admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

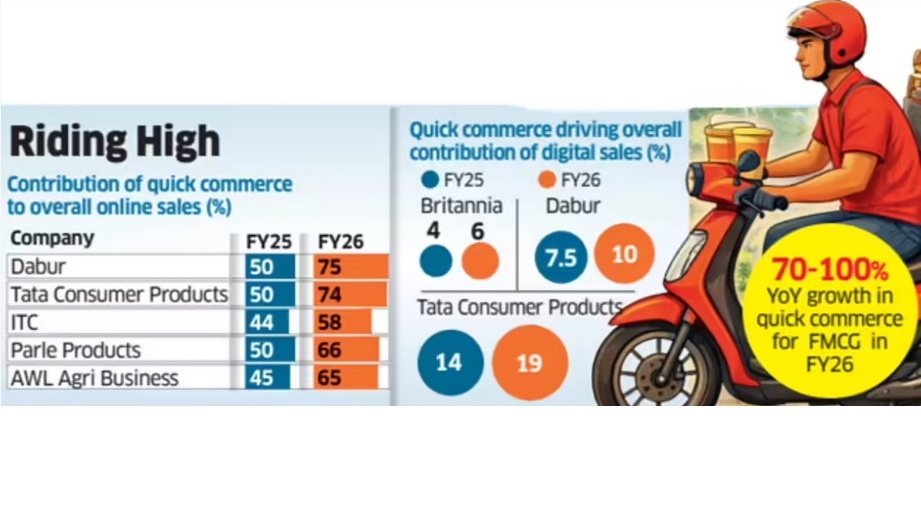

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 2, 2026

Neethi Lisa Rojan, Mint

2 May 2026, Mumbai

Fast-moving consumer goods makers are leaning on a mix of price increases, smaller pack sizes and tighter cost controls to navigate raw-material volatility triggered by the ongoing US-Iran war, while still reporting robust volume growth for the March quarter. The ongoing war blew up end February this year, disrupting global supply chains.

Executives at top firms said calibrated pricing and ‘shrinkflation’ are helping them protect margins. The trend shows staples demand have held up, but also points to a gradual pass-through of higher commodity and packaging costs to consumers as geopolitical disruptions keep input prices elevated.

At Hindustan Unilever Ltd, the strategy is already in motion. The company has implemented calibrated price hikes and adjusted grammage across products. “We are taking calibrated pricing action in the range of 2-5%,” chief financial officer Niranjan Gupta said in a post-earnings briefing on Thursday. “We use a combination of both the put-down price as well as optimizing the fill levels,” said Gupta. The management also noted that its products in the homecare segment such as soaps (Lux, Pears, Dove, etc.) and detergents (Surf Excel, Rin, etc.) will be the first to be affected by price hikes. Interestingly, this happened at a time when HUL’s volumes grew the fastest in 15 quarters.

Companies have anticipated how consumers will behave.

“In times of inflation, income uncertainty, etc. essentials such as packaged foods, biscuits, and household cleaning products tend to see trade-down behaviour rather than outright disappearance of demand,” said Devangshu Dutta, founder of management consultancy, Third Eyesight. “Consumers tend to shift to smaller pack sizes or private labels, rather than abandoning categories altogether,” he adds.

India’s retail inflation rose from 2.75% in January 2026 to a 10-month high of 3.40% in March, driven largely by food prices.

That balance between pricing and demand is playing out across the sector. Nestle S.A., the parent company of the Indian entity said it saw 3.5% organic sales growth during the quarter, with RIG (real internal growth or volume growth) of 1.2% and pricing of 2.3% in the January-March quarter.

“The conflict in the Middle East will have some impact on commodity and distribution costs, and possibly on consumer behavior. But it’s too early to know the full extent of this,” chief executive officer at Nestlé S.A, Philipp Navratil said in the analyst call after the results. Its India unit, Nestlé India, reported its strongest quarterly growth in nearly a decade, led by double-digit volume expansion.

