admin

July 9, 2026

Neethi Lisa Rojan & Vaeshnavi Kasthuril, MINT

Mumbai/Bengaluru, 8 July 2026

The collapse of the US-Iran peace deal in less than a month has rattled India’s consumer sector, reviving fears that higher oil prices and fresh supply-chain disruptions could squeeze demand just as companies were betting on a broader recovery.

The renewed uncertainty followed US President Donald Trump’s declaration on Wednesday that the peace deal with Iran was effectively over, alongside Washington’s decision to end a sanctions waiver on Iranian energy supplies. The market reaction was swift. The Nifty FMCG Index fell 2.49% on Wednesday, underperforming the broader market as all 15 constituents declined, led by Dabur India, Hindustan Unilever, and Tata Consumer Products, whose shares fell 3-4% each. The benchmark Nifty50 ended 2.12% lower after renewed hostilities in West Asia pushed crude prices higher.

Executives and analysts said companies have little room to respond immediately, leaving them to closely monitor devel opments as risks to costs and consumer spending mount. “I don’t think companies can react on this kind of a short notice,” said Arvind Singhal, chairman of consulting firm The Knowledge Company. “It takes 2-6 months to make any change in your plans and strategy. I think right now the Indian FMCG (fast moving consumer goods) companies will be watching the progress of monsoon more carefully than the Strait of Hormuz.”

Even after the US-Iran peace deal took effect on 18 June, consumer companies were unlikely to have expected immediate relief, analysts said.

“While everyone hoped for a cessation in hostilities, smart management teams would work on the realistic expectation that even with a ceasefire, pent-up supply chain input costs need to be absorbed over time, and pricing plans must be factored accordingly,” Devangshu Dutta, founder and chief executive of consulting firm Third Eyesight, said.

“Given that the conflict zone is active, I don’t think there is any immediate likelihood of pricing freeze or reductions, even though demand in rural areas as well as in lower-income urban segments is likely to be hit from both sides ― earnings and expenses.”

Large consumer goods companies including Dabur, Emami and Godrej Consumer had recently told investors they remained confident about consumer demand, including in rural markets.

But the renewed rise in crude prices, coupled with erratic monsoons marked by rainfall deficit in some regions and flooding in others, threatens to complicate that outlook. Higher fuel costs could lift prices of crude-linked raw materials such as plastic packaging and ingredients used in soaps and creams, while persistent inflation could push consumers to cut discretionary apne ding and trade down even on staples.

Major consumer companies had already raised prices or reduced grammage across packaged food, beverages and personal care products in the March quarter.

“As far as the crude prices are concerned, that is probably the only variable where the government has to decide as far as pricing of crude or the petroleum in India is concerned,” Singhal said.

That comes at an awkward time for India’s largest consumer companies, including Hindustan Unilever, which had earlier this year told analysts they intended to drive growth through higher volumes rather than price increases. A renewed bout of inflation could undermine that strategy.

(Published in MINT)

admin

June 22, 2026

Sharleen D’souza & Shivani Shinde, Business Standard

Mumbai, 21 June 2026

Online beauty marketplaces Reliance Retail Ventures’ Tira and Nykaa have a common mantra: growing in-house brands. Successful brand acquisitions and margin growth seem to fuel the push.

“With private labels, margins are better. It also helps both companies plug the gap in the market which other brands are not present in,” Devangshu Dutta, chief executive officer (CEO) of Third Eyesight, told Business Standard. Within in-house brands, products need some investment in research and development (R&D), he explained.

Harish Bijoor, brand and business strategy consultant at Harish Bijoor Consults, said that margins are better for platforms with in-house brands.“Typically most companies are getting insular. The idea is to own brands and own the profits from those brands. When you are a marketplace, you put in effort for other brands, this strategy helps marketplaces lock in on profits instead of losing out to other brands, which sell on the platform,” he said.

At the 49th annual general meeting of Reliance Industries (RIL) on Friday, Isha Ambani, executive director of Reliance Retail Ventures Ltd, and non-executive director of RIL, had laid out plans for Tira. “We will scale our own brands to consumers across India and beyond, ensuring Indian beauty prod-

ucts stand proudly alongside the world’s leading global giants.”

Its in-house brands include Puraveda, Pahadi Local, haircare brand Anomaly, which was recently acquired from actress Priyanka Chopra Jonas, and skincare and make-up brand Akind, which it co-created with Mira Rajput Kapoor. Its portfolio also includes Nails Our Way and Dream Immerse Play.

Ambani’s statement had come a day after Nykaa’s management had also hinted at expanding its in-house brands on its investor day on Thursday. The platform, operated by FSN E-Commerce Ventures, outlined an ambitious road map to become an over $5 billion beauty and lifestyle business.

The growth of Nykaa’s “House of Brands” is expected to be significant. The management aims to be the largest house of brands business in India by financial year 2030 (FY30). Management has guided toward a net sale value (NSV) compounded annual growth rate (CAGR) of 30 per cent over FY26-30, taking the NSV from Rs. 1,700 crore in FY26 to Rs. 5,000 crore by FY30.

