admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

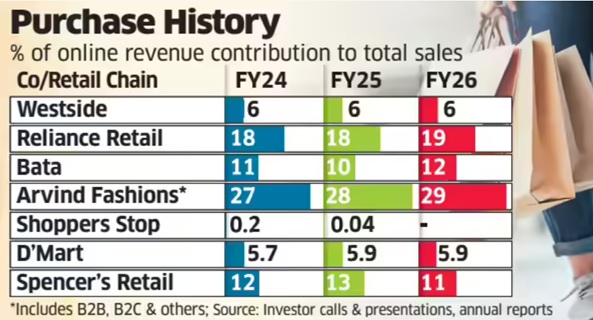

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

December 29, 2025

Yash Bhatia, Impact Magazine

29 December 2025

App, Tap, Pay and Zoom it’s delivered – that is Quick commerce for you. And in India, the narrative has so far been defined by speed, scale, high SKU counts, and the dominance of dark stores. Last week, however, Instamart nudged that model by opening an experiential store in Gurugram, allowing consumers to see and feel select products available on the platform.

The Bengaluru-based company has positioned the outlet not as a conventional retail store, but as a compact experiential format with a sharply curated assortment of around 100–200 SKUs, compared to the 15,000–20,000 SKUs typically housed in a dark store. Spanning roughly 400 sq. ft., the space is about one-tenth the size of a standard 4,000 sq. ft. dark store.

Under this model, sales proceeds are paid directly to sellers. This differs from Instamart’s regular arrangement, where payments are routed through the platform and later settled with sellers after deducting the platform’s share. IMPACT reached out to Instamart for further details, but the company declined to comment.

Sources close to the development say that Instamart has enabled sellers to open branded experiential stores in and around residential societies as part of a targeted consumer experiment. These are not conventional retail outlets, but compact experiential formats with a highly curated SKU assortment, focused on categories where consumers prefer to assess the products first-hand before purchasing, such as fresh fruits, vegetables, pulses, new product launches, and selected D2C brands. The initiative is largely centred on fresh categories and allows sellers to experiment with Instamart’s branding and service ecosystem.

Devangshu Dutta, Founder, Third Eyesight, a retail consultancy firm, says that physical presence plays a vital role in anchoring trust, particularly in premium products, groceries, and fresh produce. “Experiencing a product or brand physically can significantly enhance perceived value and help create stickiness. For this reason, offline stores continue to remain integral to the consumer products sector,” he explains.

Built on the promise of speed and convenience, quick commerce brands have come under growing scrutiny for quality and hygiene lapses at dark stores. Over the past year, several reports have flagged issues ranging from poor storage conditions and compromised freshness to the sale of expired or damaged products, particularly in food and grocery categories.

In some instances, regulatory inspections have led to licence suspensions after authorities identified hygiene violations at fulfilment centres. “Trust is what builds loyalty, and the shift is clearly moving from minutes to confidence,” says Shankar Shinde, Co-Founder, Aisles and Shelves, a behaviour-led brand consultancy in India. Shinde adds that the emergence of offline formats such as Instamart’s physical store aligns with this transition, particularly in grocery and fresh categories where consumers place a high premium on quality and consistency. “Physical touchpoints help reduce consumer anxiety, especially in a market like India, where shoppers still prefer hand-picked fresh produce such as fruits and vegetables,” he explains.

Against this backdrop, the opening of experiential centres could emerge as one way for quick commerce players to rebuild consumer trust by allowing shoppers to experience products in person before purchasing. IMPACT also reached out to Blinkit and Zepto for their views, but both declined to comment.

Kushal Bhatnagar, Associate Partner, Redseer Strategy Consultants, believes the move is aimed at unlocking incremental growth by tapping into offline-first consumers who are not yet active on quick commerce, while also catering to the offline purchase missions of existing quick commerce users. He notes that quick commerce currently reaches only about 75–80 million annual transacting users as of CY2025, even as over 90% of India’s grocery consumption continues to take place offline.