HUL reported a 21% year-on-year rise in consolidated net profit to ₹2,994 crore, while Nestle India saw net profit up 27% at ₹1,110.9 crore. year-on-year to ₹1,110.9 crore in Q4 FY26. HUL has also retained its medium-term guidance for earnings before interest, taxes, depreciation, and amortization (Ebitda) at 22.5%-23.5%.

The resilience in volumes comes even as input costs surge. Prices of crude oil-linked materials, especially packaging, have risen sharply following disruptions around the Strait of Hormuz chokepoint. High-density polyethylene, widely used in packaging, jumped about 42% in March from the previous month.

Multinationals are already bracing for the fallout. Tide and Gillette maker Procter & Gamble, said in its quarterly earnings call that it could take roughly a $1 billion post-tax hit to its fiscal 2027 profit from surging oil prices. Still, not all inputs are moving in tandem. Prices of staples such as wheat, sugar, tea and coffee have remained relatively stable, offering some cushion. Edible oils, however, remain a concern.

Palm oil, a critical input in many FMCG products, is seeing supply shifts, as producers such as Malaysia and Indonesia divert output toward biodiesel. AWL Agribusiness, which sells Fortune oil, said in the quarterly analyst call that edible oils faced a 10% price surge in March, which has already been passed to consumers. The company expects to pass on the rise in packaging material prices also soon. The company posted a 53% jump in consolidated net profit to ₹292 crore in Q4FY26, from ₹190 crore a year earlier.

Experts expect the trend of margin-saving strategies to continue.

“Depending on the product, category and brand, we will see a mix of price hikes, shrinkflation and rationalization of SKUs (stock keeping units), and also a shift from brand-related to tactical advertising and promotional spends to boost short-term demand,” Dutta said.

Elsewhere, companies are acknowledging broad-based inflation but are continuing to push through growth. Bajaj Consumer Care reported near double-digit volume gains even as managing director Naveen Pandey noted that “nearly 100%” of its cost base is under inflation. The company plans further pricing actions alongside cost optimization. Bajaj Consumer Care’s net profit for the March quarter more than doubled to ₹63.6 crore from a year ago.

Beyond the basics

The ripple effects extend beyond staples. Fashion, lifestyle and grocery retailer Trent Ltd flagged uncertainty around supply chains and inflation, warning of potential implications for near-term demand. “Duration and intensity of disruptions in the Middle East, along with its second order effect on supply chain, commodity prices and inflation in general has potential implications for near-term demand,” the company said in its results presentation.

Meanwhile, consumer appliance maker Havells India has initiated price increases after what chairman Anil Rai Gupta described as an unprecedented escalation in input costs. “I’ve not seen this kind of a price escalation in the recent past in the recent memory,” he said in the post results analyst call.“ Calibrated price actions have been initiated, he said. Havells India reported a strong 40% year-on-year increase in net profit to ₹723 crore in the March quarter.

More clarity may emerge as additional earnings roll in. Companies with higher exposure to West Asia, such as Dabur and Emami, are yet to report results and could face greater consolidated impact due to regional disruptions. “Companies such as Dabur and Emami will be more affected at the consolidated level due to issues in the MENA or Middle East and North Africa Region (6-8% revenue salience),” said analysts at Motilal Oswal Financial Services ahead of the earnings season.

For now, inventory buffers are offering temporary relief. Some companies have built raw-material stockpiles lasting up to six months, helping them absorb immediate shocks. “In our international markets, our effect will be in the raw material, practically zero to a couple of points maybe because we are well-stocked not just for this quarter, but the next quarter also. We normally carry six months inventory in international,” said Raj Pal Gandhi, whole-time director at Varun Beverages, the largest bottler of Pepsico in India, in the quarterly analyst call. This has helped the firm tide over the challenges in plastic shortage faced in March.

