admin

March 1, 2026

Apoorva Mittal, Economic Times

1 March 2026

Resshmi Nair, 31, had grown used to the dotted red bumps on her arms. Her dermatologist diagnosed it as keratosis pilaris aka strawberry skin. It is a harmless skin condition that often affects legs and arms but Nair, a Mumbai-based marketing consultant, wanted it gone. She slathered lotions and salves but to no avail. Then she chanced upon an Instagram reel which showed an oil-based in-shower spray that promised to take care of her problem. “It was very tempting as it resonated with a personal concern,” she says. She is now on her third bottle. The bumps haven’t disappeared entirely, but they have become smaller, she says.

Like Nair, there are many who seek solutions tailormade for their beauty bugbears. Consumers who once searched for moisturisers and shampoos now look for niche products for hair and skin. They want to repair skin barrier, tame baby hairs and minimise facial pores.

A new generation of Indian beauty and personal care (BPC) brands are both listening to them and leading them. Focused products, they realise, could help them stand out in a crowded sector dominated by FMCG giants. While problems like acne, frizzy hair and rough skin have always been around, experts say the commercial importance of solving them narrowly and packaging that specificity as a brand strategy have become more intense of late.

India’s direct-to-consumer (D2C) beauty and personal care market—which is heavily invested in micro-problem targeting—is estimated to be $4.5 billion in FY2025, according to consulting firm Redseer. The new-age brands could account for 25-35% of total BPC spends by 2030. “Three major factors have contributed to this: one, the rise of digital medium for both commerce and marketing, which created a segue for new brands to launch and scale; two, younger consumers (Gen Z and young millennials) have become ingredient literate and look for results over broad promises; and three, competitive intensity in the market is pressing brands to position as per the right niches,” says Kushal Bhatnagar, associate partner, Redseer.

The shift is measurable on beauty retailer Nykaa’s platform. “Consumer vocabulary is far more evolved,” says a company spokesperson. Searches driven by specic concerns or ingredients are growing faster than broad category items. While foundational concerns like acne and brightening remain relevant, the platform is seeing strong growth in queries around pigmentation, barrier repair, pore care and specic hair issues. “This fragmentation is actually a sign of a more informed and aware consumer base,” the spokesperson adds.

ZOOMING IN

For young D2C brands, this behavioural shift has opened a narrow but potent entry point. Instead of launching another shampoo or moisturiser, they launch a product targeting a single problem and market it in an easily demonstrable short-video format. In the current beauty landscape, the market has shifted from general solutions to hyper-targeted efficacy.

Moxie Beauty, founded by Nikita Khanna in 2023, illustrates the playbook. Khanna, who previously worked at McKinsey, began with a focus on wavy and frizzy hair, a segment she herself belongs to. But it was one particular styling product, the flyaway hair stick, that went viral, propelling the brand into visibility. She says, “The wavy hair routine required us to educate people, which took time. But one can understand the flyaway wand in five seconds.” And it targeted what she calls a “widely held pain point”. That helped Moxie cut through crowded feeds and end up on consumer shelves. “Being synonymous with a category helps,” she says. “When people want a wax stick or flyaway stick, they search for our brand.”

That shift—from paying for visibility to being searched for directly—is critical in a market where customer acquisition costs (CAC) can be punishingly high. For many D2C brands, launching a sharply defined product is a way to reduce discovery friction and lower early-stage CAC. But a brand cannot be built or scaled on gimmicks, says Khanna. “If you solve only for what will look good in a video and will go viral, you won’t be able to scale. And if it’s a gimmick, people won’t repeat the purchase,” she adds.

Divanshee Jindal, cofounder of the brand The Solved Skin, says companies have to get the “product-communication fit” right. Her brand’s liquid pimple patch, which is designed to mask acne under makeup, is quickly emerging as its hero product. “People get excited when a product feels relatable and authentic,” says Jindal. “A new, convenient format that solves a real pain point makes consumers willing to try a new brand. But if it’s a standard product, say, a salicylic acid face wash, they will often default to a brand they already trust.”

SMALL IS BEAUTIFUL

The idea is to start small but evolve. Moxie, for instance, has moved beyond textured hair into solving broader “Indian hair problems” like damage repair and anti-dandruff that has brought in male consumers as well. “Curly or wavy hair was a huge, underserved problem,” says Khanna. “But the thought was always to solve other problems as well.” Moxie, which recently raised $15 million in a funding round led by Bessemer Venture Partners, says it has crossed Rs. 100 crore in annual recurring revenue on its two-year mark, and is seeing roughly 50% consumers coming back in six months across platforms. However, it says profitability is harder to crack because of intense competition from new brands and changing channel mix.

