admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

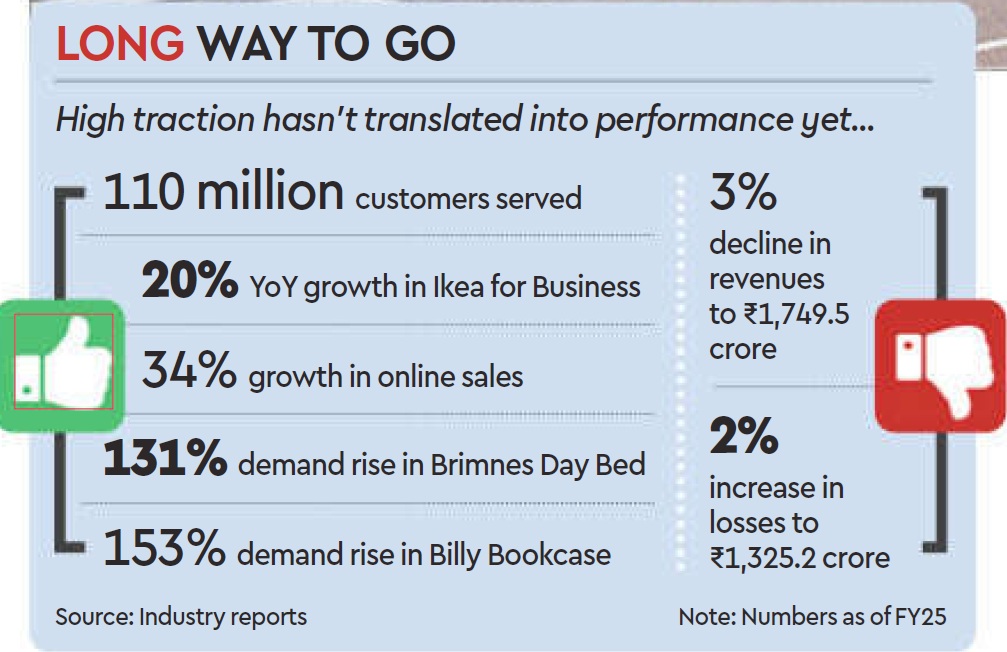

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

December 15, 2025

By Saumyangi Yadav, Entrepreneur India

Dec 15, 2025

India’s D2C ecosystem has grown rapidly over the past five years, but scale remains elusive. While thousands of brands have launched and many have crossed early revenue milestones, only a small fraction manage to break past INR 100 crore in annual revenue. According to a new report by DSG Consumer Partners, based on a survey of over 100 Indian D2C founders and operators, the problem is not demand or product-market fit, it is how brands attempt to scale.

The report shows that around 60–65 per cent of Indian D2C brands remain stuck in the INR 1–50 crore revenue band, with very few reaching the INR 100 crore mark. This stage marks the point where early traction exists, but growth begins to strain unit economics, teams, and operating systems.

Insights from over 100 D2C founders reveal that India’s fastest-growing brands win on fundamentals rather than speed alone. Clear product-market fit, disciplined data tracking, strong unit economics, creative velocity, and an early focus on retention consistently separate scalable brands from those that plateau. Founders also admit that performance marketing mistakes, pricing missteps, and weak creative systems slow growth far more than budget constraints. In a booming D2C landscape, capability gaps in operations, brand-building, and supply-chain depth are widening the divide between breakout brands and those stuck in the performance plateau.

Industry observers argue that this is where many brands mistake rapid online growth for sustainable scale.

As Devangshu Dutta, Founder & CEO, Third Eyesight, explains, “Scaling up online can be very rapid, but is also capital-hungry in terms of CAC. Given the intense competition, the lack of customer stickiness and the power of platforms, there is a constant churn of marketing spend which is a huge bleed for growing brands.”

CAC Inflation is The Real Constraint

One of the clearest findings from the playbook is that acquisition efficiency, rising CAC and unstable ROAS, is the single biggest blocker to growth, cited by more founders than funding or category expansion. Moreover, over 70 per cent of brands rely on Meta as their primary acquisition channel, increasing vulnerability to auction pressure and platform-driven volatility.

Dutta links this directly to the limits of a digital-only mindset. “Limited offline expansion can trap brands in narrow urban digital markets, blocking broader scale,” he said.

