admin

June 12, 2026

Christina Moniz, Financial Express/Brand Wagon

12 June 2026

Legacy luggage brand VIP Industries is shedding some of its old baggage. The company, which manufactures Skybags and Aristocrat along with its flagship VIP range, has gone beyond cringey makeovers solely to attract Gen Z, and has embarked on a transformation journey that leverages its legacy to purvey a fresh range of offerings.

The company is modernising its digital presence and supply chain to catch up with competitors.

Managing director Atul Jain admits that the company has been a bit slow on the e-commerce front. It is reinventing its online store, while also making its products available across other e-commerce channels. “Quick commerce is becoming an important channel since there are several use occasions and segments within the luggage market. For instance, consumers often make last-minute purchases for a weekend trip via quick commerce. School bags and backpacks for kids, also great gifting options, are seeing good demand on these platforms,” he says

The company, which once dominated the ₹16,000 crore organised luggage market in India, saw a bit of a shakeup last year when the Piramal family sold 32% of its stake to a private equity firm. But it continues to be among the top three players in the category with a 29-30% market share. “Luggage plays the role of a traveller’s companion. We are creating designs to fit that role,” says Jain. “For example, our new VIP suitcases have a coffee cup holder and our cabin trolley bag has an easy access compartment for devices like laptops and iPads.”

The transformation goes beyond the product. VIP’s 350 exclusive physical retail touchpoints in the country are being revamped to offer a new customer experience.

Unpacking opportunities

Overits 55 years, VIP has grown from a briefcase brand into Asia’s largest luggage maker, housing labels like Skybags, Aristocrat, and Carlton (premium segment). While VIP is a premium offering targeted at business and travellers, its Aristocrat brand operates in the mass market and the budget-friendly Alfa targets consumers who typically shop in the unbranded segment. Aristocrat and Alfa together contributed upwards of 40% to the company’s revenue in FY25, followed by Skybags (28%) and VIP (20%).

Like many legacy brands, the VIP Industries’ faces the challenge to ia, stay relevant among Gen Z buyers as a plethora of digital-first brands swamp the market. “VIP has lost ground on relevance and desirability to a generation for whom luggage, like sneakers, is an expression of identity. To them, VIP feels like their parents’ brand,” says Nisha Sampath, managing partner, Bright Angles Consulting. D2C players in the category operate in the business of “lifestyle accessories” and not for “luggage” per se, she points out.

With a design-forward approach, incorporating features like compression systems, silent wheels and charging ports, these new-age brands have embedded themselves in travel “culture”, while also being Instagram worthy, say experts.

Jain says Skybags is VIP’s Gen Z focussed brand, which has over 8,20,000 Instagram followers. “We are sharpening our positioning for Skybags in our design, advertising and marketing outreach, especially on social platforms. The brand has a clear differentiation with youthful colours and prints to attract younger consumers,” he adds.

While D2C players have seen notable growth in recent years, they don’t have the kind of trust and brand equity that VIP has cultivated across its brands, nor do they have the scale or revenue that legacy brands have, he says.

Experts believe there is a significant growth opportunity for legacy players given that the unbranded market still accounts for ₹13,000-14,000 crore. The important lever for legacy brands is to clearly demonstrate value beyond price. “The unorganised market competes heavily on affordability, so organised players need to communicate durability, warranty, after-sales service, and consistent quality – areas where they have a strong inherent advantage over unorganised alternatives,” says Praveen Govindu, partner at Deloitte India. He adds that these brands should also invest in advertising and communicate this value to the end consumer.

Not only are the needs different among different consumer groups, competitive pressures are also diverse. “VIP can segment the market more cleanly with its portfolio of brands if it maintains absolute distinction to ensure clear consumer targeting across not just product attributes and pricing, but also communication and channels,” says Devangshu Dutta, CEO, Third Eyesight.

(Published in Financial Express)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

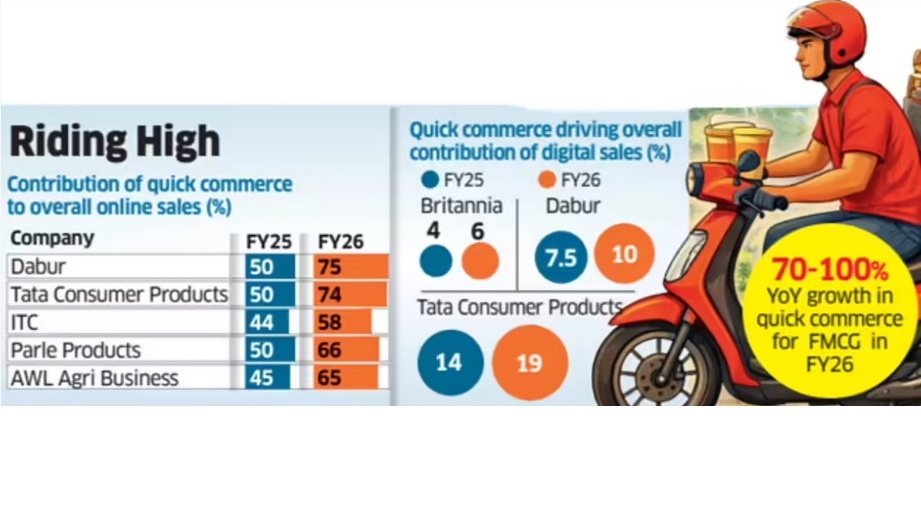

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 1, 2026

Yuthika Bhargava & Vikash Tripathi, Outlook Business

Mumbai, 1 May 2026

For generations of Indians, the word Tata hasn’t just been a brand, it has been a permanent resident in our homes. Think back to the kitchens of your childhood. It was the familiar packet of Tata salt, the Desh ka Namak, that seasoned every meal. It was the steaming cup of Tata tea that signalled the start of the day for elders at home.

In every Indian household, the name represents trust and legacy.