However, companies will now have to buy raw materials at higher prices, leaving room open for more price hikes.

(Published in MINT)

admin

March 7, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 7 March 2026

While many consumer goods companies are acquiring direct-to-consumer (D2C) startups, Reliance Consumer Products Ltd (RCPL) is pursuing a different playbook. The consumer arm of billionaire Mukesh Ambani’s Reliance Industries has been steadily buying regional legacy brands with strong local recall. By plugging these brands into Reliance’s vast retail and distribution ecosystem, the company hopes to accelerate its ambition of becoming an FMCG powerhouse.

During the December quarter, RCPL overall gross revenue stood at 5,065 crore, up 60% year-on-year, according to an earnings statement from Reliance Industries. India’s FMCG sector remains dominated by established players such as Hindustan Unilever Ltd, which reported revenue of about 64,138 crore in FY25—highlighting the scale of the opportunity Reliance is targeting as it builds its consumer business.

“What Reliance is doing is cobbling together a portfolio of brands that already have some momentum,” said Arvind Singhal, chairman of The Knowledge Company, a Gurgaon-based management consulting firm.

Which regional brands has Reliance acquired?

Over the past few years, RCPL has assembled a portfolio of regional brands across food, beverages and personal care. One of its latest additions is Chennai-based Southern Health Foods Pvt. Ltd, which sells millet-based foods, health mixes and baby nutrition products under the Manna brand. Reliance acquired the company for about 158 crore, marking its entry into the fast-growing millet and nutrition foods segment.

Earlier, RCPL bought a majority stake in Udhaiyam Agro Foods Pvt. Ltd, a Tamil Nadu-based staples brand known for pulses, flours, spices and ready-to-cook mixes. Revenue at Shri Lakshmi Agro Foods Pvt. Ltd, which sells products under the Udhaiyam brand, rose about 5% year-on-year to 668.2 crore in FY24, according to Tracxn data.

Reliance has also acquired Delhi-based Sii, a legacy condiments maker known for jams, sauces and cooking pastes as well as Velvette, the historic personal care label that pioneered shampoo sachets in India in the 1980s.

In beverages, RCPL revived Campa Cola, acquired from the Pure Drinks Group, as a mass-market challenger in the carbonated drinks segment. It has also partnered Hajpuri & Sons to distribute regional drinks such as Sosyo, Kashmira and Ginlim, and tied up with Sri Lanka’s Elephant House to manufacture and distribute its beverages in India.

What do regional brands gain from partnering with Reliance?

Regional brands that partner with or are acquired by Reliance gain access to scale that is often difficult to achieve independently. Many local brands enjoy strong loyalty in their home markets but face constraints such as limited capital, weaker supply chains and restricted distribution networks.

Under the Reliance umbrella, these brands gain access to the group’s nationwide retail and distribution ecosystem, which includes millions of kirana stores as well as large-format retail chains operated by Reliance Retail. This enables them to expand beyond their regional strongholds far faster than they could independently.

Reliance can also improve manufacturing and supply-chain efficiencies, helping these brands scale production, strengthen sourcing and reduce logistics costs. In addition, stronger marketing capabilities and financial backing allow brands to invest in packaging, advertising and product innovation—helping them evolve from local favourites into national brands.

Why is Reliance pursuing this strategy?

For Reliance Consumer Products Ltd, acquiring regional brands offers a faster and potentially less risky way to expand in India’s vast FMCG market. These brands already have loyal customers, established products and existing manufacturing. By plugging them into Reliance Retail’s distribution network, the company can rapidly expand their reach across the country.

The strategy also allows Reliance to quickly build a diverse portfolio across staples, beverages and personal care—strengthening its ability to compete with established FMCG giants such as Hindustan Unilever and ITC.

How are rival FMCG companies expanding instead?

