admin

February 16, 2026

Christina Moniz, Financial Express (Brand Wagon)

16 February 2026

Starting this month global sportswear maker Nike shifted its e-commerce operations to beauty and fashion marketplace Nykaa to address poor logistics, high delivery times and inventory niggles. With Nykaa in charge, the brand said, customers can expect free shipping on all orders and faster deliveries rang ing from twotofour days depending on the location.

The change comes at a time when Nike is struggling to cope with declining market share and operational and supply-side issues in India. Its physical store count in the country has dropped by half in the past ten years to 100 from over 200 a decade ago. Nike in India undertook major restructuring of its business between 2016 and 2019, closing 35% of its stores in those three years to take a more digital-first approach.

It’s not all doom and gloom though. The brand reported a 14% growth in sales in the fiscal ending March 2025 to clock ₹1,380 crore. But it is well behind competing brands such as Puma (₹3,274 crore) and Adidas (₹3,114 crore), both of which have over 400 stores across the country.

Given India’s size, the competitive landscape and potential, treating it as a secondary export market to be serviced from Singapore was a poor decision on Nike’s part, says Devangshu Dutta, founder and CEO, Third Eyesight.

Nike’s alignment with a local player offers important strategic lessons for global brands with big ambitions in India, especially those in the ₹8,800 crore sportswear market. Brands that have not treated India as an afterthought have succeeded in creating sustained growth and market leadership, says Dutta.

“Most of Nike’s global competitors have treated India as a market high consequence. Nike might be the leader by global revenues, in India is smaller than its global rivals like Adidas, Puma and Skechers. ASICS has a smaller base but is growing at 30% while Lotto is also looking to grow its footprint massively, observes Dutta.

Ever since Nike’s digital-first pivot, its customers in the country have raised several complaints citing delivery failures and poor service, with some deliveries reportedly taking weeks. Its decision to transfer its digital operations to Nykaa in India could potentially address these missteps and reverse the breakdown of customer experience, say experts.

Changing course

“The recent move feels like Nike acknowledging that India cannot be treated as an extension of a global system. It needs local infrastructure, local partners, and a model built specifically for how Indians shop online. Partnering with Nykaa brings local execution muscle that is hard to replicate quickly,” observes Tusharr Kumar, CEO, Only Much Louder, adding that the move is a maturity moment for global brands. “Scale alone doesn’t guarantee success. What matters is adapting to local consumer behaviour, logistical realities and service expectations,” says Kumar.

That said, Nike’s shift won’t be without challenges. The biggest one will be balancing scale with brand control, notes Yasin Hamidani, director, Media Care Brand Solutions. “While Nykaa offers strong reach and trust, Nike will need to ensure its premium positioning, product storytelling, and customer experience don’t get diluted. If managed well, this move doesn’t necessarily hurt Nike’s brand,” he states.

However, he adds that competition like Adidas and Puma, with stronger on-ground retail and omnichannel presence, may gain an edge if Nike’s visibility or momentum slows. “The partnership with Nykaa must feel strategic and not like a retreat,” he cautions.

Given that Nykaa is also a marketplace for other activewear brands, it remains to be seen how the platform maintains Nike’s premium customer experience. “On its own platform, Nike could control everything from storytelling to checkout flows and post-purchase engagement. Nike will now need to adjust to sharing customer data, promotional calendars, and operational priorities with a partner platform,” says Somdutta Singh, founder & CEO at Assiduus Global, adding that striking the right balance between leveraging Nykaa’s scale and maintaining Nike’s distinctiveness will be key.

(Published in Financial Express – Brandwagon)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

February 12, 2026

Vaeshnavi Kasthuril, Mint

Bengaluru, 6 February 2026

Global fragrance maker Bath & Body Works Inc. is betting on a reset to revive growth after years of heavy discounting and weak product innovation dulled its brand momentum across markets. The Columbus, Ohio-based retailer is pivoting to a “consumer-first” formula strategy centered around upgraded formulations, more disciplined marketing, and fewer promotions.

The reset matters as India is emerging as one of the company’s fastest-growing and best-performing markets and is also becoming a testing ground for how the brand evolves its retail model. India now ranks among Bath & Body Works’ top five international markets by growth.

“We’re seeing strong engagement across stores (in India), digital marketplaces and even quick commerce, which gives us confidence as we evolve the brand and introduce more innovation,” said Tony Garrison, global vice president at Bath & Body Works, in an interview with Mint.

The fragrance maker entered India in 2018 in partnership with Dubai-based Apparel Group and has since expanded to about 50 stores across major metros, while also building an online presence through platforms such as Nykaa, Myntra, and Amazon. Apparel Group brings over 80 global brands to India, including Victoria’s Secret, Charles & Keith, Aldo, Crocs, and Tim Hortons.

“We’re learning a lot from how the Indian consumer shops across platforms, especially the speed and convenience expectations,” Garrison said. “It’s helping us think differently about assortment, pack sizes and how we show up digitally”.

Even as discretionary spending softened, the brand’s franchise partner, Apparel Group, delivered double-digit sales growth in India and high single-digit comparable store gains in FY25. It reported a 26% year-on-year jump in FY25 revenue to ₹1,118 crore and a net profit of ₹20.5 crore, reversing a loss in the previous year.

