admin

July 13, 2026

Sowmya Ramasubramanian, Vaeshnavi Kasthuril (MINT)

Bengaluru, 13 July 2026

India’s vertical quick-commerce startups across categories like baby care, medicines and fashion, backed by venture capital heavyweights, are beginning to redefine what “quick” means.

For some, the race is no longer about cutting delivery times by a few more minutes. Instead, founders are increasingly talking about better assortment, sharper curation, stronger supply chains and healthier unit economics as the factors that will decide whether the model survives.

Baby care platform Ozi, backed by Blume Ventures and RTP Global, has settled on a roughly 60-minute delivery promise. Founder Amit Sah told Mint the company would rather optimise for “quality selection” than chase ultra-fast deliveries, arguing that customers today are looking for reliable availability and curated choices rather than insisting on receiving products in 10 minutes.

Lightspeed-backed fashion startup Slikk is pursuing a similar path. Founder Akshay Gulati said the company’s focus since inception has been building a wide catalogue rather than aggressively acquiring users.

The shift comes as the sector enters a more pragmatic phase. Quick fashion startup Blip shut down within a year of launch last June, while rival Klydo has recently pivoted its business model, raising questions about the viability of firms in every category.

The crop of vertical quick commerce startups—focused on rapid delivery within a single, specific product category—has largely emerged over the past two years, inspired by the explosive growth of grocery-focused pioneers such as Blinkit, Swiggy Instamart and IPO-bound Zepto, which have accustomed consumers to receiving groceries and everyday essentials within minutes.

Other prominent startups include Plazza for quick delivery of medicines, Instafix for mobile repairs within minutes, and Dazzl for at-home salon services.

Kalaari Capital noted in its 2025 report that quick commerce had already captured about two-thirds of online grocery orders and around 10% of India’s overall e-retail spending in 2024, transforming consumer behaviour and building the infrastructure for specialised vertical players to emerge.

“Speed was never a real moat but became a hygiene factor once every significant player could promise 10-30 minute delivery,” said Devangshu Dutta, founder and chief executive of consultancy Third Eyesight. “Assortment depth, availability, trust, and sustained price-value have been, and will remain, the true differentiation levers. For categories such as medicines and baby products, credibility and compliance outweigh saved minutes, apart from urgent purchases.”

“Unit economics can become healthier only where there’s a clear reason for frequent and repeated purchases. Groceries and medicines are repeat, low consideration categories, while fashion is high consideration, driven by fit, styling and browsing. The best quick commerce categories have low or no returns and high order frequency, whereas rapid fashion delivery faces high return rates due to product mismatch against customer expectations (sizing, fit, fabric and colour),” Dutta said.

Different categories, different playbooks

While fashion startups are investing heavily in discovery and inventory refreshes, Ozi believes the opportunity in baby care lies in curation and premiumisation.

Sah said each sub-category within baby care presents a different operational challenge. Consumables require deep availability of long-tail brands, while fashion depends on filtering products for quality rather than listing everything available. Ozi, which delivers wipes, diapers, and baby food, deliberately curates brands instead of maximising assortment, targeting parents willing to pay slightly more for trusted products.

“The customer behaviour has shifted from discovery first to search first,” Sah said, adding that shoppers today are not necessarily looking for ultra-fast delivery, but nor are they willing to wait several days. “A modern-age customer values quality. They are happy to pay an 8-10% or 12% differential, but they need quicker access to better brands and better assortment.”

Fashion startups argue that their challenge is different altogether.

Gulati said Slikk has built its business around supply rather than customer acquisition, claiming that stronger assortment has helped steadily reduce acquisition costs. The company replaces 30-40% of inventory in every dark store each month and is expanding neighbourhood by neighbourhood instead of spreading rapidly across cities.

Slikk might also consider introducing private brands for apparel, given their higher margins, Gulati said.