Beyond expanding reach, Bhatnagar sees offline formats as a way to address deeper trust barriers within the category. He adds that such formats can help deepen consumer confidence, particularly in categories where apprehensions around quality and freshness persist in quick commerce deliveries, concerns that are partly alleviated when consumers can experience products first-hand. Additionally, he points out that this approach benefits brands, especially emerging ones that are largely confined to quick commerce or a limited set of platforms, by giving them greater physical retail visibility without requiring heavy investment in traditional distribution networks.

Viewed through a financial lens, the move also carries implications for how quick commerce platforms justify value. Saurabh Parmar, fractional CMO, believes the initiative signals a shift from promise to performance, with a stronger emphasis on optimisation and a more realistic assessment of long-term value creation. He notes that while quick commerce has expanded into Tier 2 markets and seen growth in user numbers, these metrics alone still fall short of fully justifying current valuations. In this context, an offline presence becomes another lever to strengthen the overall business case.

At the same time, Parmar cautions that offline formats cannot replace the core proposition of quick commerce. He adds that experiential centres enhance brand credibility and make quick commerce feel closer to conventional retail, with the potential to eventually extend into other facets of e-commerce. However, he emphasises that quick commerce must continue to remain the frontline, as the sector’s valuations are fundamentally anchored in its speed-led proposition.

Retail experts, meanwhile, view physical touchpoints as a long-standing mechanism for building trust rather than a structural shift.

Dutta adds that such formats complement existing digital trust mechanisms such as delivery consistency, speed, ratings, and reviews by making brands feel tangible and accountable rather than abstract.

Bhatnagar notes that quick commerce currently has an average monthly transacting user base of around 40 million as of CY2025, leaving significant headroom for growth when compared to India’s overall e-commerce base of nearly 300 million active transacting users.

Beyond expanding the user base, he adds that experiential stores can also support wallet-share expansion across categories, which remains a key growth lever for the sector. “Non-grocery segments such as beauty and personal care, electronics, and fashion currently contribute about 25% of quick commerce GMV (Gross Merchandise Value), a share that is expected to rise further. Within groceries as well, platforms can drive incremental growth by building greater depth in fresh produce and staples,” Bhatnagar highlights.

From an operational perspective, however, the offline format is viewed more as a supporting layer than a core growth engine. Dutta sees Instamart’s offline presence as an experimental add-on rather than a replacement for its delivery-led model. The operating processes and economics differ significantly from those of quick commerce delivery, positioning physical formats as a complement to the speed proposition rather than an alternative. If the model proves viable and is backed by sufficient resources, it could eventually lead to a parallel scale-up of dark stores and experiential formats across different catchments.

For now, Instamart’s offline foray remains a tightly scoped experiment rather than a strategic pivot. Its significance lies less in square footage and more in what it signals about the evolving priorities of quick commerce. As the category matures, speed alone may no longer be sufficient to secure trust, loyalty, or long-term value. Experiential touchpoints, if deployed selectively, could help platforms bridge the gap between digital convenience and physical reassurance, particularly in categories where quality perception continues to remain fragile.

(Published in IMPACT)

admin

November 18, 2025

Chris Kay, Krishn Kaushik and Andrea Rodrigues in Mumbai

Nov 18 2025

Just before dawn, Kashif Sameer joins dozens of couriers zipping across Mumbai to deliver items stocked in a basement of a shopping mall run by Reliance Industries.

“I make between 20 and 30 deliveries in a day,” said the 25-year-old, who had just driven a mile across the chaotic roads of the Indian megacity to drop off groceries ordered 15 minutes earlier. “It is very popular with customers.”

The buzzing activity at the so-called dark store, a mini-warehouse operated by Reliance’s ecommerce platform JioMart, is part of a renewed push by the conglomerate’s chair and Asia’s richest man, Mukesh Ambani, to reassert his company’s position in India’s retail market.

It has added hundreds of dark stores to operate a total of nearly 20,000 physical outlets this year — almost double its pre-pandemic size — as it battles for dominance against Blinkit, Swiggy and Zepto in the country’s ballooning quick-commerce market.

