admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

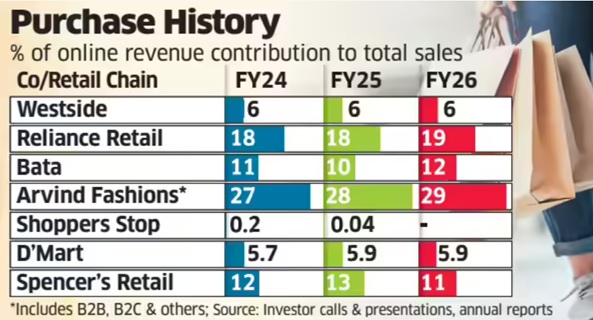

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

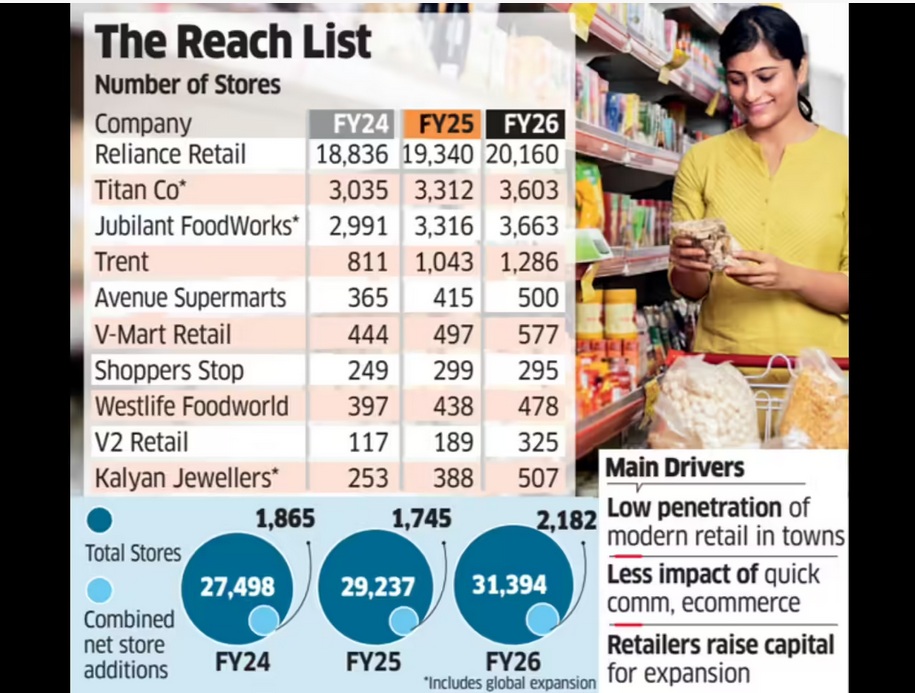

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

May 6, 2026

Vaeshnavi Kasthuril, MINT

Mumbai, 6 May 2026

Fashion retailers are speeding up deliveries to keep pace with instant-gratification shopping driven by quick-fashion startups, with established players and newer brands taking sharply different approaches.

For example, brands such as Biba and The House of Rare have adopted a more calibrated, infrastructure-led strategy rather than a rapid overhaul of existing store networks. “We’ve been doing this in a very soft way but not necessarily from the same stores because that affects the customer experience,” said Siddharth Bindra, managing director of Biba. Bindra said using retail stores as fulfilment hubs for rapid delivery creates operational constraints, particularly given store sizes and layouts. “We don’t have very large stores; they are anywhere between 1,000 and 2,000 square feet. So that’s not the right efficiency,” he said.

Instead, the brand is evaluating a hub-based model in cities with higher store density, enabling faster deliveries without disrupting stone operations. “If we do, it will be though proper hubs in cities where we have four to five stores, where we would start with quick commerce and accelerate it,” he said. This could enable same-day or two to three-hour deliveries.

The House of Rare, which houses Rare Rabbit (men’s urban fashion) and Rareism (women’s fashion), is adopting a similar approach, evaluating city-levee fulfilment hubs in markets with higher store concentrations to enable faster deliveries while keeping retail outlets focused on walk-in consumers.

The strategy reflects a broader attempt among legacy retallers to belance speed with experience, rather than treating stores as Interchangeable logistics nodes. “The eventual goal is the customer, but it creates a lot of difference in the customer experience” Bindra said, pointing to the trade-offs involved.

Different take

In contrast, some brands are moving more aggressively to integrate stones directly into fulfilment networks.

Libas, an initial public offering (IPO)-bound apparel company, is networking its operating model to plug its physical retail network Into a faster, hyperlocal delivery system.

Earlier, the 12-year-old company followed a more traditional structure. Online orders were largely fulfilled from central warehouses and delivered over a few days, while stores primarily served walk-in customers, with the two channels operating independently.

That is now changing. Libas is using its stores and nearby warehouses as local fulfilment points, allowing it to service orders within a much smaller delivery radius,

“At Libas, the time frame will be approximately 60-90 minutes at the max,” said Bhavay Pruthi, senior vice president, e-commerce and product management.

The rollout has been gradual, starting with select cities and limited catchments, typically within a 7-10km radius, where delivery timelines can be tightly controlled. It has also narrowed the product mix initialy to itams that are easier to move quickly.

The push comes as consumer expectations around delivery timelines extend beyond groceries into fashion, forcing brands to rethink supply-chain design,

Rise of quick fashion

The urgency to adapt is being shaped by a surge in quick fashion startups that are attracting investor attention despite heavy cash burm.

