admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

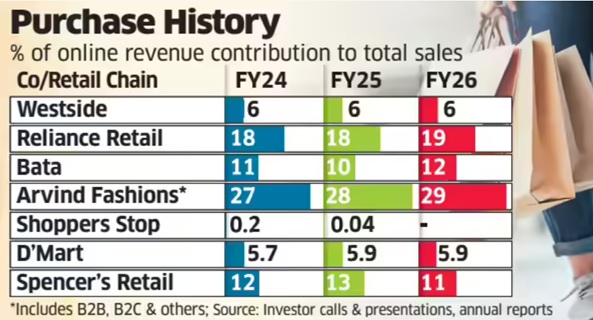

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 25, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 25 May 2026

Value fashion retailers across the country are likely to face margin pressure in the upcoming quarters as rising crude oil prices are driving up the cost of polyester and other fabrics. Executives at V-Mart Retail Ltd, Vishal Mega Mart Ltd, and Kewal Kiran Clothing Ltd (KKCL) said crude oil-linked inflation has begun to push up yarn and sourcing costs across apparel and general merchandise categories, with the full impact expected to play out over the next few months.

Value fashion retailers face a double whammy: their heavy reliance on polyester and synthetic blends exposes them to crude-linked inflation, while their price-sensitive customer base leaves little room to pass on rising costs without hurting demand.

Apparel contributes about 22.8% of the overall revenue of the country’s largest retailer, DMart, in FY26. Rising polyester and fabric prices could also weigh on this share, which has been declining since FY20.

“We see almost 60% to 70% consumption of polyester yarn or poly-based product lines, which have or will get impacted,” said Lalit Agarwal during the company’s March-quarter earnings call. Agarwal said that yarn prices had already risen sharply in recent weeks. “There is a rise of almost 10% to 15% in the yarn prices, which effectively converts to almost 5% to 7% in the apparel prices,” he said.

“Cost increases are at multiple points. One, of course, is raw material, which is not only fabric, but also polyester buttons, thread, packaging, all of that,” Devangshu Dutta, founder of Third Eyesight, a consulting firm, said. “Because with value, you cannot really pass on the price hikes so readily to the consumer.”

Dutta said that lower- and middle-income consumers were already under financial stress from broader inflationary pressures, “so, they will not be able to absorb price hikes as easily as well.”

Ebitda margins in Q4FY26 are 10.9% for V-Mart Retail, 13.6% for Vishal Mega Mart and 19.1% for Kewal Kiran Clothing.

Double whammy for value segment

Gunender Kapur, CEO of Vishal Mega Mart, during the company’s March-quarter earnings call, said the inflationary impact had started becoming visible towards the end of April and would likely intensify in the coming months.

Despite rising input costs, retailers said they are avoiding broad-based price hikes on entry-level products amid fragile demand conditions in the value segment.

Entry-level products for these retailers range from ₹199 to ₹399, with some going up to ₹1,500.

“We would never tinker with the opening price points and the lower price points in these difficult times, because those are the customers who are the most vulnerable in inflationary situations,” Kapur said.

Hemant Jain, CEO of KKCL, said the company was willing to absorb part of the pressure on profitability to protect revenues and market share.

Jain also said the company had not yet implemented price hikes despite the inflationary environment.

To cushion the impact, companies said they are increasingly relying on cost optimisation, fabric innovation, premium fashion products and deeper expansion into smaller towns to sustain growth.

V-Mart said it was attempting to offset part of the inflation through alternative fabric usage, sourcing efficiencies and tighter inventory planning.

The retailer has also blocked orders in advance and is utilising existing yarn and fabric inventories available with vendors to soften the immediate impact of rising prices.

Vishal Mega Mart’s Kapur said it has revived cost-saving measures from the post-Ukraine cotton inflation cycle, including replacing cartons with gunny bags, removing polybags from some apparel categories, and shipping footwear without outer cartons.

The retailer has also increased the use of computer-aided design systems to reduce fabric waste during cutting.

Premium products, private labels offer buffer

These value retailers are also increasingly depending on premium and higher-fashion assortments, where consumers are relatively less price sensitive, to absorb selective price increases while keeping entry-level products affordable.

Kapur said Vishal Mega Mart’s large private-label portfolio, which contributes over 74% of its revenue, gives it greater flexibility to manage pricing pressure while maintaining discounts against national brands.

KKCL on the other hand, said it would absorb part of the inflationary impact rather than immediately pass on higher costs to consumers.