Bengaluru-based fast-fashion e-commerce startup Knot, which raised $5 million from 12 Flags and Kae Capital in December 2025, is investing heavily in back-end technology. Its app captures user preferences through swipe-based interactions, while its dark stores carry much wider assortments than horizontal quick commerce operators – offering a vast, multi-category collection of goods – and customise inventory based on local demand.

“We look at fashion as a data science problem and not really an intuition problem,” co-founder and chief executive officer (CEO) Archit Nanda said.

Nanda said fashion’s long-tail nature—which relies on selling small quantities of several unique products rather than depending on a few popular items – means inventory commonality across dark stores is significantly lower than grocery, requiring specialised supply chains and hyperlocal merchandising.

The profitability test

The changing strategies also reflect growing investor scrutiny of unit economics.

Slikk’s Gulati said investors continue to back the category but increasingly want proof that businesses can balance growth with profitability rather than relying on heavy customer acquisition spending. He believes execution in neighbourhood-level operations, assortment and brand partnerships will ultimately determine the winner.

Knot’s Nanda said that fashion combines high average order values with healthy margins, making the category attractive despite its complexity.

However, analysts believe that not every vertical is equally suited to the model.

“Looking ahead, horizontal cross-subsidy will work better, with established, well-capitalised players (Myntra’s M-Now, Nykaa Now) including quick delivery into an existing catalogue and logistics network rather than building it standalone. For narrow, high-trust verticals (medicines, baby care) where the value is availability and authenticity rather than impulse, and where margins can support the delivery cost, quick commerce can work,” Dutta noted.

Kalaari Capital’s 2025 report on vertical quick commerce similarly argued that specialised players will win by solving category-specific pain points, with assortment depth, customer experience, and category expertise emerging as key differentiators.

(Published in MINT)

admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

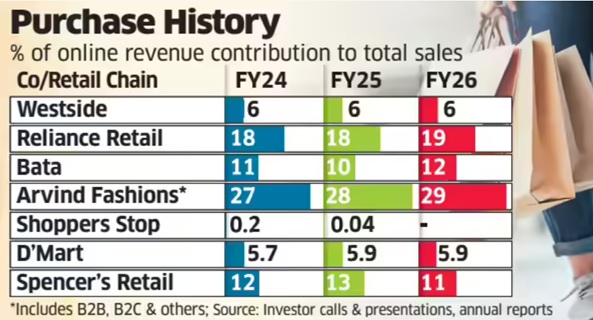

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 6, 2026

Anees Hussain and Kartikay Kashyap, Financial Express / Brand Wagon

6 February 2026

Swiggy Instamart’s Noice has consciously rejected every aesthetic that defines platform house brands. Its visual identity doesn’t sport minimalist colours or whites, no clean sans-serif, no ‘discount alternative’ signalling. Instead it uses Indian truck art inspired design with neon colours and bold text. That design architecture also personifies Swiggy’s big gamble.

Noice isn’t just a private label chasing margin expansion. It’s a differentiation play by a company that’s losing ground in a war in which being faster and cheaper is no longer enough. Early data suggests that Noice is finding traction. In namkeens, sweets, and western snacks, Noice holds a 4.4% market share on Instamart as of December 2025, competing against category leaders like Haldiram’s (16.7%) and Lay’s (9%), according to 1digitalstack.ai. This segment generated between ₹41-60 crore per month in the September-December period, with Noice’s share translating to roughly ₹1.8-2.6 crore a month. In beverages (fruit juice, mocktails, energy drinks, tea, coffee and soda), Noice more than doubled its platform sales share -from 2.6% in July to 5.8% by December. The brand now ranks 12th overall, ahead of Coolberg and gaining on established players. Category leader Real’s share fell from 12.3% to 9.5% over the same period. The beverage category generated ₹13,920.3 crore per month during July-December, with Noice’s December share of 5.8% representing about ₹88 lakh in monthly sales. Modest but shows velocity.