Yet, when N Chandrasekaran, chairman of Tata Sons, wanted to hire Whirlpool India’s head Sunil D’Souza to lead Tata Global Beverages (TGBL) in September 2019, he got a shock refusal.

Who in their right minds wouldn’t want to join a Tata company?

Well, D’Souza hadn’t heard much about TGBL. In fact, his colleague at Whirlpool India had called it a “sleepy company”.

At the time, TGBL’s revenues were a meagre ₹7,408cr compared to close to ₹50,000cr and ₹40,000cr logged by fast-moving consumer goods (FMCG) heavyweights ITC and Hindustan Unilever (HUL), respectively, in 2018–19.

Experts had noted TGBL had not much to show in terms of major product innovation for years. Primarily a tea and coffee company, it was locked in a low-growth cycle.

In 2018, various analysts had remarked that TGBL’s growth was muted as it wasn’t selling anything beyond tea and coffee.

At TGBL’s annual general meeting on July 5, 2018, Chandrasekaran said the company would exit loss-making subsidiaries and focus on profitable ones that can be scaled up. “Even though in volume terms, the company continued to be number one in the Indian market, the same was not true in value terms,” he said.

So, D’Souza’s immediate “no way” to the job offer was justified. TGBL wasn’t on his radar or anyone’s at the time.

But the headhunter convinced him to meet Chandrasekaran.

This meeting, says D’Souza, made all the difference for him. He recalls the Tata Sons’ chairman saying “I have the money. But I don’t have the team to run it.”

But the clincher for him was Chandrasekaran’s larger plan to foray into the FMCG space and the intent to disrupt the market.

In December 2019, Tatas announced D’Souza’s appointment as managing director and chief executive effective April 2020. One more important addition to this FMCG team was Tata Sons’ Ajit Krishnakumar as chief operating officer.

What followed was the duo’s visits to Mumbai, Bengaluru and Gurgaon. They walked to distributor offices and kirana stores and sat through market visits. “We drew out in great detail what we wanted this company to look like,” says Krishnakumar.

The mandate from Chandrasekaran was simple. He wanted a company commensurate with the Tata name, one that shared the same shelf space as the likes of HUL and ITC.

Humble Beginnings

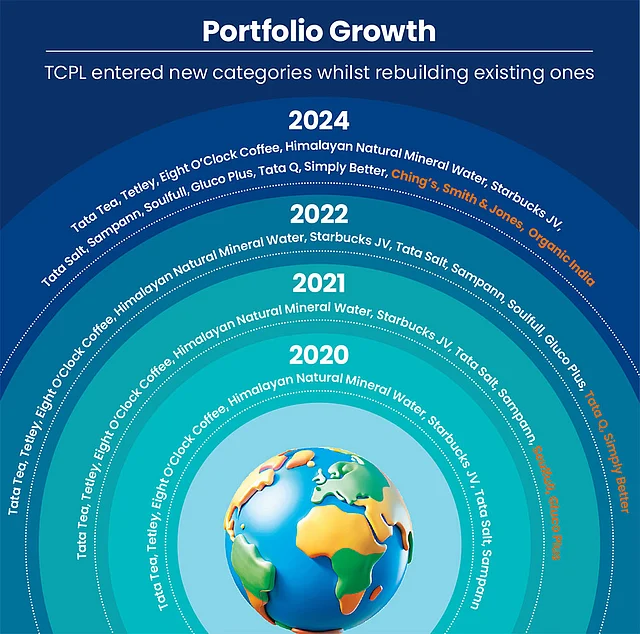

The mission to become an insurgent company in the FMCG space kickstarted with the formation of Tata Consumer Products (TCPL) in February 2020 by merging TGBL’s tea and coffee units with Tata Chemicals’ salt and pulse businesses.

However, with established FMCG rivals like HUL, ITC and Nestlé India, D’Souza and Krishnakumar had their tasks cut out. The competition had a century of headstart in India.

Within the Tata group itself, TCPL ranked eighth by revenue in 2019–20, behind Tata Motors, TCS, Tata Steel, Tata Power, Titan, Tata Communications and even Tata Chemicals.

But “things couldn’t get any worse than this, right? We were already at the bottom of the heap in FMCG. You could only get better,” recalls D’Souza about his mindset at the time (see pg 24).

Building a brand name as a Tata company opens doors. But competing is another. Could this new company take on HUL, Nestlé and ITC?

TCPL started by trimming the portfolio, streamlining the consumer products businesses spread across five continents, from India and the US to the UK, Canada, South Africa and Australia.

In Australia, the company held a 7% share of the tea market but was also running an out-of-home coffee dispensing business that was losing millions of dollars. It was shut down in December 2020.

In the US, a food-service joint venture, including a tea factory and a distribution unit, was disposed of as well in March 2021.

“We had 45 legal entities. That’s not tenable,” D’Souza says. “We exited areas where we didn’t see value. The focus clearly shifted to not just the topline, but margins.”

Six years later, TCPL’s entity count stands at 25 and is well on the way to the target of 18 entities.

What stood out in the next six years is TCPL’s sole focus to dominate the food and beverages (F&B) category. The company’s mantra: think big, move fast.

By late 2020, once the initial scramble post the merger had settled, TCPL ran a strategic exercise called Project Falcon. The result was a playbook: categories to foray into, categories to stay out of, where to build and what to buy.

The year 2021 provided a starting point for TCPL. In March that year, the United Nations officially declared 2023 as the International Year of Millets, acting on a proposal from India. The country being the largest producer of millets, accounting for 20% of global production, wanted to raise awareness of millet’s role in improving nutrition and creating sustainable market opportunities.

The timing was fortuitous for TCPL. In 2021, its first acquisition, Soulfull, was a millet-based health-food brand. This ₹155.8cr deal gave Tatas a foothold in a category it couldn’t have credibly entered on its own.

Within three years of acquisition, Soulfull’s distribution had grown from 15,000 outlets to 300,000, carried on the back of the Tata’s existing network.

