admin

May 27, 2026

Kartikey Kashyap, Financial Express

27 May 2026

Three campaigns took home the Grand Prix awards from Goafest this year: Kansai Nerolac Paints”The Barefoot Journey” by Tribes Commu-nication in the Media category; Mountain Dew’s “Darescore” by Leo in Digital & Technology; and Center fruit (Perfetti Van Melle India)” Kaisi Jeebh Laplapayee”” by Perfetti’s in-house team in the Best Use of Voice/Technology category.

All three were exceptionally creative and scored high on likeability and novelty. There was another common element that tied the three together: How they used creativity to solve real brand problems.

Take PepsiCo’s Mountain Dew Darescore campaign. Nepal’s tourism economy relies heavily on mountaineering, but over 90% of global tourist revenue flows into Mount Everest. As a result, there is overcrowding on Everest, starving the country’s other formidable peaks of income and attention.

Enter Mountain Dew. In partner-ships with the Nepal Tourism Board and the Discovery Channel, the brand built the world’s first algorithmic mountain grading system. Leo aggregated decades of expedition records, terrain complexity maps, seasonal weather hazards, rescue failure rates, and first-hand Sherpa wisdom. They funneled these metrics into an engine and assigned a quantifiable “Dare Score” to individual peaks. This data visually demonstrated that height does not equal danger, giving climbers an scale to gauge terrain toughness.

The genius of the campaign was its consumer utility. Mountain Dew printed smart QR codes on millions of its beverage bottles. When a user scanned the bottle, it unlocked an immersive digital hub, where users could simulate climbs, map out route plans, read real-time weather conditions, and submit expedition inquiries. The campaign took Mountain Dew’s slogan, “Darr Ke Aage Jeet Hai” and algorithmically decoded it for real-world application.

The result: It Swept Goafest 2026 and collected medals across vastly different categories including Integrated, Brand Experience, Social Content, and Video Craft, besides the Grand Prix. “Darescore is a powerful example of how brands are moving from storytelling to measurable participation. For decades, adventure culture celebrated only the final summit. This campaign changed the lens, it quantified courage itself,” says Prabhakar Mundkur, director, advertising & media, Percept. “What made this Grand Prix-worthy was the fusion of technology, gaming logic, data and brand philosophy into one seamless experience.”

If the Darescore campaign embedded data into storytelling, Nerolac chose to stay away from the beaten path. Its “Barefoot Journey” was a hyper-local activation designed by Tribes Communication for Nerolac Perma NoHeat, an acrylic-based, heat-reflective exterior coating. The campaign focused entirely on real-world product performance.

Every summer devotees visit various religious sites and walk barefoot along sweltering walkways or wait in queues on hot concrete floors.

Along with local authorities, the teams coated thewalkways of several high-footfall temples across south-ern India with Nerolac Perma NoHeat paint. The paint reduced the surface temperature of the pathways by up to 15°C offering relief to devotees.

This campaign won the jury over with its simplicity. According to Devangshu Dutta, founder & CEO, Third Eyesight, “Though the campaign might target a small audience, it made an impact by shifting the frame,” Dutta points out. “The campaign turned advertising into lived experience,” Mundkur says. “People didn’t just hear a claim, they felt it. This is media not as interruption, but as empathy.”

For its part, Centre fruit brought back its hoary “Kaisi Jeebh Lapla-payee” tagline using generative AI. Teaming up with WPP, BharatGPT.ai and Google Cloud, Perfetti created voice-based GenAl interactions in local dialects that turned feature phones smart. “What made the experience special was that it felt less like advertising and more like a conversation,” says Gunjan Khetan, director marketing, Perfetti Van Melle. Al was an enabler of accessibility and a tool to build cultural relevance, Khetan adds. “The brilliance lay in how it con-verted a simple sensory reaction -the uncontrollable craving triggered by taste – into a scalable interactive idea. It was playful, memorable and unmistakably Indian. More importantly, it proved that consistency in -brand codes, when combined with fresh execution, can become a formidable creative asset,” Mundkur says.

There you have it. Winning creative awards is validating, but solving the client’s problems through that creativity remains the bellringer.

