admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

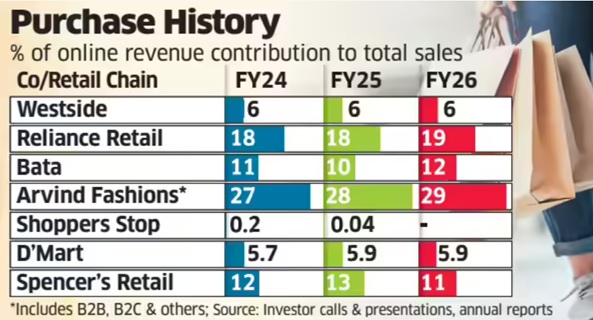

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

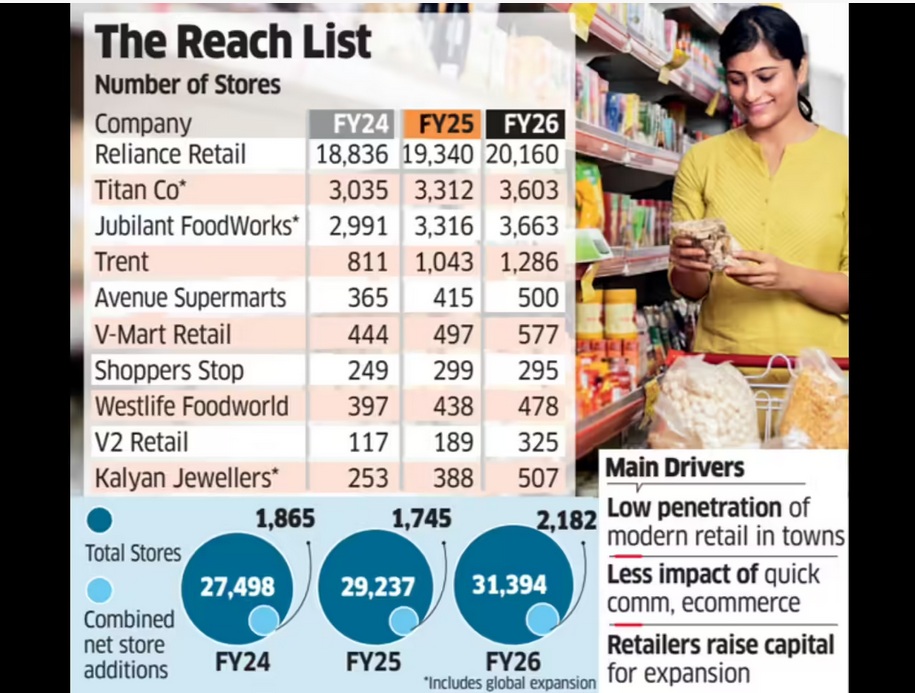

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

May 2, 2026

Neethi Lisa Rojan, Mint

2 May 2026, Mumbai

Fast-moving consumer goods makers are leaning on a mix of price increases, smaller pack sizes and tighter cost controls to navigate raw-material volatility triggered by the ongoing US-Iran war, while still reporting robust volume growth for the March quarter. The ongoing war blew up end February this year, disrupting global supply chains.

Executives at top firms said calibrated pricing and ‘shrinkflation’ are helping them protect margins. The trend shows staples demand have held up, but also points to a gradual pass-through of higher commodity and packaging costs to consumers as geopolitical disruptions keep input prices elevated.

At Hindustan Unilever Ltd, the strategy is already in motion. The company has implemented calibrated price hikes and adjusted grammage across products. “We are taking calibrated pricing action in the range of 2-5%,” chief financial officer Niranjan Gupta said in a post-earnings briefing on Thursday. “We use a combination of both the put-down price as well as optimizing the fill levels,” said Gupta. The management also noted that its products in the homecare segment such as soaps (Lux, Pears, Dove, etc.) and detergents (Surf Excel, Rin, etc.) will be the first to be affected by price hikes. Interestingly, this happened at a time when HUL’s volumes grew the fastest in 15 quarters.

Companies have anticipated how consumers will behave.

“In times of inflation, income uncertainty, etc. essentials such as packaged foods, biscuits, and household cleaning products tend to see trade-down behaviour rather than outright disappearance of demand,” said Devangshu Dutta, founder of management consultancy, Third Eyesight. “Consumers tend to shift to smaller pack sizes or private labels, rather than abandoning categories altogether,” he adds.

India’s retail inflation rose from 2.75% in January 2026 to a 10-month high of 3.40% in March, driven largely by food prices.

