admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

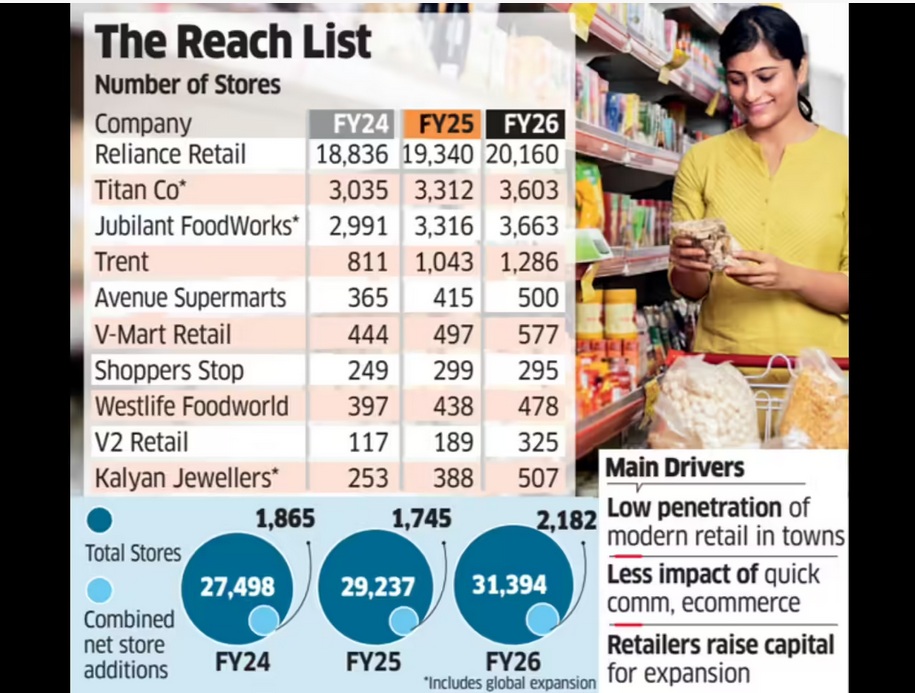

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

December 29, 2025

Yash Bhatia, Impact Magazine

29 December 2025

App, Tap, Pay and Zoom it’s delivered – that is Quick commerce for you. And in India, the narrative has so far been defined by speed, scale, high SKU counts, and the dominance of dark stores. Last week, however, Instamart nudged that model by opening an experiential store in Gurugram, allowing consumers to see and feel select products available on the platform.

The Bengaluru-based company has positioned the outlet not as a conventional retail store, but as a compact experiential format with a sharply curated assortment of around 100–200 SKUs, compared to the 15,000–20,000 SKUs typically housed in a dark store. Spanning roughly 400 sq. ft., the space is about one-tenth the size of a standard 4,000 sq. ft. dark store.

Under this model, sales proceeds are paid directly to sellers. This differs from Instamart’s regular arrangement, where payments are routed through the platform and later settled with sellers after deducting the platform’s share. IMPACT reached out to Instamart for further details, but the company declined to comment.

Sources close to the development say that Instamart has enabled sellers to open branded experiential stores in and around residential societies as part of a targeted consumer experiment. These are not conventional retail outlets, but compact experiential formats with a highly curated SKU assortment, focused on categories where consumers prefer to assess the products first-hand before purchasing, such as fresh fruits, vegetables, pulses, new product launches, and selected D2C brands. The initiative is largely centred on fresh categories and allows sellers to experiment with Instamart’s branding and service ecosystem.

Devangshu Dutta, Founder, Third Eyesight, a retail consultancy firm, says that physical presence plays a vital role in anchoring trust, particularly in premium products, groceries, and fresh produce. “Experiencing a product or brand physically can significantly enhance perceived value and help create stickiness. For this reason, offline stores continue to remain integral to the consumer products sector,” he explains.

Built on the promise of speed and convenience, quick commerce brands have come under growing scrutiny for quality and hygiene lapses at dark stores. Over the past year, several reports have flagged issues ranging from poor storage conditions and compromised freshness to the sale of expired or damaged products, particularly in food and grocery categories.

In some instances, regulatory inspections have led to licence suspensions after authorities identified hygiene violations at fulfilment centres. “Trust is what builds loyalty, and the shift is clearly moving from minutes to confidence,” says Shankar Shinde, Co-Founder, Aisles and Shelves, a behaviour-led brand consultancy in India. Shinde adds that the emergence of offline formats such as Instamart’s physical store aligns with this transition, particularly in grocery and fresh categories where consumers place a high premium on quality and consistency. “Physical touchpoints help reduce consumer anxiety, especially in a market like India, where shoppers still prefer hand-picked fresh produce such as fruits and vegetables,” he explains.