This over-reliance on online performance marketing often leads to growth that looks strong on dashboards but weak on cash flow.

Highlighting their report, Pooja Shirali, Vice President, DSG Consumer Partners, said, “Across over 90 consumer brands we’ve partnered with at DSGCP, one truth is clear: brands that master Meta’s ecosystem don’t just grow, they change their entire trajectory through strategic clarity and disciplined execution. The real drivers of scale have less to do with viral moments, and everything to do with the long-term fundamentals that make milestones like the first INR 100 crore predictable, not accidental.”

Why Omnichannel is Unavoidable

The report suggests that brands that scale sustainably are those that reduce overdependence on paid digital acquisition and expand their distribution footprint. However, offline expansion brings its own complexity.

Dutta stresses that omnichannel is not an optional add-on, but a strategic shift. “D2C brands must adopt an omnichannel approach, blending online with offline retail for sustainable and scalable reach. Clearly the channels work very differently and management teams have to be prepared and capitalised for the long haul to tackle acquiring customers with channel-appropriate strategies,” he adds.

This aligns with the DSGCP report’s broader insight that scale breaks down when brands fail to adapt operating models as they grow.

Even within digital channels, performance weakens over time. The playbook finds that 62 per cent of founders report creative fatigue, where repeated creatives fail to sustain ROAS despite higher spends. At the same time, 55 per cent admit to under-investing in CRM and retention, with most brands reporting repeat purchase rates of just 10–30 per cent.

Both the data and expert opinion point to a common theme: brands that cross the INR 100 crore mark are structurally different. They obsess over unit economics, processes, and capital efficiency rather than topline growth alone.

As Dutta puts it, “Scalable brands that cross the growth hump have leadership obsessed with unit economics and omnichannel execution rather than chasing vanity metrics. Cash always was and is king, especially at early stages of growth.”

He adds that execution strength matters as much as strategy. “They are able to grow and steer teams that build and replicate processes fast rather than spending time, effort and money reinventing all the time, and do so without constant CXO intervention.”

As competition intensifies and capital becomes more selective, the next generation of INR 100 crore D2C brands is likely to be defined not by speed, but by the ability to compound cash flows, institutionalise processes, and scale distribution beyond digital platforms.

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

(Published in Entrepreneur India)

admin

December 7, 2025

Gargi Sarkar, Inc42

7 December 2025

The past year has been nothing short of monumental for LensKart — from reporting another operationally profitable quarter in Q2 FY26 to making the public markets leap in November, and crossing a market capitalisation of INR 70,000 Cr despite a muted stock market debut.

A clear shift this year has been Lenskart’s effort to move beyond the image of a ‘basic D2C eyewear’ brand selling prescription glasses and sunglasses. The company is now working to reposition itself as a new-age tech brand.

Further, Lenskart is rethinking where and how its products are manufactured. Currently, around 20–25% of its frames are reportedly manufactured in India. The company is ramping up its domestic production. As a new manufacturing facility in Telangana is a work in progress, Lenskart intends to gradually shift most of its manufacturing operations from China to India.

In many ways, 2025 has been about scaling up for Lenskart, and as it embarks on a fresh journey as a publicly listed company, let’s take stock of the company in 2025 and where it might be headed in 2026.

Lenskart’s Smart Eyewear Bet

Lenskart began its smart eyewear journey last year with the launch of Phonic, its audio glasses. It later deepened its push into the segment by announcing a strategic investment in Ajna Lens, a Mumbai-based deeptech company that develops AI-powered XR glasses. Back then, Peyush Bansal described the move as the “next chapter” in Lenskart’s smart glasses journey.

Cut to December 2025, the company is all set to launch its AI camera smartglasses, B by Lenskart, by the end of this month.

What makes B by Lenskart noteworthy is that it isn’t being marketed as just another pair of smart glasses. The new eyewear features an integrated Sony camera that enables hands-free photo and video capture. The glasses come with a built-in AI assistant powered by Gemini 2.5 Live. They are designed to offer natural, conversational interactions and pack in a range of advanced features — from hands-free UPI payments and live translation to wellness insights and more.

What makes the move even more significant is Lenskart’s decision to open B by Lenskart to India’s developer ecosystem. By making its AI and camera technology accessible to consumer apps and independent developers, the company is enabling integrations across categories such as food delivery, entertainment, and fitness.

