admin

September 22, 2025

Christina Moniz, Financial Express

22 September 2025

It is already the largest player among organised fumiture makers with over 15% of the market. With 1,000 stores, it has the widest retail store footprint among organised players. The 102-year-old brand is also the second-largest revenue con-tributor to the parent enterprise.

So why is Interio tinkering with its name, logo and colour attributes?

“We want to move away from being viewed as a functional brand to more of a design-led lifestyle one. We have a wider range of offerings that are more modular and aesthetic,” says Reshu Saraf, head of marketing communications at Interio by Godrej.

As a first step, it has a new logo and name change – from Godrej Interio to Interio by Godrej. The brand has earmarked ₹50 crore towards an integrated campaign across TV, digital, outdoor and in-store branding to promote its new proposition over the next year. Overall, it will invest ₹300 crore in expansion and technology with the goal to more than double revenues to ₹10,000 crore by FY29.

Younger consumers don’t see furniture as utility but as lifestyle, observes Puneet Pandey, strategy head and managing partner, OPEN Strategy & Design. “By moving from ‘solid and sturdy’ to ‘stylish and aesthetic’, the brand earns the right to play at higher price points as well. Design-led positioning will also unlock repeat purchase since people no longer wait a decade to change their furniture based on utility; they want constant upgrades to refresh their living spaces as their tastes evolve,” he notes, adding that Interio needs to make the marketing leap from “catalogue to culture”.

Saraf says the brand is also building differentiation with its customer experience. “We’re using digital tools for store walkthroughs and visualisers to help visualise our products in the home. Our product portfolio, which is deeply personalised ane tailored for Indian sensibilities, it is a major differentiator that few other brands offer,” she points out.

E-commerce is also a focus area with the brand looking to increase the revenue share from 15% to 20-22% by 2029. The company is leveraging Al to improve the search functionand sharpen personalisation. Saraf adds the that offline too, the brand will have large format experience centres to help people envision what their rooms could look like, along with mid-size and small-format stores.

Interio also plans to widen its retail store footprint from 1,000 to 1,500 by 2029.

As per industry estimates, the Indian furniture market is set to grow at 11% annually to reach $64.1 billion by 2032 from $30.6 billion in 2025. It is this growth momentum that Interio is looking to cash in on.

Built-in differentiation

Although a significant chunk of Interio’s business comes from its home remodelling services, within the furniture category, it competes with global players like IKEA and digital-first brands like Pepperfry. The challenge for Interio in this market is to embed the design-led positioning in its productsandcus-tomer experience, says Nisha Sam-path, managing partner at Bright Angles Consulting.

One of its biggest advantages is the Godrej brand. “The Godrej brand stands for many values prized in interiors such as quality, trust, reliability and durability with a ‘Made in India’ tag. However, the brand has not been so successful in building an image of cutting-edge design and innovation. These are new values that can make the brand more contemporary,” she remarks.

Devangshu Dutta, CEO of Third Eyesight concurs, pointing out aside from nimble competition, Interio’s key challenges also come from the dual pressures of increasing consumer expectations for rapid delivery and customisation on the one hand, with aggressive price competition on the other.

(Published in Financial Express – Brandwagon)