Bhushan Kadam, senior vice president, White Rivers Media, says the platform enjoys certain struc-tural advantages: “Swiggy has a credible shot at building Noice into a meaningful private label play because quick commerce (q-commerce) in India is still in a high-growth phase and Swiggy already has the scale, infrastructure, and customer base to drive repeat consumption.”

Swiggy’s own performance with private labels on q-commerce has been positive. Its Supreme Harvest brand, spanning pulses, oils, spices, and dry fruits has achieved just over 20% platform penetration, accord-ing to 1digitalstack.ai. The broader private label landscape offers both encouragement and caution. Tata Digital-owned BigBasket (BB) remains the clear winner, with private labels accounting for nearly 33% of its total revenue. But BB has a crucial advantage: Sourcing infrastructure inherited from Tata’s retail operations that provides scale – and supply chain depth that pure-play q-commerce platforms are still only building.

Noice isn’t Swiggy’s first experiment with owned brands. In May 2025, the company sold its cloud kitchen brands – The Bowl Company, Homely, Soul Rasa, Istah – to Kouzina Food Tech after years of trying to operate its own restaurants. Those brands required Swiggy to manage kitchens, hire chefs, and compete with thousands of independent restaurants. Unit economics never worked out.

Noice represents a fundamentally different model. Instead of large manufacturers optimised for extended shelf lives, Noice works with regional food makers producing in small batches. Launched mid last year with 200 SKUs across 40 manufacturers, it has expanded to over 350 products from 60 makers across 20-plus categories. Packaged versions of items like paneer and rasgullas from the mithai shop fail to resonate with consumers because they might use preservatives and taste artificial. Other offerings include biscuits made with butter instead of margarine, Punjabi lassi with seven-day shelf life delivered everyday like milk.

“Noice seems to be purpose-built for q-commerce: Impulse driven categories, low switching costs and algorithmic discovery. That alone fixes the biggest flaw of Swiggy’s past private label experiment,” says Ankur Sharma, cofounder, Brandshark. It is trying to do things for which customers come back to the platform – “products that are not there on any other platform”, adds Satish Meena, advisor, Datum Intelligence.

Uphill climb

Unlike other private label brands owned by Blinkit and Zepto who largely deal in non-perishable products, Swiggy-owned-Noice currently has a 50-50 split between perishable and non-perishable categories. Perishable products fetch 25-45% margins compared to 15-25% on non-perishable private labels and just 10-15% on third-party FMCG brands. Short shelf lives that enable freshness also mean higher wastage risk if demand forecasting fails. The solution Swiggy is testing hinges on shifting the capex risk entirely to small manufacturers while using its distribution scale as a leverage.

That apart, competition in q-commerce has intensified sharply over the past year. Reliance Retail’s JioMart, Flipkart Minutes, and Amazon Now have entered meaningfully with aggressive pricing. Zepto slashed minimum order values and waived customer fees at ₹149. Swiggy waived platform fees – but only on higher-value baskets at ₹299, essentially ceding low-AOV (average order value) products that drive frequency. In the meantime, market leader Blinkit’s gross order value reached nearly twice that of Instamart’s.

In q-commerce’s brutal pricing war, it is execution that will determine if Noice becomes a genuine differentiator or just another private label. “Proving Noice is not ‘just another’ private label would be the biggest challenge for the company,” says Devangshu Dutta,, founder and CEO, Third Eyesight.

(Published in Financial Express/Brand Wagon)

admin

February 2, 2026

Sakshi Sadashiv, MINT

Bengaluru, 02 Feb 2026

BRND.ME, a roll-up commerce company, expects to complete its reverse flip (change of headquarters) from Singapore to India by March, clearing a key regulatory hurdle as it prepares to tap Indian public markets with an IPO.