Three years later, in January 2024, when TCPL announced two deals with combined worth of ₹7,000cr in quick succession, its stocks fell.

The market wasn’t convinced initially. TCPL had just committed roughly 40% of its annual revenue to two brands it did not build. At the time, it was a new player with its core business running on single-digit margins.

Analysts at Ambit Capital estimated the acquisitions would cut 2025–26 earnings by roughly 10%.

The first, a ₹5,100cr deal, was to buy Capital Foods, the company behind Ching’s Secret.

The second was a wellness play, a ₹1,900cr cheque for Organic India, a Lucknow-based brand with a devoted following in the US.

D’Souza had faith in these big-cheque acquisitions. “We are not playing this game for the next one or two years. We do these acquisitions knowing that we put money there. It will bear out over a period of time.”

Ching’s Secret had spent decades building the desi Chinese category in urban Indian homes almost single-handedly—the Schezwan chutney, the noodles and sauces.

As for Organic India, it had a network of farmers across Madhya Pradesh and Uttarakhand, a manufacturing facility in Lucknow and decades of Ayurvedic credibility in the American wellness market. It was built over years of relationships that TCPL simply did not have and could not quickly acquire.

And the numbers weren’t disappointing. By the third quarter of 2025–26, Capital Foods and Organic India together were generating ₹354cr in quarterly revenue, up 15% year on year, at gross margins of roughly 48%, well above TCPL’s blended average of 43%.

Motilal Oswal expects integration costs to ease substantially by 2026–27, after which the margin story should become clearer.

Fight for Shelf Space

From the get go TCPL was clear about the categories it wanted to enter and to avoid as well.

It didn’t want any stake in the basic edible-oil segment. This shelf had far too many players led by the likes of Fortune and Saffola.

But cold-pressed oil was a different ballgame. Consumers here were buying into a health claim with no way to verify if the product was trustworthy. “The Tata name does the magic there,” says D’Souza.

In August 2023, TCPL launched a range of cold-pressed oils under its brand Tata Simply Better, a new brand that was launched in 2022 to enter the plant-based mock-meat category.

The logic: find the trust deficit, fill it with the four-letter Tata name, became the basis for every category TCPL considered entering.

The sweet spot for the insurgent company was categories that were fragmented, where consumers didn’t fully trust what they were buying and where a credible brand could change the equation.

Biscuits was another category that TCPL gave a skip.

Britannia and Parle owned 56% of the market, built over decades of backward-integrated manufacturing and distribution muscle.

This restraint, wrote Motilal Oswal, in a recent note, is “rare in Indian FMCG”. Categories like biscuits, snacks, colas and base edible oils are permanently off the table, crowded segments where the Tata brand adds no meaningful trust-led differentiation. “Such portfolio discipline is a positive indicator of capital allocation quality,” the note observes.

Built organically, cold-pressed oil is now running at an annual revenue of ₹350cr. Dry fruits, another category Tatas entered with the same trust deficit logic is at a ₹300cr run rate.

What differentiates TCPL from other FMCG players?

The categories that Tatas have built or bought into are still being defined. HUL and Nestlé, on the other hand, are dominant in mature markets where penetration is already high. HUL is buying established brands in categories it rules, plugging gaps in existing portfolios. TCPL is buying into categories it has never played in, at scale, while the core business is still being built.

Whether this is disciplined offence or over-extension is a question the next two years of integration will answer.

Even before acquisitions came into play, among the first things D’Souza and Krishnakumar did was to build accountability. There had been no one person who owned a category (tea, salt or pulses) from manufacture to sales.

They created category leaders who were responsible for the product’s profit and loss, bar the fixed costs. Functions that did not exist were created.

In 2020, Tata Salt was present in nearly 2mn retail outlets across India. TCPL’s own salespeople directly visited just 150,000 of them. The remaining 1.85mn stores were being supplied through a chain of middlemen, called super stockists or consignee agents.

These middlemen picked up Tata Salt in bulk from big distributors and moved it onward through their own networks. No one from TCPL knew what was selling fast, what wasn’t or what product a rival had placed on the shelf just two rows away.

“That shows the strength of the brand and also the lack of distribution reach,” says D’Souza. In FMCG, this gap between a brand’s total reach and its direct reach is called the wholesale multiplier. It measures how many outlets are stocking your product for every outlet you directly supply. A multiplier of five is considered normal. TCPL’s was 15, a number almost unheard of.

This meant TCPL had no direct relationship with over 90% of the shops and no mechanism to introduce anything new in those shops.

“There was this big layer [of middlemen] in each state. We removed that entire layer. That layer alone was about 1.2% in terms of cost. Then we appointed proper distributors, recruited the right people and rebuilt the distribution system,” says D’Souza. This was a saving of 36 paise on every 1kg pack of Tata Salt with an MRP of ₹30.

Rebuilding the entire distribution ecosystem took six to seven months. The distributor base was cut from 4,500 to around 1,500–1,600. These distributors were now carrying the full portfolio, reporting directly to TCPL. The sales force was expanded by 30%.

The results were quick. TCPL’s direct outlet reach stands at approximately 2.3mn today from roughly 500,000 in 2019–20. The total reach is 4.4mn outlets now.

“There are two key benefits to getting closer to the retailer. It supports margins and gives you better visibility into what’s happening at the point of sale,” says Arvind Singhal, chairman of The Knowledge Company, a management-consulting company.

Progress is real. But TCPL has miles to go. HUL reaches more than 9mn outlets, built over nine decades. ITC reaches 7mn. Nestlé 5.2mn. India has roughly 12–15mn kirana stores.

“The whole premise was to create a distribution funnel through which you can then push different products,” says D’Souza.

Bump in the Road

The first real test for TCPL was whether the idea of pushing new products through the distribution funnel would work.

Pradeep Gupta, a kirana store owner in Varanasi, has been a witness that it worked. Six years ago, two products were always on his shelf: Tata Salt and Tata Tea Premium. He didn’t need a salesperson to tell him to stock them.

