admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

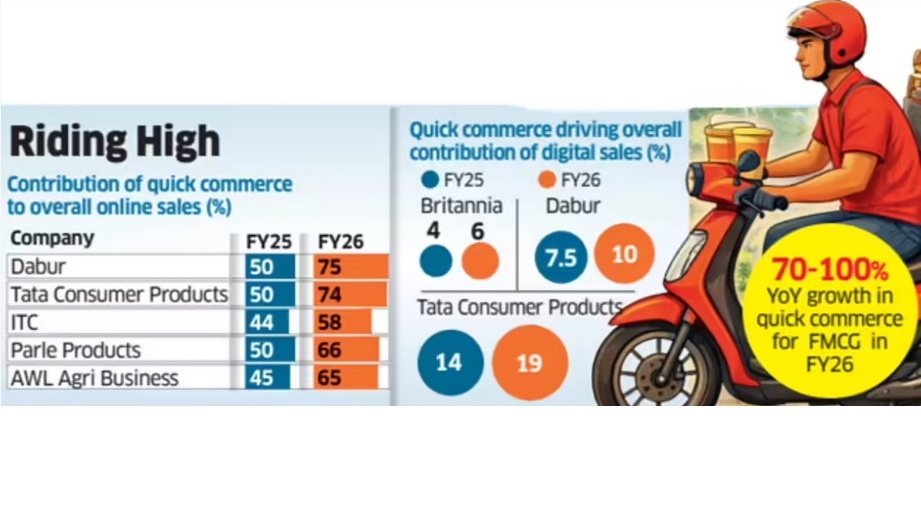

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

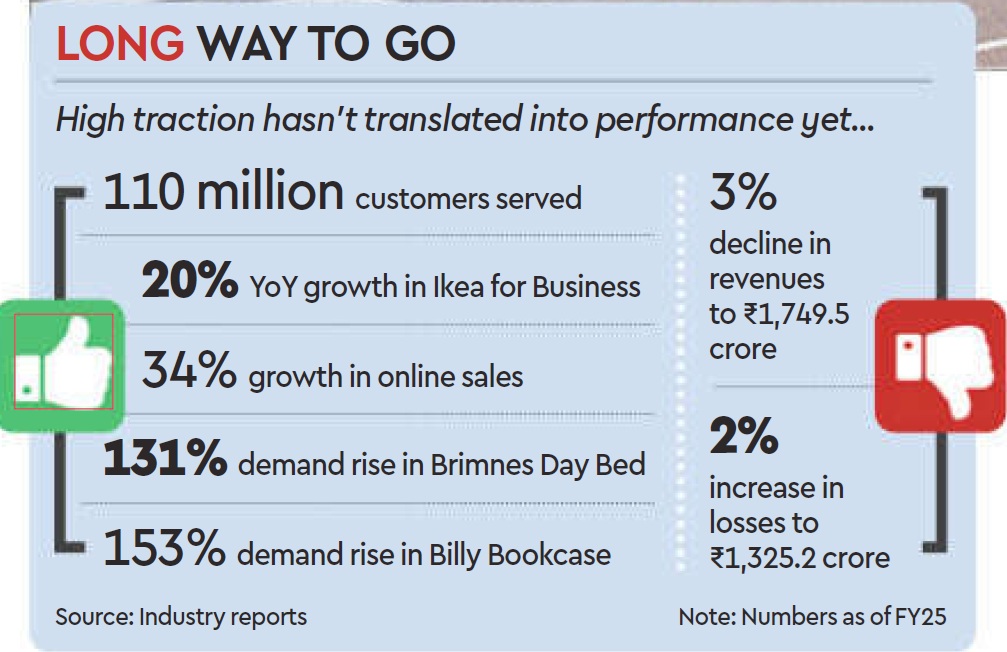

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

January 6, 2026

Saumyangi Yadav, Entrepreneur India

Jan 6, 2026

After years of rapid growth and a sharp reset, India’s direct-to-consumer (D2C) sector is expected to settle into a more balanced phase. The period of easy funding, aggressive customer acquisition and scale-at-all-costs expansion is clearly over, experts suggest. Now, what lies ahead in 2026 is a shift towards steadier growth driven by better execution, stronger retention and clearer brand positioning.