That balance between pricing and demand is playing out across the sector. Nestle S.A., the parent company of the Indian entity said it saw 3.5% organic sales growth during the quarter, with RIG (real internal growth or volume growth) of 1.2% and pricing of 2.3% in the January-March quarter.

“The conflict in the Middle East will have some impact on commodity and distribution costs, and possibly on consumer behavior. But it’s too early to know the full extent of this,” chief executive officer at Nestlé S.A, Philipp Navratil said in the analyst call after the results. Its India unit, Nestlé India, reported its strongest quarterly growth in nearly a decade, led by double-digit volume expansion.

HUL reported a 21% year-on-year rise in consolidated net profit to ₹2,994 crore, while Nestle India saw net profit up 27% at ₹1,110.9 crore. year-on-year to ₹1,110.9 crore in Q4 FY26. HUL has also retained its medium-term guidance for earnings before interest, taxes, depreciation, and amortization (Ebitda) at 22.5%-23.5%.

The resilience in volumes comes even as input costs surge. Prices of crude oil-linked materials, especially packaging, have risen sharply following disruptions around the Strait of Hormuz chokepoint. High-density polyethylene, widely used in packaging, jumped about 42% in March from the previous month.

Multinationals are already bracing for the fallout. Tide and Gillette maker Procter & Gamble, said in its quarterly earnings call that it could take roughly a $1 billion post-tax hit to its fiscal 2027 profit from surging oil prices. Still, not all inputs are moving in tandem. Prices of staples such as wheat, sugar, tea and coffee have remained relatively stable, offering some cushion. Edible oils, however, remain a concern.

Palm oil, a critical input in many FMCG products, is seeing supply shifts, as producers such as Malaysia and Indonesia divert output toward biodiesel. AWL Agribusiness, which sells Fortune oil, said in the quarterly analyst call that edible oils faced a 10% price surge in March, which has already been passed to consumers. The company expects to pass on the rise in packaging material prices also soon. The company posted a 53% jump in consolidated net profit to ₹292 crore in Q4FY26, from ₹190 crore a year earlier.

Experts expect the trend of margin-saving strategies to continue.

“Depending on the product, category and brand, we will see a mix of price hikes, shrinkflation and rationalization of SKUs (stock keeping units), and also a shift from brand-related to tactical advertising and promotional spends to boost short-term demand,” Dutta said.

Elsewhere, companies are acknowledging broad-based inflation but are continuing to push through growth. Bajaj Consumer Care reported near double-digit volume gains even as managing director Naveen Pandey noted that “nearly 100%” of its cost base is under inflation. The company plans further pricing actions alongside cost optimization. Bajaj Consumer Care’s net profit for the March quarter more than doubled to ₹63.6 crore from a year ago.

Beyond the basics

The ripple effects extend beyond staples. Fashion, lifestyle and grocery retailer Trent Ltd flagged uncertainty around supply chains and inflation, warning of potential implications for near-term demand. “Duration and intensity of disruptions in the Middle East, along with its second order effect on supply chain, commodity prices and inflation in general has potential implications for near-term demand,” the company said in its results presentation.

Meanwhile, consumer appliance maker Havells India has initiated price increases after what chairman Anil Rai Gupta described as an unprecedented escalation in input costs. “I’ve not seen this kind of a price escalation in the recent past in the recent memory,” he said in the post results analyst call.“ Calibrated price actions have been initiated, he said. Havells India reported a strong 40% year-on-year increase in net profit to ₹723 crore in the March quarter.

More clarity may emerge as additional earnings roll in. Companies with higher exposure to West Asia, such as Dabur and Emami, are yet to report results and could face greater consolidated impact due to regional disruptions. “Companies such as Dabur and Emami will be more affected at the consolidated level due to issues in the MENA or Middle East and North Africa Region (6-8% revenue salience),” said analysts at Motilal Oswal Financial Services ahead of the earnings season.

For now, inventory buffers are offering temporary relief. Some companies have built raw-material stockpiles lasting up to six months, helping them absorb immediate shocks. “In our international markets, our effect will be in the raw material, practically zero to a couple of points maybe because we are well-stocked not just for this quarter, but the next quarter also. We normally carry six months inventory in international,” said Raj Pal Gandhi, whole-time director at Varun Beverages, the largest bottler of Pepsico in India, in the quarterly analyst call. This has helped the firm tide over the challenges in plastic shortage faced in March.