Now, new products from Tata Sampann spices to Ching’s Secret sauces and Soulfull rusk are on the shelves of Gupta’s tiny store. TCPL’s distribution network made it happen. A distributor who had built his business around Tata Salt would now also handle Ching’s Secret. A salesperson who knew how to move a commodity would now pitch a branded sauce.

But not everyone was happy. The All India Consumer Products Distributors Federation (AICPDF) went up in arms against TCPL in 2025. Distributors were protesting excessive targets, stocks were piling up in warehouses and damaged goods sitting for months with no settlement.

The mismatch was structural. Salt moves through wholesale with 80% of it never seeing a retail salesperson. Most of the newer growth products like Ching’s Secret are sold almost entirely through direct retail.

Running both through the same distributor was asking a man who sold salt by the tonne to also build a market for Schezwan chutney.

The AICPDF president Dhairyashil H Patil explains what went wrong. “Salt is typically sold in large volumes. Products like Tata Sampann [a packaged pulses brand launched in 2017 under Tata Chemicals] and tea are the opposite, only about 8–10% goes through wholesale. After the merger with Capital Foods, there was a complete mismatch.”

Distributors built around salt did not find it viable to handle retail-heavy products. “Most Tata distributors derive 60–70% of their turnover from salt, so their focus remains there,” adds Patil.

TCPL eventually had to take back damaged goods sitting with distributors for six to eight months. D’Souza’s response was to separate the networks entirely.

TCPL’s growth businesses like Ching’s, Soulfull and Organic India had their own distributors and sales teams in just three months. “For any other company, it would have taken at least a year or more,” D’Souza says.

Also, the portfolio TCPL had inherited gave its own answer to what the distribution funnel could carry. Sampann, a “hobby for Tata Chemicals”, arrived at the merger doing ₹150–200cr in revenue. In 2025–26, Sampann is expected to touch ₹1,700–1,800cr, with pulses alone contributing ₹1,000 crore.

“The whole DNA of the company is to stay agile and make sure to move at full speed,” says D’Souza.

Fast and Furious

TCPL moved at full speed indeed when it came to trends. In May 2019, Beyond Meat, a company that made plant-based burgers from pea protein, listed on Nasdaq. Its stock more than doubled on the first day.

Within months, McDonald’s was testing a meatless McPlant and KFC was piloting plant-based chicken. Plant-based meat looked like the future of food.

TCPL bought into the trend. In 2022, it launched plant-based mock meat under the Tata Simply Better brand. However, the global buzz died sooner than expected. Two years later, TCPL exited the category.

The exit is not the point. What matters is that the product took 150 days from concept to shelf. TCPL had built something that would have been impossible two years before.

Mock meat required food science to replicate the texture of meat from plant protein, process technology, a team of chefs, food scientists and packaging engineers.

Capabilities were built from scratch. In the beginning, the R&D team was just 10–15 people. Today, it operates across three centres: Bengaluru as the research and packaging science hub, Mumbai for food innovation and product development, and Barabanki in Uttar Pradesh, anchoring the wellness work after the Organic India acquisition.

The team remains lean, around 60 people, roughly one-third the size of comparable FMCG rivals, estimates Vikas Gupta, R&D head at TCPL.

When D’Souza arrived in 2019, just 0.8% of TCPL’s revenue came from new product launches. The industry benchmark is 5%. TCPL was nowhere close. Today, that number stands at roughly 5%.

Onkar Kelji, research analyst at Indsec Securities, a brokerage firm, frames the economics of the chase: the early returns on innovation can be thin, he says, as companies push products aggressively and launch on e-commerce where margins are typically lower than general trade. “But if these products scale, they deliver better margins over time.”

Across the industry, the contribution of newly launched products has generally stayed under 5%. With acquisitions, that mix is expected to rise, notes Kelji.

In FMCG, innovation is not only about launching entirely new categories. It is also about rethinking what already exists. “We were singularly focused on vacuum-evaporated iodised salt,” says D’Souza.

The thinking that replaced it was simpler. “Give the consumer what they want. Plain salt. Salt with iron, with zinc. Low sodium for the health-conscious. Himalayan rock salt for the premium buyer. Sendha [during Navaratri]. One product became a portfolio,” adds D’Souza.

A patented granulation technology was developed for double-fortified salt, solving a long-standing industry problem of how to add iron to iodised salt and keep it stable.

TCPL also produced the Tata Coffee Cold Coffee liquid concentrate, a first-of-its-kind product in the Indian market that lets consumers make cold coffee at home without equipment.

The first 100 product launches after the merger took three-and-a-half years. The next 100 took 16 months. At one point, the company was turning out a new product every week, each one requiring its own supply chain, packaging, shelf-space negotiation and own sales story.

For a company that was criticised in 2018 for launching almost nothing new for years, this was a different metabolism entirely. “It’s easier when you are doing everything from scratch, says D’Souza, adding “As soon as we see a trend, we are on top of it and running with it.”

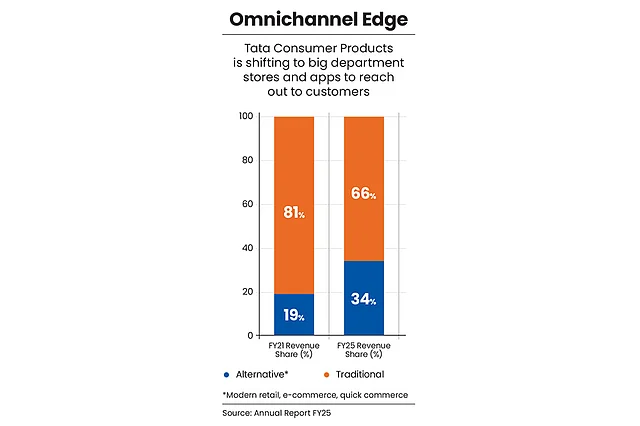

E-commerce is a good example of how TCPL, weeks into its merger, took on the very real challenge of lockdown and built a new digital vertical to boast of.

