admin

June 12, 2026

Christina Moniz, Financial Express/Brand Wagon

12 June 2026

Legacy luggage brand VIP Industries is shedding some of its old baggage. The company, which manufactures Skybags and Aristocrat along with its flagship VIP range, has gone beyond cringey makeovers solely to attract Gen Z, and has embarked on a transformation journey that leverages its legacy to purvey a fresh range of offerings.

The company is modernising its digital presence and supply chain to catch up with competitors.

Managing director Atul Jain admits that the company has been a bit slow on the e-commerce front. It is reinventing its online store, while also making its products available across other e-commerce channels. “Quick commerce is becoming an important channel since there are several use occasions and segments within the luggage market. For instance, consumers often make last-minute purchases for a weekend trip via quick commerce. School bags and backpacks for kids, also great gifting options, are seeing good demand on these platforms,” he says

The company, which once dominated the ₹16,000 crore organised luggage market in India, saw a bit of a shakeup last year when the Piramal family sold 32% of its stake to a private equity firm. But it continues to be among the top three players in the category with a 29-30% market share. “Luggage plays the role of a traveller’s companion. We are creating designs to fit that role,” says Jain. “For example, our new VIP suitcases have a coffee cup holder and our cabin trolley bag has an easy access compartment for devices like laptops and iPads.”

The transformation goes beyond the product. VIP’s 350 exclusive physical retail touchpoints in the country are being revamped to offer a new customer experience.

Unpacking opportunities

Overits 55 years, VIP has grown from a briefcase brand into Asia’s largest luggage maker, housing labels like Skybags, Aristocrat, and Carlton (premium segment). While VIP is a premium offering targeted at business and travellers, its Aristocrat brand operates in the mass market and the budget-friendly Alfa targets consumers who typically shop in the unbranded segment. Aristocrat and Alfa together contributed upwards of 40% to the company’s revenue in FY25, followed by Skybags (28%) and VIP (20%).

Like many legacy brands, the VIP Industries’ faces the challenge to ia, stay relevant among Gen Z buyers as a plethora of digital-first brands swamp the market. “VIP has lost ground on relevance and desirability to a generation for whom luggage, like sneakers, is an expression of identity. To them, VIP feels like their parents’ brand,” says Nisha Sampath, managing partner, Bright Angles Consulting. D2C players in the category operate in the business of “lifestyle accessories” and not for “luggage” per se, she points out.

With a design-forward approach, incorporating features like compression systems, silent wheels and charging ports, these new-age brands have embedded themselves in travel “culture”, while also being Instagram worthy, say experts.

Jain says Skybags is VIP’s Gen Z focussed brand, which has over 8,20,000 Instagram followers. “We are sharpening our positioning for Skybags in our design, advertising and marketing outreach, especially on social platforms. The brand has a clear differentiation with youthful colours and prints to attract younger consumers,” he adds.

While D2C players have seen notable growth in recent years, they don’t have the kind of trust and brand equity that VIP has cultivated across its brands, nor do they have the scale or revenue that legacy brands have, he says.

Experts believe there is a significant growth opportunity for legacy players given that the unbranded market still accounts for ₹13,000-14,000 crore. The important lever for legacy brands is to clearly demonstrate value beyond price. “The unorganised market competes heavily on affordability, so organised players need to communicate durability, warranty, after-sales service, and consistent quality – areas where they have a strong inherent advantage over unorganised alternatives,” says Praveen Govindu, partner at Deloitte India. He adds that these brands should also invest in advertising and communicate this value to the end consumer.

Not only are the needs different among different consumer groups, competitive pressures are also diverse. “VIP can segment the market more cleanly with its portfolio of brands if it maintains absolute distinction to ensure clear consumer targeting across not just product attributes and pricing, but also communication and channels,” says Devangshu Dutta, CEO, Third Eyesight.

(Published in Financial Express)

admin

May 27, 2026

Kartikey Kashyap, Financial Express

27 May 2026

Three campaigns took home the Grand Prix awards from Goafest this year: Kansai Nerolac Paints”The Barefoot Journey” by Tribes Commu-nication in the Media category; Mountain Dew’s “Darescore” by Leo in Digital & Technology; and Center fruit (Perfetti Van Melle India)” Kaisi Jeebh Laplapayee”” by Perfetti’s in-house team in the Best Use of Voice/Technology category.

All three were exceptionally creative and scored high on likeability and novelty. There was another common element that tied the three together: How they used creativity to solve real brand problems.

Take PepsiCo’s Mountain Dew Darescore campaign. Nepal’s tourism economy relies heavily on mountaineering, but over 90% of global tourist revenue flows into Mount Everest. As a result, there is overcrowding on Everest, starving the country’s other formidable peaks of income and attention.

Enter Mountain Dew. In partner-ships with the Nepal Tourism Board and the Discovery Channel, the brand built the world’s first algorithmic mountain grading system. Leo aggregated decades of expedition records, terrain complexity maps, seasonal weather hazards, rescue failure rates, and first-hand Sherpa wisdom. They funneled these metrics into an engine and assigned a quantifiable “Dare Score” to individual peaks. This data visually demonstrated that height does not equal danger, giving climbers an scale to gauge terrain toughness.