Mani Singhal, MD of the consulting firm Alvarez & Marsal, points out that most successful D2C brands started out with a sharply defined hero product. “Earlier it was natural vs chemical or price disruption; today it’s much more about efficacy proof, ingredient transparency, visible results and credible

storytelling,” she says.

From the manufacturer’s side, Nishit Dedhia of Kain Cosmeceuticals, a cosmetics manufacturing company, says, “It is easier today for brands to target special concerns. That specificity helps them build a differentiated product earlier on.” Most brands, he explains, x a major problem such as acne, dryness, pigmentation and then layer in a niche twist. Strawberry skin, once not a mainstream concern, is now a category. “People didn’t know the term. Once you give it a name, they identify with it,” he adds.

Dedhia describes the portfolio strategy as 8-2 or 9-1 where eight or nine products are general, incremental variations of core needs, while one or two are “category-building products” that require significant consumer education or product communication but create their own search demand. “That is the only way you get out of the vicious cycle of paying for visibility,” he says. “When people search for your brand directly, CAC comes down.”

Devangshu Dutta, founder of management consulting firm Third Eyesight, says micro-problem framing is “co-created” by consumers and companies. “The fragmentation is real, but the language used to describe it is heavily brand-driven,” he says. Terms like “strawberry skin” or “glass skin” correlate with influencer campaigns but label pre-existing dissatisfactions that mass products did not address sharply.

However, sometimes, in the race to differentiation, brands go for outlandish ideas. Dedhia says brands increasingly approach manufacturers with amusing asks in the quest to stand out. For instance, beard fillers packaged like mascara or plumpers for face and neck.

PRODUCE & PERISH

The problem is that the mortality rate of skincare brands is very high in India. Dedhia estimates that around 60% companies shut down in three years. Many brands burn through capital chasing ads and trends without building repeat customers or a community.

“For a brand to cross over from being a curiosity-driven purchase to being part of a regimen needs a minimum 25-30% of customers showing up as repeats after three months, while truly successful brands reach higher repeat numbers,” says Dutta.

Subscriptions are an even stronger test. “Generic formulations, me-too products and influencer spends can get you first users, but repeats will happen only from the user getting demonstrated value,” says Dutta.

But growth does not equal stability. CAC typically starts low for niche products, rises during scaling-up and stabilises only if organic demand takes over, says Bhatnagar of Redseer. Quick commerce accelerates discovery but compresses margins due to the high commission rates on these platforms, promotional expectations and lower average order values.

Singhal, who says a consolidation phase is underway, adds: “Niche entry can work extremely well if the problem is frequent enough and the solution is demonstrably effective.” Durable brands deliver consistent performance, build adjacencies beyond the first niche and maintain disciplined unit economics.

“If repeat rates don’t stabilise, economics becomes very challenging, very quickly.”

PERSONALISATION AHEAD

For Aparna Saxena, founder of Delhi-based beauty brand Antinorm, the next decade will be defined by even greater personalisation. Her brand has multifunctional products that are timesaving. Saxena says she surveyed about 250 women above 25 years of age and found that five-step routines typically do

not last after two months. Antinorm’s architecture rests on multifunctionality, like a leave-in cream that doubles as heat protectant and promises a “presentable” hair look without a blow-dry. Its most popular product is a spray that cleanses and moisturises, which they dub as “instant shower” or “facial in a flash”.

She says the brand, which launched in July last year, will close next fiscal with about Rs. 25 crore in revenue. Repeat rates are currently under 25% “because the denominator is expanding rapidly”, she adds. “Between 2020 and 2025, customers moved away from incumbents and got used to having options and trying newer brands,” she says. “Now they have routines in place. The next five years will be defined by more and more personalisation and micro-problem solving.” The beauty is about to go really skin deep.

(Published in Economic Times)

admin

January 17, 2026

Prachi Srivastava, Hindustan Times

January 16, 2026

We keep telling ourselves that 2026 will be the year of budgeting. So, we’ve cut back on weekend brunch, paused Zara hauls, are collecting every coupon code we can, and are furiously spinning the wheel of luck on every site’s pop-up box. One thing that’s making it a little easier: Mini-sized luxury.