Lessons from Pandemic

In March 2020, most Indians had online grocery apps on their mobile phones. These were rarely used. But the Covid-19 pandemic and subsequent lockdown reshaped this landscape.

BigBasket’s servers strained with massive order volume surge. Dunzo crashed repeatedly. Amazon Fresh ran out of delivery slots. Millions of urban Indians were struggling to restock their kitchen shelves.

At the time, TCPL’s entire e-commerce operation was one person’s part-time responsibility. The southern regional sales head looked after e-commerce. TCPL had to race against time to build a digital channel. And D’Souza’s team built it fast.

E-commerce became a dedicated function with its own head. A modern trade team was created. Every new product launch went digital first. E-commerce gave TCPL something general trade never could: unfiltered data on what actually works.

While the company’s overall innovation-to-sales ratio was 3.4% by 2022–23, it was 10% on e-commerce. Products that proved themselves online were then pushed into general trade.

“The beauty of e-commerce is that it is only you and the consumer. It is the power of your product and your brand and your value proposition,” D’Souza said in an earnings call.

E-commerce’s revenue contribution at the time of merger was 2.5%. By late 2021, it was 7%, a growth of 130% in a single year. By 2024–25, it reached 14%, overtaking modern trade for the first time. By the third quarter of 2025–26, e-commerce and quick commerce together stood at 18.5%.

“I don’t think anyone else is in this ballpark,” says D’Souza. He is not wrong. HUL’s equivalent figure runs at 7–8%, Nestlé India’s at 8.5%. The company that almost missed the decade’s defining channel shift now leads it among its peers.

What makes the number more significant, according to Motilal Oswal, is TCPL’s margins on quick commerce are comparable to traditional channels, unlike most peers, who are seeing margin erosion on the platform.

The Tata group’s acquisition of BigBasket in May 2021 gave TCPL a window into how millions of Indians shop for groceries.

In an earlier earnings call D’Souza pointed out that BigBasket is a group company, not a TCPL asset. But within the group, he said, they were working closely to find synergies.

The channel shift also fits the company’s portfolio. Quick commerce skews toward the premium buyer: the person reaching for Himalayan rock salt at ₹100 rather than iodised salt at ₹30, Organic India’s tulsi tea rather than a commodity tea bag.

The premium end of TCPL’s portfolio, built over five years, is precisely what the fastest-growing channel wants. The mass business still dominates revenue.

Half-way Mark

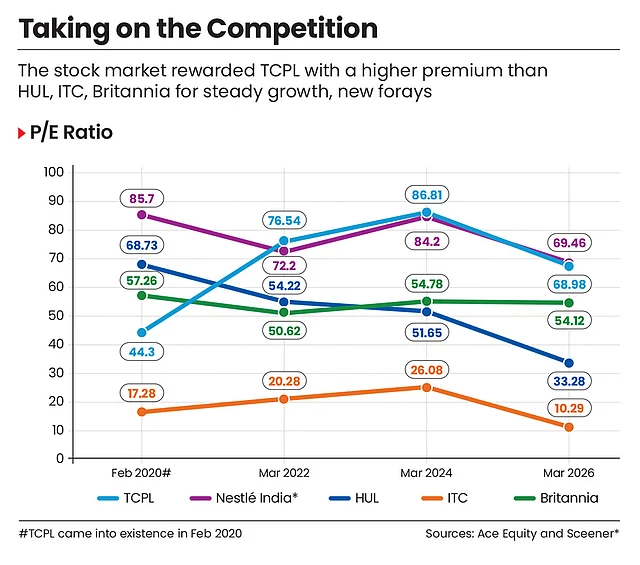

In January 2021, D’Souza said, “If we get it right, the rewards would be endless. If we didn’t, we’d have to live with it for a long time.” Five years later, he rates himself “five out of 10”. Ask him what TCPL has that HUL and Nestlé don’t, and the answer is the four letters T-A-T-A.

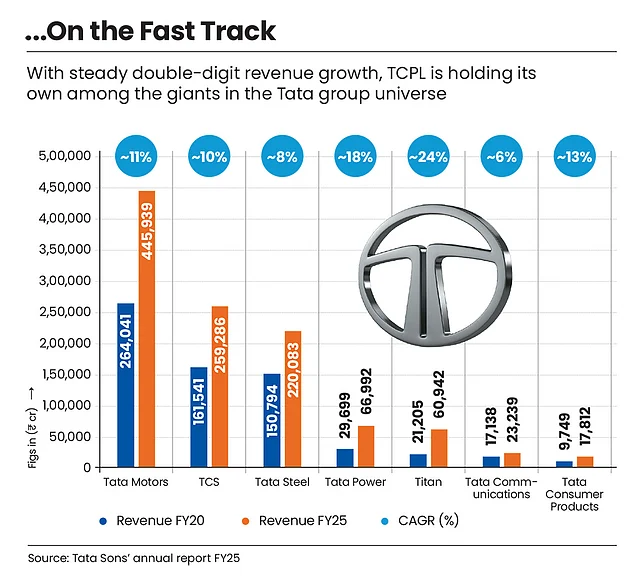

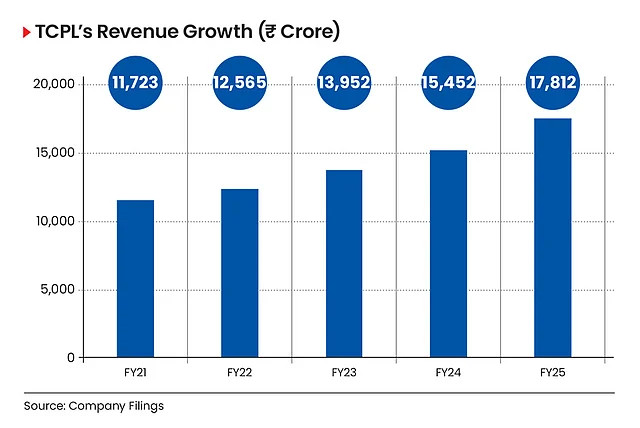

Here is what five out of 10 looks like. TCPL’s revenue has grown over 80% between 2019–20 and 2024–25. In annual terms, that is a compound rate of roughly 13%, faster than HUL’s 9.8%, Nestlé India’s 10.5% and ITC’s 9.7% over the same period, albeit off a smaller base.

