admin

July 13, 2026

Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT)

Bengaluru, 13 July 2026

India’s vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means.

For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives.

Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint the company would rather optimise for “quality selection” than chase ultra-fast deliveries, arguing that customers today are looking for reliable availability and curated choices rather than insisting on receiving products in 10 minutes.

Lightspeed-backed fashion startup Slikk is pursuing a similar path. Founder Akshay Gulati said the company’s focus since inception has been building a wide catalogue rather than aggressively acquiring users.

The shift comes as the sector enters a more pragmatic phase. Quick fashion startup Blip shut down within a year of launch last June, while rival Klydo has recently pivoted its business model, raising questions about the viability of firms in every category.

The crop of vertical quick commerce startups—focused on rapid delivery within a single, specific product category—has largely emerged over the past two years, inspired by the explosive growth of grocery-focused pioneers such as Blinkit, Swiggy Instamart and IPO-bound Zepto, which have accustomed consumers to receiving groceries and everyday essentials within minutes.

Other prominent startups include Plazza for quick delivery of medicines, Instafix for mobile repairs within minutes, and Dazzl for at-home salon services.

Kalaari Capital noted in its 2025 report that quick commerce had already captured about two-thirds of online grocery orders and around 10% of India’s overall e-retail spending in 2024, transforming consumer behaviour and building the infrastructure for specialised vertical players to emerge.

“Speed was never a real moat but became a hygiene factor once every significant player could promise 10-30 minute delivery,” said Devangshu Dutta, founder and chief executive of consultancy Third Eyesight. “Assortment depth, availability, trust, and sustained price-value have been, and will remain, the true differentiation levers. For categories such as medicines and baby products, credibility and compliance outweigh saved minutes, apart from urgent purchases.”

“Unit economics can become healthier only where there’s a clear reason for frequent and repeated purchases. Groceries and medicines are repeat, low consideration categories, while fashion is high consideration, driven by fit, styling and browsing. The best quick commerce categories have low or no returns and high order frequency, whereas rapid fashion delivery faces high return rates due to product mismatch against customer expectations (sizing, fit, fabric and colour),” Dutta said.

Different categories, different playbooks

While fashion startups are investing heavily in discovery and inventory refreshes, Ozi believes the opportunity in baby care lies in curation and premiumisation.

Sah said each sub-category within baby care presents a different operational challenge. Consumables require deep availability of long-tail brands, while fashion depends on filtering products for quality rather than listing everything available. Ozi, which delivers wipes, diapers, and baby food, deliberately curates brands instead of maximising assortment, targeting parents willing to pay slightly more for trusted products.

“The customer behaviour has shifted from discovery first to search first,” Sah said, adding that shoppers today are not necessarily looking for ultra-fast delivery, but nor are they willing to wait several days. “A modern-age customer values quality. They are happy to pay an 8-10% or 12% differential, but they need quicker access to better brands and better assortment.”

Fashion startups argue that their challenge is different altogether.

Gulati said Slikk has built its business around supply rather than customer acquisition, claiming that stronger assortment has helped steadily reduce acquisition costs. The company replaces 30-40% of inventory in every dark store each month and is expanding neighbourhood by neighbourhood instead of spreading rapidly across cities.

Slikk might also consider introducing private brands for apparel, given their higher margins, Gulati said.

Bengaluru-based fast-fashion e-commerce startup Knot, which raised $5 million from 12 Flags and Kae Capital in December 2025, is investing heavily in back-end technology. Its app captures user preferences through swipe-based interactions, while its dark stores carry much wider assortments than horizontal quick commerce operators – offering a vast, multi-category collection of goods – and customise inventory based on local demand.

“We look at fashion as a data science problem and not really an intuition problem,” co-founder and chief executive officer (CEO) Archit Nanda said.

Nanda said fashion’s long-tail nature—which relies on selling small quantities of several unique products rather than depending on a few popular items – means inventory commonality across dark stores is significantly lower than grocery, requiring specialised supply chains and hyperlocal merchandising.

The profitability test

The changing strategies also reflect growing investor scrutiny of unit economics.

Slikk’s Gulati said investors continue to back the category but increasingly want proof that businesses can balance growth with profitability rather than relying on heavy customer acquisition spending. He believes execution in neighbourhood-level operations, assortment and brand partnerships will ultimately determine the winner.