Most traditional FMCG companies are pursuing a different strategy by acquiring or investing in digital-first D2C brands. These startups often operate in fast-growing segments such as premium skincare, clean beauty and health-focused foods, helping established companies tap younger, digitally savvy consumers.

• Hindustan Unilever recently acquired skincare startup Minimalist, a fast-growing digital-first brand known for its ingredient-focused beauty products.

• Dabur India has also entered the space by acquiring premium beauty brand RAS Luxury Skincare through its 500-crore venture capital arm.

• Marico has taken a similar approach, investing in digital-first brands such as Beardo and Just Herbs to strengthen its presence in grooming and natural beauty.

Such deals allow established companies to quickly enter emerging premium categories.

What challenges could Reliance face in scaling regional brands?

Scaling regional brands nationally can be more complex than expanding digital-first startups. Many regional brands are built around specific local tastes, price sensitivities and cultural preferences that may not translate easily across markets. “India is very diverse, and consumer preferences vary significantly across regions,” said Singhal of The Knowledge Company.

Another challenge is that many regional brands lack the infrastructure to scale independently. “For many regional brands, the first real scaling often comes from the acquirer’s distribution rather than from the brand itself,” said Devangshu Dutta, founder of consulting firm Third Eyesight.

In contrast, many D2C brands are designed from the outset for a national or digital audience, making them easier to scale online. However, these startups often rely heavily on marketing spends and online channels, which can make profitability and large-scale expansion challenging.

For RCPL, the key test will be retaining the regional authenticity of these brands while using the nationwide distribution strength of Reliance Retail to expand them beyond their core markets.

(Published in Mint)

admin

January 7, 2026

Writankar Mukherjee & Shabori Das, Economic Times / Brand Equity

7 January 2026

There’s a renewed sparkle in the adage ‘Old is Gold’ at India’s biggest conglomerate Reliance. Banking on Indians’ nostalgia, it is hawking and reviving labels that once defined everyday life, Campa and BPL among them, to set its consumer venture’s cash registers ringing.

What started with sales of Rs. 3,000 crore in FY24, Reliance Industries’ fast-moving consumer goods (FMCG) business quickly accelerated towards Rs. 11,500 crore the following year. With a staggering Rs. 5,400 crore posted in the July to September FY26 quarter alone, the revival story is clearly striking a chord with consumers. But Campa, already the largest contributor to the Reliance Industries’ FMCG business, is only the beginning.

The company is injecting fresh life into acquisition of legacy brands such as Ravalgaon in confectionery and Velvette in personal care. Reliance is applying the same formula to the consumer electronics business, covering televisions, refrigerators and washing machines. Once a staple of Indian households, Kelvinator and BPL are being reintroduced.

Strategy Rings a Bell?

Driving this revival is a strategy Reliance knows well: aggressive pricing that is often 20 to 30% lower than competitors, offering generous trade margins to woo retailers, and a rapid expansion of distribution from its own stores to kiranas and local outlets, alongside local sourcing and an expanding product portfolio.

It’s a playbook that once created waves in the telecom market; this time, however, it comes with a generous dose of nostalgia.

The path ahead though may not be easy. While Campa may have yielded results in a category linked to instant gratification, electronics is a high-ticket, long-term purchase. Marketers are debating whether consumers in their 20s and 30s—spoilt for choice by global brands—would choose a Kelvinator refrigerator, a BPL TV or a Velvette shower gel over LG, Samsung, Dove or Fiama.

Deep Pockets and Retail Muscle

Reliance, experts say, has two advantages— its balance sheet and strong market presence with its own retail stores. “Reliance has the intent to dominate a market in whatever business it enters. Their brands in FMCG and electronics too have a more-than-decent chance of surviving and thriving,” says Devangshu Dutta, founder and chief executive of Third Eyesight, a consultancy in consumer space.

“As long as they have capital and management capability, they may cut their teeth,” he says.