“It’s a question of who runs out of money first,” said Arvind Singhal, chair of retail consultancy The Knowledge Company. “We will see some kind of a shakeout.”

Despite its large network of physical stores, Reliance has yet to corner the domestic consumer market like it did with telecoms a decade ago. It faces entrenched competition from established domestic and international rivals, as well as millions of kiranas, family-run convenience stores.

The sprawling Tata Group operates a wide range of consumer businesses, while global multinationals such as Unilever and Nestlé are important players in India’s household goods market.

Reliance Retail, the division that contains all of the conglomerate’s consumer-facing units, had shed tens of thousands of employees and closed underperforming stores following a bloated build-out during the Covid-19 pandemic and slowing middle-class spending.

But India’s most valuable company, which has a market value of more than $225bn and operates across oil refining, telecoms and entertainment, is expanding its retail reach again.

Reliance Retail’s latest results point to a rebound. In the quarter ending September, the unit reported revenue of about $10bn and profit of $390mn, up 18 and 22 per cent respectively from the previous year.

“Reliance’s scale in retail now is unmatched in India,” said Devangshu Dutta, chief executive of consumer advisory company Third Eyesight, in reference to the breadth of the conglomerate’s business. “This scale is unique in India and rare in global retail.”

Ambani’s retail ambitions are being led by his 34-year-old daughter, Isha. In August, she detailed plans for Reliance’s consumer brands subsidiary, which has a portfolio including Lotus Chocolate and the recently revived nostalgic Indian soft drink Campa Cola, to reach $11.7bn in revenue within five years.

Ultimately, the goal was to “become India’s largest FMCG company with a global presence”, said Isha Ambani during Reliance’s annual meeting.

The company told the Financial Times that it continued to “reinforce its position as India’s largest retailer, expanding its nationwide network”.

While Ambani originally indicated that he wanted to list Reliance Jio Infocomm, the telecoms unit, and Reliance Retail by 2024, people familiar with the company said the retail unit was not ready to go public. The billionaire said the Jio listing could happen in the first half of next year.

“Competitive intensity in every category in the discretionary retail side has picked up very sharply,” said Karan Taurani, executive vice-president at Elara Capital, who does not expect Reliance Retail to float for at least two years. “New competitors, new brands have come in and they are challenging the larger incumbents.”

The Ambanis, who operate as gatekeepers for foreign companies seeking access to India’s massive but challenging business landscape, have sought to cement their position through a spate of partnerships with western retail brands.

Foreign brands including West Elm, Pottery Barn and Superdry have stores in Reliance’s shopping malls in upmarket Mumbai. However, those joint ventures have largely struggled to gain traction with shoppers in India, where the per capita income remains less than $3,000.

The conglomerate’s foreign brands business housing these joint ventures lost Rs2.7bn ($30mn) in the financial year through March 2025, according to the latest available accounts. The Knowledge Company’s Singhal called Reliance’s push to bring international names to India “a vanity project”.

Reliance’s high-profile partnership with fast-fashion retailer Shein has also been underwhelming. The company returned to India this year under Reliance’s wing after being booted out in 2020 when relations between New Delhi and Beijing soured following military clashes along their disputed border.

Shein’s app has been downloaded just 11mn times, according to market intelligence firm Sensor Tower. Its discount prices are largely matched, if not undercut, by many Indian ecommerce and fashion retailers, say analysts.

Reliance is investing heavily in quick commerce, where deliveries are promised in 30 minutes or less. Bank of America estimates the market could reach $128bn by 2030.

The field is at present dominated by Blinkit, Swiggy and Zepto, which together control more than 90 per cent of the quick commerce delivery market and compete with Amazon and Walmart-owned Flipkart. None of the companies are profitable.

The Ambanis are eager to catch up. Over the past six months, Reliance has built about 600 dark stores across cities to plug gaps in its vast store network. By contrast, market leader Blinkit operates about 1,800 dark stores.