We’ve been here before. India’s sachet and sample-size products have been so successful, they’re studied in business school. We’ve lived through the beauty-box-subscription revolution (we still have the empty pouches somewhere). We’ve sprung for discovery kits on Nykaa and Tira (those 7ml doses will never make a difference, but still…). But luxury in small sizes? In this economy, when we’re budgeting and still craving pick-me-ups, it’s an idea whose time has come.

Everyone’s doing fun-size now: There’s one-day-use SPF as a handbag charm, tiny tubes of mascara, three-spritz niche perfumes. There are advent calendars – 30-day boxed sets for December, promising big savings. But also tasting jars of chilli-oil, one-hour-burn micro candles, single-wash detergent pods, even a single-cup insulated flask for your morning brew.

They all have starring roles in What’s in My Bag videos and GRWM reels. “Mini-product content sees higher engagement because it’s visually satisfying,” says beauty influencer Preiti Bhamra (@PreitiBhamra). “The contrast of a big hand holding a tiny product instantly catches attention.” Minis are deliberately packaged in the same style as a full-sized product, for better brand recognition. They photograph better too. Plus, think of how many more treats can fit on a shelf or a handbag, if they’re a smaller size.

Thinking small

Minis used to be linked to the Lipstick Index. The uptick in small-luxury purchases has, for decades been a recession indicator – ostensibly because when finances feel uncertain, consumers tend to avoid big purchases and turn to smaller indulgences for an emotional boost. That’s no longer true. Small is now a category unto itself.

On top beauty sites, you can filter products by mini size (not Travel Size as they were once called). Korean and Japanese brands deliberately market “ampoule” sizes for single-dose products. Platforms such as Smytten sell only sample sizes. Gemz, a mass-market brand that hasn’t launched in India yet, is aimed directly at GenZ (as the name suggests). It sells bath products in single-use packs. Hang them on the shower rod, open one, add water, lather, rinse, repeat.

Retail and luxury analyst Devangshu Dutta notes that minis are just low-risk experiments in luxury. It “encourages consumers to try premium categories they might otherwise postpone”. Think about it: A full-size Maison Francis Kurkdjian perfume may cost more than a month of Uber rides, but its mini discovery set under ₹5,000 feels like reasonable adulting. A Jo Malone candle is basically an EMI for your nose — but the 35g version? Suddenly doable.

“Across beauty, fragrance, personal care and gourmet foods, minis help brands acquire new customers faster,” Dutta adds. “They rotate better on shelves, get tried more often, and build quicker loyalty.”

I feel so used

We don’t buy minis only because they’re practical. We buy them because they hit our emotional pressure points. Clinical psychologist Dr Prerna Kohli says that when life feels overwhelming, “a small treat feels manageable.” A tiny lipstick becomes a quick hit of “at least this feels good,” even when nothing else is going right.

“There’s also a cultural twist,” Kohli adds. Indians grow up on the idea of delayed pleasure — work first, reward later. Tiny luxuries flip that script. They’re permission to feel good now. “Choosing something beautiful reminds you that you still matter, without waiting for a milestone.” Women, particularly working women and caregivers, hesitate to invest in themselves. But a tiny serum? That feels “allowed.” Less money, less guilt, and far fewer explanations.

Tiny treats thrive in the kitchen, as young professionals find them easier to experiment with, than brimming jars of an unfamiliar flavour. Food creator Natasha Gandhi (@NatashaaGandhi) says that tasting sets, mini variety packs and weekend-use portions have been doing well in the gourmet and artisanal category as diners seek restaurant-style flavours at home, but don’t want to cook the same thing over and over. In smaller kitchens and cluttered pantries, they also feel practical. They sit “at the sweet spot of ambition, convenience and low commitment.”

Too tiny to thrill

Not all minis deliver value. A 7ml sunscreen sachet isn’t enough for a user to determine if it truly suits their skin. A one-meal condiment delivers flavour, not familiarity. Single-use homecare creates packaging waste, adds to clutter, and cost-per-use can quietly climb. Luxury shampoo and conditioner minis are largely “overrated,” says Bhamra — often more indulgent illusion than practical trial.

The real red flag appears when the buying shifts from enjoyment to emotional avoidance. “It becomes unhealthy when shopping is used to numb uncomfortable emotions,” cautions Kohli. The usual symptoms apply: Shopping in secret, adding to cart the same time every day, week or month – indicating shopping during cyclical low periods, overjustification for a purchase. “Enjoyment is fine. Distraction always circles back.”