The company is approaching the FMCG and electronics businesses in startup mode, but with deep pockets. As a Reliance executive explains, the strategy is to invest and invest more, gain market share, continue to absorb losses and after achieving scale, drive efficiencies to generate profit.

The path has been carved out. Reliance Consumer Products (RCPL), the FMCG business entity and what started as a unit of Reliance Retail Ventures, is now a direct subsidiary of Reliance Industries. This shift will help the company raise funds independently and eventually launch an initial public offering (IPO), and drive valuation independent of retail. The electronic business may follow suit as it grows in scale.

Reliance did not respond to Brand Equity’s queries.

Electronics: A Tough Play

Industry executives say the electronics foray will not be an easy battle against international brands. Global brands enjoy strong appeal in the Indian market, and companies such as LG, Samsung and Sony have been present for over two decades, cementing their position. Even the newer ones like Haier and Voltas Beko are rapidly gaining market share.

Pulkit Baid, director of the electronics retail chain Great Eastern Retail, says that unlike the cola industry, where two large players (Coca-Cola and PepsiCo) dominate, consumer durables are highly fragmented. “Kelvinator enjoys the brand heritage of an Ambassador car. But we will have to see if the brand is welcomed by Gen Z with the same euphoria as Campa.”

Industry veteran Deba Ghoshal notes that very few legacy brands have been able to withstand the onslaught of new-age brands in consumer electronics. Voltas (from the Tatas) and Godrej are exceptions, he adds.

“Reliance Retail has the strategic foresight to re-establish legacy brands in consumer durables space, instead of chasing a standalone private label business,” adds Ghoshal. “There is a strong opportunity in BPL and Kelvinator, provided they are re-launched with strong value and engaging emotive hooks, and not restricted to being a price warrior. Reliance has the capability; it just needs the right strategy.”

Reliance is readying campaigns for BPL and Kelvinator to connect with the younger consumers. The company is planning to re-launch them beyond Reliance Retail stores—targeting regional retail chains and e-commerce platforms and expanding quickly into smaller towns. With India’s electronics penetration still low—15 to 18% for flat-panel TVs, 40% for refrigerators, 20% for washing machines and less than 10% for air conditioners (ACs)—Reliance has substantial headroom for growth.

Angshuman Bhattacharya, partner and national leader for consumer products and retail at EY India, says Reliance may focus on tier two and three cities. “These markets have been a low priority for the Samsungs and LGs because they want to play in the premium segment where margins are higher. That is where Reliance may expand the market. It requires a lot of capital in terms of inventories and distribution, and Reliance has the ability and potential to do so.”

FMCG: Ball is Rolling

The FMCG push is gaining strong momentum. Reliance plans to double its distribution to three million outlets this fiscal.

Over the next three years, it looks to invest Rs. 40,000 crore to create Asia’s largest integrated food parks and has already invested Rs. 3,000 crore in manufacturing.

Isha Ambani, who spearheads Reliance’s retail and FMCG businesses, drew attention to Campa’s comeback at the company’s AGM in August: “Campa-Cola now holds double-digit market share across many states, breaking a 30-year MNC duopoly of Coca-Cola and PepsiCo. Campa Energy gained two million social media followers in just 90 days.”

Her target is bold: To reach Rs. 1 lakh crore in FMCG revenue within five years and become India’s largest FMCG company with a global presence.

Market watchers say such high ambitions require high investments. Kannan Sitaram, co-founder and partner at venture capital firm Fireside Ventures, said a company like Hindustan Unilever would set aside at least `30-40 crore to launch a brand. “Advertising and marketing alone would take up more than half of that. And when you are re-launching a brand which has not been around for a long while, the spending tends to be 25 to 30% higher in the initial three to four months,” he says.

Yet, analysts believe Reliance is in the consumer brands business for the long term. Bhattacharya says whatever Reliance has learned in this short time is meaningful and serious, something nobody else has managed.

