admin

May 6, 2026

Vaeshnavi Kasthuril, MINT

Mumbai, 6 May 2026

Fashion retailers are speeding up deliveries to keep pace with instant-gratification shopping driven by quick-fashion startups, with established players and newer brands taking sharply different approaches.

For example, brands such as Biba and The House of Rare have adopted a more calibrated, infrastructure-led strategy rather than a rapid overhaul of existing store networks. “We’ve been doing this in a very soft way but not necessarily from the same stores because that affects the customer experience,” said Siddharth Bindra, managing director of Biba. Bindra said using retail stores as fulfilment hubs for rapid delivery creates operational constraints, particularly given store sizes and layouts. “We don’t have very large stores; they are anywhere between 1,000 and 2,000 square feet. So that’s not the right efficiency,” he said.

Instead, the brand is evaluating a hub-based model in cities with higher store density, enabling faster deliveries without disrupting stone operations. “If we do, it will be though proper hubs in cities where we have four to five stores, where we would start with quick commerce and accelerate it,” he said. This could enable same-day or two to three-hour deliveries.

The House of Rare, which houses Rare Rabbit (men’s urban fashion) and Rareism (women’s fashion), is adopting a similar approach, evaluating city-levee fulfilment hubs in markets with higher store concentrations to enable faster deliveries while keeping retail outlets focused on walk-in consumers.

The strategy reflects a broader attempt among legacy retallers to belance speed with experience, rather than treating stores as Interchangeable logistics nodes. “The eventual goal is the customer, but it creates a lot of difference in the customer experience” Bindra said, pointing to the trade-offs involved.

Different take

In contrast, some brands are moving more aggressively to integrate stones directly into fulfilment networks.

Libas, an initial public offering (IPO)-bound apparel company, is networking its operating model to plug its physical retail network Into a faster, hyperlocal delivery system.

Earlier, the 12-year-old company followed a more traditional structure. Online orders were largely fulfilled from central warehouses and delivered over a few days, while stores primarily served walk-in customers, with the two channels operating independently.

That is now changing. Libas is using its stores and nearby warehouses as local fulfilment points, allowing it to service orders within a much smaller delivery radius,

“At Libas, the time frame will be approximately 60-90 minutes at the max,” said Bhavay Pruthi, senior vice president, e-commerce and product management.

The rollout has been gradual, starting with select cities and limited catchments, typically within a 7-10km radius, where delivery timelines can be tightly controlled. It has also narrowed the product mix initialy to itams that are easier to move quickly.

The push comes as consumer expectations around delivery timelines extend beyond groceries into fashion, forcing brands to rethink supply-chain design,

Rise of quick fashion

The urgency to adapt is being shaped by a surge in quick fashion startups that are attracting investor attention despite heavy cash burm.

The segment has seen a flurry of funding in recent months, with Zilo raising $15.3 million in February led by Peak XV, and Knot securing $5 million in a round led by 12 Flags in December.

It has also evolved rapidly. Quick-commerce platforms such as Zepto, Instamart and Blinkit initially offered a limited range of basic fashion items for last-minute purchases. This has since expanded into a more specialized category, with vertical players offering wider assortments across party, work and occasion wear with rapid delivery timelines.

New entrants are pushing the model further. Wydo, for instance, promises deliveries within 15 to 30 minutes in Bengaluru, while Gen Z-focused offerings such as Newme’s Zip and Snitch Quick are building businesses around near-instant fashion access.

Myntra’s rapid commerce division, M-Now, accounted for about 10% of orders in the locations where it was available as of last November.

“This is the new kind of experience that customers are expecting,” Pruthi said.

Libas is working with third-party logistics providers and quick commerce platforms for the last-mile delivery, while focusing internally on faster picking, packing and order routing. Quick commerce currently accounts for about 2% of its overall sales, with scope to grow as the model scales..

Early results, however, highlight the trade-offs. “We saw very good sell-throughs for e-commerce, but it was cannibalizing existing store sales,” Pruths said.

There are also fimits to what customers are willing to buy through rapid-delivery channels. “Customers do not have the confidence to spend 15,000 for a fashion product from a quick- commerce channel,” he said.

To address this, Libas has tightened delivery radii, curated a more suitable product mix, and is testing stores with attached dark-store infrastructure to balance walk-in and online demand.

Experts say these challenges are structural.

“If you look at fashion, it’s extremely unpredictable, and if you are a brand across multiple products, it’s complicated process,” said Devangshu Dutta, founder of management consulting firm Third Eyesight.