(Published in Financial Express)

admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

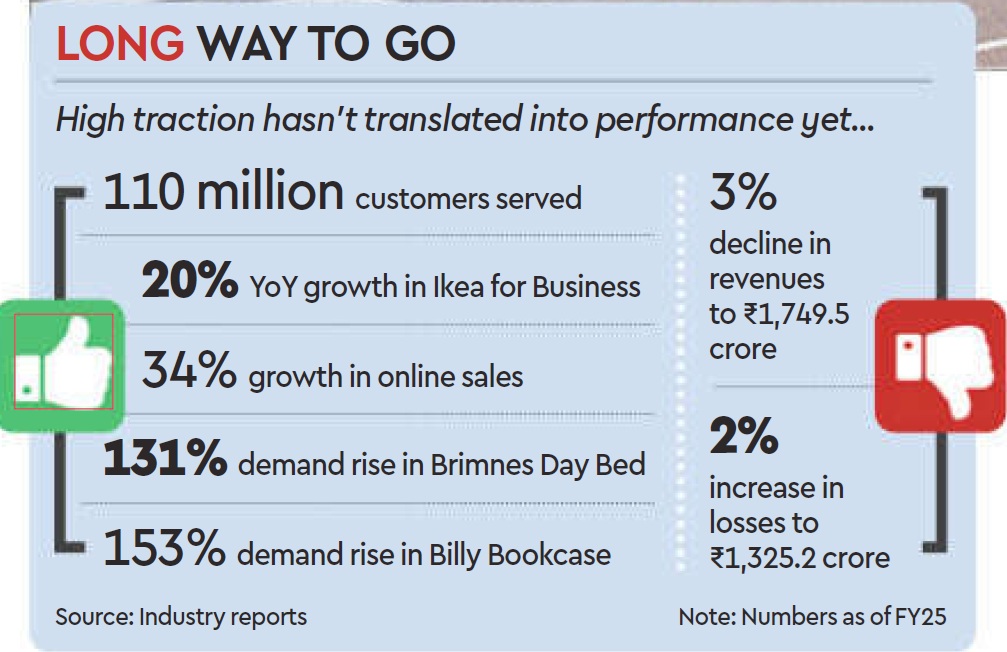

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

December 10, 2025

Shabori Das, ET Bureau

Dec 10, 2025

India’s social media platforms are powerful marketing tools but not yet retail destinations. Billions scroll and swipe daily, but few buy directly within apps. Unlike China, India faces regulatory hurdles and a lack of integrated payment systems.

A billion Indians scroll, swipe and double tap every day, but barely buy. Despite Instagram and Facebook Marketplace being in India for over a decade, social media here remains a showroom, not a store. Creators and D2C brands are hustling to convert attention into action, but the holy grail of in-app shopping where discovery, live streaming, and purchase happen seamlessly, remains out of reach.

The question is, what’s stopping India from becoming the next China or the US in social commerce?

Influence-to-Commerce Gap

Globally, social commerce is powered by influencers. In China, influencer Li Jiaqi reportedly sold products worth $2 billion on Singles’ Day on Alibaba’s online marketplace Taobao Live in 2021. Another popular influencer Zheng Xiang Xiang, with over 5 million followers on Douyin (the Chinese equivalent of TikTok), reportedly generated $18 million in sales in a week in 2023. These are numbers India’s creator economy can only dream of, for now.

To be clear, influencer marketing in India is booming. EY estimates the sector at over Rs 3,000 crore and yet, due to regulatory restrictions, social media platforms in India can’t host end-to-end transactions. What India has is content commerce, driven by players like Meesho and Myntra, not social commerce. Globally, social commerce is a $1-trillion market. China alone accounts for over $500 billion and the US, $100 billion. India’s share? Around $10 billion — despite being home to the world’s largest Gen Z population and the second-largest base of internet users after China.

What’s Holding India Back

“Just as quick commerce changed how India buys food, social commerce will change how we shop for fashion and lifestyle,” says Anand Ramanathan, partner, consumer industry leader, Deloitte South Asia.

The idea is simple: Social commerce enables an end-to-end purchase journey within a social media app. But in India, the final sale still happens elsewhere — typically on e-commerce platforms.