Perhaps in an age of overwhelm, the new luxury isn’t about owning more, but about feeling steadier. “Sometimes people simply enjoy beautiful things in small forms,” says Kohli. “We’re allowed to like something just because it makes us smile.”

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

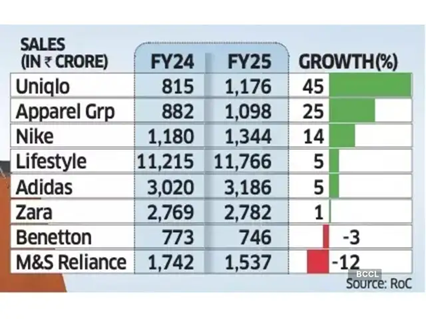

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

December 7, 2025

Gargi Sarkar, Inc42

7 December 2025

The past year has been nothing short of monumental for LensKart — from reporting another operationally profitable quarter in Q2 FY26 to making the public markets leap in November, and crossing a market capitalisation of INR 70,000 Cr despite a muted stock market debut.

A clear shift this year has been Lenskart’s effort to move beyond the image of a ‘basic D2C eyewear’ brand selling prescription glasses and sunglasses. The company is now working to reposition itself as a new-age tech brand.

Further, Lenskart is rethinking where and how its products are manufactured. Currently, around 20–25% of its frames are reportedly manufactured in India. The company is ramping up its domestic production. As a new manufacturing facility in Telangana is a work in progress, Lenskart intends to gradually shift most of its manufacturing operations from China to India.

In many ways, 2025 has been about scaling up for Lenskart, and as it embarks on a fresh journey as a publicly listed company, let’s take stock of the company in 2025 and where it might be headed in 2026.

Lenskart’s Smart Eyewear Bet

Lenskart began its smart eyewear journey last year with the launch of Phonic, its audio glasses. It later deepened its push into the segment by announcing a strategic investment in Ajna Lens, a Mumbai-based deeptech company that develops AI-powered XR glasses. Back then, Peyush Bansal described the move as the “next chapter” in Lenskart’s smart glasses journey.

Cut to December 2025, the company is all set to launch its AI camera smartglasses, B by Lenskart, by the end of this month.

What makes B by Lenskart noteworthy is that it isn’t being marketed as just another pair of smart glasses. The new eyewear features an integrated Sony camera that enables hands-free photo and video capture. The glasses come with a built-in AI assistant powered by Gemini 2.5 Live. They are designed to offer natural, conversational interactions and pack in a range of advanced features — from hands-free UPI payments and live translation to wellness insights and more.

What makes the move even more significant is Lenskart’s decision to open B by Lenskart to India’s developer ecosystem. By making its AI and camera technology accessible to consumer apps and independent developers, the company is enabling integrations across categories such as food delivery, entertainment, and fitness.

“By opening its AI smartglasses to third-party developers, Lenskart is moving from a one-time product-sale model to a platform ecosystem model. In the long run, this could unlock recurring revenue streams and higher margins,” said a product developer.

Besides, the company is aligning itself with a younger customer cohort, aided by affordability, style, and technology.

“That’s what seems to define their current strategy. Over time, they’ve also brought in elements of innovation like virtual try-ons, and any product, feature, or service that brings novelty and appeals to younger customers has become part of their brand approach,” said Devangshu Dutta, the founder of Third Eyesight.

Next, the timing couldn’t be better for Lenskart to place its bet on smart glasses. An IDC report reveals that despite a slowdown in smartwatch and earwear segments in the second half of 2025, smart glass shipments shot off more than 1,000% over the last year.

However, it’s not going to be smooth sailing from here.

At its core, Lenskart is still a consumer-facing company, and it needs new products to keep its revenue growing. But the competition is already heating up. Jio unveiled its own AI-powered smart glasses, Jio Frames, at Reliance Industries’ 48th annual general meeting. And of course, Meta continues to lead the global smart glasses market.

At this point, smart eyewear is a niche category, which comes with a hefty price tag.

“Unless cost drops dramatically, mass adoption is still a distant dream. As of now, the product will only attract early adopters and tech enthusiasts, rather than the mainstream consumer,” Dutta adds.

Lenskart’s Make In India Push

Lenskart is not only widening its product range but also ramping up its manufacturing. The company currently operates centralised manufacturing facilities in India (Bhiwadi in Rajasthan and Gurugram in Haryana), Singapore, and the UAE. It also has manufacturing operations in China.