In quick commerce, “we have to be there because everybody is”, said a person close to the conglomerate. “It is a long-term strategy.”

On a call with analysts last month, Reliance Retail’s finance chief Dinesh Taluja admitted to delays in entering quick commerce. But he insisted that Reliance offered better prices, more variety and wider reach across smaller Indian cities where it is often the only formal retailer.

“The competition today is mainly in the top 10, 20 cities,” Taluja said. “We are present in almost a thousand cities. Competition will take many years to reach where we already have a head start there.”

Still, Reliance was facing an uphill battle, warned Elara’s Taurani. “JioMart is making a late entry,” he said, “it will be very tough to disrupt players here.”

(Published in Financial Times, all copyrights owned by FT)

admin

September 5, 2025

Pooja Yadav, Exchange4Media

4 September 2025

Quick commerce today is no longer just about delivering groceries in 10 minutes. It has emerged as one of India’s most coveted retail media channels, where brands are willing to pay a steep premium for visibility.

If FY25 was about building scale, FY26 is definitely shaping up to be about pricing power. With consumer adoption of 10–20-minute delivery apps surging, advertisers are competing for limited inventory, pushing ad rates up by 30–50% year-on-year.

“Ad rates on quick commerce platforms have surged by 30–40% year-onyear, especially during high-impact windows like festive seasons and major cricket events. This is fuelled by rising user engagement and proven performance outcomes. With more sophisticated ad formats and attribution models now in play, advertisers increasingly view the premium as justified,” added Uday Mohan, COO, Havas Media India & Havas Play.

Scale, Pricing & Soaring Ad Rates

While agencies point to surging demand, market data shows that platforms themselves are firming up monetisation models with steep onboarding thresholds.

As per market estimations, Swiggy Instamart offers tiered onboarding packages ranging from ₹4.5 lakh to ₹10 lakh, adjustable against advertising spends over a three-month period. Zepto reportedly asks new or small brands to commit anywhere between ₹2 lakh and ₹7 lakh per month on ads, depending on the category. Blinkit, on the other hand, charges ₹25,000 per SKU per state as a non-refundable onboarding fee, which is credited to the brand’s ad wallet.

This aggressive push comes against the backdrop of a sector that has grown at breakneck speed. According to CareEdge Analytics’ July 2025 data, India’s quick commerce market was valued at around ₹64,000 crore in FY25, growing at a staggering 142% CAGR during FY22–FY25 on the back of evolving consumer preferences, hyperlocal infrastructure, and a low base.

The momentum is expected to continue with strong double-digit growth over the next few years, as adoption deepens in Tier II & III cities, delivery networks expand, and instant fulfilment becomes mainstream.

At the same time, platforms are pivoting from pure hypergrowth to sustainable profitability—tapping into advertising, subscriptions, private labels and tech-led inventory optimization as key revenue levers. This shift is being enabled by India’s expanding digital backbone: with over 1.12 billion mobile connections and 806 million internet users (a 6.5% YoY rise), the country is projected to cross 900 million internet users by the end of 2025. Rising smartphone penetration in both urban and rural areas, aided by affordable data and policy support, has created one of the world’s largest online consumer pools, with 270 million e-shoppers in 2024, making India the second-largest e-retail market globally.

Unsurprisingly, advertisers are flocking to these platforms because that’s where their consumers are. Even though seller commissions contribute the bulk of revenues (68–74%), ad placements and brand boosts already account for 9–11%. Industry data shows that ad rates on quick commerce apps have climbed by 30–50% in just a year, with premiums doubling during high-impact windows like festivals and cricket tournaments. This steep inflation reflects both rising consumer traffic and the limited nature of in-app inventory, pushing brands to pay top dollar for guaranteed visibility at the point of purchase.

Bain’s ‘How India Shops Online 2025’ report also underscores this momentum: beauty, personal care, and snacking categories are already outpacing overall e-retail growth, and these are the very segments leaning most aggressively into quick commerce ads.

