admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

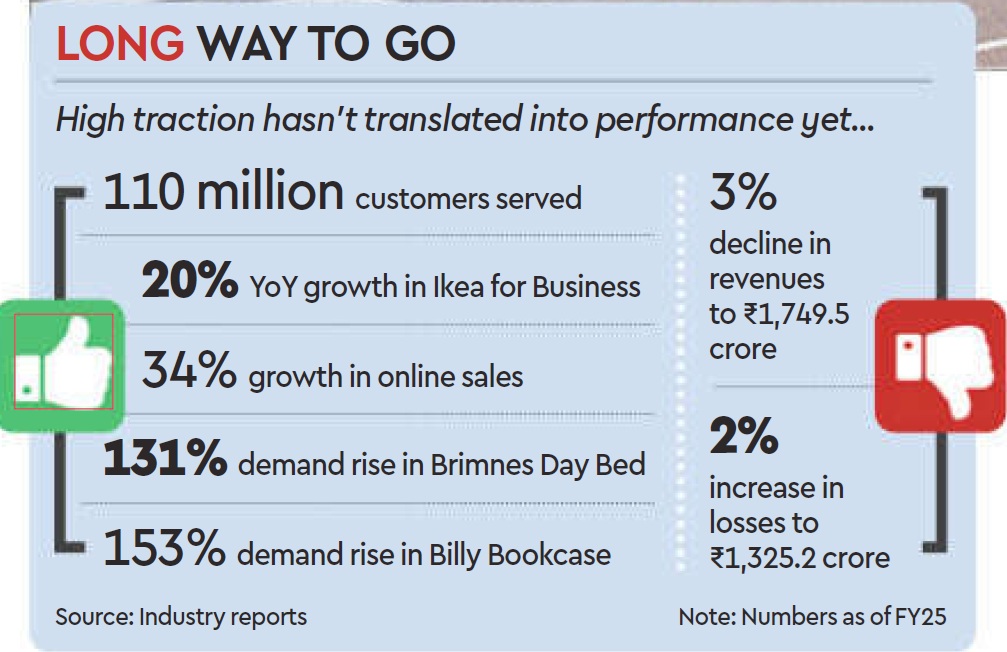

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

February 16, 2026

Christina Moniz, Financial Express (Brand Wagon)

16 February 2026

Starting this month global sportswear maker Nike shifted its e-commerce operations to beauty and fashion marketplace Nykaa to address poor logistics, high delivery times and inventory niggles. With Nykaa in charge, the brand said, customers can expect free shipping on all orders and faster deliveries rang ing from twotofour days depending on the location.

The change comes at a time when Nike is struggling to cope with declining market share and operational and supply-side issues in India. Its physical store count in the country has dropped by half in the past ten years to 100 from over 200 a decade ago. Nike in India undertook major restructuring of its business between 2016 and 2019, closing 35% of its stores in those three years to take a more digital-first approach.

It’s not all doom and gloom though. The brand reported a 14% growth in sales in the fiscal ending March 2025 to clock ₹1,380 crore. But it is well behind competing brands such as Puma (₹3,274 crore) and Adidas (₹3,114 crore), both of which have over 400 stores across the country.

Given India’s size, the competitive landscape and potential, treating it as a secondary export market to be serviced from Singapore was a poor decision on Nike’s part, says Devangshu Dutta, founder and CEO, Third Eyesight.

Nike’s alignment with a local player offers important strategic lessons for global brands with big ambitions in India, especially those in the ₹8,800 crore sportswear market. Brands that have not treated India as an afterthought have succeeded in creating sustained growth and market leadership, says Dutta.

“Most of Nike’s global competitors have treated India as a market high consequence. Nike might be the leader by global revenues, in India is smaller than its global rivals like Adidas, Puma and Skechers. ASICS has a smaller base but is growing at 30% while Lotto is also looking to grow its footprint massively, observes Dutta.

Ever since Nike’s digital-first pivot, its customers in the country have raised several complaints citing delivery failures and poor service, with some deliveries reportedly taking weeks. Its decision to transfer its digital operations to Nykaa in India could potentially address these missteps and reverse the breakdown of customer experience, say experts.

Changing course

“The recent move feels like Nike acknowledging that India cannot be treated as an extension of a global system. It needs local infrastructure, local partners, and a model built specifically for how Indians shop online. Partnering with Nykaa brings local execution muscle that is hard to replicate quickly,” observes Tusharr Kumar, CEO, Only Much Louder, adding that the move is a maturity moment for global brands. “Scale alone doesn’t guarantee success. What matters is adapting to local consumer behaviour, logistical realities and service expectations,” says Kumar.

That said, Nike’s shift won’t be without challenges. The biggest one will be balancing scale with brand control, notes Yasin Hamidani, director, Media Care Brand Solutions. “While Nykaa offers strong reach and trust, Nike will need to ensure its premium positioning, product storytelling, and customer experience don’t get diluted. If managed well, this move doesn’t necessarily hurt Nike’s brand,” he states.

However, he adds that competition like Adidas and Puma, with stronger on-ground retail and omnichannel presence, may gain an edge if Nike’s visibility or momentum slows. “The partnership with Nykaa must feel strategic and not like a retreat,” he cautions.