“By opening its AI smartglasses to third-party developers, Lenskart is moving from a one-time product-sale model to a platform ecosystem model. In the long run, this could unlock recurring revenue streams and higher margins,” said a product developer.

Besides, the company is aligning itself with a younger customer cohort, aided by affordability, style, and technology.

“That’s what seems to define their current strategy. Over time, they’ve also brought in elements of innovation like virtual try-ons, and any product, feature, or service that brings novelty and appeals to younger customers has become part of their brand approach,” said Devangshu Dutta, the founder of Third Eyesight.

Next, the timing couldn’t be better for Lenskart to place its bet on smart glasses. An IDC report reveals that despite a slowdown in smartwatch and earwear segments in the second half of 2025, smart glass shipments shot off more than 1,000% over the last year.

However, it’s not going to be smooth sailing from here.

At its core, Lenskart is still a consumer-facing company, and it needs new products to keep its revenue growing. But the competition is already heating up. Jio unveiled its own AI-powered smart glasses, Jio Frames, at Reliance Industries’ 48th annual general meeting. And of course, Meta continues to lead the global smart glasses market.

At this point, smart eyewear is a niche category, which comes with a hefty price tag.

“Unless cost drops dramatically, mass adoption is still a distant dream. As of now, the product will only attract early adopters and tech enthusiasts, rather than the mainstream consumer,” Dutta adds.

Lenskart’s Make In India Push

Lenskart is not only widening its product range but also ramping up its manufacturing. The company currently operates centralised manufacturing facilities in India (Bhiwadi in Rajasthan and Gurugram in Haryana), Singapore, and the UAE. It also has manufacturing operations in China.

Back home, Lenskart has also signed a non-binding MoU with the Government of Telangana for setting up a greenfield manufacturing facility for optical glasses. The proposed investment stands at INR 1,500 Cr and will be supported by certain incentives and assistance from the state government.

The new production facility is expected to strengthen Lenskart’s domestic manufacturing capabilities while reducing its exposure to foreign exchange fluctuations and import-related volatility.

However, the expansion comes with its own set of challenges. While the new manufacturing plant in Telangana is expected to strengthen Lenskart’s vertical integration, it will come with a hefty cost burden.

Profitability Still A Troubling Question

The cost structure is becoming increasingly important for Lenskart. Despite its headline-grabbing profitability, the company is still operating on fairly thin margins.

Lenskart reported a net profit of INR 297 Cr in FY25, a notable turnaround from a loss of INR 10 Cr in FY24. However, market analysts caution that the business’ core operations were unprofitable. It was largely “other income” or investment income that drove the FY25 bottom line.

“Though Lenskart has increased its revenue from INR 3,789 Cr in FY23 to INR 6,651 Cr in FY25, the company’s profitability has largely improved due to a rise in other income. While it reported a PAT of INR 297 Cr in FY25, a closer look shows that the profit was driven significantly by an increase in other income, which jumped to INR 356 Cr in FY25,” SimranJeet Singh Bhatia, senior research analyst for equity at Almondz Group.

The point of concern here is that Lenskart turned operationally profitable only after its market debut. Bhatia believes that at least three to four quarters of consecutive profitability will be needed to prove the company’s underlying strength.

However, making matters worse are the company’s climbing expenses, which stood at INR 1,980.3 Cr in Q2 FY26, up 18.5% YoY.

What Lies Ahead?

The year was equally sour for the eyewear major. While its IPO generated significant buzz and saw strong subscription levels, its market debut turned out to be a muted affair.

At the upper end of its INR 382 to INR 402 IPO price band, the public issue implied a price-to-earnings (P/E) multiple of roughly 235–238 times its FY25 profits, placing it among the most expensive consumer tech listings in India.

On its first day of trading, Lenskart Solutions Ltd. was listed on the NSE at INR 395 per share, a discount of 1.74% to the issue price of INR 402. The stock, however, fell close to 9% shortly thereafter. On the BSE, it debuted at INR 390, marking a discount of nearly 3%.

After the IPO, Bhatia adds, the biggest concern surrounding Lenskart is the store-level unit economics, particularly because a significant share of the IPO proceeds is being directed toward expanding its company-owned, company-operated store network.