These retailers are also increasingly leaning on expansion into smaller towns and deeper markets to drive incremental growth as discretionary spending in larger urban centres remains uneven.

Value fashion retailers have underperformed the broader market amid growing concerns over rising input costs and margin pressure. Shares of V-Mart Retail, V2 Retail Ltd, Vishal Mega Mart and Kewal Kiran Clothing have fallen between 4% and 11% on a year-to-date basis, while the benchmark BSE rose 6.1% during the same period.

(Published in MINT)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

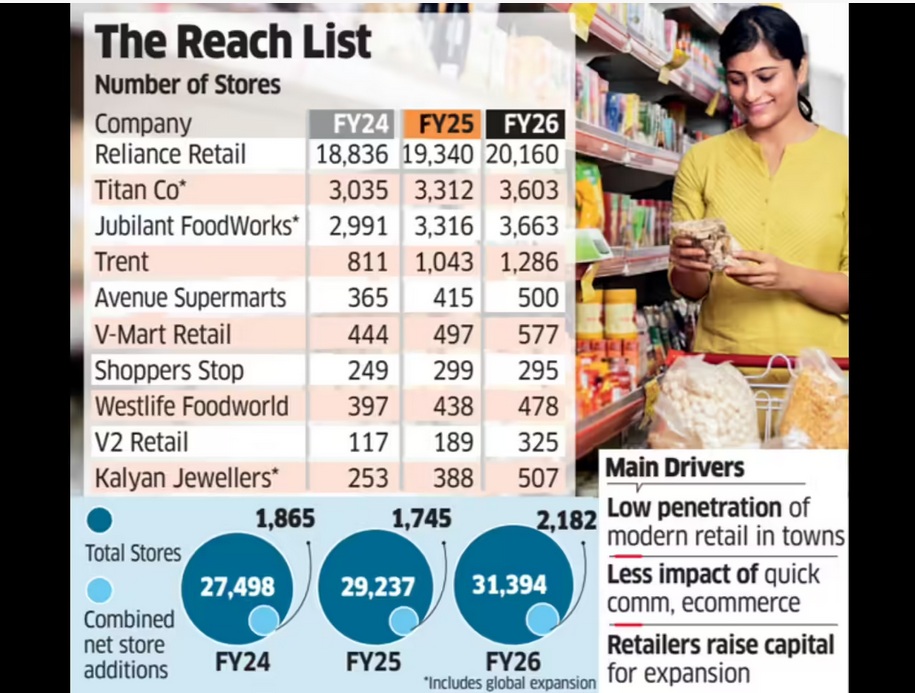

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

October 24, 2025

Entrepreneur India

Oct 23, 2025

Indian consumers are increasingly opting for private labels and in-house brands over established ones, and retailers are taking note. According to EY’s ‘Future Consumer Index 2025’, more than half of India’s consumers are now choosing in-house brands over legacy labels.

The report highlights that 52 per cent of Indian consumers have switched to private labels for better value, while 70 per cent believe these in-house brands offer comparable or superior quality. Backed by this shift, retailers from BigBasket to DMart, and quick-commerce players like Zepto and Blinkit, are doubling down on their private label strategies, viewing them as a path to higher margins, stronger brand loyalty, and greater pricing control.

“Indian consumers’ growing preference for private labels reflects both short-term price pressures and a longer-term structural evolution in retail,” said Devangshu Dutta, CEO of Third Eyesight, speaking to Entrepreneur India.

Trending globally

The surge isn’t unique to India. A recent report by the Institute of Grocery Distribution (IGD) notes that globally, private labels now account for over 45 per cent of grocery volume and are expanding faster than legacy brands.

In India, this shift is becoming increasingly visible in-store. The EY report found that 74 per cent of consumers have noticed more private label options where they shop, and 70 per cent say these products are now displayed more prominently, often placed at eye level, signalling a strategic retail push.

Commenting on this trend, Angshuman Bhattacharya, Partner and National Leader, Consumer Products and Retail Sector, EY-Parthenon, said, “Consumer behaviour has traditionally evolved in response to changing economic situations, but the current shifts appear to be more permanent. Retailers are confidently launching private labels and allocating prime shelf space to them, while technology is enhancing the shopping experience by providing consumers with limitless options and the ability to compare products.”

From price-fighters to power brands

According to Dutta, private labels are no longer just “copycat” alternatives meant to undercut national brands.

“For retailers, not just in India but globally, lookalike private labels used to be tools at the opening price point to hook the customer, who saw them as credible, affordable alternatives to national brands,” he explained, adding, “However, as retailers have grown, they have gained both scale and expertise to widen and deepen their supply chains.”