admin

September 5, 2025

Pooja Yadav, Exchange4Media

4 September 2025

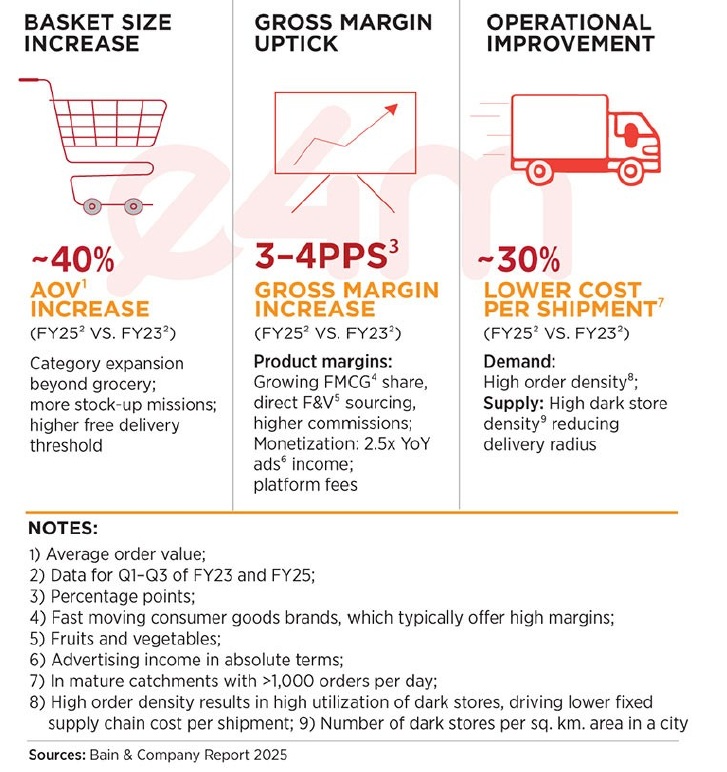

Quick commerce today is no longer just about delivering groceries in 10 minutes. It has emerged as one of India’s most coveted retail media channels, where brands are willing to pay a steep premium for visibility.

If FY25 was about building scale, FY26 is definitely shaping up to be about pricing power. With consumer adoption of 10–20-minute delivery apps surging, advertisers are competing for limited inventory, pushing ad rates up by 30–50% year-on-year.

“Ad rates on quick commerce platforms have surged by 30–40% year-onyear, especially during high-impact windows like festive seasons and major cricket events. This is fuelled by rising user engagement and proven performance outcomes. With more sophisticated ad formats and attribution models now in play, advertisers increasingly view the premium as justified,” added Uday Mohan, COO, Havas Media India & Havas Play.

Scale, Pricing & Soaring Ad Rates

While agencies point to surging demand, market data shows that platforms themselves are firming up monetisation models with steep onboarding thresholds.

As per market estimations, Swiggy Instamart offers tiered onboarding packages ranging from ₹4.5 lakh to ₹10 lakh, adjustable against advertising spends over a three-month period. Zepto reportedly asks new or small brands to commit anywhere between ₹2 lakh and ₹7 lakh per month on ads, depending on the category. Blinkit, on the other hand, charges ₹25,000 per SKU per state as a non-refundable onboarding fee, which is credited to the brand’s ad wallet.

This aggressive push comes against the backdrop of a sector that has grown at breakneck speed. According to CareEdge Analytics’ July 2025 data, India’s quick commerce market was valued at around ₹64,000 crore in FY25, growing at a staggering 142% CAGR during FY22–FY25 on the back of evolving consumer preferences, hyperlocal infrastructure, and a low base.

The momentum is expected to continue with strong double-digit growth over the next few years, as adoption deepens in Tier II & III cities, delivery networks expand, and instant fulfilment becomes mainstream.

At the same time, platforms are pivoting from pure hypergrowth to sustainable profitability—tapping into advertising, subscriptions, private labels and tech-led inventory optimization as key revenue levers. This shift is being enabled by India’s expanding digital backbone: with over 1.12 billion mobile connections and 806 million internet users (a 6.5% YoY rise), the country is projected to cross 900 million internet users by the end of 2025. Rising smartphone penetration in both urban and rural areas, aided by affordable data and policy support, has created one of the world’s largest online consumer pools, with 270 million e-shoppers in 2024, making India the second-largest e-retail market globally.

Unsurprisingly, advertisers are flocking to these platforms because that’s where their consumers are. Even though seller commissions contribute the bulk of revenues (68–74%), ad placements and brand boosts already account for 9–11%. Industry data shows that ad rates on quick commerce apps have climbed by 30–50% in just a year, with premiums doubling during high-impact windows like festivals and cricket tournaments. This steep inflation reflects both rising consumer traffic and the limited nature of in-app inventory, pushing brands to pay top dollar for guaranteed visibility at the point of purchase.