“In China, live streaming contributes nearly 20% of total e-commerce revenue. In India, it hasn’t taken off,” says Puneet Sehgal, CEO of D2C apparel brand Freakins. He believes in-app checkout could be transformative. “Our Gen Z audience spends over an hour daily on social media. If the purchase could happen right there, it’s one step less for the consumer — and one step closer to a sale.”

The China Contrast

China’s social commerce revolution was built on three forces — speed, scale and seamlessness. Influencer Zheng, for instance, showcases each product for barely three seconds and moves on. That brevity, combined with integrated payments, drives impulse buying at staggering volumes.

India’s influencer-driven commerce, by contrast, is still warming up. Projected to touch $ 55 billion by 2030, it remains largely limited to discovery and advertising.

The barriers aren’t technological, they’re regulatory. India’s payment rules require clear accountability and settlement tracking, making it difficult for global platforms to enable in-app sales. Meta’s 2023 policy shift also directed purchases off-platform, keeping Instagram and Facebook Marketplace confined to discovery and promotion, rather than purchase. For now, social media in India remains a potent marketing engine, not yet a retail destination.

Experiments and Exceptions

Some Indian players are testing new waters. Myntra’s Glamstream, launched this July, lets influencers host live sessions where viewers can “shop the look” in real time — though the final checkout still redirects you to the Myntra app.

“India’s creator economy influences over $300 billion in annual consumer spending,” says Sunder Balasubramanian, chief marketing officer at Myntra.“That could grow to $1 trillion in the next few years, making India one of the fastest-growing creator economies globally,” adds Lakshminarayan Swaminathan, vice president-product management, Myntra.

The potential is clear. In 2021, Taobao Live hosted a 12-hour live streamed sale with influencer Li Jiaqi in China that clocked $2 billion in presales and attracted 250 million viewers.

Closer home, Sujata Biswas, co-founder of Suta Sarees, recalls Instagram’s shortlived Shop Now feature. “We saw an immediate dip in transactions after it was withdrawn,” she says. “Fashion is about instant gratification. You see it, you want it and buy it right away.”

The D2C Advantage

India’s D2C market, valued at $87 billion as of 2025 by Deloitte, could be the biggest gainer if social commerce does take off. Most D2C brands currently pay 25–35% retailer margins to platforms like Myntra and Nykaa. Social commerce could let them bypass intermediaries and sell directly to their audiences.

“Anything that reduces friction between intent and purchase is gold,” says Sehgal. “If that entire journey — from watching to buying — happens within the same app, conversion rates would shoot up.”

Even so, social platforms come with their own costs. TikTok, for instance, charges promotional, marketplace and fulfilment fees. But for Indian D2C players, the larger hurdle isn’t cost — it’s access.

Open vs Closed Ecosystems

“India’s retail market is far more open than China’s,” explains Devangshu Dutta, CEO of ThirdEyesight, a retail consulting firm. “In China, closed ecosystems like WeChat and Douyin created the perfect environment for social commerce to thrive. In India, where consumers can freely move between Google, Meta and e-commerce giants, those closed loops don’t exist.”

Globally, TikTok Shop, Douyin, WeChat, Pinduoduo, and Taobao Live dominate social commerce. According to Business of Apps, a data provider for the global app industry, TikTok earned $23 billion in 2024, with nearly 23% of it from in-app and commerce purchases.

If similar models are launched in India, e-commerce giants would face direct competition from the very platforms that fuel their traffic.

The Wait Continues

From beauty tutorials to thrift stores, social media spawns thriving micro economies. Yet, true social commerce — where discovery leads directly to purchase — hasn’t yet clicked.

The next big leap for India’s e-commerce may not come from deeper discounts or faster delivery but from social media itself. “The idea of instant gratification is key,” says Biswas. “When the ‘Shop Now’ button comes back, we’ll be the first to use it.”

Till then, India scrolls, likes, shares — and waits.

(Published in Economic Times)

admin

November 13, 2025

Saumyangi Yadav,Entrepreneur

Nov 13, 2025

India’s consumer landscape is undergoing a decisive shift in 2025. While D2C brands that once thrived on digital-only distribution are now aggressively building an offline footprint, legacy FMCG majors are simultaneously acquiring digital-first brands to strengthen their portfolios and tap into new consumer behaviours.