Over time, he said, investments in formulation, packaging, and quality consistency have increased consumer trust.

“Private labels now compete on functional benefits rather than only on price, particularly in food staples and apparel, but also in brown goods and white goods, and increasingly in personal care and other FMCG categories,” he added. [Must read: “Private Label Maturity Model”]

Retailers scale up private labels

As demand for in-house brands grows, retailers are scaling up their strategies across sectors.

BigBasket, one of India’s largest online grocery platforms, reported that 35–40 per cent of its FY24 sales came from private labels like Fresho, BB Royal, and Tasties. The company aims to push this share closer to 45 per cent through expansion in frozen foods and ready-to-eat categories.

DMart’s private label arm, Align Retail, has reportedly more than doubled its sales in two years, touching INR 3,322 crore in FY25. The retailer’s in-house brands in staples, apparel, and home essentials have helped boost margins in a highly competitive retail landscape.

Zepto, the quick-commerce player, is taking private labels into the 10-minute delivery domain. Its brand Relish, focused on meats and eggs, has achieved INR 40 crore in monthly sales.

Meanwhile, Reliance Retail has also expanded its portfolio of private labels, including Good Life, Enzo, and Puric, across groceries, personal care, and household products, strengthening its broader FMCG play. In 2024, Reliance Retail’s Tira Beauty also announced the launch of its latest private label brand, Nails Our Way, signifying a major expansion in its beauty offerings.

Capturing a lion’s share in retail

Dutta noted that in India, private labels will remain a core pillar of modern retail strategy rather than a cyclical response to cost pressures.

“Consumers increasingly view retailers as brand owners rather than intermediaries. As private labels mature in branding and innovation, their growth aligns more and more with brand equity development rather than just opportunistic cost-saving,” he said.

From a retailer’s perspective, private labels deliver higher gross margins and greater strategic control, Dutta said. [Must read: “Private Label Maturity Model”]

Another report by the Private Label Manufacturers Association (PLMA), using Circana data, found that in 2024, private-label sales in food and non-edible categories grew faster than bigger brands globally. While figures vary by region and quarter, the pattern remains consistent: private labels are outpacing traditional FMCG growth.

Collectively, these shifts show that private labels are becoming a major revenue driver for retailers in India, and are fast evolving from value alternatives into brands with genuine consumer pull.

(Published in Entrepreneur India)

admin

August 18, 2025

Hiral Goyal, The Morning Context

18 August 2025

A trend that has been playing out through big and small changes over the last two decades is that in urban India the kirana store is easily replaceable.

When it comes to buying groceries, urban Indians have a number of options. They can visit a fancy supermarket run by a conglomerate or order online through a number of e-commerce and instant-delivery companies. And if the above doesn’t seem easy enough, they can hop over to a nearby mom-and-pop store.

It would appear it is now the turn of smaller towns in the country to witness the kirana disruption. Even though 99% of grocery shopping in these tier-3 cities is done through neighborhood general stores, there are startups that believe this is an outdated and inefficient form of retail and a change is in order.

One such company is SuperK. The startup’s mission is to build a grocery store model in small towns that has all of the advantages of modern retail packed in a compact 800-square-foot store. This is what Anil Thontepu and Neeraj Menta had set out to do when they founded the company in 2019. The idea was to bring a modern trade-like grocery shopping experience to small-town India a wide assortment of products at a better value.

“There is a cost-efficient world of general trade and a customer-loving world of modern retail,” says Thontepu. “We wanted to see if we can bridge this gap…and do something for the small-town people by bringing the best of both these worlds.”

Over the past five years, the Bengaluru-headquartered startup has opened over 130 stores across 80 towns in Andhra Pradesh. And it doesn’t want to stop there. The company wants to expand to another 300 towns in Andhra Pradesh and nearby states of Karnataka and Telangana over the next 24, months. That’s quite an ambitious target. But the founders believe the market size for Superk is so large that they should be able to build a Rs 2,000-3,000 стоore ($228-342 million) annual business from Andhra and Telangana alone.