Bain’s ‘How India Shops Online 2025’ report also underscores this momentum: beauty, personal care, and snacking categories are already outpacing overall e-retail growth, and these are the very segments leaning most aggressively into quick commerce ads.

“Ad rates on quick commerce platforms have jumped by nearly 40–50% compared to last year. This spike reflects that premium brands are willing to pay for immediacy and guaranteed visibility, where ad placement directly links to instant purchase behaviour,” said Mandar Lande, founder of Waayu, a zero-commission food delivery app in India.

According to Aditya Aima, Managing Director, Growth Markets; Co-MD, India & MENA, AnyMind Group, ad rates on quick commerce platforms have not only risen but demand has intensified. “The surge is fuelled by three dynamics: sticky consumer behavior with high visit frequency, dense purchase intent compared to social or entertainment platforms, and the scarcity of ad real estate.”

Quick commerce becomes a strategic channel

For brands, quick commerce has moved far beyond being a fulfillment partner. It has become a strategic advertising channel, especially for those in fast-moving and competitive categories like beauty, wellness, snacks, and personal care. The platforms offer not just last-mile delivery but also front-of-shelf visibility in an increasingly cluttered digital environment.

According to Seshu Kumar Tirumala, Chief Buying and Merchandising Officer, bigbasket, “Brands are moving beyond purely search-centric strategies and increasingly adopting immersive display activations with formats like Spotlight Videos, Banners with Add-to-Cart (ATC), targeted banners, and ATC widgets. For established brands, most investments still flow into performance-led formats such as Sponsored/PLA ads, while a portion is reserved for top-funnel initiatives like storytelling, new launches, and high-visibility events. Emerging or smaller brands usually begin with awareness and consideration campaigns before shifting focus toward performance once they’ve built stronger customer connections.” Unlike marketplaces or social media, quick commerce blends data-led targeting, high engagement, and measurable ROI.

Many brands pair Q-comm placements with collab ads on Meta, Google, and Criteo to build visibility while keeping consumers engaged across the funnel. This creates a sharper, closed-loop system where awareness, consideration, and conversion happen almost instantly. “D2C brands have been rapidly scaling up ad spends on quick commerce platforms, up to 40–50% year-on-year, with a significant share during the festive season. Among the key reasons are fast-growing adoption of Qcomm by consumers and better ROI than marketplaces,” said Shrikant Shenoy, AVP at Lodestar UM.

What sets this instant delivery model apart is its ability to compress the purchase journey. Marketplaces drive comparisons, and social platforms spark discovery, but Q-comm taps into impulse buying with SKU-level attribution.

“The quick delivery model encourages impulse purchases and immediate gratification shopping, which is particularly valuable for D2C brands. Qcomm platforms have lower competition density, and ad formats are more native and less cluttered than traditional e-commerce,” said Devangshu Dutta, founder of Third Eyesight.

“When someone opens Blinkit or Zepto, they’re usually in active purchase mode, not just browsing. For consumables, personal care, or lifestyle products, this is the sweet spot of marketing,” Dutta noted.

“Ad rates on quick commerce have gone up by more than 20% in the last year. If you want a prime slot, say a homepage banner in a big city, you might even be paying 50% more than last year. Because every brand wants it. When a Blinkit or Swiggy placement can move your product in minutes, not weeks, those ads aren’t just distribution, they are discovery,” said Mohit Singh, Head of Product at Zippee, a quick commerce logistics platform.

Meanwhile, pricing pressures are only going up. Ratnakar Bharti, VP, Media, Mudramax said, “Quick commerce isn’t just ‘fast delivery’ anymore, it has become high-intent retail media sitting right next to the ‘add to cart’ button, with sales that can be measured in real time. Quick commerce platforms say their ads business grew 5X in a year to about $200M ARR. At that kind of scale, inventory quality improves, targeting gets sharper, and the medium starts looking like the next big retail media play.”

“In a nutshell, expect meaningfully higher prices in peak weeks — often up to 2x — and a higher year-round floor price due to steeper minimums and fees. The trade-off is harder proof of sales at the exact SKU, which is why demand and prices are rising,” Bharti added.