The segment has seen a flurry of funding in recent months, with Zilo raising $15.3 million in February led by Peak XV, and Knot securing $5 million in a round led by 12 Flags in December.

It has also evolved rapidly. Quick-commerce platforms such as Zepto, Instamart and Blinkit initially offered a limited range of basic fashion items for last-minute purchases. This has since expanded into a more specialized category, with vertical players offering wider assortments across party, work and occasion wear with rapid delivery timelines.

New entrants are pushing the model further. Wydo, for instance, promises deliveries within 15 to 30 minutes in Bengaluru, while Gen Z-focused offerings such as Newme’s Zip and Snitch Quick are building businesses around near-instant fashion access.

Myntra’s rapid commerce division, M-Now, accounted for about 10% of orders in the locations where it was available as of last November.

“This is the new kind of experience that customers are expecting,” Pruthi said.

Libas is working with third-party logistics providers and quick commerce platforms for the last-mile delivery, while focusing internally on faster picking, packing and order routing. Quick commerce currently accounts for about 2% of its overall sales, with scope to grow as the model scales..

Early results, however, highlight the trade-offs. “We saw very good sell-throughs for e-commerce, but it was cannibalizing existing store sales,” Pruths said.

There are also fimits to what customers are willing to buy through rapid-delivery channels. “Customers do not have the confidence to spend 15,000 for a fashion product from a quick- commerce channel,” he said.

To address this, Libas has tightened delivery radii, curated a more suitable product mix, and is testing stores with attached dark-store infrastructure to balance walk-in and online demand.

Experts say these challenges are structural.

“If you look at fashion, it’s extremely unpredictable, and if you are a brand across multiple products, it’s complicated process,” said Devangshu Dutta, founder of management consulting firm Third Eyesight.

While demand for faster deliveries is rising, it remains a small slice of the overall market, with profitability still uncertain due to limited assortments and high fulfilment costs. For traditional retailers, adopting the model requires a fundamental reworking of supply chains that were not built for near-instant delivery, Dutta added.

(Published in MINT)

admin

February 16, 2026

Christina Moniz, Financial Express (Brand Wagon)

16 February 2026

Starting this month global sportswear maker Nike shifted its e-commerce operations to beauty and fashion marketplace Nykaa to address poor logistics, high delivery times and inventory niggles. With Nykaa in charge, the brand said, customers can expect free shipping on all orders and faster deliveries rang ing from twotofour days depending on the location.

The change comes at a time when Nike is struggling to cope with declining market share and operational and supply-side issues in India. Its physical store count in the country has dropped by half in the past ten years to 100 from over 200 a decade ago. Nike in India undertook major restructuring of its business between 2016 and 2019, closing 35% of its stores in those three years to take a more digital-first approach.

It’s not all doom and gloom though. The brand reported a 14% growth in sales in the fiscal ending March 2025 to clock ₹1,380 crore. But it is well behind competing brands such as Puma (₹3,274 crore) and Adidas (₹3,114 crore), both of which have over 400 stores across the country.

Given India’s size, the competitive landscape and potential, treating it as a secondary export market to be serviced from Singapore was a poor decision on Nike’s part, says Devangshu Dutta, founder and CEO, Third Eyesight.

Nike’s alignment with a local player offers important strategic lessons for global brands with big ambitions in India, especially those in the ₹8,800 crore sportswear market. Brands that have not treated India as an afterthought have succeeded in creating sustained growth and market leadership, says Dutta.

“Most of Nike’s global competitors have treated India as a market high consequence. Nike might be the leader by global revenues, in India is smaller than its global rivals like Adidas, Puma and Skechers. ASICS has a smaller base but is growing at 30% while Lotto is also looking to grow its footprint massively, observes Dutta.

Ever since Nike’s digital-first pivot, its customers in the country have raised several complaints citing delivery failures and poor service, with some deliveries reportedly taking weeks. Its decision to transfer its digital operations to Nykaa in India could potentially address these missteps and reverse the breakdown of customer experience, say experts.

Changing course

“The recent move feels like Nike acknowledging that India cannot be treated as an extension of a global system. It needs local infrastructure, local partners, and a model built specifically for how Indians shop online. Partnering with Nykaa brings local execution muscle that is hard to replicate quickly,” observes Tusharr Kumar, CEO, Only Much Louder, adding that the move is a maturity moment for global brands. “Scale alone doesn’t guarantee success. What matters is adapting to local consumer behaviour, logistical realities and service expectations,” says Kumar.

That said, Nike’s shift won’t be without challenges. The biggest one will be balancing scale with brand control, notes Yasin Hamidani, director, Media Care Brand Solutions. “While Nykaa offers strong reach and trust, Nike will need to ensure its premium positioning, product storytelling, and customer experience don’t get diluted. If managed well, this move doesn’t necessarily hurt Nike’s brand,” he states.

However, he adds that competition like Adidas and Puma, with stronger on-ground retail and omnichannel presence, may gain an edge if Nike’s visibility or momentum slows. “The partnership with Nykaa must feel strategic and not like a retreat,” he cautions.

Given that Nykaa is also a marketplace for other activewear brands, it remains to be seen how the platform maintains Nike’s premium customer experience. “On its own platform, Nike could control everything from storytelling to checkout flows and post-purchase engagement. Nike will now need to adjust to sharing customer data, promotional calendars, and operational priorities with a partner platform,” says Somdutta Singh, founder & CEO at Assiduus Global, adding that striking the right balance between leveraging Nykaa’s scale and maintaining Nike’s distinctiveness will be key.

(Published in Financial Express – Brandwagon)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.