Against this backdrop, the opening of experiential centres could emerge as one way for quick commerce players to rebuild consumer trust by allowing shoppers to experience products in person before purchasing. IMPACT also reached out to Blinkit and Zepto for their views, but both declined to comment.

Kushal Bhatnagar, Associate Partner, Redseer Strategy Consultants, believes the move is aimed at unlocking incremental growth by tapping into offline-first consumers who are not yet active on quick commerce, while also catering to the offline purchase missions of existing quick commerce users. He notes that quick commerce currently reaches only about 75–80 million annual transacting users as of CY2025, even as over 90% of India’s grocery consumption continues to take place offline.

Beyond expanding reach, Bhatnagar sees offline formats as a way to address deeper trust barriers within the category. He adds that such formats can help deepen consumer confidence, particularly in categories where apprehensions around quality and freshness persist in quick commerce deliveries, concerns that are partly alleviated when consumers can experience products first-hand. Additionally, he points out that this approach benefits brands, especially emerging ones that are largely confined to quick commerce or a limited set of platforms, by giving them greater physical retail visibility without requiring heavy investment in traditional distribution networks.

Viewed through a financial lens, the move also carries implications for how quick commerce platforms justify value. Saurabh Parmar, fractional CMO, believes the initiative signals a shift from promise to performance, with a stronger emphasis on optimisation and a more realistic assessment of long-term value creation. He notes that while quick commerce has expanded into Tier 2 markets and seen growth in user numbers, these metrics alone still fall short of fully justifying current valuations. In this context, an offline presence becomes another lever to strengthen the overall business case.

At the same time, Parmar cautions that offline formats cannot replace the core proposition of quick commerce. He adds that experiential centres enhance brand credibility and make quick commerce feel closer to conventional retail, with the potential to eventually extend into other facets of e-commerce. However, he emphasises that quick commerce must continue to remain the frontline, as the sector’s valuations are fundamentally anchored in its speed-led proposition.

Retail experts, meanwhile, view physical touchpoints as a long-standing mechanism for building trust rather than a structural shift.

Dutta adds that such formats complement existing digital trust mechanisms such as delivery consistency, speed, ratings, and reviews by making brands feel tangible and accountable rather than abstract.

Bhatnagar notes that quick commerce currently has an average monthly transacting user base of around 40 million as of CY2025, leaving significant headroom for growth when compared to India’s overall e-commerce base of nearly 300 million active transacting users.

Beyond expanding the user base, he adds that experiential stores can also support wallet-share expansion across categories, which remains a key growth lever for the sector. “Non-grocery segments such as beauty and personal care, electronics, and fashion currently contribute about 25% of quick commerce GMV (Gross Merchandise Value), a share that is expected to rise further. Within groceries as well, platforms can drive incremental growth by building greater depth in fresh produce and staples,” Bhatnagar highlights.

From an operational perspective, however, the offline format is viewed more as a supporting layer than a core growth engine. Dutta sees Instamart’s offline presence as an experimental add-on rather than a replacement for its delivery-led model. The operating processes and economics differ significantly from those of quick commerce delivery, positioning physical formats as a complement to the speed proposition rather than an alternative. If the model proves viable and is backed by sufficient resources, it could eventually lead to a parallel scale-up of dark stores and experiential formats across different catchments.

For now, Instamart’s offline foray remains a tightly scoped experiment rather than a strategic pivot. Its significance lies less in square footage and more in what it signals about the evolving priorities of quick commerce. As the category matures, speed alone may no longer be sufficient to secure trust, loyalty, or long-term value. Experiential touchpoints, if deployed selectively, could help platforms bridge the gap between digital convenience and physical reassurance, particularly in categories where quality perception continues to remain fragile.

(Published in IMPACT)

admin

November 26, 2025

Aakriti Bansal, Medianama

November 26, 2025

MediaNama’s Take: The Central Consumer Protection Authority’s (CCPA) decision to publish 18 self-declarations confirms only a partial picture of its dark pattern(s) identifying exercise. The authority has stated that 26 platforms have filed their declarations, but it has made only 18 of them public. This gap means the public still cannot see what eight major platforms submitted or whether those filings contain any meaningful detail. Moreover, even among the published declarations, several are one-paragraph statements that offer almost no insight into the scope or accuracy of the companies’ internal audits.

