admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

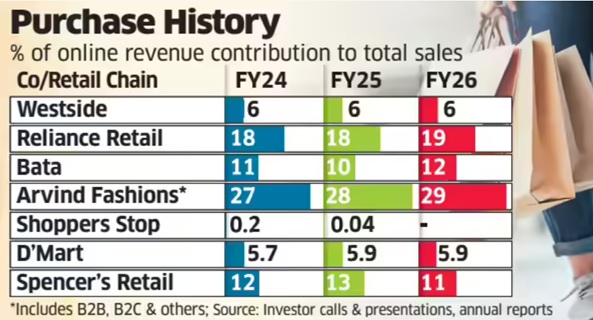

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

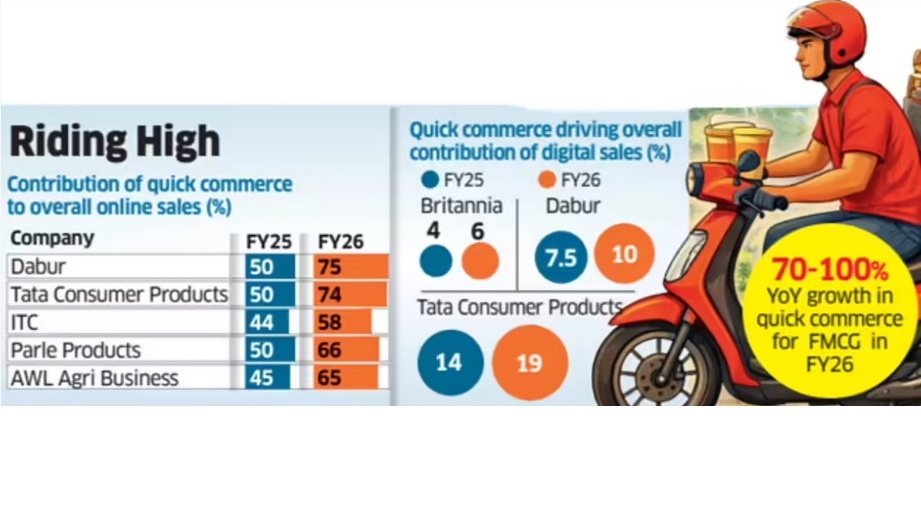

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

February 6, 2026

Anees Hussain and Kartikay Kashyap, Financial Express / Brand Wagon

6 February 2026

Swiggy Instamart’s Noice has consciously rejected every aesthetic that defines platform house brands. Its visual identity doesn’t sport minimalist colours or whites, no clean sans-serif, no ‘discount alternative’ signalling. Instead it uses Indian truck art inspired design with neon colours and bold text. That design architecture also personifies Swiggy’s big gamble.

Noice isn’t just a private label chasing margin expansion. It’s a differentiation play by a company that’s losing ground in a war in which being faster and cheaper is no longer enough. Early data suggests that Noice is finding traction. In namkeens, sweets, and western snacks, Noice holds a 4.4% market share on Instamart as of December 2025, competing against category leaders like Haldiram’s (16.7%) and Lay’s (9%), according to 1digitalstack.ai. This segment generated between ₹41-60 crore per month in the September-December period, with Noice’s share translating to roughly ₹1.8-2.6 crore a month. In beverages (fruit juice, mocktails, energy drinks, tea, coffee and soda), Noice more than doubled its platform sales share -from 2.6% in July to 5.8% by December. The brand now ranks 12th overall, ahead of Coolberg and gaining on established players. Category leader Real’s share fell from 12.3% to 9.5% over the same period. The beverage category generated ₹13,920.3 crore per month during July-December, with Noice’s December share of 5.8% representing about ₹88 lakh in monthly sales. Modest but shows velocity.

Bhushan Kadam, senior vice president, White Rivers Media, says the platform enjoys certain struc-tural advantages: “Swiggy has a credible shot at building Noice into a meaningful private label play because quick commerce (q-commerce) in India is still in a high-growth phase and Swiggy already has the scale, infrastructure, and customer base to drive repeat consumption.”