To fuel this expansion, Superk raised Rs 100 crore ($11.7 million) in Series B funding last month. The round, led by Binny Bansal’s 3STATE Ventures and CaratLane founder Mithun Sacheti, valued Superk at 2-2.5x its previous valuation of Rs 160 crore (about $18.25 million) in 202/

Now, Superk is not entirely unique. It competes with startups like Frendy, Apna Mart and Wheelocity, which are also trying to organize the retail market in India’s smaller towns. What sets SuperK apart is its larger, bolder approach. Grocery chain Apna Mart, for instance, runs franchisee stores in tier-2 or tier-3 markets and also offers 15-minute home delivery, SuperK’s focus is only on supermarkets. Frendy operates mini-marts and micro-kiranas in villages and towns with fewer than 10,000 people, but SuperK targets small towns with populations between 20,000 and 500,000. And Wheelocity supplies only fresh produce to rural areas, while Superk sells dry groceries as well as packaged consumer goods.

This rather radical shift in focus-away from tier-1 and tier-2 cities-ties in with India’s changing consumption pattern. “Consumer mindsets are changing even in smaller cities,” says Devangshu Dutta, founder and chief executive of Third Eyesight, adding that these consumers are beginning to favour more modern retail environments. And NielsenIQ’s latest report says rural markets in India grew twice as fast as cities between April and June 2025.

In this landscape, SuperK fits like a glove, with its franchise-first approach. Thanks to an asset-light model, the company has the agility to go deeper into smaller towns.

But it won’t be all that easy either. As Dutta says, “Changing grocery habits is a long, capital-intensive game.” Moreover, big retail chains are also jumping on the bandwagon. Hypermarket chain Vishal Mega Mart, for instance, already operates 47% of its stores in tier-3 cities and plans to expand into cities with populations exceeding 50,000. Supermarket chain operator DMart is also focusing on tier-2 and tier-3 cities.

However, Superk founders believe they are prepared for the challenge. Menta says the startup has arrived at a business model that is scalable, sustainable and, more importantly, offers value to its customers.

It’s too early to say whether they will be successful in this endeavour. That said, SuperK appears to have built a smart retail business for small-town India.

Refining small-town retail

SuperK’s founders have drawn inspiration from domestic and international retail chains like DMart and Costco. But they haven’t duplicated their strategies and made their own tweaks instead. For instance, large retail chains usually run company-owned and company operated, or COCO, stores. Though this approach is more cost-intensive than the franchise model, it allows a company to ensure a uniform customer experience across all outlets:

Superk doesn’t do that. It runs only franchise-owned and franchise-operated (FOFO) stores, which are no bigger than 800 sq ft. The company is not the first to have experimented with this model, but Thontepu believes that everyone else before them “did not try with the right spirit”. A franchise-owned store, argues co-founder Menta, is run differently from a company-owned store one has to keep in mind the store owner’s incentives, needs and concerns.

Under the franchise model, entrepreneurs invest between Rs 12 lakh (about $13,690) and Rs 15 lakh (about $17,110) to set up a Superk store. Of this, Rs 4 lakh (nearly $4,560) is spent on the store fit-out and infrastructure, the rest goes towards buying inventory. These stores, according to Menta, typically achieve a breakeven point after six months. On average, a retail store takes longer than that-12-15 months to reach breakeven.

Superk fills the shelves by procuring its inventory directly from brands as well as distributors. “The inventory is recommended by us through a mobile application. Store owners have an option to make certain changes within the limits that we have set for them,” says Thontepu. Revenue is shared and the model is similar to the one followed by nearly all retailers in India. Franchisees earn varying levels of margins on different kinds of products, depending on how easy or tough it is to sell those items. For instance, staples like dal and rice have lower margins, while confectionary items and products that need greater effort to sell enjoy higher margins of up to 20%.

In addition to this, there’s a private label business, especially loose items like pulses. In fact, private labelling is part of the company’s efforts to bring some standardization in India’s unorganized retail market. “A customer coming to our store should be able to blindly expect consistent quality on the product they’re buying,” says Menta. “We have organized our sourcing, processing, cleaning, packaging, testing. Everything that a brand would do to provide a great-quality product to their customer.”

Unlike distributors or other retailers who operate franchise models though, Superk claims that it does not dump its inventory on store owners. Menta says the franchise structure is designed in a way that Superk does not benefit from selling unnecessary stock to store owners. “If I lose, he will lose. If he loses, I lose. That is the way (the structure) is created. We, in fact, recommend owners to remove some products if they are not selling.” says Menta.

On the customer side of things, Superk’s value proposition comes down to offering the best prices. More than a year ago, for instance, it introduced a membership programme that offers customers cashback that is redeemable on their future purchases. “If they pay Rs 300 [approximately $3.5) for a six-month membership, they get 10% cashback on all purchases that they are making up to Rs 300 every month,” explains Thontepu. He says 35-40% of Superk’s more than 500,000 customers are enrolled in this programme.