TCPL reported a consolidated annual turnover of ₹17,618cr in 2024–25. Its operating margin, what survives from every rupee of revenue after paying for everything, runs at 14–15%. HUL’s is 23–24%.

Closing this gap requires high-margin businesses like Ching’s, Organic India, Soulfull, cold-pressed oil to grow fast enough to become roughly a third of total revenue. Right now, they are 8–9%.

Tea costs, which TCPL cannot control, need to normalise. Integration costs from the 2024 acquisitions need to wind down.

Motilal Oswal projects margins reaching 17% in three years. The path to 20%-plus, where HUL and Nestlé operate, is considerably longer than that.

Return on capital, how much profit a company earns on every rupee invested, tells the same story from a different angle. TCPL’s sits at roughly 10%. HUL’s is 27%. D’Souza points out that the core business, stripped of the 2024 acquisition capital, delivers 30%-plus.

The acquisitions are dragging the consolidated number while they are still being absorbed. Most analysts expect the trajectory to improve. The question is whether it does so within the timeline management has guided.

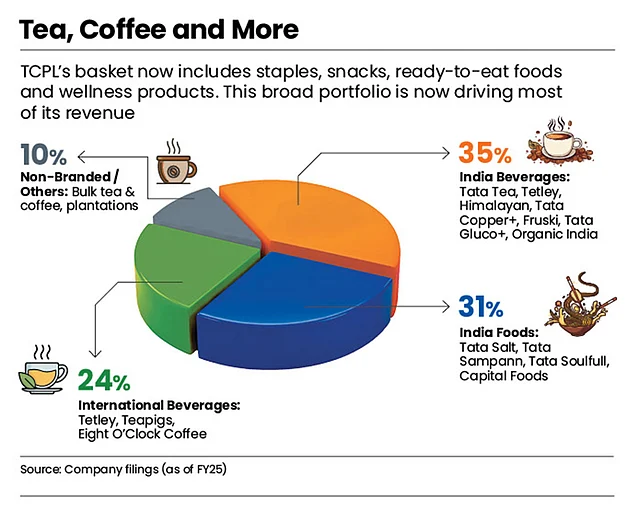

D’Souza describes the portfolio in three segments: the international business: Tetley, steady and cash-generative. The India staples: tea and salt, large but low-margin, subject to commodity costs he cannot control. And the growth businesses: Ching’s, Organic India, Soulfull and cold-pressed oil, which are small today but carry the highest margins and expectations.

“All three pieces need to come together,” says D’Souza.

“Each piece in the portfolio has a very specific purpose,” explains Krishnakumar. International for steady margins. Sampann for growth. Capital Foods and Organic India for both. “The headline target ties it together: a double-digit-plus topline and a bottom line growing higher than that,” he adds.

Today, the portfolio spans tea, coffee, water, ready-to-drink beverages, salt, pulses, spices, ready-to-cook and ready-to-eat offerings, breakfast cereals, snacks and mini meals.

However, the product range is in the food and beverages (F&B) universe. The company does not yet cover much else. “Without personal care or home care, TCPL is not yet a comprehensive FMCG powerhouse,” says Devangshu Dutta, founder of Third Eyesight, a boutique management-consulting firm.

Krishnakumar’s response is: “On a revenue basis, F&B accounts for nearly 80% of the FMCG universe. Outside of F&B, it requires a very different set of skills, a very different DNA.”

TCPL is not making bets in personal-care or home-care segments in the near future.

The Long Game

“There’s no magic breakout moment,” says Krishnakumar. What he points to instead are accumulations: salt crossing million packets a day, the stock market re-rating and the innovation pipeline turning out a new product every week.

The competition, however, is not waiting. HUL’s quick commerce is logging 3% of revenue, growing at over 100%. ITC plans to spend ₹20,000cr over five years with the bulk for foods. Nestlé is deepening its product pipeline.

These rival FMCG companies are now moving faster than they have in years. For TCPL, the race has gotten harder.

At the same time, these giant competitiors have their own challenges. HUL draws only 25% of its revenue from foods. Nestlé is concentrated in dairy and confectionery.

ITC, which is still moving away from tobacco, draws 40% of its revenue from packaged foods and personal care combined.

While these Goliaths have their attention split, TCPL’s focused approach is perhaps the one thing they cannot replicate. “In any category that we have a stake in, we would be among the top three brands,” says a confident D’Souza.

Six years in, the pieces are in place. “Our strategic road map and the strong foundation we have laid for the business have yielded good results…Our overarching ambition is to evolve into a full-fledged FMCG company,” Chandrasekaran said in TCPL annual report 2024–25.

Whether TCPL becomes big and matches his vision is a question the next six years will answer.