Swiggy’s own performance with private labels on q-commerce has been positive. Its Supreme Harvest brand, spanning pulses, oils, spices, and dry fruits has achieved just over 20% platform penetration, accord-ing to 1digitalstack.ai. The broader private label landscape offers both encouragement and caution. Tata Digital-owned BigBasket (BB) remains the clear winner, with private labels accounting for nearly 33% of its total revenue. But BB has a crucial advantage: Sourcing infrastructure inherited from Tata’s retail operations that provides scale – and supply chain depth that pure-play q-commerce platforms are still only building.

Noice isn’t Swiggy’s first experiment with owned brands. In May 2025, the company sold its cloud kitchen brands – The Bowl Company, Homely, Soul Rasa, Istah – to Kouzina Food Tech after years of trying to operate its own restaurants. Those brands required Swiggy to manage kitchens, hire chefs, and compete with thousands of independent restaurants. Unit economics never worked out.

Noice represents a fundamentally different model. Instead of large manufacturers optimised for extended shelf lives, Noice works with regional food makers producing in small batches. Launched mid last year with 200 SKUs across 40 manufacturers, it has expanded to over 350 products from 60 makers across 20-plus categories. Packaged versions of items like paneer and rasgullas from the mithai shop fail to resonate with consumers because they might use preservatives and taste artificial. Other offerings include biscuits made with butter instead of margarine, Punjabi lassi with seven-day shelf life delivered everyday like milk.

“Noice seems to be purpose-built for q-commerce: Impulse driven categories, low switching costs and algorithmic discovery. That alone fixes the biggest flaw of Swiggy’s past private label experiment,” says Ankur Sharma, cofounder, Brandshark. It is trying to do things for which customers come back to the platform – “products that are not there on any other platform”, adds Satish Meena, advisor, Datum Intelligence.

Uphill climb

Unlike other private label brands owned by Blinkit and Zepto who largely deal in non-perishable products, Swiggy-owned-Noice currently has a 50-50 split between perishable and non-perishable categories. Perishable products fetch 25-45% margins compared to 15-25% on non-perishable private labels and just 10-15% on third-party FMCG brands. Short shelf lives that enable freshness also mean higher wastage risk if demand forecasting fails. The solution Swiggy is testing hinges on shifting the capex risk entirely to small manufacturers while using its distribution scale as a leverage.

That apart, competition in q-commerce has intensified sharply over the past year. Reliance Retail’s JioMart, Flipkart Minutes, and Amazon Now have entered meaningfully with aggressive pricing. Zepto slashed minimum order values and waived customer fees at ₹149. Swiggy waived platform fees – but only on higher-value baskets at ₹299, essentially ceding low-AOV (average order value) products that drive frequency. In the meantime, market leader Blinkit’s gross order value reached nearly twice that of Instamart’s.

In q-commerce’s brutal pricing war, it is execution that will determine if Noice becomes a genuine differentiator or just another private label. “Proving Noice is not ‘just another’ private label would be the biggest challenge for the company,” says Devangshu Dutta,, founder and CEO, Third Eyesight.

(Published in Financial Express/Brand Wagon)

admin

December 3, 2025

Pooja Yadav, Exchange4Media

3 December 2025

Over the last few months, India’s e‑commerce and quick‑commerce ecosystem has undergone a wave of structural regulatory and tax reforms. Be it the Goods and Services Tax Council (GST Council) formally bringing “local delivery services” under the tax net with an 18% levy, or the newly implemented labour and social-security reforms expanding obligations for gig workers on aggregator platforms like Swiggy and Zomato, the cost and compliance landscape for delivery and fulfilment is shifting significantly.

The latest GST clarification, delivery fees, packaging charges, and logistics surcharges are now creating a ripple effect across pricing, platform margins, and seller compliance requirements.

The past few months have already shown concrete signals that platforms are revising their incentives, delivery promises, and fee structures. Following the GST clarification, major food‑delivery players have raised their platform fees, for instance, Zomato reportedly increased its per‑order fee from ₹10 to ₹12 (pre‑GST), while Swiggy also raised fees in select markets. Some quick‑commerce arms are also reworking free‑delivery thresholds or fee waiver conditions. Swiggy Instamart also recently updated its free‑delivery threshold to orders above ₹299, with handling and surge fees applying below that level, per reports.

Meanwhile, some platforms seem to be signalling a de‑emphasis on “ultra‑fast for every order” as universally viable; free or fast delivery now appears increasingly tied to higher order values or subscription/membership perks.