“Brands pay a premium for Q-Comm because it drives sales at the point of purchase. What began as experimental spends has now become a steady line item in media plans, thanks to strong ROI and proven results,” added Jatin Kapoor, MD, AdsFlourish.

Beauty, beverages & snacking lead the charge

Notably, not all categories are leaning on quick commerce equally. Industry executives point out that beauty & personal care, beverages, snacking, and wellness are the biggest spenders, given their high repeatability, impulse-driven nature, and urban skew.

Beauty and personal care brands, for instance, are using Q-comm not just to drive trial packs and quick replenishment, but also to run festival-led campaigns targeting affluent millennials. Similarly, beverages and packaged snacks are thriving on the “in-the-moment” consumption occasions that these apps uniquely enable.

“The biggest spenders are beverages, beauty, packaged foods, and wellness. Those categories thrive on impulse and repeat consumption, which is exactly what quick commerce delivers best,” Singh added. As per many industry experts, wellness and lifestyle brands, too, are seeing outsized returns. From daily supplements to discreet personal care items, quick commerce is proving to be a low-friction purchase environment with high conversion rates.

“Quick commerce platforms have lower competition density, and ad formats are more native and less cluttered than traditional e-commerce,” explained Dutta.

Media buyers also note that Q-comm platforms are evolving fast, offering more contextual in-app placements and data-driven targeting. This is creating a level playing field for challenger brands that lack legacy shelf space in offline retail.

“Quick commerce advertising is inherently contextual. A beverage or snack brand running an IPL campaign is literally tapping into the consumer’s 15-minute window of intent, it’s that instant,” added Mohan.

With ad rates on quick commerce platforms climbing 30–50% year-on-year, it’s clear the medium is shifting from experimental budgets to a core retail media channel. However, with competition heating up, festive weeks commanding 2X pricing, and minimum spends rising, the question is: how long before quick commerce ads start resembling the crowded, high-cost landscape of traditional e-commerce marketplaces?

(Published in Exchange4Media)

admin

August 6, 2025

Naini Thaker, Forbes India

Aug 06, 2025

It’s a known fact that of the thousands of startups founded each year, only a small fraction survive—and even fewer scale to become unicorns. Rarer still are those unicorns which, after reaching dizzying heights, come crashing down. The Good Glamm Group is one such cautionary tale.

Once celebrated as a unicorn that cracked the code on content-to-commerce, the company’s meteoric rise was matched only by the speed of its unravelling. At the heart of its downfall lies a critical misstep: The relentless pursuit of growth through acquisitions and brand launches, even as cracks in its house-of-brands model began to show. Instead of pausing to consolidate and build sustainably, Good Glamm doubled down—prioritising valuation over viability.

That strategy came to a head on July 23 when founder and CEO Darpan Sanghvi announced the dissolution of the group’s house-of-brands structure. In a LinkedIn post, Sanghvi confirmed that lenders would now oversee the sale of individual brands, effectively ending the company’s vision of building a digital-first FMCG conglomerate.

Despite raising $30 million in 2024 and undergoing multiple rounds of restructuring, the group failed to integrate its acquisitions or generate sustainable profitability. With key investors such as Accel and Bessemer Venture Partners exiting the board and leadership turnover accelerating, the company’s ambitious empire—built on rapid expansion and aggressive brand aggregation—has now been reduced to a lender-led breakup.

In the aftermath of the announcement, Sanghvi offered a candid reflection on what went wrong. “In hindsight, it wasn’t one decision, one market force, or one acquisition. It was three levers we pulled, which together, turned Momentum into a Trap,” he wrote in a LinkedIn post. According to Sanghvi, the group’s downfall stemmed from doing “too much, too fast and too big”.

He elaborated: “At first, Momentum feels like your greatest ally. Every headline, every funding round, every big launch is a shot of adrenaline. And you start believing you can do more and more and more. But momentum has a dark side. If you stop steering and go in a hundred different directions, it doesn’t just carry you forward, it drags you faster and faster until you can’t breathe.”