Back home, Lenskart has also signed a non-binding MoU with the Government of Telangana for setting up a greenfield manufacturing facility for optical glasses. The proposed investment stands at INR 1,500 Cr and will be supported by certain incentives and assistance from the state government.

The new production facility is expected to strengthen Lenskart’s domestic manufacturing capabilities while reducing its exposure to foreign exchange fluctuations and import-related volatility.

However, the expansion comes with its own set of challenges. While the new manufacturing plant in Telangana is expected to strengthen Lenskart’s vertical integration, it will come with a hefty cost burden.

Profitability Still A Troubling Question

The cost structure is becoming increasingly important for Lenskart. Despite its headline-grabbing profitability, the company is still operating on fairly thin margins.

Lenskart reported a net profit of INR 297 Cr in FY25, a notable turnaround from a loss of INR 10 Cr in FY24. However, market analysts caution that the business’ core operations were unprofitable. It was largely “other income” or investment income that drove the FY25 bottom line.

“Though Lenskart has increased its revenue from INR 3,789 Cr in FY23 to INR 6,651 Cr in FY25, the company’s profitability has largely improved due to a rise in other income. While it reported a PAT of INR 297 Cr in FY25, a closer look shows that the profit was driven significantly by an increase in other income, which jumped to INR 356 Cr in FY25,” SimranJeet Singh Bhatia, senior research analyst for equity at Almondz Group.

The point of concern here is that Lenskart turned operationally profitable only after its market debut. Bhatia believes that at least three to four quarters of consecutive profitability will be needed to prove the company’s underlying strength.

However, making matters worse are the company’s climbing expenses, which stood at INR 1,980.3 Cr in Q2 FY26, up 18.5% YoY.

What Lies Ahead?

The year was equally sour for the eyewear major. While its IPO generated significant buzz and saw strong subscription levels, its market debut turned out to be a muted affair.

At the upper end of its INR 382 to INR 402 IPO price band, the public issue implied a price-to-earnings (P/E) multiple of roughly 235–238 times its FY25 profits, placing it among the most expensive consumer tech listings in India.

On its first day of trading, Lenskart Solutions Ltd. was listed on the NSE at INR 395 per share, a discount of 1.74% to the issue price of INR 402. The stock, however, fell close to 9% shortly thereafter. On the BSE, it debuted at INR 390, marking a discount of nearly 3%.

After the IPO, Bhatia adds, the biggest concern surrounding Lenskart is the store-level unit economics, particularly because a significant share of the IPO proceeds is being directed toward expanding its company-owned, company-operated store network.

Entering the new year as a public company, Lenskart will have to prove that its scale-up plans are justified and that it has greater control over its balance sheet. 2026 will be a critical juncture for the company, as the next three to four quarters will be closely watched for signs of sustainable growth, improved margins, and stronger operational discipline.

[Edited by Shishir Parasher]

(Published in Inc42)

admin

December 3, 2025

Pooja Yadav, Exchange4Media

3 December 2025

Over the last few months, India’s e‑commerce and quick‑commerce ecosystem has undergone a wave of structural regulatory and tax reforms. Be it the Goods and Services Tax Council (GST Council) formally bringing “local delivery services” under the tax net with an 18% levy, or the newly implemented labour and social-security reforms expanding obligations for gig workers on aggregator platforms like Swiggy and Zomato, the cost and compliance landscape for delivery and fulfilment is shifting significantly.

The latest GST clarification, delivery fees, packaging charges, and logistics surcharges are now creating a ripple effect across pricing, platform margins, and seller compliance requirements.

The past few months have already shown concrete signals that platforms are revising their incentives, delivery promises, and fee structures. Following the GST clarification, major food‑delivery players have raised their platform fees, for instance, Zomato reportedly increased its per‑order fee from ₹10 to ₹12 (pre‑GST), while Swiggy also raised fees in select markets. Some quick‑commerce arms are also reworking free‑delivery thresholds or fee waiver conditions. Swiggy Instamart also recently updated its free‑delivery threshold to orders above ₹299, with handling and surge fees applying below that level, per reports.

Meanwhile, some platforms seem to be signalling a de‑emphasis on “ultra‑fast for every order” as universally viable; free or fast delivery now appears increasingly tied to higher order values or subscription/membership perks.