While demand for faster deliveries is rising, it remains a small slice of the overall market, with profitability still uncertain due to limited assortments and high fulfilment costs. For traditional retailers, adopting the model requires a fundamental reworking of supply chains that were not built for near-instant delivery, Dutta added.

(Published in MINT)

admin

February 11, 2026

Vaeshnavi Kasthuril, Mint

Bengaluru, 11 February 2026

Sales of winter wear were underwhelming for the second year in a row as an unusually delayed and milder winter disrupted demand for heavy winter wear, particularly in north and west India, executives at two of India’s top clothing retailers said. Initial optimism for a bumper season this year compounded the disappointment for retailers.

While early signs of a La Niña—a weather pattern typically known for bringing freezing temperatures to India—triggered some early buying in the previous quarter, the season remained unusually mild, leaving stores with a surplus of winter clothing. Excess rainfall and cyclonic activity during the festive period in parts of eastern and southern India further weighed on seasonal buying, compounding the pressure on winter sales which are typically front-loaded.

This slump is particularly painful because winter sales are the industry’s largest annual driver. These months coincide with India’s massive wedding season, when spending peaks. Together, they account for roughly 20% of total yearly revenue for apparel companies, according to industry estimates. India’s apparel market was estimated to be worth more than ₹1.9 trillion in FY25, of which 41% was organised, credit ratings firm CareEdge said in January 2026.

V-Mart: margin over volume

Lalit Agarwal, managing director of V-Mart Retail, said, “Northern India saw a delayed or milder winter initially, leading to dispersed demand for heavy winter wear. Winter demand was definitely delayed a little bit—it didn’t get lost, but it was erratic.” He added that while festive demand held up, “demand visibility was uncertain, particularly in winter-led categories, and we consciously chose to protect margins rather than chase volumes.”

V-Mart’s revenue grew a little over 10% year-on-year to ₹1,126.4 crore in Q3 from ₹1,023.7 crore a year earlier and ₹889.05 crore in the third quarter of FY24, but this growth was largely driven by wedding and festive-season clothing, executives at the company said.

Anand Agarwal, chief financial officer of V-Mart Retail, said despite forecasts of a strong, early winter, “peak winters were delayed across North and West India, leading to a lull post-Diwali.” He added, “While the festive period went off reasonably well, winter demand did not pan out as anticipated,” attributing the softer sales to fewer peak winter days and unusually warmer temperatures.

Despite the delayed demand, the company managed to avoid a build-up of unsold inventory during the quarter. “Inventory health remained strong despite the delayed winter, and in some categories we were even short of inventory,” said Anand Agarwal, indicating that the eventual dip in temperatures led to a sudden pick-up in demand in select winter categories rather than excess stock.

Winter-led assortments continue to account for a sizeable share of the company’s quarterly sales, underscoring its sensitivity to weather patterns. “Winter and pre-winter categories accounted for about 40-45% of the overall mix during the quarter, and this share rose to over 60% during peak winter weeks in December,” said Agarwal during the third-quarter earnings call. The higher share of winter wear sales during peak weeks helped cushion margins, even as volumes remained below expectations. Lalit Agarwal said the company refrained from aggressive discounting amid uncertain demand. “Higher full-price sell-through during the winter quarter supported margins, as we did not undertake aggressive discounting,” he said.

Vishal Mega Mart: the late recovery

Gunender Kapur, managing director and chief executive officer of rival Vishal Mega Mart, said delayed winters usually force retailers to push promotions to ensure that they don’t carry forward all that merchandise, because the next opportunity to sell it would be the following year.

Despite this, the company’s performance held up, he said, highlighting that winter sales achieved robust double-digit same-store growth for the entire season and the full quarter, effectively overcoming the sluggish demand during December. Kapur noted that demand for winter clothing increased significantly in January, adding, “Winter merchandise is still selling well, both in our stores and in other stores, we believe.”

Vishal Mega Mart reported revenue growth of about 17% to ₹3,670.3 crore in Q3 FY26 from ₹3,135.9 crore in Q3 FY25 and ₹2,623.5 crore in Q3 FY24, largely on the back of wedding and festive-season demand.

Kapur said the company was unsure whether there would be significant unsold winter merchandise at the end of the season, adding that maintaining pricing discipline helped protect profit margins. “Merchandise that sells in December typically fetches a higher price than January merchandise for winter because sales often begin by late December or early January,” he said. “In our case, there was no problem. We achieved same-store sales growth of over 10%, even with the winter merchandise we purchased for the autumn-winter season.”