According to Bain and Flipkart, India’s e-retail market is projected to reach $170–190 billion in GMV by 2030, driven by a growing online shopper base and evolving commerce models. As adoption deepens across Tier-2 and Tier-3 cities, high-frequency categories such as grocery and lifestyle are expected to drive a larger share of growth, making repeat purchase and habit formation critical for D2C brands.

Against this backdrop, 2026 is shaping up as the year when D2C brands are judged less on ambition and more on outcomes.

A Post-Hype Phase of D2C

Industry observers say the D2C ecosystem has clearly moved beyond its hype-driven phase. Devangshu Dutta, Founder and Chief Executive of retail consultancy Third Eyesight, describes the current moment as one of structural correction rather than contraction.

“India’s D2C ecosystem is in a post-hype phase where growth may be slower but structurally healthier,” Dutta says, adding, “Earlier growth cycles prioritised visibility and sales at the expense of profitability and consistency. Now, success is being measured by repeat rates, contribution margins and the ability to fund growth internally.”

Tighter funding is also driving this shift. With D2C investments slowing and overall capital remaining cautious, brands are now being pushed to show predictability rather than promise. Tracxn data shows Indian D2C startups raised USD 757 million in 2024, significantly lower than previous years, while overall PE-VC investments in India remained flat at USD 33 billion in 2025, according to Venture Intelligence.

As a result, Dutta notes that many D2C companies are rationalising portfolios, tightening inventory cycles and optimising supply chains. Marketing strategies, too, are evolving, with greater emphasis on retention, community-building and owned channels instead of discount-led growth.

Uniqueness Will Define Winners

If capital discipline is one defining force, speed is another. Harish Bijoor, business and brand strategy expert, argues that D2C’s next phase will be shaped by how brands respond to a faster, more fragmented commerce environment.

“The e-commerce revolution led to a more refined orientation of D2C, and that has now given way to a q-commerce revolution that is even faster,” Bijoor says, adding, “The D2C revolution is going to be leveraged by speed. A whole host of players will invest time, energy and innovation into this.”

In Bijoor’s view, traditional e-commerce is now the slowest layer in a spectrum where quick commerce is the fastest, and D2C sits in between. In such a landscape, competing purely on price is no longer sustainable. He believes differentiation will increasingly come from uniqueness and premium positioning rather than ubiquity.

“When you know that you get a particular great-tasting biryani at just one place with no branches, you will go to that place. That uniqueness is what will distinguish D2C commerce in the future,” he says.

Bijoor adds that many D2C brands have been trapped in price wars under the guise of differentiation. He also argued that brands that premiumise and resist excessive omnichannel dilution are more likely to build desirability and long-term value.

Consumers Move Beyond Metros

Structural shifts in demand are reshaping how and where D2C brands grow. India now has one of the world’s largest and most diverse online consumer bases, with growth increasingly driven by Tier-2, Tier-3 and smaller towns rather than metros alone. Internet adoption continues to deepen across rural and semi-urban India, expanding the addressable market well beyond early digital buyers.

This widening base is changing the nature of growth. Consumers are becoming more deliberate in how they spend, weighing value, quality and trust more carefully than before.

As Devangshu Dutta notes, Indian consumers have always been discerning, but rising living costs and economic uncertainty have made them even more thoughtful, pushing brands to earn repeat demand rather than rely on impulse or discount-led purchases.

“Value is not just about discounts,” he says. “It’s a balance of price, performance and trust. For D2C brands, repeat consumption has to be earned through consistent quality, transparent pricing and dependable service.”

High-frequency categories such as grocery, lifestyle and general merchandise are expected to drive much of this expansion. Bain estimates these segments will account for two out of every three e-retail dollars by 2030, reinforcing the importance of habit formation and retention-led models.

Quick Commerce Expands Discovery, Not Profitability

Quick commerce has emerged as a powerful but complex growth lever for D2C brands. The format now accounts for a significant share of India’s e-grocery demand and has scaled into a multi-billion-dollar market, becoming a key discovery channel for food and everyday consumption brands.