Where The Model Broke?

In October 2017, Sanghvi launched direct-to-consumer (DTC) beauty brand MyGlamm. Most brands at the time were big on selling on marketplaces such as Amazon or Nykaa. However, Sanghvi believed, “We wanted to be truly DTC and not just digitally enabled. We believed that to own the customer, the transaction needs to happen on our own platform.”

But the biggest challenge with being a DTC brand is its customer acquisition cost (CAC). Towards the end of 2019, the company was spending about $15 (over ₹1,000) to acquire a customer to transact on their website. “Around the same time, our revenue run rate was ₹100 crore. We were spending about $0.5 million to acquire 30,000 customers a month. That’s when we realised it was time to solve the CAC problem,” Sanghvi told Forbes India in 2022. In an attempt to find a solution, Sanghvi turned to the content-to-commerce model.

And then, started the acquisition spree. According to Sanghvi, with a single brand in a single category one can’t build scale. He told Forbes India, “The most you can scale it is ₹1,000 crore, if you want a company that’s doing ₹8,000 or ₹10,000 crore in revenue, it has to be multiple brands across multiple categories.” In hindsight, this perspective might be debatable.

As Devangshu Dutta, founder of consultancy Third Eyesight, points out, the “house of brands” model is essentially a modern-day consumer-facing business conglomerate—and its success hinges on multiple factors working in harmony. While there are examples globally and in India of such models thriving, both privately and publicly, the reality is far more nuanced. “Brands take time to grow, and organisations take time to mature,” Dutta notes, emphasising that rapid aggregation of founder-led businesses under a single ownership umbrella is no guarantee of success.

In recent years, Dutta feels the influx of capital into early-stage startups and copycat models—often seen as lower risk due to their success in other geographies—has shortened business lifecycles and inflated expectations. The hope is that synergies across the portfolio will unlock outsized value, but that rarely plays out as planned. “It is well-documented that more than 70 percent of mergers and acquisitions fail,” he adds, citing reasons such as weak brand fundamentals, lack of synergy, inadequate capital, limited management bandwidth, and internal misalignment.

In the case of Good Glamm, these fault lines became increasingly visible as the group expanded faster than it could integrate or stabilise.

Scaling Without Steering

In FY21, the company had losses of ₹43.63 crore, which rose to ₹362.5 crore in FY22 and went up to ₹917 crore in FY23. Despite the mounting losses, Good Glamm marked its entry into the US market, in a joint venture with tennis player Serena Williams to launch a new brand—Wyn Beauty by Serena Williams. The launch was in partnership with US-based beauty retailer Ulta Beauty.

For its international expansion, it invested close to ₹250 crore over three years. “We anticipate that the international business will account for 25 to 35 percent of our total group revenues by the end of next year. This strategic focus on international expansion is pivotal as we prepare for our IPO in October 2025,” he told Forbes India in April 2024.

Clearly, things didn’t pan out as expected. As Sanghvi rightly points out, it was indeed a momentum trap. “You tell yourself you’ll fix the leaks after the next milestone. But the milestones keep coming, and so do the leaks. Soon, you’re running from fire to fire, never realising that the whole building is getting hotter. And somewhere along the way, you lose the stillness to think,” he writes on his LinkedIn post.

Dutta feels that a strong balance sheet is the most fundamental requirement, “to provide growth-funding for the acquisitions or for allowing the time needed for the acquisitions to mature into self-sustaining businesses over years. In the case of VC-funded businesses, the pressure to scale in a short time can go against what may be best for the business or for its individual brands”.

The Good Glamm Group’s fall is a reminder that scale alone doesn’t build resilience. Its story reflects the risks of expanding faster than a business can integrate, and of prioritising valuation over value. The house-of-brands model can work—but only when backed by strategic clarity, operational discipline, and patience. This is less a warning and more a reminder for founders: Scale is not success, and speed is not strategy.