As analysts suggest, these trends signal a maturing phase for India’s D2C ecosystem, one that blends physical retail and strategic consolidation.

Offline Push Accelerates

According to a recent CBRE report, ‘India’s D2C Revolution: The New Retail Order’, D2C brands leased nearly 5.95 lakh sq ft of retail space between January and June 2025, accounting for 18 per cent of all retail leasing during this period, up sharply from 8 per cent in the first half of 2024. Fashion and apparel dominated the expansion, contributing close to 60 per cent of D2C leasing, followed by homeware and furnishings and jewellery at about 12 per cent each, while health and personal care brands accounted for roughly six per cent. The shift is equally visible in the choice of retail formats: 46 per cent of D2C leasing went to high streets, 40 per cent to malls, and the remaining to standalone stores, reflecting the category’s growing focus on visibility, trial and experiential discovery.

Experts suggest that it represents a strategic pivot to blended engagement.

As Devangshu Dutta, CEO of Third Eyesight, notes, “India’s D2C surge is powered by digital-first consumers, tremendous improvement in seamless logistics, and low-cost market entry, supported subsequently by substantial amounts of investor capital chasing those startups that stand out from the competition. Yet, lasting success demands a more holistic view: the divide between online and offline is a business construct, not a consumer reality. The larger chunk of retail sales still happens through physical channels and, for brands that want to be mainstream, an omnichannel presence is absolutely essential.”

This also aligns with the broader market outlook. The India Brand Equity Foundation (IBEF), in its Indian FMCG Industry Analysis (October 2025), estimates the value of India’s D2C market at USD 80 billion in 2024, with expectations of crossing USD 100 billion in 2025. Much of this growth is being led by categories that combine frequent purchase cycles with strong digital discovery, beauty, personal care, and food and beverage segments where consumers are open to experimentation but demand authenticity, transparency, and a compelling product narrative.

“The Gen Z and millennial consumer cohorts value newness but also authenticity and unique product stories, which are best communicated in spaces that are controlled by the brand,” Dutta added, “In the launch and growth phases, this could be the brand’s digital presence including website and social media, but over time this can include pop-up stores, kiosks, shop-in-shops and even exclusive brand stores.”

CBRE’s data reflects this shift clearly, with D2C brands increasingly opting for flexible store formats and high-street locations to maximise traffic and visibility.

M&A Gains Momentum

Parallel to the offline push is a noticeable wave of consolidation. Large FMCG companies are accelerating acquisitions to capture emerging consumer niches and strengthen their digital-native capabilities.

In recent years, Hindustan Unilever has acquired Minimalist; Marico has bought Beardo, Just Herbs, True Elements, and Plix; ITC has taken over Yoga Bar; and Emami has secured full ownership of The Man Company. These deals, reported widely across business media in 2024 and 2025, point to the need for established companies to fast-track entry into high-growth, ingredient-forward, and youth-focused categories without the lead time of in-house incubation.

“Legacy FMCG companies are acquiring D2C brands to rapidly gain access to new consumer segments, product innovation, and digital-native capabilities, including direct engagement and insights. Such deals enable large companies to diversify portfolios, accelerate entry into trending segments by-passing the initial launch risks, and rejuvenate their brands with modern digital marketing expertise,” Dutta explained.

Challenges and Risks

But the acquisitions do not come without risk and challenges, analysts warned.

“However, integrating D2C operations also poses challenges, including cultural differences, the risk of stifling entrepreneurial agility, and the need to harmonise data and omnichannel strategies. The ability to nurture acquired brands without diluting their distinctive appeal will determine acquisition success,” Dutta added.

Yet even as the ecosystem expands, challenges remain. Offline stores add operational complexity, inventory planning, staffing, last-mile logistics, and real-time data integration. Still, the bottom line is that India’s D2C sector is moving into a hybrid era defined by tighter omnichannel integration, sharper product storytelling, and portfolio realignment through acquisitions.

(Published in Entrepreneur)