However, companies will now have to buy raw materials at higher prices, leaving room open for more price hikes.

(Published in MINT)

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

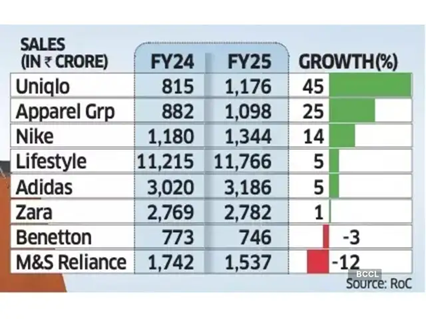

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

December 1, 2025

Priyamvada C, Mint

1 Dec 2025

A wave of investor capital is flowing into India’s laboratory-grown diamond (LGD) segment, as fastscaling brands tap rising consumer adoption in a market now worth well over $300 million. New-age brands have raised multiple rounds of capital on the back of growing market share and improving margins.

Actor Shilpa Shetty-backed Limelight, which is in talks to raise its second round of capital this year, joins the growing list of other small brands such as Onya, Giva, Jewelbox, Lucira Jewellery and Aukera, among others, who have snagged monies in recent months. Limelight has appointed Ambit Capital to raise about $20 million to fund its expansion plans, two people familiar with the matter said.

Confirming the fundraise, the six year-old company’s co-founder Pooja Madhavan said the funds will be used towards store expansion and brand building as it looks to touch 100 stores over the next year. “We are in final talks with growth PE funds and reputed family offices (for the fundraise),” she told Mint.

Other similar fundraises include Onya’s ₹5.5 crore in a pre-seed round led by Zeropearl VC last week, Aukera’s $15 million raise led by Peak XV Partners and Aditya Birla Ventures-backed Giva raised ₹530 crore in an internal round led by Premji Invest, Epiq Capital and Edelweiss Discovery Fund, as it looks to scale up its lab-grown diamond offerings.

Nine pure-play lab grown diamond startups collectively raised a record $26.4 million in 2025, compared with $4.7 million across eight startups last year, data from market intelligence provider Tracxn showed.

The development comes as India’s lab-grown diamond jewellery market, valued at about $300-350 million in 2024, expects to grow at a compound annual growth rate (CAGR) of 15% over the next decade, as per consultancy firm Redseer’s estimates. As the market evolves, several prominent jewellery brands will gradually pivot from exclusively natural/mined diamonds in favour of lab-grown alternatives, alongside high-end jewellers incorporating the lab-growns into their select collections, which will drive sales volumes and act as an affordable entry point for consumers.

This segment has particularly picked pace in the last five years, with millennials and gen Z leading this shift, driven by better value, trendier designs from new-age brands, and growing comfort with lab-grown diamonds as a certified, high-quality product. This category has also widened beyond occasional fashion to gifting, daily wear and increasingly bridal, reflecting sustained consumer confidence and a willingness to treat them as a mainstream jewellery option, Rohan Agarwal, partner at Redseer told Mint in an emailed statement.

He further added that new-age brands have steadily gained market share in the mid-ticket gifting and daily wear segment with many trying to push into premium ranges. While the competitive landscape is still evolving, incumbents have already started responding by launching LGD lines of their own, although the extent to which they can challenge remains to be seen.

Major Indian brands that are considering a foray into this category include Malabar Gold & Diamonds, Senco Gold, which has launched the subbrand Sennes and Tata’s Trent, which launched its brand Pome in Westside stores.

Devangshu Dutta, founder and chief executive officer at Delhi-based consulting firm Third Eyesight, echoed the sentiment. He explained that new-age lab grown diamond players are forcing traditional jewellers to introduce LGD options or risk losing younger customers. “Not just precious jewellery brands, even those that started as fashion jewellery are expanding their range with LGD designs.”

“Down the road, there is potentially scope for consolidation as investors tend to prefer a handful of scaled platforms with strong brand recall and robust economics. So, as the category matures, there may be strategic acquisitions by large jewellery houses and corporates, as well as mergers among funded startups,” he added.

Those startups that can combine in-house manufacturing, design capabilities and data-driven retail expansion would be at an advantage, Dutta said. “Key future growth areas for LGD startups include omnichannel retail presence within India, with offline stores especially in demand-dense locations such as the metros and Tier 1 cities, export markets both with potential cost advantages and brand expansion, and extending into fashion jewellery, everyday wear, coloured lab grown stones and even luxury collaborations that position lab grown as aspirational rather than merely budget friendly.”

(Published in Mint)