs; a trend largely mimicked from the western markets.

From the companies’ perspective gross margins are invariably higher in design enhanced jewellery as compared to traditional designs.

Leading silver jewellery brand Giva jewellery too had recently bagged a Rs 200 crore funding led by Premji Invest to expand its product line. The round also saw participation from existing investors such as Aditya Birla Ventures, Alteria Capital and A91 Partners. Giva reportedly launches 250 new designs every month, as per the company’s disclosure.

“We look forward to leveraging Premji Invest’s playbook on omnichannel across several consumer brands and retail businesses to strengthen our leadership position and establish our pan India presence,” said Ishendra Agarwal, founder and CEO, Giva.

Giva plans to use the capital for inventory management and expanding its offline presence in India. The company has secured Rs 130 crore funding till date, excluding the current funding.

Fine jewellery in India are priced between Rs 5,000 to Rs 50,000. Major players in the segment include Caratlane, Tanishq, Bluestone among others.

(Published in Financial Express)