It looks like these pressures are forcing platforms to reconsider long-standing quick-commerce levers such as ultra-fast delivery, first-order free offers, zero delivery fees, and flash discounts — which have historically driven customer acquisition and retention.

While Zomato did not comment directly, it referred to the Code on Social Security, 2020 (CoSS), noting that the platform is prepared for gig-worker obligations and does not expect the rules to negatively impact long-term business sustainability.

According to Kapil Sharma of Amazon Ads, “The e‑commerce landscape will continue to evolve, but some fundamentals remain constant such as delivering value to consumers and providing advertisers with meaningful ways to engage. Our full-funnel ad solutions allow brands to focus on objectives such as new product launches, brand building, or promoting larger pack sizes, ensuring campaigns remain relevant and effective even as the ecosystem adapts to changing costs and regulations.”

e4m reached out to Swiggy, Meesho, Zepto and BigBasket for comments, but did not receive responses until the time of publishing.

Several experts told e4m that the economic model of quick commerce, built on heavily subsidised delivery and small-ticket frequent orders, is under pressure. Platforms will need to find sustainable levers to retain customers without eroding margins. The industry has started to see a strategic recalibration where speed is increasingly becoming a hygiene factor rather than a differentiator, free delivery is becoming conditional, and platforms are nudging consumers toward larger baskets, subscription models, curated bundles, and scheduled deliveries. Brands, in turn, are also shifting focus from mass discounting to premiumisation, value-led messaging, and precise cohort-based targeting.

Will Free Delivery Become Rare?

With the new social‑security obligations for gig workers under India’s labour reforms, and the added cost burden of delivery services now subject to GST, the economic logic underlying “free delivery” as a marketing lever is coming under stress. Chetan Asher, Founder and CEO of Tonic Worldwide, echoes this view, noting that quick-commerce platforms previously operated on thin contribution margins and heavily subsidised small-ticket, frequent orders. With rising delivery costs and mandatory social-security contributions, universal free delivery is becoming increasingly unsustainable.

Industry analysts point out that the new social-security mandates and GST on delivery fees have lifted per-order costs noticeably. Most quick-commerce platforms already operate at low single-digit contribution levels, making blanket “free delivery” hard to justify. It may continue, but only as a conditional incentive tied to higher basket values, subscription memberships, or flexible delivery slots, rather than as a universal subsidy.

Shradha Agarwal, Co- Founder & Global CEO, Grapes Worldwide, added from an advertising standpoint, “It’s already happened, brands like Zomato, Swiggy, Amazon and Flipkart, who know we are going to buy from them, have shifted from ‘buy now’ tactics to ‘stay with me’ strategies. Those days are gone when platforms were giving blanket discounts, now brands are the ones tightening their offers.” Citing an example she mentioned how offline pricing is ₹235, but online it is sold at ₹185, with online adding to top-line rather than bottom-line.

On promo hooks like ‘₹0 delivery’, ‘first-order free’ or ’10-minute delivery’, Agarwal said, “As labour codes, compliance costs, and social-security contributions kick in, platforms will have less room to burn cash on promos that don’t create sustainable value. Consumers care more about convenience than freebies.”

On ad spend shifts, she noted, “Offer-driven campaigns will weaken, while value-driven storytelling will rise. ATL and influencer campaigns will strengthen, and performance marketing will become more strategic. Retail media will become non-negotiable.”

From a brand perspective, Asher pointed out that quick-commerce spends are increasingly evaluated against contribution margin rather than sheer GMV growth. Discounts and zero-fee offers are losing bite as customer acquisition costs rise. First-party data, replenishment journeys, and sharper cohort-based offers are gaining importance, ensuring that incentives remain ROI-focussed rather than mass-oriented. Similarly, speed claims such as “0 delivery” or “10-minute delivery” are becoming less differentiating in top cities, where most players already deliver within 15–20 minutes. Consumers now respond better to reliable ETAs, fair fee structures, and transparent pricing than aggressive speed promises.

Adding her viewpoint, Pooja Dhamdhere, Commerce Lead at Starcom India, said, “Incentives like free delivery or first-order offers are likely to evolve rather than disappear, and platforms will explore strategies such as tiered benefits, curated bundles, or differentiated pricing for specific cohorts.”

