admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

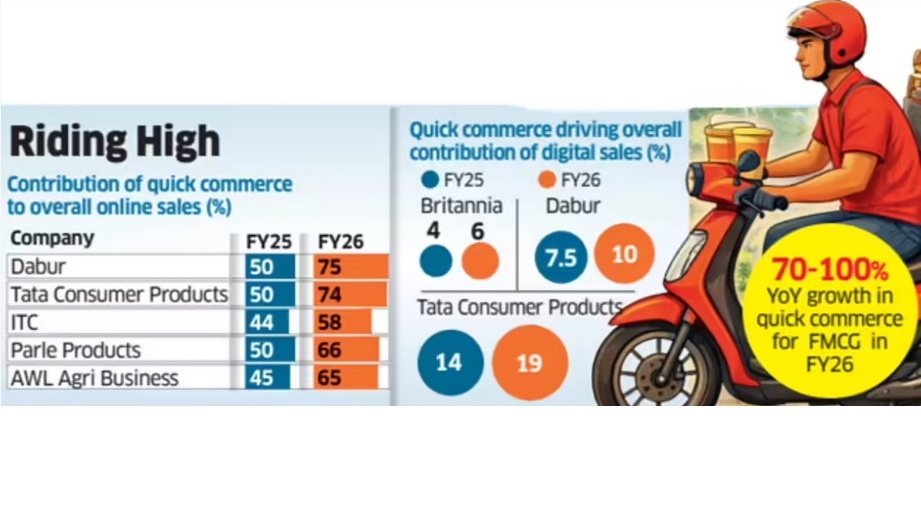

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

February 2, 2026

Sakshi Sadashiv, MINT

Bengaluru, 02 Feb 2026

BRND.ME, a roll-up commerce company, expects to complete its reverse flip (change of headquarters) from Singapore to India by March, clearing a key regulatory hurdle as it prepares to tap Indian public markets with an IPO.

Despite the rise of private labels from quick-commerce giants such as Swiggy Instamart and Zepto, CEO Ananth Narayanan remains confident. He argues that BRND.ME’s core categories—spanning complex, value-added products such as specialized haircare and niche party supplies—possess a level of brand loyalty and complexity that is difficult for generic retail labels to replicate. While private labels are currently displacing national brands in high-frequency, simple categories like dairy and staples, Narayanan believes the company’s core categories remain protected from this encroachment as they drive searches.

Having shifted its strategy from aggressive acquisitions to organic scaling, the company is now doubling down on its four largest brands: MyFitness (peanut butter), Botanic Hearth (haircare), Majestic Pure (aromatherapy), and PartyPropz (celebration supplies).

About 10-15% of BRND.ME’s India business currently comes from quick commerce, a channel the company plans to scale, Narayanan said. The company is the leader in party supplies on quick-commerce platforms, benefiting from impulse-driven demand. “People forget birthdays and anniversaries, so it’s a classic category to build a brand on quick commerce,” he said. The category contributes about ₹200 crore of revenue. The company also leads the peanut butter category through MyFitness, with a 30% market share on all quick commerce platforms and annual revenue of ₹270 crore.

The company’s revenue run rate stands at about $200 million. Male consumers worried about male-pattern baldness now account for about 35% of haircare sales. The company aims for a 10-fold jump in aromatherapy and haircare sales from $6 million to $60 million within four years, led by Majestic Pure and Botanic Hearth.

Drawing on his experience running Myntra, Narayanan said that private labels typically have a ceiling. “Even when we pushed hard on private labels at Myntra, they never went beyond 25-30% of the overall portfolio. That tends to remain the case as the categories we operate in are very hard to displace because we drive searches.”

This dynamic is already visible across several quick-commerce categories. The peanut butter segment is heavily consolidated on Blinkit, with Pintola and MyFitness together accounting for about 73% of sales, according to data from Datum Intelligence. Similar patterns have emerged in other categories. Blinkit’s popcorn segment, for instance, has rapidly consolidated into a duopoly, with 4700BC and Act II controlling 99% of sales.

Private labels muscling in

While Blinkit has consciously avoided launching private-label products on its platform, Swiggy has done so through Noice, and Zepto through Relish and Daily Good. For established brands, these private labels are becoming harder to ignore. Swiggy has scaled Noice aggressively, expanding the portfolio from about 200 to 350 stock keeping units (SKUs) and onboarding more manufacturing partners while moving beyond staples into categories such as beverages and ready-to-cook foods. These products are aimed at delivering significantly higher margins of 35-40%, compared with 10-15% on third-party brands, Mint reported earlier.

Private labels now contribute an estimated 6-8% of quick-commerce sales, up from 1-2% two years ago, according to data from 1digitalstack.ai, though penetration in perishables remains limited because of supply-chain complexity and quality concerns. A broader push into fresh categories could lift private-label share to 10-15%. Noice has already captured 3.4% of wafer sales and 1.9% of biscuit sales on the platform within months of its launch, according to 1digitalstack.ai data. The two categories are dominated by Lay’s and Britannia, which have a market share of about 35% each in their respective segments.

Zepto’s private-label push spans multiple everyday categories, including Relish for meat products, Daily Good for staples, Chyll for ice cubes and juices, and Aaha! for snacks, sweets, cereals and batters.

This growing presence creates a structural ‘trap’ for digital-first brands. Devangshu Dutta, chief executive at Third Eyesight, a consultancy firm, said, “Brands that are overly dependent on a single sales platform remain structurally vulnerable to being replaced by the platform’s own private labels, which are designed to capitalise on product opportunities that already have proven demand.” Platforms, he explained, tend to dominate high-frequency purchases, often undercutting brands on both price and visibility.

Persistently high online customer acquisition costs add to the pressure, particularly if the customer relationship is owned by the platform rather than the brand. “This has been one of the significant friction points for all digital-only brands, and weighs especially heavily on companies that have online-heavy portfolios with multiple brands in play,” Dutta added.

(Published in Mint)