Knot’s Nanda said that fashion combines high average order values with healthy margins, making the category attractive despite its complexity.

However, analysts believe that not every vertical is equally suited to the model.

“Looking ahead, horizontal cross-subsidy will work better, with established, well-capitalised players (Myntra’s M-Now, Nykaa Now) including quick delivery into an existing catalogue and logistics network rather than building it standalone. For narrow, high-trust verticals (medicines, baby care) where the value is availability and authenticity rather than impulse, and where margins can support the delivery cost, quick commerce can work,” Dutta noted.

Kalaari Capital’s 2025 report on vertical quick commerce similarly argued that specialised players will win by solving category-specific pain points, with assortment depth, customer experience, and category expertise emerging as key differentiators.

(Published in MINT)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

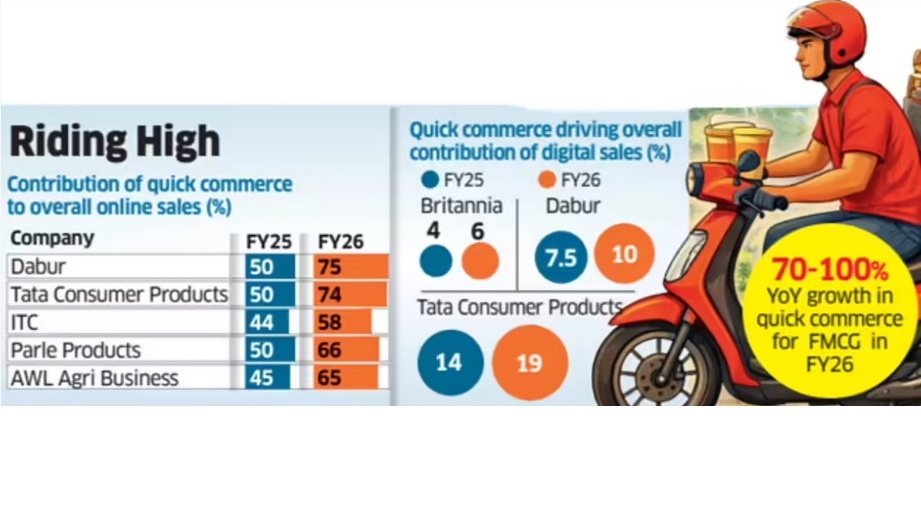

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

February 12, 2026

Vaeshnavi Kasthuril, Mint

Bengaluru, 6 February 2026

Global fragrance maker Bath & Body Works Inc. is betting on a reset to revive growth after years of heavy discounting and weak product innovation dulled its brand momentum across markets. The Columbus, Ohio-based retailer is pivoting to a “consumer-first” formula strategy centered around upgraded formulations, more disciplined marketing, and fewer promotions.

The reset matters as India is emerging as one of the company’s fastest-growing and best-performing markets and is also becoming a testing ground for how the brand evolves its retail model. India now ranks among Bath & Body Works’ top five international markets by growth.

“We’re seeing strong engagement across stores (in India), digital marketplaces and even quick commerce, which gives us confidence as we evolve the brand and introduce more innovation,” said Tony Garrison, global vice president at Bath & Body Works, in an interview with Mint.

The fragrance maker entered India in 2018 in partnership with Dubai-based Apparel Group and has since expanded to about 50 stores across major metros, while also building an online presence through platforms such as Nykaa, Myntra, and Amazon. Apparel Group brings over 80 global brands to India, including Victoria’s Secret, Charles & Keith, Aldo, Crocs, and Tim Hortons.

“We’re learning a lot from how the Indian consumer shops across platforms, especially the speed and convenience expectations,” Garrison said. “It’s helping us think differently about assortment, pack sizes and how we show up digitally”.

Even as discretionary spending softened, the brand’s franchise partner, Apparel Group, delivered double-digit sales growth in India and high single-digit comparable store gains in FY25. It reported a 26% year-on-year jump in FY25 revenue to ₹1,118 crore and a net profit of ₹20.5 crore, reversing a loss in the previous year.