However, expansion beyond metros remains challenging. RedSeer data shows non-metro markets contribute just over 20 per cent of quick commerce GMV, even as platforms scale to over 150 cities, with breakeven economics in smaller towns requiring significantly higher throughput.

Praveen Govindu, partner at Deloitte India, cautions that while quick commerce has helped many D2C brands gain discovery, particularly in food and beverage, it is not a sustainable growth engine on its own.

“From a customer acquisition standpoint, quick commerce is not fundamentally different from traditional e-commerce,” Govindu says, adding, “It is an expensive channel, and competition will only intensify. Over the long term, brands cannot rely on burning capital there.”

Omnichannel Enters Its Toughest Phase Yet

As digital acquisition costs rise, India’s ad market is projected to grow nearly 8 per cent in 2025 to Rs 1.37 lakh crore, with digital accounting for almost half of the spends, brands are being pushed to diversify distribution. Yet omnichannel presence alone is no longer enough.

“Many brands talk about omnichannel, personalisation and seamless journeys, but in practice these efforts are still disjointed. In 2026, the focus will shift from intent to execution,” Govindu says.

RedSeer projects India’s retail market to cross USD 2 trillion by 2030, with nearly 90 per cent of consumption still happening offline. For D2C brands, this makes offline expansion unavoidable, but success will depend on consistent execution across pricing, inventory, service and communication.

Consumers, Govindu notes, do not consciously differentiate between online, offline or social platforms. “They simply want a consistent experience,” he says. “Even small inconsistencies can erode trust.”

AI-Led Discovery and Experience

Perhaps the most transformative force shaping 2026 will be the evolution of buying journeys themselves. Govindu sees the rise of AI-led and agentic commerce as a major inflection point.

“Conversational platforms and AI-driven assistants will increasingly influence discovery, purchase, fulfilment and post-sales experiences. What earlier happened across multiple touchpoints is now beginning to happen in one place,” he says.

This convergence amplifies the importance of content-led discovery, owned data and deep consumer understanding. Brands that can unify storytelling, commerce and service into a coherent narrative are more likely to build loyalty in an environment where switching costs are low and alternatives are abundant.

Whether growth comes through D2C websites, marketplaces, quick commerce or offline stores, experts agree that the real differentiator will be a brand’s ability to build durable consumer relationships. As investors shift focus from short-term metrics to long-term value creation like retention, margins and brand strength, the next phase of India’s D2C story is less about rapid expansion and more about refinement.

(Published in Entrepreneur India)

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

admin

August 18, 2025

Hiral Goyal, The Morning Context

18 August 2025

A trend that has been playing out through big and small changes over the last two decades is that in urban India the kirana store is easily replaceable.

When it comes to buying groceries, urban Indians have a number of options. They can visit a fancy supermarket run by a conglomerate or order online through a number of e-commerce and instant-delivery companies. And if the above doesn’t seem easy enough, they can hop over to a nearby mom-and-pop store.

It would appear it is now the turn of smaller towns in the country to witness the kirana disruption. Even though 99% of grocery shopping in these tier-3 cities is done through neighborhood general stores, there are startups that believe this is an outdated and inefficient form of retail and a change is in order.

One such company is SuperK. The startup’s mission is to build a grocery store model in small towns that has all of the advantages of modern retail packed in a compact 800-square-foot store. This is what Anil Thontepu and Neeraj Menta had set out to do when they founded the company in 2019. The idea was to bring a modern trade-like grocery shopping experience to small-town India a wide assortment of products at a better value.

“There is a cost-efficient world of general trade and a customer-loving world of modern retail,” says Thontepu. “We wanted to see if we can bridge this gap…and do something for the small-town people by bringing the best of both these worlds.”

Over the past five years, the Bengaluru-headquartered startup has opened over 130 stores across 80 towns in Andhra Pradesh. And it doesn’t want to stop there. The company wants to expand to another 300 towns in Andhra Pradesh and nearby states of Karnataka and Telangana over the next 24, months. That’s quite an ambitious target. But the founders believe the market size for Superk is so large that they should be able to build a Rs 2,000-3,000 стоore ($228-342 million) annual business from Andhra and Telangana alone.

