admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

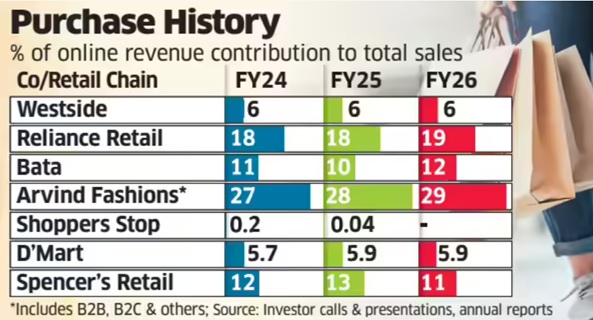

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

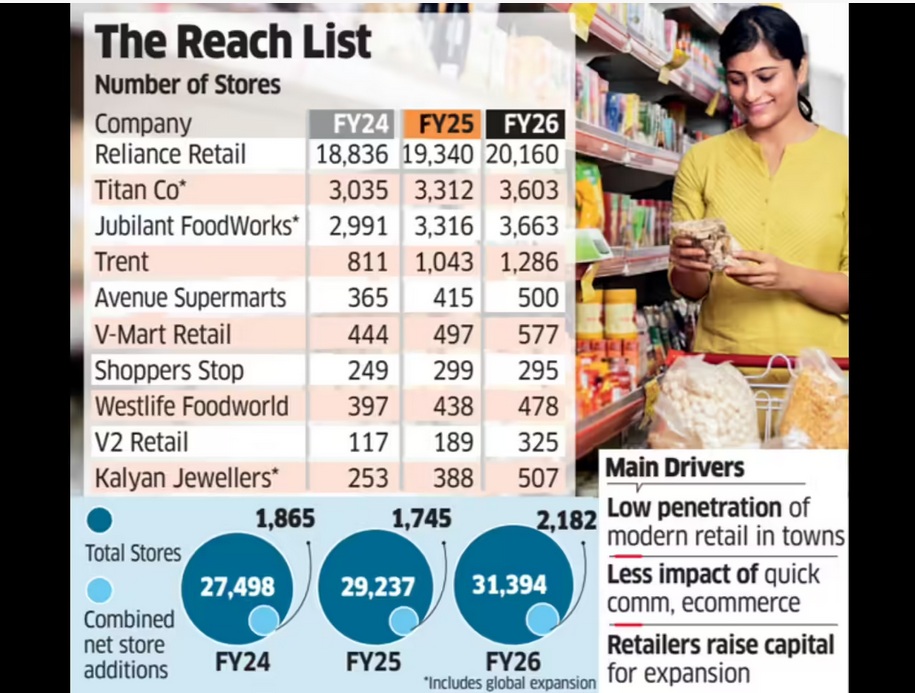

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

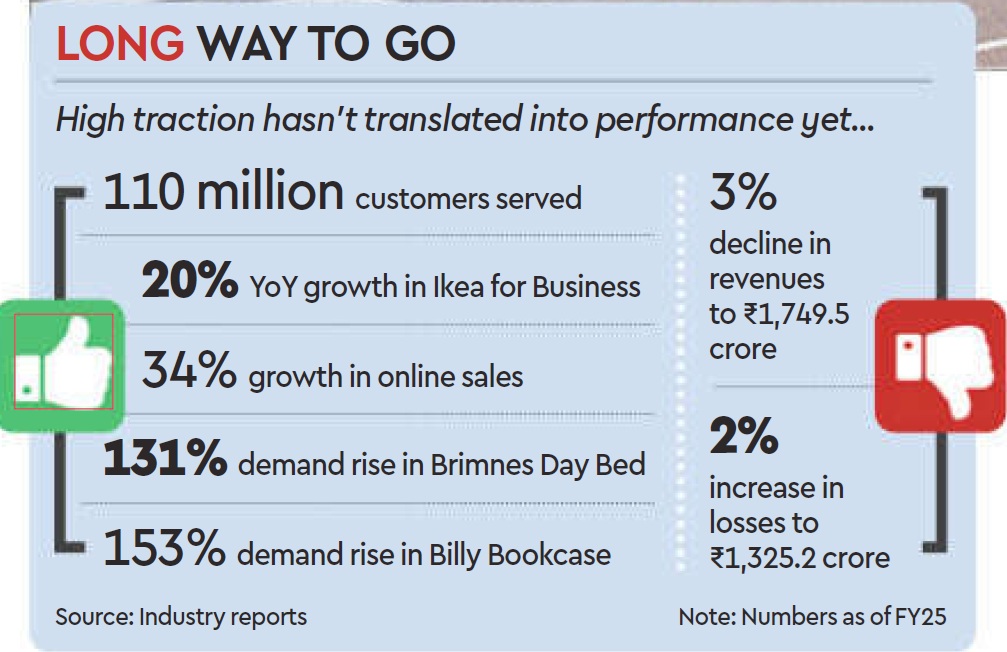

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

January 9, 2025

Sagar Malviya, Economic Times

9 January 2025

Starbucks, Barista, Chaayos and Third Wave Coffee are among café chains facing the brunt of a slowdown in discretionary consumer spending. The impact is more severe for these retailers as they opened hundreds of new stores last fiscal year even as losses widened. To be sure, smaller chains such as Tim Hortons and Blue Tokai have bucked the trend.

Experts attribute the expansion rush to the urge among these retailers – both chains and standalone stores – to outpace competition. In certain instance, it led the same retailer to add stores in the same location, impacting its own growth instead of growing the pie.