The genius of the campaign was its consumer utility. Mountain Dew printed smart QR codes on millions of its beverage bottles. When a user scanned the bottle, it unlocked an immersive digital hub, where users could simulate climbs, map out route plans, read real-time weather conditions, and submit expedition inquiries. The campaign took Mountain Dew’s slogan, “Darr Ke Aage Jeet Hai” and algorithmically decoded it for real-world application.

The result: It Swept Goafest 2026 and collected medals across vastly different categories including Integrated, Brand Experience, Social Content, and Video Craft, besides the Grand Prix. “Darescore is a powerful example of how brands are moving from storytelling to measurable participation. For decades, adventure culture celebrated only the final summit. This campaign changed the lens, it quantified courage itself,” says Prabhakar Mundkur, director, advertising & media, Percept. “What made this Grand Prix-worthy was the fusion of technology, gaming logic, data and brand philosophy into one seamless experience.”

If the Darescore campaign embedded data into storytelling, Nerolac chose to stay away from the beaten path. Its “Barefoot Journey” was a hyper-local activation designed by Tribes Communication for Nerolac Perma NoHeat, an acrylic-based, heat-reflective exterior coating. The campaign focused entirely on real-world product performance.

Every summer devotees visit various religious sites and walk barefoot along sweltering walkways or wait in queues on hot concrete floors.

Along with local authorities, the teams coated thewalkways of several high-footfall temples across south-ern India with Nerolac Perma NoHeat paint. The paint reduced the surface temperature of the pathways by up to 15°C offering relief to devotees.

This campaign won the jury over with its simplicity. According to Devangshu Dutta, founder & CEO, Third Eyesight, “Though the campaign might target a small audience, it made an impact by shifting the frame,” Dutta points out. “The campaign turned advertising into lived experience,” Mundkur says. “People didn’t just hear a claim, they felt it. This is media not as interruption, but as empathy.”

For its part, Centre fruit brought back its hoary “Kaisi Jeebh Lapla-payee” tagline using generative AI. Teaming up with WPP, BharatGPT.ai and Google Cloud, Perfetti created voice-based GenAl interactions in local dialects that turned feature phones smart. “What made the experience special was that it felt less like advertising and more like a conversation,” says Gunjan Khetan, director marketing, Perfetti Van Melle. Al was an enabler of accessibility and a tool to build cultural relevance, Khetan adds. “The brilliance lay in how it con-verted a simple sensory reaction -the uncontrollable craving triggered by taste – into a scalable interactive idea. It was playful, memorable and unmistakably Indian. More importantly, it proved that consistency in -brand codes, when combined with fresh execution, can become a formidable creative asset,” Mundkur says.

There you have it. Winning creative awards is validating, but solving the client’s problems through that creativity remains the bellringer.

(Published in Financial Express)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

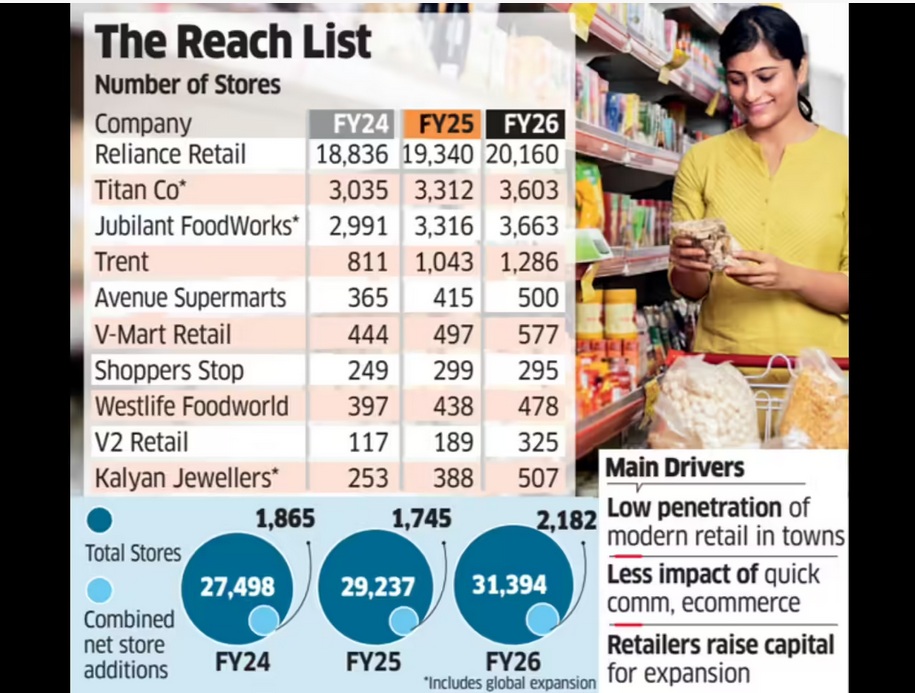

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.