“Ad rates on quick commerce platforms have jumped by nearly 40–50% compared to last year. This spike reflects that premium brands are willing to pay for immediacy and guaranteed visibility, where ad placement directly links to instant purchase behaviour,” said Mandar Lande, founder of Waayu, a zero-commission food delivery app in India.

According to Aditya Aima, Managing Director, Growth Markets; Co-MD, India & MENA, AnyMind Group, ad rates on quick commerce platforms have not only risen but demand has intensified. “The surge is fuelled by three dynamics: sticky consumer behavior with high visit frequency, dense purchase intent compared to social or entertainment platforms, and the scarcity of ad real estate.”

Quick commerce becomes a strategic channel

For brands, quick commerce has moved far beyond being a fulfillment partner. It has become a strategic advertising channel, especially for those in fast-moving and competitive categories like beauty, wellness, snacks, and personal care. The platforms offer not just last-mile delivery but also front-of-shelf visibility in an increasingly cluttered digital environment.

According to Seshu Kumar Tirumala, Chief Buying and Merchandising Officer, bigbasket, “Brands are moving beyond purely search-centric strategies and increasingly adopting immersive display activations with formats like Spotlight Videos, Banners with Add-to-Cart (ATC), targeted banners, and ATC widgets. For established brands, most investments still flow into performance-led formats such as Sponsored/PLA ads, while a portion is reserved for top-funnel initiatives like storytelling, new launches, and high-visibility events. Emerging or smaller brands usually begin with awareness and consideration campaigns before shifting focus toward performance once they’ve built stronger customer connections.” Unlike marketplaces or social media, quick commerce blends data-led targeting, high engagement, and measurable ROI.

Many brands pair Q-comm placements with collab ads on Meta, Google, and Criteo to build visibility while keeping consumers engaged across the funnel. This creates a sharper, closed-loop system where awareness, consideration, and conversion happen almost instantly. “D2C brands have been rapidly scaling up ad spends on quick commerce platforms, up to 40–50% year-on-year, with a significant share during the festive season. Among the key reasons are fast-growing adoption of Qcomm by consumers and better ROI than marketplaces,” said Shrikant Shenoy, AVP at Lodestar UM.

What sets this instant delivery model apart is its ability to compress the purchase journey. Marketplaces drive comparisons, and social platforms spark discovery, but Q-comm taps into impulse buying with SKU-level attribution.

“The quick delivery model encourages impulse purchases and immediate gratification shopping, which is particularly valuable for D2C brands. Qcomm platforms have lower competition density, and ad formats are more native and less cluttered than traditional e-commerce,” said Devangshu Dutta, founder of Third Eyesight.

“When someone opens Blinkit or Zepto, they’re usually in active purchase mode, not just browsing. For consumables, personal care, or lifestyle products, this is the sweet spot of marketing,” Dutta noted.

“Ad rates on quick commerce have gone up by more than 20% in the last year. If you want a prime slot, say a homepage banner in a big city, you might even be paying 50% more than last year. Because every brand wants it. When a Blinkit or Swiggy placement can move your product in minutes, not weeks, those ads aren’t just distribution, they are discovery,” said Mohit Singh, Head of Product at Zippee, a quick commerce logistics platform.

Meanwhile, pricing pressures are only going up. Ratnakar Bharti, VP, Media, Mudramax said, “Quick commerce isn’t just ‘fast delivery’ anymore, it has become high-intent retail media sitting right next to the ‘add to cart’ button, with sales that can be measured in real time. Quick commerce platforms say their ads business grew 5X in a year to about $200M ARR. At that kind of scale, inventory quality improves, targeting gets sharper, and the medium starts looking like the next big retail media play.”

“In a nutshell, expect meaningfully higher prices in peak weeks — often up to 2x — and a higher year-round floor price due to steeper minimums and fees. The trade-off is harder proof of sales at the exact SKU, which is why demand and prices are rising,” Bharti added.

“Brands pay a premium for Q-Comm because it drives sales at the point of purchase. What began as experimental spends has now become a steady line item in media plans, thanks to strong ROI and proven results,” added Jatin Kapoor, MD, AdsFlourish.