LocalCircles’ new survey adds further complications, reporting that 21 of the 26 platforms that submitted declarations still display at least one dark pattern. This finding suggests that the CCPA’s reliance on voluntary self-assessment may not be enough to shift platform behaviour at scale. It also raises questions about what the unpublished declarations contain and whether the missing submissions are similarly sparse or incomplete.

Notably, the CCPA has not clarified how it plans to verify the accuracy of any of the declarations, whether published or unpublished. If filings remain unverified for months, compliance risks turning into a box-ticking exercise rather than a meaningful regulatory process. Therefore, the next phase matters far more than the publication of select declarations, because the current approach raises more questions than it answers.

What’s the News

The CCPA has made 18 dark pattern self-declarations public, despite stating that 26 platforms have filed their compliance letters. The publication follows an RTI filed by MediaNama that revealed which companies had submitted their declarations, and pointed out that none of the filings had been available to the public at the time.

These declarations stem from the Ministry’s June 5 advisory, which required e-commerce and quick commerce companies to conduct internal audits under the 2023 Guidelines for Prevention and Regulation of Dark Patterns and submit compliance letters within 90 days.

For context, Moneycontrol reported that Amazon has still not filed its declaration and has asked for additional time. A senior government official told the publication that the government “has done what it had to” and does not plan further discussions.

The official also said that any punitive action would depend on consumer complaints routed through channels such as the national consumer helpline. This indicates that the enforcement approach continues to be reactive rather than compliance-driven.

What Did The CCPA Ask Platforms To Do?

The June 5 advisory set out a simple compliance framework for digital platforms. It asked every e-commerce and quick commerce company to complete a self-audit of its website and mobile app within 90 days and check their interfaces for the 13 dark patterns listed in the 2023 guidelines. Platforms were required to file a self-declaration confirming compliance once this internal review was complete.

However, the advisory did not specify how the audit should be conducted. Companies were free to choose any methodology, and the CCPA did not prescribe a standard format, a uniform checklist, or a minimum evidence requirement. Also, the advisory did not require independent audits or third-party validation.

Furthermore, there was no explanation of how the CCPA planned to verify whether the declarations were accurate or complete. In effect, the responsibility for defining the scope, depth, and rigour of the audit rested entirely with each platform.

What the CCPA Has Done With the Declarations

As mentioned before, the CCPA has now published 18 self-declarations on its website. The release confirms that companies submitted their compliance letters, but it does not indicate whether the authority evaluated the accuracy or depth of the filings.

Several platforms submitted very short statements that simply assert compliance without describing any checks or findings. BigBasket, Zomato, Blinkit and Swiggy were among the companies that filed especially minimal disclosures. The CCPA has not explained why these filings were accepted or whether any follow-up questions were asked. Therefore, asking for and disclosing self-declarations shows some administrative progress, but it does not reflect any regulatory scrutiny.

This lack of verification aligns with concerns raised by Devangshu Dutta, Founder of business consulting firm Third Eyesight. He told MediaNama that self-declarations “do not change things much” when regulators do not audit submissions or impose consequences.

Further, Dutta remarked that most companies comply at the minimum level required if their claims are not examined and are not made public in full. According to him, revenue-driving design choices such as forced add-ons, confusing checkout flows or misleading scarcity claims will not be voluntarily removed sans oversight.

What Independent Evidence Shows

LocalCircles’ latest audit presents a sharply different picture from the companies’ filings. The organisation found that 21 of the 26 platforms that submitted “dark pattern free” declarations still use one or more manipulative design practices. The assessment relied on feedback from more than 250,000 consumers across 392 districts along with AI-assisted testing.

The most common violations include forced action, subscription traps, bait and switch, basket sneaking, interface interference and disguised advertisements. In practice, these dark patterns respectively mean that users are pushed into steps they did not choose, face hidden or hard-to-cancel subscriptions, see offers change during checkout, encounter fees added at the last moment, get nudged toward platform-favoured choices, and come across ads that appear as regular listings.

LocalCircles also identified drip pricing (gradually adding mandatory fees during the checkout process) on 11 of the 26 companies, including Flipkart, Myntra, Cleartrip, MakeMyTrip, BigBasket, Zomato and Blinkit, among others. The organisation said that many platforms appear to misunderstand what qualifies as drip pricing, which has led to incomplete corrections.