Globally, Bath & Body Works’ earnings reflect soft consumer demand as well as margin pressures. Its revenue declined 1% to $1.59 billion in the third quarter of FY25, while net income fell 27% year-on-year to $577 million.

Reviving the fragrance engine

While legacy scents such as Japanese Cherry Blossom, Champagne Toast, and Thousand Wishes remain global blockbusters, the company admits it hasn’t produced enough new hits at a similar scale in recent years. Japanese Cherry Blossom is a $250 million fragrance.

“I think we haven’t done the best job of keeping up with some of the fragrance trends. We haven’t done a lot of innovation, and that’s what you’re going to see this year. This is a big change year for us,” Garrison said.

The company plans to elevate its home fragrance portfolio, bringing in more premium candle collections, gift-ready packaging, and deeper, more sophisticated scent profiles. The broader goal is to encourage shoppers to trade up within the brand rather than wait for markdowns. “We want customers to see the value in the product itself… not just the promotion,” Garrison said.

New retail formats

To test new retail formats, the company and Apparel Group plan to pilot a small “neighbourhood store” format of roughly 500 square feet in select non-metro markets later this year. These stores will focus heavily on core body care lines and hero fragrances, while creating a more discovery-led environment for first-time shoppers.

India is also emerging as a key market in testing how far premiumisation can go. Garrison noted that the company has not seen a slowdown locally: “India has actually been one of our strongest markets in the post-Covid period. Even when consumers are careful, they still spend on small luxuries that make them feel good”.

What experts say

Retail experts caution that the reset in India won’t be without challenges. Devangshu Dutta, founder of Third Eyesight, noted that brands often fall back on discounting when volumes don’t come through. He added that the personal care market has become intensely crowded, making brand clarity critical.

While the brand is leaning into quick commerce and smaller stores, Dutta cautioned that premium brands still need larger formats to build experience-led differentiation. “Neighbourhood stores can be spokes, but you still need the hub—the large store—to communicate the brand experience,” he said.

Race Intensifies

The turnaround plan comes at a time when rivals, including The Body Shop and Forest Essentials, are also vying for the Indian consumer’s wallet. The Body Shop plans to achieve ₹1,100 crore in revenue in India within the next three to five years. India’s fragrance market was valued at $1.0 billion in 2024 and is projected to grow at a 13.9% CAGR to $3.23 billion by 2033.

(Published in Mint)

admin

February 2, 2026

Sakshi Sadashiv, MINT

Bengaluru, 02 Feb 2026

BRND.ME, a roll-up commerce company, expects to complete its reverse flip (change of headquarters) from Singapore to India by March, clearing a key regulatory hurdle as it prepares to tap Indian public markets with an IPO.

Despite the rise of private labels from quick-commerce giants such as Swiggy Instamart and Zepto, CEO Ananth Narayanan remains confident. He argues that BRND.ME’s core categories—spanning complex, value-added products such as specialized haircare and niche party supplies—possess a level of brand loyalty and complexity that is difficult for generic retail labels to replicate. While private labels are currently displacing national brands in high-frequency, simple categories like dairy and staples, Narayanan believes the company’s core categories remain protected from this encroachment as they drive searches.

Having shifted its strategy from aggressive acquisitions to organic scaling, the company is now doubling down on its four largest brands: MyFitness (peanut butter), Botanic Hearth (haircare), Majestic Pure (aromatherapy), and PartyPropz (celebration supplies).

About 10-15% of BRND.ME’s India business currently comes from quick commerce, a channel the company plans to scale, Narayanan said. The company is the leader in party supplies on quick-commerce platforms, benefiting from impulse-driven demand. “People forget birthdays and anniversaries, so it’s a classic category to build a brand on quick commerce,” he said. The category contributes about ₹200 crore of revenue. The company also leads the peanut butter category through MyFitness, with a 30% market share on all quick commerce platforms and annual revenue of ₹270 crore.

The company’s revenue run rate stands at about $200 million. Male consumers worried about male-pattern baldness now account for about 35% of haircare sales. The company aims for a 10-fold jump in aromatherapy and haircare sales from $6 million to $60 million within four years, led by Majestic Pure and Botanic Hearth.