Mover and Shaker

Competitors, including Tata Consumer Products, Dabur and PepsiCo’s largest bottler in India Varun Beverages, have acknowledged the turbulence created by Reliance in the FMCG sector. But the industry hopes low penetration levels will ensure there is room for everyone.

Varun Beverages chairman Ravi Jaipuria did not mince his words in the company’s latest earnings call in October-end: “They (Reliance) have woken all of us up and we are becoming more attentive… it is a very healthy sign for the country because our per capita consumption is so low that in the next five to 10 years, this market may double or triple…there is a huge room, and we see only positives in this.”

The revival of legacy brands and aggressive push into FMCG and consumer electronics indicates that Reliance is preparing for the long haul. In this fight driven by nostalgia, competitive pricing, deep pockets and distribution muscle, the battle for shelf space has just begun.

(Published in Economic Times/Brand Equity)

admin

September 16, 2024

Sesa Sen, NDTV Profit

16 September 2024

As India’s economy grows and digital technologies reshape consumer behavior, the future of kirana stores—the quintessential neighbourhood grocery shops—hangs precariously in the balance.

These soap-to-staple sellers, once impervious to change, now confront an existential threat from quick commerce players like Blinkit, Instamart, Zepto, and from modern retailers such as DMart and Star Bazaar, raising a pivotal question: Can kiranas survive the pressure of change, or will they die a slow death?

The All India Consumer Products Distributors Federation, that represents four lakh packaged goods distributors and stockists, has recently raised alarms, urging Union Minister for Commerce and Industry Piyush Goyal to investigate the unchecked proliferation of quick commerce platforms and its potential ramifications for small traders.

Their concerns are not unfounded. Data suggests that the share of modern retail, including online commerce, which is currently below 10%, is set to cross 30% over the next 3-5 years. Much of this growth will come at the cost of traditional retail.

“Unless the government takes on an activist role to support the smallest of business owners, the shift toward large corporate formats is inevitable,” according to Devangshu Dutta, head of retail consultancy Third Eyesight.

Casualties Of The Boom

Madan Sachdev, a second-generation grocer operating Vandana Stores in eastern Delhi, has thrived in the recent years, adapting to the digital age by taking orders via WhatsApp and employing extra hands for home delivery.

Despite having weathered the storm of competition from giants like Amazon and BigBazaar, he now finds himself disheartened, as his monthly sales have halved to about Rs 30,000, all thanks to quick commerce.

Sachdev is worried about meeting expenses such as rent, his children’s education, and other household bills. He finds himself at a crossroads, uncertain about how to modernise his store or adopt new-age strategies in order to attract customers in an increasingly competitive market.

India’s $600 billion grocery market, a cornerstone for quick commerce, is largely dominated by more than 13 million local mom-and-pop stores.

Retailers like Sachdev are also seeing a steep decline in their profit margins from FMCG companies, which now hover around 10-12%, down from the 18-20% margins seen before the Covid-19 pandemic. The consumer goods companies are instead offering higher margins to quick commerce platforms so that they can afford the price tags.

Quick deliveries account for $5 billion, or 45%, of the country’s $11 billion online grocery market, according to Goldman Sachs. It is projected to capture 70% of the online grocery market, forecasted to grow to $60 billion by 2030, as consumers increasingly prioritise convenience and speed.

Many of the mom-and-pop shops are family-run and have been in business for generations. Yet they lack the resources to modernise and compete effectively with larger chains. Modern retail businesses, including quick commerce, begin with significantly more capital, thanks to funding from corporate investors, venture capital, private equity, and public markets.

“They can scale quickly and capture market share due to a superior product-service mix, larger infrastructure, and more robust business processes,” said Dutta.

Moreover, their ability to engage in price competition poses a challenge for small retailers and distributors, making it difficult for them to compete.

“This is something that has happened worldwide, in the largest markets, and I don’t think India will be an exception,” Dutta said, adding that it would be incomplete to single out a specific format of corporate business such as quick commerce as the sole villain in this situation.