V2 Retail: the outlier

In contrast, V2 Retail recorded strong performance in the third quarter, largely driven by winter wear. Revenue surged nearly 60% year-on-year to ₹929.2 crore in Q3 from ₹590.9 crore a year earlier. This is perhaps because V-Mart and Vishal Mega Mart are more concentrated in north and central India, where winter demand was more uneven this season, while V2 has a stronger presence in eastern and north-eastern markets, including Bihar, Jharkhand, Odisha and Assam.

Managing director Akash Agarwal said the early onset of winter led to a “very good season” for the company. He noted that winter garments typically command a much higher average selling price (ASP) than summer products, which resulted in a visible bump in average bill value during the third quarter, led by higher sales of jackets and sweaters. Agarwal said this high-ASP, high-margin category accounted for the bulk of Q3 sales and was a key driver of the company’s same-store sales growth.

A worsening problem?

Two straight years of sluggish sales because of erratic winters highlight broader challenges around climate change for apparel retailers, which peg their inventory based on weather patterns and demand.

“Seasons have always been inherently unpredictable, and retailers have never been able to forecast with certainty how cold or warm a winter will be or how long it will last,” said Devangshu Dutta, founder of Third Eyesight, a consulting firm. However, he said that the challenge has intensified over the past 15-20 years as apparel businesses have scaled up and expanded their store footprints nationwide, stretching product development and supply chains over several months.

“No matter how hard you work on the plan, your forecast will always be wrong. You will either overshoot or undershoot,” Dutta said, adding that this leaves retailers grappling with either shortages or excess stock. Winterwear, he said, is particularly vulnerable because it has a higher value per unit, a much shorter selling window, and a smaller market, factors which together create a “humongous problem” for retailers.

Data from a World Meteorological Organisation report published on 16 January showed that 2025 was among the three warmest years on record worldwide, continuing a decade-long streak of exceptional heat despite the cooling La Niña phase. This is a clear sign that background warming from greenhouse gases is overwhelming natural variability, the report said. It suggested that climate change will intensify seasonal shifts and extreme weather in the years and decades ahead, making industries tied to seasonal patterns, such as winter apparel, increasingly vulnerable to unpredictable weather swings and weaker cold spells.

(Published in Mint)

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

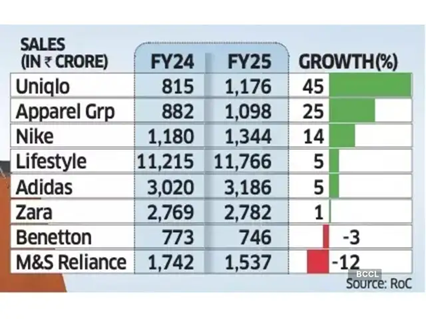

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

September 24, 2025

Shabori Das & Sagar Malviya, Economic Times

Bengaluru/Mumbai, 24 September 2025

Chinese fast-fashion platform Shein plans to triple the number of launches in India and shrink its design-to-launch timeline by a third to deepen its push into an increasingly competitive market, a top official said.

The company, which re-entered India through a partnership with Reliance Retail in February this year, said it is overhauling its supply chain to enable faster turnaround times. To achieve this, it has moved away from large-scale manufacturing hubs to smaller production lines with each line focused on creating a single new design daily.

“Our current timelines, measured from ‘thought to site’, stand at 46 days. We are targeting 30 days,” said Vineeth Nair, chief executive of Reliance’s fashion platform Ajio that steers Shein in India. “We currently deliver 320 styles a day – about 10,000 a month – and plan to scale that to over 30,000 styles monthly in the coming months,” he told ET.

Speaking about the speed of manufacturing, Nair said, “We quantify our options in terms of production lines, with each line optimised to deliver one design option per day, rather than factories. Some of our large production units have been repurposed into multiple lines.”

Shein first launched in India in 2018 with its own online shop. However, the app was banned by the Ministry of Electronics and Information Technology (MeitY) along with TikTok, WeChat and over 55 other Chinese apps.

One of the primary issues and controversies surrounding Shein’s India operations was the use of the consumer data by the Chinese apparel retailer.

Under the current partnership model, Reliance Retail is operating Shein under licensing agreement and ensures complete customer data ownership as per the company.

Unlike international markets, Shein India products are made in India.