Globally, Bath & Body Works’ earnings reflect soft consumer demand as well as margin pressures. Its revenue declined 1% to $1.59 billion in the third quarter of FY25, while net income fell 27% year-on-year to $577 million.

Reviving the fragrance engine

While legacy scents such as Japanese Cherry Blossom, Champagne Toast, and Thousand Wishes remain global blockbusters, the company admits it hasn’t produced enough new hits at a similar scale in recent years. Japanese Cherry Blossom is a $250 million fragrance.

“I think we haven’t done the best job of keeping up with some of the fragrance trends. We haven’t done a lot of innovation, and that’s what you’re going to see this year. This is a big change year for us,” Garrison said.

The company plans to elevate its home fragrance portfolio, bringing in more premium candle collections, gift-ready packaging, and deeper, more sophisticated scent profiles. The broader goal is to encourage shoppers to trade up within the brand rather than wait for markdowns. “We want customers to see the value in the product itself… not just the promotion,” Garrison said.

New retail formats

To test new retail formats, the company and Apparel Group plan to pilot a small “neighbourhood store” format of roughly 500 square feet in select non-metro markets later this year. These stores will focus heavily on core body care lines and hero fragrances, while creating a more discovery-led environment for first-time shoppers.

India is also emerging as a key market in testing how far premiumisation can go. Garrison noted that the company has not seen a slowdown locally: “India has actually been one of our strongest markets in the post-Covid period. Even when consumers are careful, they still spend on small luxuries that make them feel good”.

What experts say

Retail experts caution that the reset in India won’t be without challenges. Devangshu Dutta, founder of Third Eyesight, noted that brands often fall back on discounting when volumes don’t come through. He added that the personal care market has become intensely crowded, making brand clarity critical.

While the brand is leaning into quick commerce and smaller stores, Dutta cautioned that premium brands still need larger formats to build experience-led differentiation. “Neighbourhood stores can be spokes, but you still need the hub—the large store—to communicate the brand experience,” he said.

Race Intensifies

The turnaround plan comes at a time when rivals, including The Body Shop and Forest Essentials, are also vying for the Indian consumer’s wallet. The Body Shop plans to achieve ₹1,100 crore in revenue in India within the next three to five years. India’s fragrance market was valued at $1.0 billion in 2024 and is projected to grow at a 13.9% CAGR to $3.23 billion by 2033.

(Published in Mint)

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

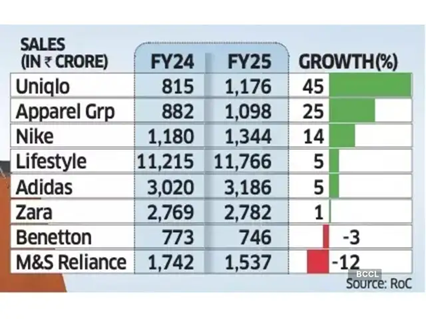

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

September 24, 2025

Shabori Das & Sagar Malviya, Economic Times

Bengaluru/Mumbai, 24 September 2025

Chinese fast-fashion platform Shein plans to triple the number of launches in India and shrink its design-to-launch timeline by a third to deepen its push into an increasingly competitive market, a top official said.

The company, which re-entered India through a partnership with Reliance Retail in February this year, said it is overhauling its supply chain to enable faster turnaround times. To achieve this, it has moved away from large-scale manufacturing hubs to smaller production lines with each line focused on creating a single new design daily.

“Our current timelines, measured from ‘thought to site’, stand at 46 days. We are targeting 30 days,” said Vineeth Nair, chief executive of Reliance’s fashion platform Ajio that steers Shein in India. “We currently deliver 320 styles a day – about 10,000 a month – and plan to scale that to over 30,000 styles monthly in the coming months,” he told ET.

Speaking about the speed of manufacturing, Nair said, “We quantify our options in terms of production lines, with each line optimised to deliver one design option per day, rather than factories. Some of our large production units have been repurposed into multiple lines.”

Shein first launched in India in 2018 with its own online shop. However, the app was banned by the Ministry of Electronics and Information Technology (MeitY) along with TikTok, WeChat and over 55 other Chinese apps.

One of the primary issues and controversies surrounding Shein’s India operations was the use of the consumer data by the Chinese apparel retailer.

Under the current partnership model, Reliance Retail is operating Shein under licensing agreement and ensures complete customer data ownership as per the company.

Unlike international markets, Shein India products are made in India.

“It’s still early days – just about three months since we introduced Shein to the India Gen Z,” Nair said. “And we are still in the process of adding multiple products, which we intend to do in the next few months.”

He said the brand is witnessing two million daily average users, dominated by 21-year-old women who account for 62% of the traffic.

Shein, the world’s biggest ecommerce-centred fashion retailer, however, may find it hard to replicate its global success in India, according to Devangshu Dutta, founder of retail consulting firm Third Eyesight.

“Shein’s edge internationally has been its speed of dropping its products, and the width of its product category. The India model is not the same. The India model of fashion is slower, and the product category width is not as large,” he noted. “Hence, the brand will in all probability end up competing with the already established market like Myntra, Zudio and the likes.”

(Published in Economic Times)