It looks like these pressures are forcing platforms to reconsider long-standing quick-commerce levers such as ultra-fast delivery, first-order free offers, zero delivery fees, and flash discounts — which have historically driven customer acquisition and retention.

While Zomato did not comment directly, it referred to the Code on Social Security, 2020 (CoSS), noting that the platform is prepared for gig-worker obligations and does not expect the rules to negatively impact long-term business sustainability.

According to Kapil Sharma of Amazon Ads, “The e‑commerce landscape will continue to evolve, but some fundamentals remain constant such as delivering value to consumers and providing advertisers with meaningful ways to engage. Our full-funnel ad solutions allow brands to focus on objectives such as new product launches, brand building, or promoting larger pack sizes, ensuring campaigns remain relevant and effective even as the ecosystem adapts to changing costs and regulations.”

e4m reached out to Swiggy, Meesho, Zepto and BigBasket for comments, but did not receive responses until the time of publishing.

Several experts told e4m that the economic model of quick commerce, built on heavily subsidised delivery and small-ticket frequent orders, is under pressure. Platforms will need to find sustainable levers to retain customers without eroding margins. The industry has started to see a strategic recalibration where speed is increasingly becoming a hygiene factor rather than a differentiator, free delivery is becoming conditional, and platforms are nudging consumers toward larger baskets, subscription models, curated bundles, and scheduled deliveries. Brands, in turn, are also shifting focus from mass discounting to premiumisation, value-led messaging, and precise cohort-based targeting.

Will Free Delivery Become Rare?

With the new social‑security obligations for gig workers under India’s labour reforms, and the added cost burden of delivery services now subject to GST, the economic logic underlying “free delivery” as a marketing lever is coming under stress. Chetan Asher, Founder and CEO of Tonic Worldwide, echoes this view, noting that quick-commerce platforms previously operated on thin contribution margins and heavily subsidised small-ticket, frequent orders. With rising delivery costs and mandatory social-security contributions, universal free delivery is becoming increasingly unsustainable.

Industry analysts point out that the new social-security mandates and GST on delivery fees have lifted per-order costs noticeably. Most quick-commerce platforms already operate at low single-digit contribution levels, making blanket “free delivery” hard to justify. It may continue, but only as a conditional incentive tied to higher basket values, subscription memberships, or flexible delivery slots, rather than as a universal subsidy.

Shradha Agarwal, Co- Founder & Global CEO, Grapes Worldwide, added from an advertising standpoint, “It’s already happened, brands like Zomato, Swiggy, Amazon and Flipkart, who know we are going to buy from them, have shifted from ‘buy now’ tactics to ‘stay with me’ strategies. Those days are gone when platforms were giving blanket discounts, now brands are the ones tightening their offers.” Citing an example she mentioned how offline pricing is ₹235, but online it is sold at ₹185, with online adding to top-line rather than bottom-line.

On promo hooks like ‘₹0 delivery’, ‘first-order free’ or ’10-minute delivery’, Agarwal said, “As labour codes, compliance costs, and social-security contributions kick in, platforms will have less room to burn cash on promos that don’t create sustainable value. Consumers care more about convenience than freebies.”

On ad spend shifts, she noted, “Offer-driven campaigns will weaken, while value-driven storytelling will rise. ATL and influencer campaigns will strengthen, and performance marketing will become more strategic. Retail media will become non-negotiable.”

From a brand perspective, Asher pointed out that quick-commerce spends are increasingly evaluated against contribution margin rather than sheer GMV growth. Discounts and zero-fee offers are losing bite as customer acquisition costs rise. First-party data, replenishment journeys, and sharper cohort-based offers are gaining importance, ensuring that incentives remain ROI-focussed rather than mass-oriented. Similarly, speed claims such as “0 delivery” or “10-minute delivery” are becoming less differentiating in top cities, where most players already deliver within 15–20 minutes. Consumers now respond better to reliable ETAs, fair fee structures, and transparent pricing than aggressive speed promises.

Adding her viewpoint, Pooja Dhamdhere, Commerce Lead at Starcom India, said, “Incentives like free delivery or first-order offers are likely to evolve rather than disappear, and platforms will explore strategies such as tiered benefits, curated bundles, or differentiated pricing for specific cohorts.”