The “House of Nykaa” GMV grew over 65 per cent in FY26, with an improvement in profitability. In a report on the company’s focus on in-house brands business, Motilal Oswal said, “House of Brands is expected to grow faster than the core marketplace business and become a meaningfully larger contributor to group revenues and profits by FY30. We believe profit contribution is expected to increase disproportionately, given the higher gross margins, stronger pricing control, and lower dependence on third-party brands.”

Nykaa’s platform creates a structural incubation advantage, it said. “Fashion today serves about 300,000 styles across categories, while customer discovery increasingly happens through content, personalisation, and creator-led commerce. This allows the company to identify emerging brands and categories early, before allocating capital behind them,” the report added.

As of the fourth quarter of financial year (FY26), “House of Nykaa” had 12 brands across Beauty and Fashion categories at various growth stages, and two successful acquisitions of Dot & Key and Earth Rhythm. Dot & Key has grown 13 times over the last three years, while Kay Beauty has grown three times over this period, said the company. During the Q4FY26 results, the company had said that the strong performance of “House of Nykaa” had impacted margins positively. P Ganesh, chief financial officer, FSN E-Commerce while explaining the margin growth said, “…with gross margin improving by 132 basis points

in FY26, led by strong performance of House of Nykaa and improved service income across businesses.”

For FY26, “House of Nykaa” delivered a strong Rs. 3,176 crore of GMV. “That’s an about 50 per cent year-on-year increase. Served more than 17 million consumers and expanded distribution beyond online as well to 150,000 GT doors. As a reminder, this unit includes brands across beauty and fashion, seven brands in Beauty and in Fashion five brands, with an increased focus on one in particular, which is Nykd,” said Adwaita Nayar, executive director, cofounder and chief executive officer, “House of Nykaa Brands”, during the fourth quarter results.

(Published in Business Standard)

admin

June 8, 2026

Arushi Jain, The Times of India

8 June 2026

Their faces have launched many campaigns and brought crores to the film industry. But can they sell a moisturiser as successfully? India’s beauty market is the hottest growth story globally, estimated to reach $40 billion from $23 billion (2026) and eyeing the fourth-largest spot by 2030 (currently at number seven).

Last month, Estée Lauder announced the buyout of Forest Essentials, one of India’s oldest, Ayurveda-based brands. In 2025, Hindustan Unilever acquired five-year-old skin and hair care brand, Minimalist. A 2025 McKinsey & Company x Business of Fashion survey found that 78% of global beauty executives see India as the most promising growth market. Even celebrities have shown up with chequebooks, but fans are no longer buying at face value.

While Hailey Bieber’s Rhode built a cult following through what she calls an “outside of the box” strategy, Deepika Padukone’s 82°E reported a 30% revenue dip in FY25. Nykaa is in talks to acquire a stake in the brand.

India’s consumer has evolved faster than the brands serving them. They are reading labels now, not just recognising famous faces on packaging. Star power, it turns out, only gets you so far.

Fame gets you in the door. Formulation keeps you there

If a celebrity is the invitation to the party, formulation is what keeps the guest at the after-party. Despite India’s celebrity beauty segment crossing an estimated `5,000 crore in GMV in FY24, scale has not translated into customer retention. The initial spike, familiar to anyone who has tracked a celebrity launch, gives way to an uncomfortable question: what brings a customer back?

“Celebrity isn’t necessarily a sustainable brand asset,” says Devangshu Dutta, CEO of retail consultancy Third Eyesight. “While celebrities can act as interest-creators and trial-generators, repeat purchases are built on functional reasons, not imagery alone.”

Founders echo the same reality from the ground. “Honestly, people come back for what works,” says Aashka Goradia Goble, co-founder of RENÉE Cosmetics. “If a product performs well, feels easy to use, is priced right, and becomes part of someone’s everyday routine, they’ll keep reaching for it.”

Price, too, remains a decisive filter. Sunny Leone, founder of StarStruck, says, “In India, price is the main component.” The journey from first purchase to loyalty is driven by habit, and habit, in beauty, is built on results.

Positioning over popularity

The gap between a viral campaign and a repeat purchase is wider than most A-listers realise. Brand guru Harish Bijoor locates the problem in what he calls the “spinal cord” of a brand: a single, clear positioning that holds the entire business together.

Rihanna’s Fenty is inseparable from its commitment to shade inclusivity. Kylie Jenner’s Kylie Cosmetics was built around one obsession: lips. “It is extremely important to understand what you want to be and focus on just one thing and not on everything,” Bijoor says. That clarity is precisely where most Indian celebrity beauty brands are still finding their footing.

The old playbook: launch a brand online, wrap it in the language of “clean” or “natural,” and wait for a global conglomerate to come calling has run its course. Today, strategic buyers and consumers alike want a brand that can stand on its own. The question is no longer whether a celebrity can generate awareness. It is whether the brand they have built can survive them.

What the labels that last have in common

The brands breaking through are doing so quietly and methodically. In a category where fame can spark interest but not always guarantee repeat purchase, Katrina Kaif’s Kay Beauty, launched with Nykaa in 2019, has emerged as one of celebrity beauty’s more consistent success stories.