Beauty, beverages & snacking lead the charge

Notably, not all categories are leaning on quick commerce equally. Industry executives point out that beauty & personal care, beverages, snacking, and wellness are the biggest spenders, given their high repeatability, impulse-driven nature, and urban skew.

Beauty and personal care brands, for instance, are using Q-comm not just to drive trial packs and quick replenishment, but also to run festival-led campaigns targeting affluent millennials. Similarly, beverages and packaged snacks are thriving on the “in-the-moment” consumption occasions that these apps uniquely enable.

“The biggest spenders are beverages, beauty, packaged foods, and wellness. Those categories thrive on impulse and repeat consumption, which is exactly what quick commerce delivers best,” Singh added. As per many industry experts, wellness and lifestyle brands, too, are seeing outsized returns. From daily supplements to discreet personal care items, quick commerce is proving to be a low-friction purchase environment with high conversion rates.

“Quick commerce platforms have lower competition density, and ad formats are more native and less cluttered than traditional e-commerce,” explained Dutta.

Media buyers also note that Q-comm platforms are evolving fast, offering more contextual in-app placements and data-driven targeting. This is creating a level playing field for challenger brands that lack legacy shelf space in offline retail.

“Quick commerce advertising is inherently contextual. A beverage or snack brand running an IPL campaign is literally tapping into the consumer’s 15-minute window of intent, it’s that instant,” added Mohan.

With ad rates on quick commerce platforms climbing 30–50% year-on-year, it’s clear the medium is shifting from experimental budgets to a core retail media channel. However, with competition heating up, festive weeks commanding 2X pricing, and minimum spends rising, the question is: how long before quick commerce ads start resembling the crowded, high-cost landscape of traditional e-commerce marketplaces?

(Published in Exchange4Media)

admin

May 25, 2025

Gargi Sarkar, Inc42

25 May 2025

SUMMARY: Swiggy and Zomato are scaling back non-core bets such as 10-minute food delivery, private labels, and event logistics to sharpen focus on core businesses and improve profitability. Both companies are betting on platform fees and selective verticals like quick commerce and ticketing, but analysts warn that financial discipline, not endless expansion, is key to long-term sustainability. The foodtech duo is stuck in a balancing act of rationalising what works and doesn’t. However, going ahead, this rationalisation game is only going to get more pronounced as they will strive to shield their core bread and butter businesses

For foodtech giants Swiggy and Zomato (now Eternal), the last few years have been about engaging in a battle for expansion, so much so that it has become difficult to tell them apart.

From quick commerce and cloud kitchens to intercity food delivery and even selling tickets for events and concerts, the two companies appear to be aping each other’s every move to be everything everywhere all at once.

However, what began as a bold bet to dominate every possible vertical falling under the ambit of food, lifestyle and entertainment is now undergoing a major course correction.

For starters, both are reconsidering their blitzkrieg, and while at it, they are gracefully stepping away from non-core bets, diluting underperforming or experimental units to focus on core operations to drive profitability.

For context: Zomato, which once saw the future of food logistics in ultra-fast deliveries, gave up on its 15-minute food delivery service, Quick, four months after its launch in January. It has also pulled the plug on its home-made meal service, Zomato Everyday. Tailored for office-goers and budget-conscious consumers, the service was floated in January 2025.

Swiggy, too, has made similar retreats. It suspended Swiggy Genie, its courier and pick-up-and-drop service that had gained popularity during the pandemic. The company also gave up on its private label food business by entering a strategic agreement with Kouzina, a chain of virtual restaurants, granting it exclusive rights to operate Swiggy’s digital-first food brands.

So, what has triggered this metaphorical fission in strategy?

One possible reason could be the growing realisation that profitability hinges on diversifying smartly rather than untamed expansion.

A market analyst, who did not wish to be named, pointed out that the duo’s attempt to rule their customers’ wallets for everything from food to groceries and entertainment to lifestyle has been quite ambitious. “The course correction was overdue,” the analyst said.