Drawing on his experience running Myntra, Narayanan said that private labels typically have a ceiling. “Even when we pushed hard on private labels at Myntra, they never went beyond 25-30% of the overall portfolio. That tends to remain the case as the categories we operate in are very hard to displace because we drive searches.”

This dynamic is already visible across several quick-commerce categories. The peanut butter segment is heavily consolidated on Blinkit, with Pintola and MyFitness together accounting for about 73% of sales, according to data from Datum Intelligence. Similar patterns have emerged in other categories. Blinkit’s popcorn segment, for instance, has rapidly consolidated into a duopoly, with 4700BC and Act II controlling 99% of sales.

Private labels muscling in

While Blinkit has consciously avoided launching private-label products on its platform, Swiggy has done so through Noice, and Zepto through Relish and Daily Good. For established brands, these private labels are becoming harder to ignore. Swiggy has scaled Noice aggressively, expanding the portfolio from about 200 to 350 stock keeping units (SKUs) and onboarding more manufacturing partners while moving beyond staples into categories such as beverages and ready-to-cook foods. These products are aimed at delivering significantly higher margins of 35-40%, compared with 10-15% on third-party brands, Mint reported earlier.

Private labels now contribute an estimated 6-8% of quick-commerce sales, up from 1-2% two years ago, according to data from 1digitalstack.ai, though penetration in perishables remains limited because of supply-chain complexity and quality concerns. A broader push into fresh categories could lift private-label share to 10-15%. Noice has already captured 3.4% of wafer sales and 1.9% of biscuit sales on the platform within months of its launch, according to 1digitalstack.ai data. The two categories are dominated by Lay’s and Britannia, which have a market share of about 35% each in their respective segments.

Zepto’s private-label push spans multiple everyday categories, including Relish for meat products, Daily Good for staples, Chyll for ice cubes and juices, and Aaha! for snacks, sweets, cereals and batters.

This growing presence creates a structural ‘trap’ for digital-first brands. Devangshu Dutta, chief executive at Third Eyesight, a consultancy firm, said, “Brands that are overly dependent on a single sales platform remain structurally vulnerable to being replaced by the platform’s own private labels, which are designed to capitalise on product opportunities that already have proven demand.” Platforms, he explained, tend to dominate high-frequency purchases, often undercutting brands on both price and visibility.

Persistently high online customer acquisition costs add to the pressure, particularly if the customer relationship is owned by the platform rather than the brand. “This has been one of the significant friction points for all digital-only brands, and weighs especially heavily on companies that have online-heavy portfolios with multiple brands in play,” Dutta added.

(Published in Mint)

admin

December 10, 2025

Shabori Das, ET Bureau

Dec 10, 2025

India’s social media platforms are powerful marketing tools but not yet retail destinations. Billions scroll and swipe daily, but few buy directly within apps. Unlike China, India faces regulatory hurdles and a lack of integrated payment systems.

A billion Indians scroll, swipe and double tap every day, but barely buy. Despite Instagram and Facebook Marketplace being in India for over a decade, social media here remains a showroom, not a store. Creators and D2C brands are hustling to convert attention into action, but the holy grail of in-app shopping where discovery, live streaming, and purchase happen seamlessly, remains out of reach.

The question is, what’s stopping India from becoming the next China or the US in social commerce?

Influence-to-Commerce Gap

Globally, social commerce is powered by influencers. In China, influencer Li Jiaqi reportedly sold products worth $2 billion on Singles’ Day on Alibaba’s online marketplace Taobao Live in 2021. Another popular influencer Zheng Xiang Xiang, with over 5 million followers on Douyin (the Chinese equivalent of TikTok), reportedly generated $18 million in sales in a week in 2023. These are numbers India’s creator economy can only dream of, for now.

To be clear, influencer marketing in India is booming. EY estimates the sector at over Rs 3,000 crore and yet, due to regulatory restrictions, social media platforms in India can’t host end-to-end transactions. What India has is content commerce, driven by players like Meesho and Myntra, not social commerce. Globally, social commerce is a $1-trillion market. China alone accounts for over $500 billion and the US, $100 billion. India’s share? Around $10 billion — despite being home to the world’s largest Gen Z population and the second-largest base of internet users after China.