(Published in Forbes India)

admin

August 24, 2024

Writankar Mukherjee & Navneeta Nandan, Economic Times

24 August 2024

Quick-commerce operators such as Blinkit, Swiggy Instamart and Zepto are aggressively trying to lure away consumers from large ecommerce platforms like Amazon and Flipkart by matching their prices across groceries and fast-selling general merchandise, triggering a price war in the home delivery space.

This is a departure from the earlier pricing strategy of quick-commerce players who typically charged 10-15% premium over average ecommerce marketplace prices for instant deliveries, industry executives said.

The strategy now is to win consumers from large ecommerce at a time when urban shoppers increasingly prefer faster and scheduled deliveries, they said.

An ET study of prices of 30 commonly used products in daily necessities, discretionary groceries and other categories, including electronics and toys, in both ecommerce and quick-commerce platforms reveal the pricing disparity has been bridged. “The pricing premium which quick commerce used to charge for instant deliveries is gone with these platforms now joining a race with large ecommerce to offer competitive pricing to shift consumer loyalties,” said B Krishna Rao, senior category head at biscuits major Parle Products.

It seems to be working. Quick commerce is the fastest growing channel for all leading fast-moving consumer goods companies, accounting for 30-40% of their total online retail sales, according to company disclosures in earning calls.

These platforms are also expanding their basket with larger FMCG packs to cater to monthly shopping needs but also non-groceries such as electronic products, home improvement, kitchen appliances, basic apparel, shoes and toys amongst others.

“Consumers have all the apps on their phones and all they want is quick deliveries at the best price,” said Rao of Parle Products.

The increasing competition is putting pressure on ecommerce majors to reduce delivery time.

‘Market acquisition cost’

Flipkart is even eyeing a quick-commerce foray by piloting a 10-minute delivery service called Minutes in some parts of Bengaluru.

Jayen Mehta, managing director of Gujarat Cooperative Milk Marketing Federation that owns the Amul brand, said now that people are buying regularly from quick commerce with an increase in their assortment, legacy ecommerce platforms like Big Basket and Amazon are trying to deliver faster and same day, which has increased competition pressure.

“At the end of the day, consumers compare across channels before buying. So, pricing equality has become important,” Mehta said. “But then, quick commerce has a delivery charge if the order is below a certain value,” he added.

But does their business model allow quick-commerce players to wage a sustained price war against ecommerce platforms?

Quick commerce model requires multiple dark stores to be set up in close vicinity in each market, while ecommerce players mostly make deliveries from centralised warehouses.

But then, quick commerce platforms right now are at a phase where ecommerce was 7-8 years back, said Devangshu Dutta, CEO of consulting firm Third Eyesight.

“Price matching by quick commerce is to acquire market share and is part of market acquisition cost even when it might not be profitable at a per unit transaction level,” he told ET. “They may have to sacrifice margins in the short term to get customers shopping more frequently.”

Blinkit chief executive Albinder Singh Dhindsa earlier this month said the advent of quick commerce has made people want things faster than they would have otherwise got from ecommerce.

“This has led to a direct share shift of a number of non-grocery use cases to quick commerce where customers were primarily reliant on ecommerce for buying these products,” he said in the Zomato-owned quick-commerce platform’s June quarter earnings release.

Dhindsa said quick-commerce platforms are gaining sales by incremental growth in consumption, shift in purchases from next day ecommerce deliveries and mid-premium retail chains.

Citing an example, he claimed the demand Blinkit has generated for online-first oral care brand Perfora is a testament that such brands’ growth and adoption on quick commerce is much faster than on ecommerce.

(Published in Economic Times)

admin

October 13, 2023

Anand JC, Economic Times

13 October 2023

Once the butt of jokes in Dalal Street circles, 113-year-old ITC has turned a new leaf in recent years, as its strategy to derive higher revenue from its consumer business is bearing fruit, bit by bit.

Registered in Calcutta as the Imperial Tobacco Company, the FMCG major has always relied on its cigarettes and leaf tobacco business for a major chunk of its revenues. ITC’s true diversification move might have begun with the launch of its hotel in Chennai in 1975, including a failed attempt at the financial services business, but it wasn’t until August 2001 that the tale of the FMCG behemoth came to be.