According to serial entrepreneur Alok Chawla and Founder at Kiko Live, added that while platforms may continue absorbing delivery costs in the short term, the long-term economics will require charging for ultra-fast or low-value orders. “Once platforms pass the actual delivery costs to consumers, we expect order frequency and small-cart behaviour to change, with many users shifting to larger baskets or neighbourhood retailers offering free delivery,” he noted.

Alternative Consumer-Incentive Models

Devangshu Dutta, founder and chief executive of Third Eyesight, who is an expert in the consumer and modern retail sector, stated, “I think platforms will pass a significant portion of the new 18% GST burden on delivery to end-consumers, either through higher delivery charges or repackaged platform fees. Some of this cost may also be clawed back from restaurant partners and quick-commerce brands via revised commissions, slotting fees or mandatory participation in marketing programmes, especially in categories where the platform has stronger bargaining power. Overall, I expect higher minimum-order thresholds and a tighter margin environment for restaurants and small D2C brands that rely heavily on third-party platforms.”

Analysts highlight strategies such as minimum-order thresholds, where free or lower-fee delivery applies only above a certain cart value, nudging consumers to order larger baskets rather than frequent small-ticket items. Subscription and membership-based models are also gaining prominence, offering benefits like waived or discounted delivery, priority fulfilment, and access to exclusive promotions in exchange for a fixed fee.

Scheduled or batch delivery windows are being used to optimise logistics, reduce cost pressure on ultra-fast last-mile fulfilment, and improve operational efficiency. Meanwhile, curated bundles and value packs, including weekly or monthly combos, allow consumers to plan purchases while enhancing per-unit economics for platforms. These levers also enable brands to maintain margin integrity without over-reliance on short-term discounting.

From a marketing perspective, this shift is prompting agencies and creative-first firms to move toward value-led messaging, premiumisation, and cohort-based targeting. Dhamdhere explained, “Platforms are optimising assortments by surfacing premium SKUs, nudging higher average order values, and using search optimisation to strengthen profitability. Brands are now focusing on aspirational consumers with curated bundles, subscriptions, and value-led propositions, rather than mass discounting. Performance campaigns will continue, but clarity of value and sustainable margin-led offers are becoming key for acquisition and retention.”

2026: Will regulatory pressure force a recalibration?

As 2026 approaches, the combined impact of GST on delivery services and mandatory social-security contributions for gig workers is forcing a fundamental rethink of quick-commerce economics. With blanket discounts, zero delivery fees and ultra-fast delivery no longer viable as mass levers, platforms are shifting toward basket-building, subscriptions, curated bundles and conditional incentives. The growth thesis is evolving from “habit formation at any cost” to protecting contribution margins through reliable ETAs, transparent pricing and premium assortments rather than aggressive subsidies.

Brands are recalibrating alongside this shift. Premiumisation, value-led propositions and sharper cohort-based targeting are taking precedence over broad discounting, and campaigns are increasingly evaluated on ROI, repeat behaviour and lifetime value rather than raw GMV. Tiered memberships, scheduled deliveries and subscription-led conveniences are emerging as key retention tools, while short-form video, influencer ecosystems and retail media help articulate value in a tighter cost environment.

Chawla said platforms will have to move beyond “₹0 delivery”, “first order free” and “10-minute delivery” as core propositions because the delivery cost burn far exceeds margins on small-ticket orders. Many consumers currently place multiple micro-orders a day simply because delivery is free, but once fees come into play, behaviour will likely shift toward clubbing orders or reverting to neighbourhood retailers, who themselves are rapidly digitising through partners like Kiko Live.

In the next phase, he adds, free instant delivery will only be sustainable for larger baskets, whereas scheduled delivery may become the default for free delivery, with paid instant delivery as an optional upgrade. Subscriptions may drive loyalty, but only up to a point, since the heaviest users would consume more deliveries than the subscription fee can realistically subsidise, making it difficult for platforms to make the model profitable.

This points to a clear playbook for 2026. “Free delivery” and mass discounting are expected to fade, giving way to conditional, tier-based formats that reward higher basket values, subscriptions or specific cohorts. Brand platform partnerships will also move toward profitability rather than promotional burn, with campaigns designed to protect margins instead of fuelling discount-led spikes.

Taken together, the signs suggest that 2026 will not mark the end of convenience, but the end of convenience that is subsidised blindly. The real test now is who absorbs this new cost of convenience, platforms, brands, or consumers. And as that battle plays out, another tension is already emerging: whether small and regional advertisers can survive the rising cost of visibility in India’s digital economy.

(published in Exchange4Media)