He believes that foodtechs are now forced to burn the visceral fat in the form of non-core businesses because those have been slowing them down, also eating into the revenues of core businesses and impacting operational efficiencies.

“Moreover, the more the segments, the higher the chances of operational hiccups. Managing logistics, customer experience, and quality control across a wide array of verticals inevitably leads to fragmentation and strain on core operations,” he added.

State Of Eternal Affairs: Zomato’s Diversification Saga

Eternal’s push to transform Zomato into a broader lifestyle platform in 2024 was not only about ambition but also a strategic response to a slowing core business — food delivery, according to industry observers.

Also, a glance at the table below reveals how the company has seen a marginal QoQ increase in its monthly transacting users.

In terms of monthly transacting customers, Zomato’s food delivery growth began strong with a 6.84% QoQ jump in Q1, but momentum quickly slowed, and Q2 saw only a 1.97% sequential rise, followed by a slight decline of 0.97% in Q3. This dip signalled stagnation, and although Q4 showed a mild recovery (1.95%), overall FY25 growth of the company’s monthly transacting users (food delivery) was modest at just 2.96%

Interestingly, Eternal founder and CEO Deepinder Goyal, too, acknowledged a slowdown in the company’s food delivery business while announcing the company’s Q4 FY25 results. He said the slowdown was due to rising competition from quick commerce platforms and weak discretionary spending. Goyal added that services like Zepto Cafe, Swiggy Snacc, and Blinkit Bistro, too, were eating into demand for restaurant deliveries.

In terms of Zomato’s food delivery numbers, average monthly transacting numbers grew to 20.9 Mn in Q4 FY25 from 20.5 Mn in Q4 FY24. Net order value (NOV) growth also remained subdued at 14% YoY versus the 20% YoY growth guidance.

Hence, the company was under pressure to unlock new revenue streams. Blinkit’s success became the reference point, and the company started envisioning similar success stories with other verticals too, a former Zomato employee said.

This was when the company got engulfed in the wave of diversification, paving the path for Zomato’s yet another bold move (besides Blinkit) — the INR 2,078 Cr acquisition of Paytm’s movies and events ticketing business, Insider, in August last year.

The acquisition that was planned with the launch of the ‘District’ app meant but one thing — declaration of war against BookMyShow, the lone behemoth in the realm of the entertainment ticketing segment. Even the company knew the path wouldn’t be all rainbows and sunshine.

In its Q4 FY24 earnings call, the management acknowledged that while the gross order value (GOV) of the going-out vertical continues to grow at over 100% YoY, the business still operates at an adjusted EBITDA loss of -2 to -2.5% of net order value (NOV).

Besides, given that the transition of users from Paytm’s ticketing business and Zomato’s dining out platform to the District app requires sustained investment, the company doesn’t expect the business to turn profitable in the near term.

But Zomato expects losses to eventually see stability at current levels.

“However, even with plateauing losses, the company will have to keep spending on creating supply. This means: curating new event experiences, forging partnerships and acquiring new users for the District app… and all of this translates into one thing — prolonged burn,” the market analyst added.

Moving on, Zomato’s ambition to become a lifestyle super app didn’t just manifest into flashy verticals like events, entertainment, and ticketing — it also showed up in its renewed aggression in food delivery, the very space where it first made its name.

Therefore, Zomato began piloting a 15-minute food delivery service in select parts of Mumbai and Bengaluru early this year.

But the company now finds the initiative extremely difficult to operationalise as it has failed to generate incremental demand.

“Customers do not necessarily want food fast, they just want it reliably. A 10-minute turnaround without full control over the supply chain leads to poor customer experiences, operational stress, and negligible upside. Instead of delighting users, it makes the company vulnerable to inconsistent quality and frequent delays,” a Zomato insider added.

Satish Meena, the founder of Datum Intelligence, opined that without controlling the entire supply chain, delivering food items within 10 to 15 minutes cannot be a profitable proposition.