“India is a tough, friction-laden environment at any given point in time, including government processes which don’t make it any easier,” he said.

Peer Pressure

Data from research firm Kantar shows that general trade, which comprises kirana and paan-beedi shops, have grown 4.2% on a 12-month basis in June, while quick commerce grew 29% during the same period.

Shoppers are becoming more omnichannel, rather than gravitating towards one particular channel, said Manoj Menon, director- commercial, Kantar Worldpanel, South Asia. “While the growth [for quick commerce and e-commerce] might appear to have declined compared to a year ago, a point to note is that the base for these channels has significantly grown. Therefore, achieving this level of growth is still commendable.”

Consumer goods companies such as Hindustan Unilever Ltd., Dabur India Ltd., Tata Consumer Products Ltd., etc., have acknowledged the salience of quick commerce to their packaged food, personal and homecare products. The platform currently comprises roughly 40% of their digital sales.

“We are working all the major players in the quick commerce space and devising product mix and portfolio. This is a very high growth channel for us,” according to Mohit Malhotra, chief executive officer, Dabur India.

Elara Capital analysts have pointed out that the share of quick commerce is expected to rise to60% in the near future with e-commerce and modern trade turning costlier for FMCG brands than quick commerce. “The larger brands tend to make better margins on quick-commerce platforms versus e-commerce due to lower discounts on the former,” it said in a report.

However, it is too premature to draw a parallel between kirana and quick commerce in terms of competition, given the significant size difference.

The average spend per consumer on FMCG in kirana stores stands at Rs. 21,285 annually while the same is Rs. 4,886 for quick commerce, according to Menon.

Rural Vs Urban Divide

Quick commerce is still an urban phenomenon. In contrast, in rural settings, where internet penetration is still catching up and access to large retail chains is limited, kirana stores continue to thrive.

According to Naveen Malpani, partner, Grant Thornton Bharat, while the growth of quick commerce is undeniable, this channel is not poised to replace traditional retail, which still has a wider reach in the country. “It will complement older models, filling a niche for immediate, smaller purchases. Also, a 10-20-minute delivery may not have a strong market pull in rural markets where distance and time are not much of a concern.”

Yet many others believe, even in these areas, the challenge is palpable.

The small businesses are beginning to feel the sting of same slow decline that once befell the ubiquitous telephone booths in the era of mobile phone, according to Sameer Gandotra, chief executive officer of Frendy, a start-up that is building ‘mini DMart’ in small towns where giants like Reliance and Tatas have yet to establish their presence.

As rural customers slowly start to embrace digital shopping and seek more variety, kirana stores must adapt or risk becoming obsolete, he said.

Besides, the popularity of quick commerce is set to challenge the dominance of incumbent e-commerce platforms, especially in categories such as beauty and personal care, packaged foods and apparel.

“Quick commerce is primarily operational in metros and tier 1 markets, which is impacting the sales of traditional companies in these areas. However, if quick-commerce players were to extend their operations to tier 2 and tier 3, it would even challenge companies such as DMart and Nykaa, and would pare sales and profitability,” noted analysts at Elara Securities.

Frendy’s Gandotra believes the journey for kirana stores is not a lost cause, but it requires strategic interventions. Many kirana store owners struggle to integrate point-of-sale systems, inventory management software, or even digital payment solutions. These stores need to embrace technology.

Another aspect is the need for policy support. Regulations to ensure fair competition can prevent monopolisation by large retailers. Additionally, subsidies, tax benefits, and grants for infrastructure improvements can help small businesses adapt to changing market dynamics. With renewed support, kirana stores can continue to be the backbone of Indian retail.

Nonetheless, there will be some who’ll be left behind during this shift. Analysts at Elara Capital warn that the swift rise of quick-commerce platforms, combined with aggressive discounting, could wipe off 25-30% of traditional grocery stores.

(Published on NDTV Profit)