All of this sounds good even promising in theory. But will it be enough to build a sustainable and scalable retail business?

A long, hard look

Let’s first look at what really works in SuperK’s favour.

One, the focus on selling staples under a private label brand. This has been done successfully before. One example is Nilgiri’s, one of India’s oldest supermarket chains.

Founded in 1905, Niligiri’s operated under a franchise model and sold dairy, baked goods, chocolates and other items produced under its own brand. The supermarket chain was sold by debt-ridden Future Group for Rs 67 crore ($7.65 million) in 2023, less than one-third the price the latter paid to acquire the company from private equity firm Actis in 2014. However, its history is worth learning from.

Shomik Mukherjee, a Delhi-based consumer goods advisor who was a partner at Actis while the firm was in control of Nilgiri’s, recalls the value proposition created by Nilgiri’s private label products. “In the case of private labels, it is essential for a company to have a reason why people will walk into that store. For Nilgiri’s, it was bakery and dairy products,” says Mukherjee. Owning a private label that brought in customers also ensured that franchisee owners had incentives to continue working with Nilgiri’s. “It is about giving the franchisees a safe portfolio of private label goods that are desired by customer instead of something that is shoved down the franchisees’ throat to derive margin,” he says.

You see, the overall grocery business operates on a very low margin. But private labelling, says Satish Meena, founder of Datum Intelligence, offers the highest margins – 35-40% – in the grocery business, after fresh produce, making it a lucrative business to get into.

Superk, which sells essential items through its private label, has the opportunity to earn better margins in grocery retail. More importantly, private labelling holds the potential to become SuperK’s identity and boost customer retention and loyalty.

Two, SuperK’s franchise model allows it to expand to more locations rapidly as compared to a regular modern trade chain with company-owned stores, says Mukherjee. This model makes SuperK’s business asset-light and brings down the cost of running a network of stores. “Under this model, the franchisor does not incur the upfront cost of opening a store or having to deal with the trouble of hiring and replacing store managers,” he adds. Since most store owners in a franchise model are landowners, there is a greater stability in operations as well, he explains. Moreover, Superk stores are quite small (800 sq ft), allowing easier availability of property.

The franchise model, however, is not entirely foolproof. One of the inherent problems is the difficulty in implementing standard operating procedures (SOPs) across all stores. And the problem only worsens as the company expands operations to different cities. While Superk stores boast a no-frills fit-out that can be easily set up anywhere, how these stores are maintained through the wear and tear over the years is yet to be seen.

A bigger fear is that the store owner may start running their own store without the Superk branding. “If Superk loses the franchisee owner, it also loses the location in which the store was operating,” says Mukherjee.

Moreover, most franchisee owners in the retail business typically tend to be experienced general store owners who might not be willing to adopt new technology. “Since they have run a store before, they think they know how and what to order for inventory and may not follow SuperK’s tech-enabled recommendations,” says Mukherjee.

There’s another problem. While the founders claim to have seen considerable success (35-40% sign-ups) in the rollout of SuperK’s membership programme for customers, Third Eyesight’s Dutta raises concerns about its future growth. “Indian consumers’ price sensitivity limits membership fee potential,” he says. According to him, the programme’s value in the tier-3 market lies more in customer acquisition and retention than direct revenue generation. “Long-term success requires a cashback programme to drive purchase frequency and basket size increases to offset the costs,” says Dutta.

Menta, however, has a different view. He says SuperK’s subscription is designed in a way that benefits customers only when they make full basket purchases. Moreover, the company has different pricing slabs for membership depending on the various basket sizes, which makes the model more viable. Considering the programme is a little more than a year old, it is still too early to judge whether it will find a lot of takers in small towns.

For now, the founders are in no hurry to expand their business across India. “There is no reason to go into five states. Then, you are spread thin and your economics will not work out. It’s a business of managing operations at a very low cost,” says Menta. The plan is to stick to one region and continue to go deeper into it. “A lot of our competitors who started five years ago spread to so many places that it became very difficult for them to manage,” he adds.

This is also the crux of how Thontepu and Menta are building SuperK. By implementing what they have learnt not only from their own experiments, but also from the failures and successes of other businesses. While there’s no guarantee that Superk will become a roaring success, it does appear to have set an example by starting small and growing patiently. And if the latest funding is any proof, investors are interested.

(With inputs from Neethi Lisa Rojan)

(Published in The Morning Context)