Trust Can Erode Due To Gap Between Declarations And User Experience

Sachin Taparia, Founder of LocalCircles, said that the problem begins with the absence of any verification. “Our understanding is that CCPA is wanting that companies submit a self-declaration at the earliest. However, there is no cross checking of claims that is being done by the CCPA, and as a result the companies are not being as thorough with their dark-pattern detection and resolution,” he said.

Taparia added that discrepancies between declarations and user experience could harm trust. “LocalCircles has found dark patterns on 21 of the 26 platforms submitting self-declarations. If this exercise is not done with high accuracy, both platforms doing so and CCPA could see consumer trust being impacted,” he said.

Importantly, Dutta echoed this concern, saying that the absence of penalties or reputation-related consequences allows companies to self-declare compliance while keeping revenue-generating patterns intact. He described the current process as “more an administrative formality [rather] than a behaviour-changing regulatory tool”.

Why This Matters

The gap between self-declarations and independent audits in the true sense of the word brings the real enforcement question into focus. What should the next phase of regulation look like?

In this context, Dutta said that regulators need to move beyond self-certifications and mandate detailed user experience (UX) audit reports that map every user journey, including pop-ups, onboarding, search, checkout, cancellations and returns.

He explained that regulators should reinforce this by demanding substantive evidence instead of brief compliance letters. This evidence can include screenshots and screen recordings of key flows, version histories that show how an interface changed over time, and product design documents or A/B testing results that reveal why specific nudges were introduced. To explain, A/B testing is essentially a method for comparing two versions of something to see which one performs better.

Furthermore, Dutta noted that platforms already collect extensive data on user complaints and drop-off points, which can help identify harmful or confusing design choices. He also said that independent third-party attestations, similar to security or accessibility audits, can provide a credible external check and increase the cost of non-compliance.

Multiple Annual Audits For Apps that Change Interface Frequently

Notably, Dutta stressed that most dark pattern categories appear across e-commerce, quick commerce and Direct-to-Consumer (D2C) websites, which means regulators can create a baseline audit standard that works across sectors instead of relying on platform-specific interpretations. He also suggested that audits should occur at least once a year, and companies that frequently modify their interfaces may need to report two or three times annually.

The larger concern now is whether the CCPA plans to move toward such a structured framework. Without independent verification and clear audit expectations, companies can continue declaring compliance even when manipulative designs remain embedded in their interfaces.

(Published in Medianama)

admin

November 4, 2023

Faizan Haidar, Economic Times

4 November 2023

Some of the super-luxury brands that have opened stores at the recently inaugurated luxury mall, Jio World Plaza in Mumbai, have put in a condition that at least four top brands – such as Louis Vuitton, Gucci, Cartier, Burberry, Tiffany, Valentino, Bulgari, Zegna, Giorgio Armani and Bottega Veneta – should be present in the same complex, to ensure the position of their brands is not diluted.

ET has seen copies of the agreements between Reliance Industries, the owner of Jio World Centre, and five brands, accessed through data analytic firm CRE Matrix.

Reliance Industries and the brands did not respond to emails seeking comment till press time on Friday. Brands often have an exclusivity clause with the mall where they don’t want competing brands near their stores. However, in the high-end segment, to ensure a similar buyer profile, they want similar stores nearby. Jio World Plaza already meets the condition with several of these super-luxury brands having opened their outlets there.

“If at least four among the mentioned brands are not open within six months of us starting the operation, we should be entitled to a reduction of the licence fee by 25% for the period that this criteria remains unfulfilled,” Christian Dior Trading, which will operate Dior, has said in the agreement.

Dior will pay ₹21.56 lakh in monthly rent for a 3,317 sq ft space in the complex. Gucci has given a list of six luxury brands – Louis Vuitton, Dior, Cartier, Bulgari, Valentino and Burberry – and demanded that at least four have to be represented in the shopping centre.

Louis Vuitton, Cartier and Bulgari have also put in similar conditions. Most of them have kept the right to terminate the agreement after serving the notice for nine to 12 months.

“In the super-luxury segment, most of the brands complement each other and that is why they want the presence of these brands next to each other. Good mall developers also go with zoning of brands and don’t want to mix the super-luxury brands with the premium or mid to premium brands. As more luxury brands are contemplating India entry, we will see more luxury spaces coming up,” said Devangshu Dutta, founder of retail consulting firm Third Eyesight.

India only has a handful of malls that give space exclusively to super-luxury brands.