To fuel this expansion, Superk raised Rs 100 crore ($11.7 million) in Series B funding last month. The round, led by Binny Bansal’s 3STATE Ventures and CaratLane founder Mithun Sacheti, valued Superk at 2-2.5x its previous valuation of Rs 160 crore (about $18.25 million) in 202/

Now, Superk is not entirely unique. It competes with startups like Frendy, Apna Mart and Wheelocity, which are also trying to organize the retail market in India’s smaller towns. What sets SuperK apart is its larger, bolder approach. Grocery chain Apna Mart, for instance, runs franchisee stores in tier-2 or tier-3 markets and also offers 15-minute home delivery, SuperK’s focus is only on supermarkets. Frendy operates mini-marts and micro-kiranas in villages and towns with fewer than 10,000 people, but SuperK targets small towns with populations between 20,000 and 500,000. And Wheelocity supplies only fresh produce to rural areas, while Superk sells dry groceries as well as packaged consumer goods.

This rather radical shift in focus-away from tier-1 and tier-2 cities-ties in with India’s changing consumption pattern. “Consumer mindsets are changing even in smaller cities,” says Devangshu Dutta, founder and chief executive of Third Eyesight, adding that these consumers are beginning to favour more modern retail environments. And NielsenIQ’s latest report says rural markets in India grew twice as fast as cities between April and June 2025.

In this landscape, SuperK fits like a glove, with its franchise-first approach. Thanks to an asset-light model, the company has the agility to go deeper into smaller towns.

But it won’t be all that easy either. As Dutta says, “Changing grocery habits is a long, capital-intensive game.” Moreover, big retail chains are also jumping on the bandwagon. Hypermarket chain Vishal Mega Mart, for instance, already operates 47% of its stores in tier-3 cities and plans to expand into cities with populations exceeding 50,000. Supermarket chain operator DMart is also focusing on tier-2 and tier-3 cities.

However, Superk founders believe they are prepared for the challenge. Menta says the startup has arrived at a business model that is scalable, sustainable and, more importantly, offers value to its customers.

It’s too early to say whether they will be successful in this endeavour. That said, SuperK appears to have built a smart retail business for small-town India.

Refining small-town retail

SuperK’s founders have drawn inspiration from domestic and international retail chains like DMart and Costco. But they haven’t duplicated their strategies and made their own tweaks instead. For instance, large retail chains usually run company-owned and company operated, or COCO, stores. Though this approach is more cost-intensive than the franchise model, it allows a company to ensure a uniform customer experience across all outlets:

Superk doesn’t do that. It runs only franchise-owned and franchise-operated (FOFO) stores, which are no bigger than 800 sq ft. The company is not the first to have experimented with this model, but Thontepu believes that everyone else before them “did not try with the right spirit”. A franchise-owned store, argues co-founder Menta, is run differently from a company-owned store one has to keep in mind the store owner’s incentives, needs and concerns.

Under the franchise model, entrepreneurs invest between Rs 12 lakh (about $13,690) and Rs 15 lakh (about $17,110) to set up a Superk store. Of this, Rs 4 lakh (nearly $4,560) is spent on the store fit-out and infrastructure, the rest goes towards buying inventory. These stores, according to Menta, typically achieve a breakeven point after six months. On average, a retail store takes longer than that-12-15 months to reach breakeven.

Superk fills the shelves by procuring its inventory directly from brands as well as distributors. “The inventory is recommended by us through a mobile application. Store owners have an option to make certain changes within the limits that we have set for them,” says Thontepu. Revenue is shared and the model is similar to the one followed by nearly all retailers in India. Franchisees earn varying levels of margins on different kinds of products, depending on how easy or tough it is to sell those items. For instance, staples like dal and rice have lower margins, while confectionary items and products that need greater effort to sell enjoy higher margins of up to 20%.

In addition to this, there’s a private label business, especially loose items like pulses. In fact, private labelling is part of the company’s efforts to bring some standardization in India’s unorganized retail market. “A customer coming to our store should be able to blindly expect consistent quality on the product they’re buying,” says Menta. “We have organized our sourcing, processing, cleaning, packaging, testing. Everything that a brand would do to provide a great-quality product to their customer.”