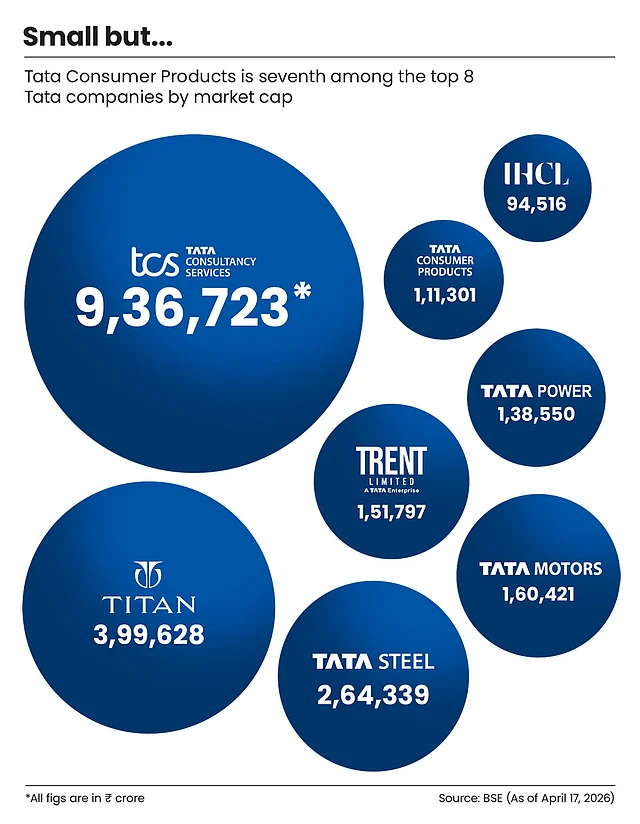

Within the Tata group, TCPL’s revenue ranking may not have moved much: eighth in 2019–20, seventh today. Both profits and market capitalisation have grown more than three times. It’s now worth over ₹1 lakh crore, nearly seven times Tata Chemicals, and more than double that of Tata Communications.

The market is not pricing what TCPL is. It is pricing what it might become. “Because if you’re not in the top three, there is no point,” says D’Souza. The man who chose to walk into the “sleepy company” is not done yet.

(Published in Outlook Business)

admin

March 1, 2026

Apoorva Mittal, Economic Times

1 March 2026

Resshmi Nair, 31, had grown used to the dotted red bumps on her arms. Her dermatologist diagnosed it as keratosis pilaris aka strawberry skin. It is a harmless skin condition that often affects legs and arms but Nair, a Mumbai-based marketing consultant, wanted it gone. She slathered lotions and salves but to no avail. Then she chanced upon an Instagram reel which showed an oil-based in-shower spray that promised to take care of her problem. “It was very tempting as it resonated with a personal concern,” she says. She is now on her third bottle. The bumps haven’t disappeared entirely, but they have become smaller, she says.

Like Nair, there are many who seek solutions tailormade for their beauty bugbears. Consumers who once searched for moisturisers and shampoos now look for niche products for hair and skin. They want to repair skin barrier, tame baby hairs and minimise facial pores.

A new generation of Indian beauty and personal care (BPC) brands are both listening to them and leading them. Focused products, they realise, could help them stand out in a crowded sector dominated by FMCG giants. While problems like acne, frizzy hair and rough skin have always been around, experts say the commercial importance of solving them narrowly and packaging that specificity as a brand strategy have become more intense of late.

India’s direct-to-consumer (D2C) beauty and personal care market—which is heavily invested in micro-problem targeting—is estimated to be $4.5 billion in FY2025, according to consulting firm Redseer. The new-age brands could account for 25-35% of total BPC spends by 2030. “Three major factors have contributed to this: one, the rise of digital medium for both commerce and marketing, which created a segue for new brands to launch and scale; two, younger consumers (Gen Z and young millennials) have become ingredient literate and look for results over broad promises; and three, competitive intensity in the market is pressing brands to position as per the right niches,” says Kushal Bhatnagar, associate partner, Redseer.

The shift is measurable on beauty retailer Nykaa’s platform. “Consumer vocabulary is far more evolved,” says a company spokesperson. Searches driven by specic concerns or ingredients are growing faster than broad category items. While foundational concerns like acne and brightening remain relevant, the platform is seeing strong growth in queries around pigmentation, barrier repair, pore care and specic hair issues. “This fragmentation is actually a sign of a more informed and aware consumer base,” the spokesperson adds.

ZOOMING IN

For young D2C brands, this behavioural shift has opened a narrow but potent entry point. Instead of launching another shampoo or moisturiser, they launch a product targeting a single problem and market it in an easily demonstrable short-video format. In the current beauty landscape, the market has shifted from general solutions to hyper-targeted efficacy.

Moxie Beauty, founded by Nikita Khanna in 2023, illustrates the playbook. Khanna, who previously worked at McKinsey, began with a focus on wavy and frizzy hair, a segment she herself belongs to. But it was one particular styling product, the flyaway hair stick, that went viral, propelling the brand into visibility. She says, “The wavy hair routine required us to educate people, which took time. But one can understand the flyaway wand in five seconds.” And it targeted what she calls a “widely held pain point”. That helped Moxie cut through crowded feeds and end up on consumer shelves. “Being synonymous with a category helps,” she says. “When people want a wax stick or flyaway stick, they search for our brand.”

That shift—from paying for visibility to being searched for directly—is critical in a market where customer acquisition costs (CAC) can be punishingly high. For many D2C brands, launching a sharply defined product is a way to reduce discovery friction and lower early-stage CAC. But a brand cannot be built or scaled on gimmicks, says Khanna. “If you solve only for what will look good in a video and will go viral, you won’t be able to scale. And if it’s a gimmick, people won’t repeat the purchase,” she adds.

Divanshee Jindal, cofounder of the brand The Solved Skin, says companies have to get the “product-communication fit” right. Her brand’s liquid pimple patch, which is designed to mask acne under makeup, is quickly emerging as its hero product. “People get excited when a product feels relatable and authentic,” says Jindal. “A new, convenient format that solves a real pain point makes consumers willing to try a new brand. But if it’s a standard product, say, a salicylic acid face wash, they will often default to a brand they already trust.”

SMALL IS BEAUTIFUL

The idea is to start small but evolve. Moxie, for instance, has moved beyond textured hair into solving broader “Indian hair problems” like damage repair and anti-dandruff that has brought in male consumers as well. “Curly or wavy hair was a huge, underserved problem,” says Khanna. “But the thought was always to solve other problems as well.” Moxie, which recently raised $15 million in a funding round led by Bessemer Venture Partners, says it has crossed Rs. 100 crore in annual recurring revenue on its two-year mark, and is seeing roughly 50% consumers coming back in six months across platforms. However, it says profitability is harder to crack because of intense competition from new brands and changing channel mix.