“It’s still early days – just about three months since we introduced Shein to the India Gen Z,” Nair said. “And we are still in the process of adding multiple products, which we intend to do in the next few months.”

He said the brand is witnessing two million daily average users, dominated by 21-year-old women who account for 62% of the traffic.

Shein, the world’s biggest ecommerce-centred fashion retailer, however, may find it hard to replicate its global success in India, according to Devangshu Dutta, founder of retail consulting firm Third Eyesight.

“Shein’s edge internationally has been its speed of dropping its products, and the width of its product category. The India model is not the same. The India model of fashion is slower, and the product category width is not as large,” he noted. “Hence, the brand will in all probability end up competing with the already established market like Myntra, Zudio and the likes.”

(Published in Economic Times)

admin

May 23, 2025

By Kunal Purohit and Ananya Bhattacharya, Rest of World

Mumbai, India, 23 May 2025

Online retail continues to elude India’s richest man.

The Shein India app, launched by Mukesh Ambani’s Reliance Retail in partnership with the Chinese fast-fashion giant, has struggled to gain traction in a market where Amazon and Walmart have been fighting neck-to-neck for nearly a decade. Downloads for Shein India nosedived from 50,000 a day shortly after its launch in early February to 3,311 in early April, according to AppMagic, a U.S.-based app performance tracker.

In April, when U.S. tariffs hit China, the app saw renewed interest as it was in the news, but experts are unclear on whether this growth is sustainable.

“Unlike earlier times, now … [the] market is saturated with multiple options and offers, and user interest can quickly dwindle,” Yugal Joshi, partner at global research firm Everest Group, told Rest of World.

Kushal Bhatnagar of Indian consulting firm Redseer, however, sees the late-April spike as a healthy sign, given that Reliance has yet to run paid marketing campaigns for Shein.

Reliance Retail declined to respond to Rest of World’s queries about its partnership with Shein.

Reliance launched Shein for India five years after the original Shein app was banned in the country over border tensions with China. But the Shein that has returned is entirely separate from Shein’s global platform: Rather than selling made-in-China clothes and accessories directly to consumers, Shein now operates as a technology partner, while Reliance Retail handles the heavy lifting — from sourcing and manufacturing to distribution. All consumer data is managed by the Indian company.

The partnership is part of Ambani’s broader effort to overhaul his retail business, whose valuation fell to $50 billion in 2025 from $125 billion in 2022. Although the company has made a push into digital platforms like JioMart, Ajio, and most recently Shein India, the bulk of its retail revenue still comes from its 18,000 physical stores.

Lagging behind Amazon and Walmart-backed Flipkart, which together control nearly 60% of India’s e-commerce market, Reliance has spent years trying to break into the sector. Between 2020 and 2025, Ambani’s group acquired majority stakes in companies spanning digital services, online pharmaceuticals, and quick commerce. But the investments have yet to position Reliance as a serious challenger to Amazon and Flipkart.

Analysts say the Indian behemoth hopes to leverage Shein’s artificial intelligence-powered trendspotting and automated inventory systems to pursue an ambitious goal: capturing a major share of India’s e-commerce market, projected to hit $345 billion by 2030.

According to Kaustav Sengupta, director of insights at VisionNxt, an Indian government-funded initiative that uses AI to forecast fashion trends, such a model is likely to make good use of Reliance’s humongous customer data sets: more than 476 million subscribers for its Jio telecom brand, 300 million users for e-commerce platform JioMart, and 452 million subscribers for its news and entertainment portfolio, consisting of 63 channels, a streaming service, and digital news outlets.

“With these data points, Reliance wants to now sell fashion products, so all it needs is a system where it can feed all these data points,” Sengupta told Rest of World. He said the model would be able to predict best-selling products and suggest the right prices for them.

The original Shein app uses AI-driven models for intelligent warehousing and to spot customer trends before manufacturing a new product. It scales the manufacturing up or tweaks the designs based on the feedback. At any given time, the Shein website has a catalogue of more than 600,000 items. Its Indian iteration does not match up, according to reviews on the Google Play store. Several customer reviews for Reliance’s Shein app are critical of higher prices and reduced options. The app’s rating hovered at 2 out of 5 until February; in May, it climbed to 4.4, but reviews were still a mixed bag.

Reviews of the Indian app highlight the disparity with Shein’s global version, criticizing higher prices and a reduced selection of categories and styles.