Unlike distributors or other retailers who operate franchise models though, Superk claims that it does not dump its inventory on store owners. Menta says the franchise structure is designed in a way that Superk does not benefit from selling unnecessary stock to store owners. “If I lose, he will lose. If he loses, I lose. That is the way (the structure) is created. We, in fact, recommend owners to remove some products if they are not selling.” says Menta.

On the customer side of things, Superk’s value proposition comes down to offering the best prices. More than a year ago, for instance, it introduced a membership programme that offers customers cashback that is redeemable on their future purchases. “If they pay Rs 300 [approximately $3.5) for a six-month membership, they get 10% cashback on all purchases that they are making up to Rs 300 every month,” explains Thontepu. He says 35-40% of Superk’s more than 500,000 customers are enrolled in this programme.

All of this sounds good even promising in theory. But will it be enough to build a sustainable and scalable retail business?

A long, hard look

Let’s first look at what really works in SuperK’s favour.

One, the focus on selling staples under a private label brand. This has been done successfully before. One example is Nilgiri’s, one of India’s oldest supermarket chains.

Founded in 1905, Niligiri’s operated under a franchise model and sold dairy, baked goods, chocolates and other items produced under its own brand. The supermarket chain was sold by debt-ridden Future Group for Rs 67 crore ($7.65 million) in 2023, less than one-third the price the latter paid to acquire the company from private equity firm Actis in 2014. However, its history is worth learning from.

Shomik Mukherjee, a Delhi-based consumer goods advisor who was a partner at Actis while the firm was in control of Nilgiri’s, recalls the value proposition created by Nilgiri’s private label products. “In the case of private labels, it is essential for a company to have a reason why people will walk into that store. For Nilgiri’s, it was bakery and dairy products,” says Mukherjee. Owning a private label that brought in customers also ensured that franchisee owners had incentives to continue working with Nilgiri’s. “It is about giving the franchisees a safe portfolio of private label goods that are desired by customer instead of something that is shoved down the franchisees’ throat to derive margin,” he says.

You see, the overall grocery business operates on a very low margin. But private labelling, says Satish Meena, founder of Datum Intelligence, offers the highest margins – 35-40% – in the grocery business, after fresh produce, making it a lucrative business to get into.

Superk, which sells essential items through its private label, has the opportunity to earn better margins in grocery retail. More importantly, private labelling holds the potential to become SuperK’s identity and boost customer retention and loyalty.

Two, SuperK’s franchise model allows it to expand to more locations rapidly as compared to a regular modern trade chain with company-owned stores, says Mukherjee. This model makes SuperK’s business asset-light and brings down the cost of running a network of stores. “Under this model, the franchisor does not incur the upfront cost of opening a store or having to deal with the trouble of hiring and replacing store managers,” he adds. Since most store owners in a franchise model are landowners, there is a greater stability in operations as well, he explains. Moreover, Superk stores are quite small (800 sq ft), allowing easier availability of property.

The franchise model, however, is not entirely foolproof. One of the inherent problems is the difficulty in implementing standard operating procedures (SOPs) across all stores. And the problem only worsens as the company expands operations to different cities. While Superk stores boast a no-frills fit-out that can be easily set up anywhere, how these stores are maintained through the wear and tear over the years is yet to be seen.

A bigger fear is that the store owner may start running their own store without the Superk branding. “If Superk loses the franchisee owner, it also loses the location in which the store was operating,” says Mukherjee.

Moreover, most franchisee owners in the retail business typically tend to be experienced general store owners who might not be willing to adopt new technology. “Since they have run a store before, they think they know how and what to order for inventory and may not follow SuperK’s tech-enabled recommendations,” says Mukherjee.

There’s another problem. While the founders claim to have seen considerable success (35-40% sign-ups) in the rollout of SuperK’s membership programme for customers, Third Eyesight’s Dutta raises concerns about its future growth. “Indian consumers’ price sensitivity limits membership fee potential,” he says. According to him, the programme’s value in the tier-3 market lies more in customer acquisition and retention than direct revenue generation. “Long-term success requires a cashback programme to drive purchase frequency and basket size increases to offset the costs,” says Dutta.