At Rs 250 to Rs 350 for a cup of coffee, most chains target affluent, discerning coffee enthusiasts with artisanal brewing and experiential consumption, restricting the consumer base.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said the number of outlets have been expanding since 2022.

This was true for not just the new brands but also existing ones, Dutta said. “Cafe density in larger cities has gone up dramatically in the last couple of years.”

Growth rate fell to just 5% in FY24 from nearly 70% at Barista and Chaayos while Starbucks’ sales growth declined to 12% in FY24 from 70% in FY23. Third Wave saw sales growth slump to 67% from 355% during the period. Cafe Coffee Day posted a 9% increase in FY24, though sharply slowing from 59% a year ago.

Tim Hortons, however, more than doubled its sales last fiscal, its first full year of operations. Blue Tokai also bucked the slowdown trend with a 70% growth in FY24, compared to 73% in FY23.

Blue Tokai cofounder Matt Chitharanjan believes growth in India’s out-of-home coffee market is more than just a caffeine surge—reflecting the country’s shifting economic fabric. “Coffee consumption is strongly linked to income growth and India has reached a tipping point where it will support growth in the segment and should only accelerate going forward,” Chitharanjan told ET. “We have not seen any slowdown in coffee consumption and our positioning is also more product centric instead of just a cafe, which helped in double-digit same store sales growth.”

Tim Hortons, a Canadian coffee chain, which opened its first outlet in India in 2022, plans to have over 100 stores in the next three years. British coffee and sandwich chain Pret A Manger too launched its first shop in Mumbai as part of a franchise agreement with Reliance Brands. It plans to open up to 100 stores over the next five years. Third Wave and Blue Tokai are running more than 250 stores combined while Starbucks had over 330 stores as of March-end.

Tata Starbucks—the equal JV between Tata Consumer Products and US-based Starbucks Corp—said store footfalls have become a concern and the company has tweaked portfolio and pricing to attract traffic. Last year, the chain introduced classic hot and iced coffee starting at Rs 150 for a small cup, about 20-30% cheaper than regular coffee offered at Starbucks and other cafe chains.

“The stress is being seen across the quick service restaurant segment. It’s an overall consumer spending issue, especially in urban areas. And my hypothesis is probably food inflation is higher than what we think,” Sunil D’Souza, MD at Tata Consumer Products said during the December quarter earnings call.

Globally as well as in India, coffee growers have been hit with uncertain weather conditions while geopolitical factors are also affecting supply chains, which in turn, lifted prices to a record high. “The biggest challenge is erratic weather and climate change which has sent coffee prices to a 50-year high, but we will have to see how it impacts our pricing and profit after the current harvest,” said Chitharanjan at Blue Tokai.

(Published in Economic Times)

admin

October 7, 2024

Writankar Mukherjee, Economic Times

7 October 2024

Reliance Retail has initiated efforts to enter the thriving quick commerce market in a move that is set to escalate competition for Zomato-owned Blinkit, Swiggy Instamart and BigBasket, among others. The country’s largest retailer has started offering quick commerce services in select areas in Navi Mumbai and Bengaluru through its ecommerce platform JioMart since last weekend.

It will initially sell grocery items from its retail stores totalling about 3,000 nationwide, eventually adding value fashion and small electronic products such as smartphones, laptops and speakers, a senior executive said. All orders will be fulfilled from its own network of stores including Reliance Digital and Trends.

The retail arm of Reliance Industries plans to rapidly scale up its quick commerce venture pan-India by this month-end with the aim to deliver most orders in 10-15 minutes and the rest within 30 minutes, the executive said. The company will use its acquired logistics service Grab for the fulfilment.

Reliance, however, doesn’t have any plan to set up dark stores or neighbourhood warehouses, unlike other quick commerce operators, the executive said. Analysts said this may become a challenge in delivering orders within 30 minutes in large cities where traffic is high during peak hours.

To entice customers, Reliance won’t charge any delivery fee, platform fee or surge fee irrespective of the order value, and keep a major focus on untapped smaller cities and towns where quick commerce operators like Blinkit are yet to enter, the executive said. Other platforms have a delivery fee and platform fee.

Reliance plans to offer a wider choice of products of 10,000-12,000 stock keeping units by linking its entire store inventory to the quick commerce business, which too is much more than rivals.

Eventually, the company aims to cover 1,150 cities spanning 5,000 pin codes where it runs grocery stores. The executive said the company would target a bigger share of business from towns and smaller cities hitherto untapped by quick commerce firms.

“Reliance has reworked the way orders are delivered for JioMart. Earlier, orders had a scheduled delivery taking 1-2 days by small trucks who would take multiple orders and deliver them one by one. Now, all grocery orders will be quick commerce where one delivery bike or cycle will deliver one order. Each grocery store will cover a 3 KM radius,” the executive said.

Earlier this year, the company tried to reduce JioMart delivery timings to a few hours or at least the same day under its hyperlocal initiative. It has fine-tuned the process further to 10-30 minute delivery. “This has become a top-of-the-kind requirement in the market right now,” the executive said.

A spokesperson for Reliance Retail didn’t respond to ET’s queries.

Devangshu Dutta, chief executive at consulting firm Third Eyesight, said Reliance can ultimately use a blended approach of quick commerce deliveries in areas near its stores and scheduled deliveries a bit far away.

“Since they are in a market share acquisition mode in quick commerce, charging no transaction fees and offering higher discounts on products is a given. There is significant scope for deep-pocketed players like Reliance to strengthen presence in quick commerce. They have aggressively backed other experiments in the retail business once they worked, and may do it again,” said Dutta.

For fast-moving consumer goods companies, quick commerce is the fastest growing channel, accounting for 30-35% of total online sales.

(Published in Economic Times)