Mani Singhal, MD of the consulting firm Alvarez & Marsal, points out that most successful D2C brands started out with a sharply defined hero product. “Earlier it was natural vs chemical or price disruption; today it’s much more about efficacy proof, ingredient transparency, visible results and credible

storytelling,” she says.

From the manufacturer’s side, Nishit Dedhia of Kain Cosmeceuticals, a cosmetics manufacturing company, says, “It is easier today for brands to target special concerns. That specificity helps them build a differentiated product earlier on.” Most brands, he explains, x a major problem such as acne, dryness, pigmentation and then layer in a niche twist. Strawberry skin, once not a mainstream concern, is now a category. “People didn’t know the term. Once you give it a name, they identify with it,” he adds.

Dedhia describes the portfolio strategy as 8-2 or 9-1 where eight or nine products are general, incremental variations of core needs, while one or two are “category-building products” that require significant consumer education or product communication but create their own search demand. “That is the only way you get out of the vicious cycle of paying for visibility,” he says. “When people search for your brand directly, CAC comes down.”

Devangshu Dutta, founder of management consulting firm Third Eyesight, says micro-problem framing is “co-created” by consumers and companies. “The fragmentation is real, but the language used to describe it is heavily brand-driven,” he says. Terms like “strawberry skin” or “glass skin” correlate with influencer campaigns but label pre-existing dissatisfactions that mass products did not address sharply.

However, sometimes, in the race to differentiation, brands go for outlandish ideas. Dedhia says brands increasingly approach manufacturers with amusing asks in the quest to stand out. For instance, beard fillers packaged like mascara or plumpers for face and neck.

PRODUCE & PERISH

The problem is that the mortality rate of skincare brands is very high in India. Dedhia estimates that around 60% companies shut down in three years. Many brands burn through capital chasing ads and trends without building repeat customers or a community.

“For a brand to cross over from being a curiosity-driven purchase to being part of a regimen needs a minimum 25-30% of customers showing up as repeats after three months, while truly successful brands reach higher repeat numbers,” says Dutta.

Subscriptions are an even stronger test. “Generic formulations, me-too products and influencer spends can get you first users, but repeats will happen only from the user getting demonstrated value,” says Dutta.

But growth does not equal stability. CAC typically starts low for niche products, rises during scaling-up and stabilises only if organic demand takes over, says Bhatnagar of Redseer. Quick commerce accelerates discovery but compresses margins due to the high commission rates on these platforms, promotional expectations and lower average order values.

Singhal, who says a consolidation phase is underway, adds: “Niche entry can work extremely well if the problem is frequent enough and the solution is demonstrably effective.” Durable brands deliver consistent performance, build adjacencies beyond the first niche and maintain disciplined unit economics.

“If repeat rates don’t stabilise, economics becomes very challenging, very quickly.”

PERSONALISATION AHEAD

For Aparna Saxena, founder of Delhi-based beauty brand Antinorm, the next decade will be defined by even greater personalisation. Her brand has multifunctional products that are timesaving. Saxena says she surveyed about 250 women above 25 years of age and found that five-step routines typically do

not last after two months. Antinorm’s architecture rests on multifunctionality, like a leave-in cream that doubles as heat protectant and promises a “presentable” hair look without a blow-dry. Its most popular product is a spray that cleanses and moisturises, which they dub as “instant shower” or “facial in a flash”.

She says the brand, which launched in July last year, will close next fiscal with about Rs. 25 crore in revenue. Repeat rates are currently under 25% “because the denominator is expanding rapidly”, she adds. “Between 2020 and 2025, customers moved away from incumbents and got used to having options and trying newer brands,” she says. “Now they have routines in place. The next five years will be defined by more and more personalisation and micro-problem solving.” The beauty is about to go really skin deep.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

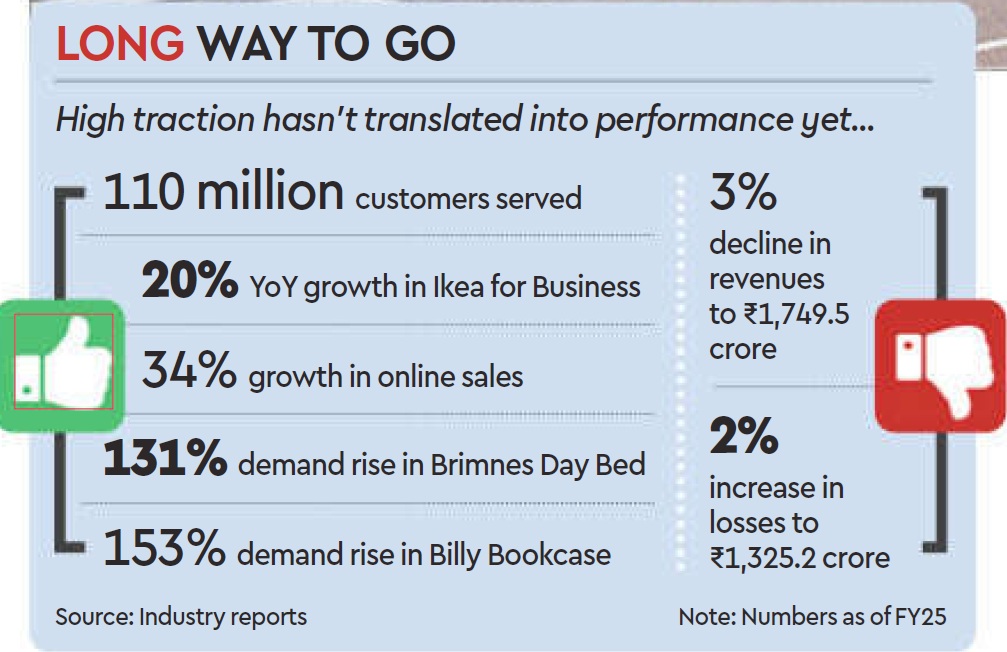

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)