Menta, however, has a different view. He says SuperK’s subscription is designed in a way that benefits customers only when they make full basket purchases. Moreover, the company has different pricing slabs for membership depending on the various basket sizes, which makes the model more viable. Considering the programme is a little more than a year old, it is still too early to judge whether it will find a lot of takers in small towns.

For now, the founders are in no hurry to expand their business across India. “There is no reason to go into five states. Then, you are spread thin and your economics will not work out. It’s a business of managing operations at a very low cost,” says Menta. The plan is to stick to one region and continue to go deeper into it. “A lot of our competitors who started five years ago spread to so many places that it became very difficult for them to manage,” he adds.

This is also the crux of how Thontepu and Menta are building SuperK. By implementing what they have learnt not only from their own experiments, but also from the failures and successes of other businesses. While there’s no guarantee that Superk will become a roaring success, it does appear to have set an example by starting small and growing patiently. And if the latest funding is any proof, investors are interested.

(With inputs from Neethi Lisa Rojan)

(Published in The Morning Context)

admin

September 16, 2024

Sesa Sen, NDTV Profit

16 September 2024

As India’s economy grows and digital technologies reshape consumer behavior, the future of kirana stores—the quintessential neighbourhood grocery shops—hangs precariously in the balance.

These soap-to-staple sellers, once impervious to change, now confront an existential threat from quick commerce players like Blinkit, Instamart, Zepto, and from modern retailers such as DMart and Star Bazaar, raising a pivotal question: Can kiranas survive the pressure of change, or will they die a slow death?

The All India Consumer Products Distributors Federation, that represents four lakh packaged goods distributors and stockists, has recently raised alarms, urging Union Minister for Commerce and Industry Piyush Goyal to investigate the unchecked proliferation of quick commerce platforms and its potential ramifications for small traders.

Their concerns are not unfounded. Data suggests that the share of modern retail, including online commerce, which is currently below 10%, is set to cross 30% over the next 3-5 years. Much of this growth will come at the cost of traditional retail.

“Unless the government takes on an activist role to support the smallest of business owners, the shift toward large corporate formats is inevitable,” according to Devangshu Dutta, head of retail consultancy Third Eyesight.

Casualties Of The Boom

Madan Sachdev, a second-generation grocer operating Vandana Stores in eastern Delhi, has thrived in the recent years, adapting to the digital age by taking orders via WhatsApp and employing extra hands for home delivery.

Despite having weathered the storm of competition from giants like Amazon and BigBazaar, he now finds himself disheartened, as his monthly sales have halved to about Rs 30,000, all thanks to quick commerce.

Sachdev is worried about meeting expenses such as rent, his children’s education, and other household bills. He finds himself at a crossroads, uncertain about how to modernise his store or adopt new-age strategies in order to attract customers in an increasingly competitive market.

India’s $600 billion grocery market, a cornerstone for quick commerce, is largely dominated by more than 13 million local mom-and-pop stores.

Retailers like Sachdev are also seeing a steep decline in their profit margins from FMCG companies, which now hover around 10-12%, down from the 18-20% margins seen before the Covid-19 pandemic. The consumer goods companies are instead offering higher margins to quick commerce platforms so that they can afford the price tags.

Quick deliveries account for $5 billion, or 45%, of the country’s $11 billion online grocery market, according to Goldman Sachs. It is projected to capture 70% of the online grocery market, forecasted to grow to $60 billion by 2030, as consumers increasingly prioritise convenience and speed.

Many of the mom-and-pop shops are family-run and have been in business for generations. Yet they lack the resources to modernise and compete effectively with larger chains. Modern retail businesses, including quick commerce, begin with significantly more capital, thanks to funding from corporate investors, venture capital, private equity, and public markets.

“They can scale quickly and capture market share due to a superior product-service mix, larger infrastructure, and more robust business processes,” said Dutta.

Moreover, their ability to engage in price competition poses a challenge for small retailers and distributors, making it difficult for them to compete.