Swiggy’s U-Turns

In 2024, also the year of its public listing, Swiggy aggressively expanded its service offerings, launching several new verticals to diversify beyond its core food delivery business.

Among the most prominent launches was Bolt, a 10-minute food delivery platform. Initially launched in Bengaluru, Chennai and Mumbai, Bolt quickly expanded to over 400 cities, with over 40,000 restaurants, including KFC, McDonald’s and Starbucks.

To complement Bolt, Swiggy introduced Snacc, a separate app for instant delivery of snacks, beverages, and small meals within 15 minutes.

Continuing to diversify its portfolio, Swiggy launched Pyng, an AI-powered platform that bridges users with verified experts like yoga teachers or chartered accountants.

With this, Swiggy marked its entry into the on-demand services marketplace, making professional services easier to access.

Apart from these customer-facing services, Swiggy also entered events via Scenes and the B2B space with Assure, to keep pace with Zomato.

Interestingly, Swiggy, too, has begun consolidating its operations. The company has shut down Genie, its hyperlocal courier business, which competed with Porter, Borzo and Uber.

According to a competitor, sourcing delivery riders specifically for packages is a challenge, particularly in cities like Bengaluru. For Swiggy, which was already managing fleets for food delivery and quick commerce through Instamart, sustaining a separate rider network for Genie only added to the complexity.

In another such move, Swiggy exited its private label food business by transferring exclusive rights for its digital-first brands, including The Bowl Company and Homely, to cloud kitchen operator Kouzina.

Balance Sheet Blues

Imperative to highlight that the rollbacks by Zomato and Swiggy are rooted in the growing pressures on their respective balance sheets.

After diversifying at a breakneck speed, they are now faced with the hard realities of cost structures that don’t always align with revenue potential.

In Q4 FY25, Zomato and Swiggy both reported robust top-line growth. Zomato’s revenue surged to INR 5,833 Cr, largely buoyed by its three core pillars — the food delivery business (INR 1,739 crore), Blinkit’s quick commerce arm (INR 769 Cr), and Hyperpure, its B2B supply chain vertical, which posted a 99% YoY growth in revenue to INR 1,840 Cr.

However, despite the momentum, the company’s net profit declined sharply to INR 39 Cr in the quarter, largely thanks to ongoing investments in Blinkit and newer bets like the ‘District’ lifestyle app.

Meanwhile, Swiggy clocked INR 4,410 Cr in revenue in Q4, up 45% YoY, but saw its net loss nearly double to INR 1,081 Cr. The widening losses were fuelled by surging operational expenses.

“All of this explains the strategic pullbacks witnessed lately, Swiggy exiting Genie and private labels, Zomato pulling the plug on services like Quick and Legends. The rationalisation marks a reset, indicating that while growth via diversification was necessary, financial discipline and profitability are in the spotlight,” the market analyst said.

Platform Fee To The Rescue… But For How Long?

While it won’t be easy for Zomato and Swiggy to suddenly change course, the future of these two foodtech giants is all about heading towards a more focussed set of revenue streams driven by value rather than FOMO.

In the process, both foodtech giants appear to have struck gold with the platform fee, which has grown from just INR 2 in 2023 to INR 10 today.

But the real question is: Can rising platform fee help the duo neutralise the impact of aggressive expansion? Or is rationalisation the only way forward?

Devangshu Dutta, the founder of Third Eyesight, thinks otherwise. He believes that the companies will not stop looking for new revenue streams, even as they will continue to amputate the ones that offer little value.

“All of these companies have to look for growth, which is a given. If their existing businesses are not delivering the kind of growth they need to justify their stock price or valuation, then they have to look at new avenues.”

According to him, we are bound to see a flurry of experiments, trials of different services and new verticals as these companies attempt to expand their addressable markets.

At the end of the day, the foodtech duo is stuck in a balancing act of rationalising what works and doesn’t. However, going ahead, this rationalisation game is only going to get more pronounced as they will strive to shield their core bread and butter businesses.

[Edited by Shishir Parasher]

(Published in Inc42)