As of April 25, Reliance Retail said only 12,000 products were live on Shein India, a stark contrast to the 600,000 items available on Shein’s global platforms. While Shein is reportedly set to debut on the London Stock Exchange this year, Ambani’s years-old promise to take Reliance Retail public remains unfulfilled.

Reliance Retail, which accounts for around 30% of the conglomerate’s overall business, is facing a slowdown in annual growth. Its sales rose just 7.9% in the fiscal year ending March 2025, down from 17.8% the previous year. Meanwhile, shares of rival Tata Group’s retail and fashion arm, Trent, have soared by 133%.

“Reliance would have looked at reviving that momentum and riding on it, while for Shein, adding India back on its portfolio of markets could be a plus point before its proposed public listing,” Devangshu Dutta, founder of Third Eyesight, a brand management consultancy that has worked with various global e-commerce brands including Ikea, told Rest of World.

A Reliance Retail official privy to information about its fast fashion expansion plans told Rest of World the partnership with Shein also hinges on global manufacturing ambitions as the Chinese company is trying to “source its products from other countries like India” to meet the “additional demand that is coming from newer markets.” Reliance Retail has tapped a network of small and midsize Indian manufacturers to locally source products, and its subsidiary Nextgen Fast Fashion Limited is leading the charge. “We need to first scale up our domestic manufacturing, before our partnership starts manufacturing for global markets. Let us see how that goes, first,” the official said, requesting anonymity as he is not authorized to share this information publicly.

India’s Gen Z population is at 377 million and counting, and their spending power is set to surpass $2 trillion by 2035, according to a 2024 report by Boston Consulting Group. Every fast-fashion retailer wants to capture this market, but it “is very new even for Reliance,” Rimjim Deka, founder of Indian fast-fashion platform Littlebox, told Rest of World.

Deka said smaller brands like hers “just see [a trend] and implement it,” which could take a large conglomerate months to do, by which time the trend may have lost relevance.

Reliance’s previous attempts to attract young shoppers with clothing brands like Foundry and Yousta failed to find much success. Anandita Bhuyan, who works in trend forecasting and product creation for fast-fashion clients like H&M and Myntra, told Rest of World the company has struggled to effectively leverage consumer data and target India’s youth.

According to the Reliance Retail official, the company is confident that if “there are 10 existing brands, the 11th brand will also get picked up as long as there is value and there is fashion.”

“Shein already has a recall among the youth. It gives us yet another brand in our portfolio through which we can cater to the youth,” the official said.

Shein was built in China on the back of more than 5,400 micro manufacturers — a scattered and loosely organized network of small and midsize factories.

In January this year, on a visit to China, Deka met with manufacturers working for Shein and Temu. On the outskirts of Guangzhou, Deka saw factories set up in areas that appeared residential, with “women sitting inside houses” making clothes.

“The tech is built in a way that somebody sitting there is able to see that, okay, next 15 days or next one month, how much I should be making … that is the kind of integration they have done,” Deka said.

Deka told Rest of World this model is easier to replicate at a smaller scale. “Me, coming from [the] supply chain industry, I understand that it is much easier for a brand like us because we are at a very smaller scale. We can still go to those people, we can still build it in a very unorganized way and then pull it off,” she said. Her company’s annual net revenue is 750 million Indian rupees ($8.6 million).

“[But] somebody like Reliance, they just cannot go haphazard here. … It has to be always organized,” Deka said.

Shein moved its headquarters to Singapore sometime between late 2021 and early 2022, a strategic departure to distance itself from its Chinese origins and facilitate hassle-free international expansion amid the U.S.-China trade war.

India is part of Shein’s wider strategy to diversify its supply chain — one that also includes a newly leased warehouse near Ho Chi Minh City in Vietnam, and efforts to establish alternative manufacturing hubs in Brazil and Turkey.

But in India, Reliance needs Shein as much as Shein needs Reliance for its global pivot. According to Bloomberg, Reliance Retail is focusing on creating leaner operations to weather a wider consumption slump in the Indian economy.

“It remains to be seen whether the Reliance-Shein combine can deliver on the brand’s promise with a wide range of products, fast and on-trend,” Dutta said. “In the years that Shein has been absent, the Indian market has evolved further, competition has intensified, and past goodwill is not enough to provide sales momentum.”

Kunal Purohit is a freelance journalist based in Mumbai, India.

Ananya Bhattacharya is a reporter for Rest of World covering South Asia’s tech scene. She is based in Mumbai, India.

(Published in Rest of World)