“This is something that has happened worldwide, in the largest markets, and I don’t think India will be an exception,” Dutta said, adding that it would be incomplete to single out a specific format of corporate business such as quick commerce as the sole villain in this situation.

“India is a tough, friction-laden environment at any given point in time, including government processes which don’t make it any easier,” he said.

Peer Pressure

Data from research firm Kantar shows that general trade, which comprises kirana and paan-beedi shops, have grown 4.2% on a 12-month basis in June, while quick commerce grew 29% during the same period.

Shoppers are becoming more omnichannel, rather than gravitating towards one particular channel, said Manoj Menon, director- commercial, Kantar Worldpanel, South Asia. “While the growth [for quick commerce and e-commerce] might appear to have declined compared to a year ago, a point to note is that the base for these channels has significantly grown. Therefore, achieving this level of growth is still commendable.”

Consumer goods companies such as Hindustan Unilever Ltd., Dabur India Ltd., Tata Consumer Products Ltd., etc., have acknowledged the salience of quick commerce to their packaged food, personal and homecare products. The platform currently comprises roughly 40% of their digital sales.

“We are working all the major players in the quick commerce space and devising product mix and portfolio. This is a very high growth channel for us,” according to Mohit Malhotra, chief executive officer, Dabur India.

Elara Capital analysts have pointed out that the share of quick commerce is expected to rise to60% in the near future with e-commerce and modern trade turning costlier for FMCG brands than quick commerce. “The larger brands tend to make better margins on quick-commerce platforms versus e-commerce due to lower discounts on the former,” it said in a report.

However, it is too premature to draw a parallel between kirana and quick commerce in terms of competition, given the significant size difference.

The average spend per consumer on FMCG in kirana stores stands at Rs. 21,285 annually while the same is Rs. 4,886 for quick commerce, according to Menon.

Rural Vs Urban Divide

Quick commerce is still an urban phenomenon. In contrast, in rural settings, where internet penetration is still catching up and access to large retail chains is limited, kirana stores continue to thrive.

According to Naveen Malpani, partner, Grant Thornton Bharat, while the growth of quick commerce is undeniable, this channel is not poised to replace traditional retail, which still has a wider reach in the country. “It will complement older models, filling a niche for immediate, smaller purchases. Also, a 10-20-minute delivery may not have a strong market pull in rural markets where distance and time are not much of a concern.”

Yet many others believe, even in these areas, the challenge is palpable.

The small businesses are beginning to feel the sting of same slow decline that once befell the ubiquitous telephone booths in the era of mobile phone, according to Sameer Gandotra, chief executive officer of Frendy, a start-up that is building ‘mini DMart’ in small towns where giants like Reliance and Tatas have yet to establish their presence.

As rural customers slowly start to embrace digital shopping and seek more variety, kirana stores must adapt or risk becoming obsolete, he said.

Besides, the popularity of quick commerce is set to challenge the dominance of incumbent e-commerce platforms, especially in categories such as beauty and personal care, packaged foods and apparel.

“Quick commerce is primarily operational in metros and tier 1 markets, which is impacting the sales of traditional companies in these areas. However, if quick-commerce players were to extend their operations to tier 2 and tier 3, it would even challenge companies such as DMart and Nykaa, and would pare sales and profitability,” noted analysts at Elara Securities.

Frendy’s Gandotra believes the journey for kirana stores is not a lost cause, but it requires strategic interventions. Many kirana store owners struggle to integrate point-of-sale systems, inventory management software, or even digital payment solutions. These stores need to embrace technology.

Another aspect is the need for policy support. Regulations to ensure fair competition can prevent monopolisation by large retailers. Additionally, subsidies, tax benefits, and grants for infrastructure improvements can help small businesses adapt to changing market dynamics. With renewed support, kirana stores can continue to be the backbone of Indian retail.

Nonetheless, there will be some who’ll be left behind during this shift. Analysts at Elara Capital warn that the swift rise of quick-commerce platforms, combined with aggressive discounting, could wipe off 25-30% of traditional grocery stores.

(Published on NDTV Profit)