Given that Nykaa is also a marketplace for other activewear brands, it remains to be seen how the platform maintains Nike’s premium customer experience. “On its own platform, Nike could control everything from storytelling to checkout flows and post-purchase engagement. Nike will now need to adjust to sharing customer data, promotional calendars, and operational priorities with a partner platform,” says Somdutta Singh, founder & CEO at Assiduus Global, adding that striking the right balance between leveraging Nykaa’s scale and maintaining Nike’s distinctiveness will be key.

(Published in Financial Express – Brandwagon)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

February 12, 2026

Vaeshnavi Kasthuril, Mint

Bengaluru, 6 February 2026

Global fragrance maker Bath & Body Works Inc. is betting on a reset to revive growth after years of heavy discounting and weak product innovation dulled its brand momentum across markets. The Columbus, Ohio-based retailer is pivoting to a “consumer-first” formula strategy centered around upgraded formulations, more disciplined marketing, and fewer promotions.

The reset matters as India is emerging as one of the company’s fastest-growing and best-performing markets and is also becoming a testing ground for how the brand evolves its retail model. India now ranks among Bath & Body Works’ top five international markets by growth.

“We’re seeing strong engagement across stores (in India), digital marketplaces and even quick commerce, which gives us confidence as we evolve the brand and introduce more innovation,” said Tony Garrison, global vice president at Bath & Body Works, in an interview with Mint.

The fragrance maker entered India in 2018 in partnership with Dubai-based Apparel Group and has since expanded to about 50 stores across major metros, while also building an online presence through platforms such as Nykaa, Myntra, and Amazon. Apparel Group brings over 80 global brands to India, including Victoria’s Secret, Charles & Keith, Aldo, Crocs, and Tim Hortons.

“We’re learning a lot from how the Indian consumer shops across platforms, especially the speed and convenience expectations,” Garrison said. “It’s helping us think differently about assortment, pack sizes and how we show up digitally”.

Even as discretionary spending softened, the brand’s franchise partner, Apparel Group, delivered double-digit sales growth in India and high single-digit comparable store gains in FY25. It reported a 26% year-on-year jump in FY25 revenue to ₹1,118 crore and a net profit of ₹20.5 crore, reversing a loss in the previous year.

Globally, Bath & Body Works’ earnings reflect soft consumer demand as well as margin pressures. Its revenue declined 1% to $1.59 billion in the third quarter of FY25, while net income fell 27% year-on-year to $577 million.

Reviving the fragrance engine

While legacy scents such as Japanese Cherry Blossom, Champagne Toast, and Thousand Wishes remain global blockbusters, the company admits it hasn’t produced enough new hits at a similar scale in recent years. Japanese Cherry Blossom is a $250 million fragrance.

“I think we haven’t done the best job of keeping up with some of the fragrance trends. We haven’t done a lot of innovation, and that’s what you’re going to see this year. This is a big change year for us,” Garrison said.

The company plans to elevate its home fragrance portfolio, bringing in more premium candle collections, gift-ready packaging, and deeper, more sophisticated scent profiles. The broader goal is to encourage shoppers to trade up within the brand rather than wait for markdowns. “We want customers to see the value in the product itself… not just the promotion,” Garrison said.

New retail formats

To test new retail formats, the company and Apparel Group plan to pilot a small “neighbourhood store” format of roughly 500 square feet in select non-metro markets later this year. These stores will focus heavily on core body care lines and hero fragrances, while creating a more discovery-led environment for first-time shoppers.

India is also emerging as a key market in testing how far premiumisation can go. Garrison noted that the company has not seen a slowdown locally: “India has actually been one of our strongest markets in the post-Covid period. Even when consumers are careful, they still spend on small luxuries that make them feel good”.

What experts say

Retail experts caution that the reset in India won’t be without challenges. Devangshu Dutta, founder of Third Eyesight, noted that brands often fall back on discounting when volumes don’t come through. He added that the personal care market has become intensely crowded, making brand clarity critical.

While the brand is leaning into quick commerce and smaller stores, Dutta cautioned that premium brands still need larger formats to build experience-led differentiation. “Neighbourhood stores can be spokes, but you still need the hub—the large store—to communicate the brand experience,” he said.

Race Intensifies

The turnaround plan comes at a time when rivals, including The Body Shop and Forest Essentials, are also vying for the Indian consumer’s wallet. The Body Shop plans to achieve ₹1,100 crore in revenue in India within the next three to five years. India’s fragrance market was valued at $1.0 billion in 2024 and is projected to grow at a 13.9% CAGR to $3.23 billion by 2033.

(Published in Mint)

admin

November 18, 2025

Chris Kay, Krishn Kaushik and Andrea Rodrigues in Mumbai

Nov 18 2025

Just before dawn, Kashif Sameer joins dozens of couriers zipping across Mumbai to deliver items stocked in a basement of a shopping mall run by Reliance Industries.

“I make between 20 and 30 deliveries in a day,” said the 25-year-old, who had just driven a mile across the chaotic roads of the Indian megacity to drop off groceries ordered 15 minutes earlier. “It is very popular with customers.”