Despite the rise of private labels from quick-commerce giants such as Swiggy Instamart and Zepto, CEO Ananth Narayanan remains confident. He argues that BRND.ME’s core categories—spanning complex, value-added products such as specialized haircare and niche party supplies—possess a level of brand loyalty and complexity that is difficult for generic retail labels to replicate. While private labels are currently displacing national brands in high-frequency, simple categories like dairy and staples, Narayanan believes the company’s core categories remain protected from this encroachment as they drive searches.

Having shifted its strategy from aggressive acquisitions to organic scaling, the company is now doubling down on its four largest brands: MyFitness (peanut butter), Botanic Hearth (haircare), Majestic Pure (aromatherapy), and PartyPropz (celebration supplies).

About 10-15% of BRND.ME’s India business currently comes from quick commerce, a channel the company plans to scale, Narayanan said. The company is the leader in party supplies on quick-commerce platforms, benefiting from impulse-driven demand. “People forget birthdays and anniversaries, so it’s a classic category to build a brand on quick commerce,” he said. The category contributes about ₹200 crore of revenue. The company also leads the peanut butter category through MyFitness, with a 30% market share on all quick commerce platforms and annual revenue of ₹270 crore.

The company’s revenue run rate stands at about $200 million. Male consumers worried about male-pattern baldness now account for about 35% of haircare sales. The company aims for a 10-fold jump in aromatherapy and haircare sales from $6 million to $60 million within four years, led by Majestic Pure and Botanic Hearth.

Drawing on his experience running Myntra, Narayanan said that private labels typically have a ceiling. “Even when we pushed hard on private labels at Myntra, they never went beyond 25-30% of the overall portfolio. That tends to remain the case as the categories we operate in are very hard to displace because we drive searches.”

This dynamic is already visible across several quick-commerce categories. The peanut butter segment is heavily consolidated on Blinkit, with Pintola and MyFitness together accounting for about 73% of sales, according to data from Datum Intelligence. Similar patterns have emerged in other categories. Blinkit’s popcorn segment, for instance, has rapidly consolidated into a duopoly, with 4700BC and Act II controlling 99% of sales.

Private labels muscling in

While Blinkit has consciously avoided launching private-label products on its platform, Swiggy has done so through Noice, and Zepto through Relish and Daily Good. For established brands, these private labels are becoming harder to ignore. Swiggy has scaled Noice aggressively, expanding the portfolio from about 200 to 350 stock keeping units (SKUs) and onboarding more manufacturing partners while moving beyond staples into categories such as beverages and ready-to-cook foods. These products are aimed at delivering significantly higher margins of 35-40%, compared with 10-15% on third-party brands, Mint reported earlier.

Private labels now contribute an estimated 6-8% of quick-commerce sales, up from 1-2% two years ago, according to data from 1digitalstack.ai, though penetration in perishables remains limited because of supply-chain complexity and quality concerns. A broader push into fresh categories could lift private-label share to 10-15%. Noice has already captured 3.4% of wafer sales and 1.9% of biscuit sales on the platform within months of its launch, according to 1digitalstack.ai data. The two categories are dominated by Lay’s and Britannia, which have a market share of about 35% each in their respective segments.

Zepto’s private-label push spans multiple everyday categories, including Relish for meat products, Daily Good for staples, Chyll for ice cubes and juices, and Aaha! for snacks, sweets, cereals and batters.

This growing presence creates a structural ‘trap’ for digital-first brands. Devangshu Dutta, chief executive at Third Eyesight, a consultancy firm, said, “Brands that are overly dependent on a single sales platform remain structurally vulnerable to being replaced by the platform’s own private labels, which are designed to capitalise on product opportunities that already have proven demand.” Platforms, he explained, tend to dominate high-frequency purchases, often undercutting brands on both price and visibility.

Persistently high online customer acquisition costs add to the pressure, particularly if the customer relationship is owned by the platform rather than the brand. “This has been one of the significant friction points for all digital-only brands, and weighs especially heavily on companies that have online-heavy portfolios with multiple brands in play,” Dutta added.

(Published in Mint)