According to serial entrepreneur Alok Chawla and Founder at Kiko Live, added that while platforms may continue absorbing delivery costs in the short term, the long-term economics will require charging for ultra-fast or low-value orders. “Once platforms pass the actual delivery costs to consumers, we expect order frequency and small-cart behaviour to change, with many users shifting to larger baskets or neighbourhood retailers offering free delivery,” he noted.

Alternative Consumer-Incentive Models

Devangshu Dutta, founder and chief executive of Third Eyesight, who is an expert in the consumer and modern retail sector, stated, “I think platforms will pass a significant portion of the new 18% GST burden on delivery to end-consumers, either through higher delivery charges or repackaged platform fees. Some of this cost may also be clawed back from restaurant partners and quick-commerce brands via revised commissions, slotting fees or mandatory participation in marketing programmes, especially in categories where the platform has stronger bargaining power. Overall, I expect higher minimum-order thresholds and a tighter margin environment for restaurants and small D2C brands that rely heavily on third-party platforms.”

Analysts highlight strategies such as minimum-order thresholds, where free or lower-fee delivery applies only above a certain cart value, nudging consumers to order larger baskets rather than frequent small-ticket items. Subscription and membership-based models are also gaining prominence, offering benefits like waived or discounted delivery, priority fulfilment, and access to exclusive promotions in exchange for a fixed fee.

Scheduled or batch delivery windows are being used to optimise logistics, reduce cost pressure on ultra-fast last-mile fulfilment, and improve operational efficiency. Meanwhile, curated bundles and value packs, including weekly or monthly combos, allow consumers to plan purchases while enhancing per-unit economics for platforms. These levers also enable brands to maintain margin integrity without over-reliance on short-term discounting.

From a marketing perspective, this shift is prompting agencies and creative-first firms to move toward value-led messaging, premiumisation, and cohort-based targeting. Dhamdhere explained, “Platforms are optimising assortments by surfacing premium SKUs, nudging higher average order values, and using search optimisation to strengthen profitability. Brands are now focusing on aspirational consumers with curated bundles, subscriptions, and value-led propositions, rather than mass discounting. Performance campaigns will continue, but clarity of value and sustainable margin-led offers are becoming key for acquisition and retention.”

2026: Will regulatory pressure force a recalibration?

As 2026 approaches, the combined impact of GST on delivery services and mandatory social-security contributions for gig workers is forcing a fundamental rethink of quick-commerce economics. With blanket discounts, zero delivery fees and ultra-fast delivery no longer viable as mass levers, platforms are shifting toward basket-building, subscriptions, curated bundles and conditional incentives. The growth thesis is evolving from “habit formation at any cost” to protecting contribution margins through reliable ETAs, transparent pricing and premium assortments rather than aggressive subsidies.

Brands are recalibrating alongside this shift. Premiumisation, value-led propositions and sharper cohort-based targeting are taking precedence over broad discounting, and campaigns are increasingly evaluated on ROI, repeat behaviour and lifetime value rather than raw GMV. Tiered memberships, scheduled deliveries and subscription-led conveniences are emerging as key retention tools, while short-form video, influencer ecosystems and retail media help articulate value in a tighter cost environment.

Chawla said platforms will have to move beyond “₹0 delivery”, “first order free” and “10-minute delivery” as core propositions because the delivery cost burn far exceeds margins on small-ticket orders. Many consumers currently place multiple micro-orders a day simply because delivery is free, but once fees come into play, behaviour will likely shift toward clubbing orders or reverting to neighbourhood retailers, who themselves are rapidly digitising through partners like Kiko Live.

In the next phase, he adds, free instant delivery will only be sustainable for larger baskets, whereas scheduled delivery may become the default for free delivery, with paid instant delivery as an optional upgrade. Subscriptions may drive loyalty, but only up to a point, since the heaviest users would consume more deliveries than the subscription fee can realistically subsidise, making it difficult for platforms to make the model profitable.

This points to a clear playbook for 2026. “Free delivery” and mass discounting are expected to fade, giving way to conditional, tier-based formats that reward higher basket values, subscriptions or specific cohorts. Brand platform partnerships will also move toward profitability rather than promotional burn, with campaigns designed to protect margins instead of fuelling discount-led spikes.