The buzzing activity at the so-called dark store, a mini-warehouse operated by Reliance’s ecommerce platform JioMart, is part of a renewed push by the conglomerate’s chair and Asia’s richest man, Mukesh Ambani, to reassert his company’s position in India’s retail market.

It has added hundreds of dark stores to operate a total of nearly 20,000 physical outlets this year — almost double its pre-pandemic size — as it battles for dominance against Blinkit, Swiggy and Zepto in the country’s ballooning quick-commerce market.

“It’s a question of who runs out of money first,” said Arvind Singhal, chair of retail consultancy The Knowledge Company. “We will see some kind of a shakeout.”

Despite its large network of physical stores, Reliance has yet to corner the domestic consumer market like it did with telecoms a decade ago. It faces entrenched competition from established domestic and international rivals, as well as millions of kiranas, family-run convenience stores.

The sprawling Tata Group operates a wide range of consumer businesses, while global multinationals such as Unilever and Nestlé are important players in India’s household goods market.

Reliance Retail, the division that contains all of the conglomerate’s consumer-facing units, had shed tens of thousands of employees and closed underperforming stores following a bloated build-out during the Covid-19 pandemic and slowing middle-class spending.

But India’s most valuable company, which has a market value of more than $225bn and operates across oil refining, telecoms and entertainment, is expanding its retail reach again.

Reliance Retail’s latest results point to a rebound. In the quarter ending September, the unit reported revenue of about $10bn and profit of $390mn, up 18 and 22 per cent respectively from the previous year.

“Reliance’s scale in retail now is unmatched in India,” said Devangshu Dutta, chief executive of consumer advisory company Third Eyesight, in reference to the breadth of the conglomerate’s business. “This scale is unique in India and rare in global retail.”

Ambani’s retail ambitions are being led by his 34-year-old daughter, Isha. In August, she detailed plans for Reliance’s consumer brands subsidiary, which has a portfolio including Lotus Chocolate and the recently revived nostalgic Indian soft drink Campa Cola, to reach $11.7bn in revenue within five years.

Ultimately, the goal was to “become India’s largest FMCG company with a global presence”, said Isha Ambani during Reliance’s annual meeting.

The company told the Financial Times that it continued to “reinforce its position as India’s largest retailer, expanding its nationwide network”.

While Ambani originally indicated that he wanted to list Reliance Jio Infocomm, the telecoms unit, and Reliance Retail by 2024, people familiar with the company said the retail unit was not ready to go public. The billionaire said the Jio listing could happen in the first half of next year.

“Competitive intensity in every category in the discretionary retail side has picked up very sharply,” said Karan Taurani, executive vice-president at Elara Capital, who does not expect Reliance Retail to float for at least two years. “New competitors, new brands have come in and they are challenging the larger incumbents.”

The Ambanis, who operate as gatekeepers for foreign companies seeking access to India’s massive but challenging business landscape, have sought to cement their position through a spate of partnerships with western retail brands.

Foreign brands including West Elm, Pottery Barn and Superdry have stores in Reliance’s shopping malls in upmarket Mumbai. However, those joint ventures have largely struggled to gain traction with shoppers in India, where the per capita income remains less than $3,000.

The conglomerate’s foreign brands business housing these joint ventures lost Rs2.7bn ($30mn) in the financial year through March 2025, according to the latest available accounts. The Knowledge Company’s Singhal called Reliance’s push to bring international names to India “a vanity project”.

Reliance’s high-profile partnership with fast-fashion retailer Shein has also been underwhelming. The company returned to India this year under Reliance’s wing after being booted out in 2020 when relations between New Delhi and Beijing soured following military clashes along their disputed border.

Shein’s app has been downloaded just 11mn times, according to market intelligence firm Sensor Tower. Its discount prices are largely matched, if not undercut, by many Indian ecommerce and fashion retailers, say analysts.

Reliance is investing heavily in quick commerce, where deliveries are promised in 30 minutes or less. Bank of America estimates the market could reach $128bn by 2030.

The field is at present dominated by Blinkit, Swiggy and Zepto, which together control more than 90 per cent of the quick commerce delivery market and compete with Amazon and Walmart-owned Flipkart. None of the companies are profitable.

The Ambanis are eager to catch up. Over the past six months, Reliance has built about 600 dark stores across cities to plug gaps in its vast store network. By contrast, market leader Blinkit operates about 1,800 dark stores.

In quick commerce, “we have to be there because everybody is”, said a person close to the conglomerate. “It is a long-term strategy.”

On a call with analysts last month, Reliance Retail’s finance chief Dinesh Taluja admitted to delays in entering quick commerce. But he insisted that Reliance offered better prices, more variety and wider reach across smaller Indian cities where it is often the only formal retailer.

“The competition today is mainly in the top 10, 20 cities,” Taluja said. “We are present in almost a thousand cities. Competition will take many years to reach where we already have a head start there.”

Still, Reliance was facing an uphill battle, warned Elara’s Taurani. “JioMart is making a late entry,” he said, “it will be very tough to disrupt players here.”

(Published in Financial Times, all copyrights owned by FT)