What’s Holding India Back

“Just as quick commerce changed how India buys food, social commerce will change how we shop for fashion and lifestyle,” says Anand Ramanathan, partner, consumer industry leader, Deloitte South Asia.

The idea is simple: Social commerce enables an end-to-end purchase journey within a social media app. But in India, the final sale still happens elsewhere — typically on e-commerce platforms.

“In China, live streaming contributes nearly 20% of total e-commerce revenue. In India, it hasn’t taken off,” says Puneet Sehgal, CEO of D2C apparel brand Freakins. He believes in-app checkout could be transformative. “Our Gen Z audience spends over an hour daily on social media. If the purchase could happen right there, it’s one step less for the consumer — and one step closer to a sale.”

The China Contrast

China’s social commerce revolution was built on three forces — speed, scale and seamlessness. Influencer Zheng, for instance, showcases each product for barely three seconds and moves on. That brevity, combined with integrated payments, drives impulse buying at staggering volumes.

India’s influencer-driven commerce, by contrast, is still warming up. Projected to touch $ 55 billion by 2030, it remains largely limited to discovery and advertising.

The barriers aren’t technological, they’re regulatory. India’s payment rules require clear accountability and settlement tracking, making it difficult for global platforms to enable in-app sales. Meta’s 2023 policy shift also directed purchases off-platform, keeping Instagram and Facebook Marketplace confined to discovery and promotion, rather than purchase. For now, social media in India remains a potent marketing engine, not yet a retail destination.

Experiments and Exceptions

Some Indian players are testing new waters. Myntra’s Glamstream, launched this July, lets influencers host live sessions where viewers can “shop the look” in real time — though the final checkout still redirects you to the Myntra app.

“India’s creator economy influences over $300 billion in annual consumer spending,” says Sunder Balasubramanian, chief marketing officer at Myntra.“That could grow to $1 trillion in the next few years, making India one of the fastest-growing creator economies globally,” adds Lakshminarayan Swaminathan, vice president-product management, Myntra.

The potential is clear. In 2021, Taobao Live hosted a 12-hour live streamed sale with influencer Li Jiaqi in China that clocked $2 billion in presales and attracted 250 million viewers.

Closer home, Sujata Biswas, co-founder of Suta Sarees, recalls Instagram’s shortlived Shop Now feature. “We saw an immediate dip in transactions after it was withdrawn,” she says. “Fashion is about instant gratification. You see it, you want it and buy it right away.”

The D2C Advantage

India’s D2C market, valued at $87 billion as of 2025 by Deloitte, could be the biggest gainer if social commerce does take off. Most D2C brands currently pay 25–35% retailer margins to platforms like Myntra and Nykaa. Social commerce could let them bypass intermediaries and sell directly to their audiences.

“Anything that reduces friction between intent and purchase is gold,” says Sehgal. “If that entire journey — from watching to buying — happens within the same app, conversion rates would shoot up.”

Even so, social platforms come with their own costs. TikTok, for instance, charges promotional, marketplace and fulfilment fees. But for Indian D2C players, the larger hurdle isn’t cost — it’s access.

Open vs Closed Ecosystems

“India’s retail market is far more open than China’s,” explains Devangshu Dutta, CEO of ThirdEyesight, a retail consulting firm. “In China, closed ecosystems like WeChat and Douyin created the perfect environment for social commerce to thrive. In India, where consumers can freely move between Google, Meta and e-commerce giants, those closed loops don’t exist.”

Globally, TikTok Shop, Douyin, WeChat, Pinduoduo, and Taobao Live dominate social commerce. According to Business of Apps, a data provider for the global app industry, TikTok earned $23 billion in 2024, with nearly 23% of it from in-app and commerce purchases.

If similar models are launched in India, e-commerce giants would face direct competition from the very platforms that fuel their traffic.

The Wait Continues

From beauty tutorials to thrift stores, social media spawns thriving micro economies. Yet, true social commerce — where discovery leads directly to purchase — hasn’t yet clicked.

The next big leap for India’s e-commerce may not come from deeper discounts or faster delivery but from social media itself. “The idea of instant gratification is key,” says Biswas. “When the ‘Shop Now’ button comes back, we’ll be the first to use it.”

Till then, India scrolls, likes, shares — and waits.

(Published in Economic Times)