Having relied on its cigarette business since 1910, ITC has increasingly sought to earn more from its ‘cleaner’ consumer goods products. In a 2018 interview, CEO Sanjiv Puri admitted that while the journey to diversify the company started a long time ago, it only got traction around 2008. Under Puri’s first term as the ITC chairman, the company embarked on the ‘ITC Next’ strategy. The first decade was focused on preparing the company for the transition, he said. ITC now can innovate products, create brands and allow “pro-neurs” or professional entrepreneurs to build businesses in FMCG.

The plan has worked

ITC, a darling of dividend-led investing lovers, has always been a long-term growth story in the making. Nearly two decades after entering the food business, the company holds a leadership position across categories.

As per the company’s latest annual report, it holds the leadership spot in the branded Atta market through Aashirvaad, cream biscuits segment via Sunfeast, bridges segment of snack foods via Bingo!, notebooks via Classmate and dhoop segment via Mangaldeep. Its Yippee noodles trails Nestle’s Maggi, as the latter continues to lead in a highly consolidated market. However, Yippee has managed to gobble up Maggi’s share at an enviable pace. Capturing these positions, this quickly is no easy feat either.

One of the things that worked for ITC is their understanding of the distribution of products, stemming from their strength in the tobacco business. ITC started exploring aggressively diversifying away from the tobacco business around the 90s, says Devangshu Dutta, head of retail consultancy Third Eyesight.

ITC’s foray into the food business was supported by its presence in the hotel business. “Some of the marquee products that used to be served in their hotel restaurants, packaged dal and so on, they packaged and sold but it was not a humungous success. It was marginal at best.”

“But they started understanding the distribution aspect because those were sold through traditional distribution channels,” Dutta says.

ITC also put in a lot of financial muscle behind the brand building, given no dearth of resources, Dutta says. This helped them grow rapidly in product categories in which they didn’t have a presence earlier on.

“Starting from scratch, particularly on the foods side, ITC has been one of the most successful companies in the last 15-20 years. Their overall revenue this year has been roughly Rs 19,000 crore, out of which Rs 15,000-16,000 is purely from foods segment,” Amnish Aggarwal, Head of Research, Prabhudas Lilladher told ET Online.

“For a company which started this business, maybe, say, two decades back, this is a very big achievement,” he says.

Unlike its commanding position in its cigarette business, ITC’s ‘other-FMCG’ ambitions faced stiff competition from local and national companies in categories including soaps, shampoos, atta, snacks, biscuits, noodles and confectioneries.

Supporting ITC’s ‘other-FMCG’ ambitions is its core competency, the cigarette business. ITC’s consumer business’ growth has weathered storms, in part, thanks to the cash flows generated by its cigarette business which has helped it create stronger brands, an essential part of any consumer-centric business. Through its cigarette business, ITC also gets unparalleled access to a network of brick-and-mortar stores that have a diverse presence across India.

Also complimenting its growth is ITC’s agri-business, a segment which has also grown in strength over the years. From 10 per cent in FY14, the agri-business in FY23 contributed around 24 per cent to the company’s revenue from operations, as per ET Online’s calculations. ITC over the years has invested in building a competitive agri-commodity sourcing expertise. Some of these structural advantages have facilitated the company’s sourcing of agri raw materials for ITC’s branded packaged foods businesses, be it towards its atta, dairy or spices.

Like its peers, ITC too has given a fair deal of importance to its digital push, with more and more companies launching their D2C platforms. These platforms help customers buy products directly from the company website without the hassle of dealing with channel partners, and at the same time, the companies get their hands on first-party data. Such access can help the company market its offerings better. ITC, like some of its other peers, has also been investing in start-ups to diversify its product portfolio. It recently invested in Yoga Bar and Mother Sparsh.

The numbers behind ITC’s consumer business behemoth

Built to engage in the tobacco business, ITC got into cigarette packaging nearly 100 years ago. Another intent in recent decades has been to focus more on the non-cigarette business.