Taken together, the signs suggest that 2026 will not mark the end of convenience, but the end of convenience that is subsidised blindly. The real test now is who absorbs this new cost of convenience, platforms, brands, or consumers. And as that battle plays out, another tension is already emerging: whether small and regional advertisers can survive the rising cost of visibility in India’s digital economy.

(published in Exchange4Media)

admin

November 27, 2025

Viveat Susan Pinto, Financial Express

November 27, 2025

Several of the country’s top retailers, malls and brands have kicked off a shopping extravaganza on the occasion of Black Friday, offering steep discounts across product categories.

A Western import, the day which symbolises the beginning of the Christmas shopping season in the US, the UK and Europe, gained popularity in India over the past two years as a crucial sale window after Diwali.

Domestic retailers, say experts, are using this period to exhaust existing inventory at steep discounts as they gear up for the winter season.

This year, discounts are up to 60-80% across fashion, lifestyle, electronics and cosmetics, higher than the 50% seen last year. E-tailers such as Ajio have pushed the pedal even harder, offering as much as 85-90% on denims, jackets and select products during the sale this year.

Bigger Deals, Longer Duration

“Retailers in India are building Black Friday as an important off-season peak. The participation of brands is growing, deals are getting bigger and the sale days are more,” Devangshu Dutta, founder and chief executive of Third Eyesight, a Gurugram-based retail consultancy, said. That is visible from the intense promotional activity this year. What began as a flash sale event a couple of years ago has now extended to a week-long sale period this year, experts said.

Pushpa Bector, senior executive director and business head, DLF Retail, said that brands this year are ready with strong offers, driven in part by GST cuts and a stable economic outlook. “Early trends show healthy interest across categories by consumers. We expect a strong double-digit uplift over the Black Friday period, setting us up for a strong close to the year,” she said.

Retailer Strategies

While Black Friday typically falls on the last Friday of November, some retailers such as Flipkart, Croma, Vijay Sales, Nykaa and Tata Cliq have kicked off their Black Friday sales last week itself to build on the excitement. For electronic retailers, said Nilesh Gupta, director, Vijay Sales, Black Friday will extend into Cyber Monday next week (falling on December 1), making it even more relevant for them to focus on the occasion.

“We’ve been building Black Friday as a retail property in the last few of years as it fills the post-Diwali void quite well. Black Friday also extends well into Cyber Monday which comes immediately after. While we started with a few categories in the initial years, we now have offers across all our segments. Discounts are up to 45-50% this year in line with last year,” he said.

Rival Croma is also offering up to 50% discount on products this year, executives said.

“Black Friday has become one of India’s most anticipated shopping moments. At Croma, we are focused on delivering value across categories with steal deals, bundled savings, and limited-time offers,” Croma’s CEO & MD Shibashish Roy said.

Croma will also introduce a special late-night shopping window on November 28 at select stores across India. For two hours—from 10 pm to 11:59 pm —these stores will remain open with exclusive additional discounts on some of the season’s most in-demand products.

Nishank Joshi, chief marketing officer, Nexus Select Malls, said it is elevating the Black Friday experience with bigger assured gifts, giveaways and reward points if consumers upload their bills on their Nexus One apps.

Mayank Lalpuria, director, marketing (north, central & west) at Phoenix Mills, which operates Phoenix malls, said that it was expecting double-digit year-on-year growth and strong footfalls during the Black Friday period.

Tanu Prasad, CEO – Malls, Oberoi Realty, said that the firm was seeing far more planned purchases towards premium products and a rise in family-oriented outings. “We are anticipating an encouraging response at the (Black Friday) weekend resulting in a strong kick-off to the (December) shopping season,” Prasad said.

Direct-to-consumer brands such as Inc.5 footwear and NEWME said that they have rolled out big deals for Black Friday. “We’re looking at a 30x surge in orders across both offline and online for Black Friday,” NEWME Co-founder & CEO Sumit Jasoria said.

“Our customers look forward to Black Friday, and this year, we’re excited to bring fresh new launches, curated edits, and our widest range yet,” Rajesh Kadam, CEO, Inc.5 Footwear, said.

(Published in Financial Express)