The main reason is less about star power and more about strategy. “If you contrast Kay Beauty and 82°E (Deepika Padukone’s brand), Kay Beauty has two distinct advantages,” says Dutta. “Firstly, being priced for a much larger audience, and secondly, having the active participation of Nykaa across channels in terms of merchandising and visibility push for the brand.”

Nykaa is candid about what made the difference. “When we co-created Kay Beauty with Katrina, shade ranges and formulations designed for Indian skin tones and climate were severely limited,” a spokesperson shares, adding that the celebrity association “amplified the brand rather than substituted for it.” The strategy appears to have paid off: Kay Beauty is now a ₹500 crore-plus annualised GMV brand, with new launches contributing 21% of revenue as of Q3 FY26.

Why Indian skin demands more than a famous name

For Indian celebrity brands, the challenge is not just performance; it is perception. “Domestically, we see the mentality for buyers is to look at international brands first based on trust, and then try domestic brands based on lower price value,” says Leone.

Indian consumers are also highly specific in what they expect. According to market research firm Mintel, shoppers are increasingly drawn to formulations that are clinically tested and grounded in both science and local familiarity. Products must perform in Mumbai’s humidity and Delhi’s pollution and suit the full spectrum of Indian skin tones.

“Indian consumers love products that do more than one job, last long in our weather, and actually match Indian skin tones,” says Goradia. They are cautious spenders, she adds, but willing to invest when they see real quality and innovation.

Nykaa says this ingredient awareness is now visible across the country, not just metros. “Consumers are reading about niacinamide and retinol, they know what they want from a sunscreen, and are making considered purchase decisions. Brands need to earn their place on merit in every market,” says the spokesperson.

“A brand that addresses these needs well and remains within the customer’s budget succeeds,” says Dutta.

Gen Z will drive 50% of India’s beauty consumption by 2030

By 2030, Gen Z will drive 50% of India’s beauty and personal care consumption, a third of all sales will happen online, and per capita income is forecast to rise 138% in real terms by 2040, according to Euromonitor. Nykaa founder and CEO Falguni Nayar told Bloomberg that comparing India’s beauty routines to South Korea’s famed 14-step regimens is premature, “It is still day zero for beauty consumption in India.”

The global conglomerates have done the math. Estée Lauder, L’Oréal, and Puig are all moving deeper into India, betting on a consumer who is younger, more digitally fluent, and more ingredient-literate than any previous generation. The brands they are acquiring, Forest Essentials, Minimalist, Kama Ayurveda, share a common thread: They are built on something that exists independently of a famous face. “This is an industry that is very crowded and takes a lot of time to grow,” says Leone. “Western brands focus on global distribution and profit and loss. Not just turnover at a loss.” The celebrities who will build something lasting are the ones who understand that the launch is the easiest part. As Bijoor puts it: “Celebrity beauty is not skin deep at all. It is a deep brand science.”

(Published in The Times of India)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

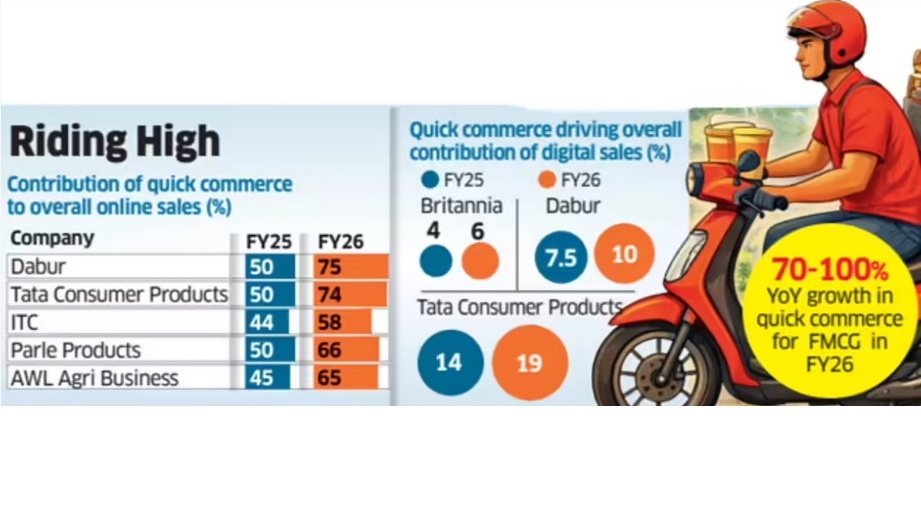

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 15, 2026

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving “imported inflation” and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below):

1. Dual Impact on Industry and Consumers:

2. Vulnerability of Small Businesses (SMEs):

3. Income vs. Expenditure Strain:

4. Ripple Effect of Crude Oil Beyond Logistics:

5. Shifts in Consumer Spending Patterns & “Shrinkflation”:

The panel noted that while the Reserve Bank of India (RBI) has adequate foreign exchange reserves to defend the rupee temporarily, the definitive solution relies heavily on the cooling down of global geopolitical tensions (such as the Middle East conflict affecting the Strait of Hormuz). Until then, Indian consumers will need careful financial planning and smart spending adjustments to navigate this inflationary phase. [Video below.]