Puri saw it coming.

Upon being asked about the FMCG business overtaking cigarettes, Puri had said “We do not give guidance. But it will certainly happen because the other businesses are growing faster.”

After contributing nearly 62 per cent to the overall revenue in FY14, the cigarettes business in FY23 contributed only around 37 per cent.

ET Online calculations show that the other-FMCG business contributed 17 per cent to the overall revenue in FY14, which grew to 25 per cent in FY23.

Data confirms the claims made in the above segment. ITC’s non-cigarettes businesses have grown over 31-fold and currently form over two-thirds of its net segmental revenues. The company’s other-FMCG business didn’t start turning consistent profits up until FY14. Since then, it has gone from strength to strength.

ITC’s Other FMCG segment (the second largest contributor to sales) is also witnessing strong earnings and growth momentum, unlike most consumer staples peers.

The segment clocked a revenue of 19 per cent YoY while Nestle and Britannia saw 21 and 11 per cent growth each. FMCG EBITDA performance was even better, with the margin expanding by 430 bps YoY to 13.3 per cent & EBITDA growing 2.1x YoY.

Laughing stock no more

For years, the cigarette business has funded the growth of ITC’s other businesses like non-cigarette FMCG products, sometimes to the ire of shareholders who weren’t happy with the slow growth in financials and scrip value.

A slower growth in scrip value meant that for years ITC was also the laughing stock among social media circles. The stock often remained elusive during market rallies in the previous decade, offering poor returns in comparison to FMCG peers. Between 2014 and July 2022, ITC rose with dividends rose 53 per cent while Nifty50 rose 200 per cent, as per moneydhan.com, a SEBI RIA. ITC’s shares trailed the Sensex for five out of eight years through 2020.

“In the last ten years, HUL has done far, far better than ITC. And if you look at other companies in the same universe, say Dabur, it has also given superior performance. ITC has actually underperformed many of the large consumer names,” Aggarwal said.

But fast forward to 2023, not only is it among the best performers within the benchmark index, ITC has even trumped it. While Nifty50 has gained around 17 per cent in the last year, ITC has grown nearly 40 per cent. The ITC scrip in July crossed a market capitalization of Rs 6 lakh crore, beating HUL to become the largest FMCG company.

Sin stock

Prompting a move away to other segments is the nature of the cigarettes business. Tobacco is toxic, and investors are increasingly recognising it as such. Sin stocks are shares of companies engaged in a business or industry that is considered unethical or immoral.

While Environment, Social, and Governance (ESG) investing may be at a nascent stage in India, it is a serious parameter for global investors. Asia’s largest cigarette maker ITC cannot ignore it.

“The company sustained its ‘AA’ rating by MSCI-ESG –the highest amongst global tobacco companies– and was also included in the Dow Jones Sustainability Emerging Markets Index,” Puri noted in the company’s 2022 sustainability report.

Cigarettes, a bitter but essential overhang

For all the accolades for its gains in its other-FMCG business, ITC is nowhere close to ending its love for cigarettes, not that we are claiming it wants to. The Gold Flake-maker currently controls nearly 80% of the cigarette market.

The numbers in recent years suggest that the segment is flourishing more than ever before.

On an annualized basis, the return on depreciated cigarette assets is approaching a staggering 240%, three times the level two decades ago, as per a Bloomberg report. The entire legal cigarette industry was bleeding in the recent past due to punitive and discriminatory taxation on cigarettes. Taxes on cigarettes in India are multiple times higher than in developed countries viz. 17x of USA, 10x of Japan, 7x of Germany and so on, data shows.

But, companies are now recovering due to stable taxation. ITC’s three four-year cigarette sales CAGR are at their best levels since FY15 despite the company not taking material price increases over the last 13-14 months, as per a Motilal Oswal report.

ITC, which accounts for three out of every four cigarettes sold in the white market in the country, is currently seeing its best growth levels in over a decade, and is far superior to the flattish volumes of the past ten and twenty years.

(Published in Economic Times)