Entering the new year as a public company, Lenskart will have to prove that its scale-up plans are justified and that it has greater control over its balance sheet. 2026 will be a critical juncture for the company, as the next three to four quarters will be closely watched for signs of sustainable growth, improved margins, and stronger operational discipline.

[Edited by Shishir Parasher]

(Published in Inc42)

admin

December 3, 2025

Pooja Yadav, Exchange4Media

3 December 2025

Over the last few months, India’s e‑commerce and quick‑commerce ecosystem has undergone a wave of structural regulatory and tax reforms. Be it the Goods and Services Tax Council (GST Council) formally bringing “local delivery services” under the tax net with an 18% levy, or the newly implemented labour and social-security reforms expanding obligations for gig workers on aggregator platforms like Swiggy and Zomato, the cost and compliance landscape for delivery and fulfilment is shifting significantly.

The latest GST clarification, delivery fees, packaging charges, and logistics surcharges are now creating a ripple effect across pricing, platform margins, and seller compliance requirements.

The past few months have already shown concrete signals that platforms are revising their incentives, delivery promises, and fee structures. Following the GST clarification, major food‑delivery players have raised their platform fees, for instance, Zomato reportedly increased its per‑order fee from ₹10 to ₹12 (pre‑GST), while Swiggy also raised fees in select markets. Some quick‑commerce arms are also reworking free‑delivery thresholds or fee waiver conditions. Swiggy Instamart also recently updated its free‑delivery threshold to orders above ₹299, with handling and surge fees applying below that level, per reports.

Meanwhile, some platforms seem to be signalling a de‑emphasis on “ultra‑fast for every order” as universally viable; free or fast delivery now appears increasingly tied to higher order values or subscription/membership perks.

It looks like these pressures are forcing platforms to reconsider long-standing quick-commerce levers such as ultra-fast delivery, first-order free offers, zero delivery fees, and flash discounts — which have historically driven customer acquisition and retention.

While Zomato did not comment directly, it referred to the Code on Social Security, 2020 (CoSS), noting that the platform is prepared for gig-worker obligations and does not expect the rules to negatively impact long-term business sustainability.

According to Kapil Sharma of Amazon Ads, “The e‑commerce landscape will continue to evolve, but some fundamentals remain constant such as delivering value to consumers and providing advertisers with meaningful ways to engage. Our full-funnel ad solutions allow brands to focus on objectives such as new product launches, brand building, or promoting larger pack sizes, ensuring campaigns remain relevant and effective even as the ecosystem adapts to changing costs and regulations.”

e4m reached out to Swiggy, Meesho, Zepto and BigBasket for comments, but did not receive responses until the time of publishing.

Several experts told e4m that the economic model of quick commerce, built on heavily subsidised delivery and small-ticket frequent orders, is under pressure. Platforms will need to find sustainable levers to retain customers without eroding margins. The industry has started to see a strategic recalibration where speed is increasingly becoming a hygiene factor rather than a differentiator, free delivery is becoming conditional, and platforms are nudging consumers toward larger baskets, subscription models, curated bundles, and scheduled deliveries. Brands, in turn, are also shifting focus from mass discounting to premiumisation, value-led messaging, and precise cohort-based targeting.

Will Free Delivery Become Rare?

With the new social‑security obligations for gig workers under India’s labour reforms, and the added cost burden of delivery services now subject to GST, the economic logic underlying “free delivery” as a marketing lever is coming under stress. Chetan Asher, Founder and CEO of Tonic Worldwide, echoes this view, noting that quick-commerce platforms previously operated on thin contribution margins and heavily subsidised small-ticket, frequent orders. With rising delivery costs and mandatory social-security contributions, universal free delivery is becoming increasingly unsustainable.

Industry analysts point out that the new social-security mandates and GST on delivery fees have lifted per-order costs noticeably. Most quick-commerce platforms already operate at low single-digit contribution levels, making blanket “free delivery” hard to justify. It may continue, but only as a conditional incentive tied to higher basket values, subscription memberships, or flexible delivery slots, rather than as a universal subsidy.

Shradha Agarwal, Co- Founder & Global CEO, Grapes Worldwide, added from an advertising standpoint, “It’s already happened, brands like Zomato, Swiggy, Amazon and Flipkart, who know we are going to buy from them, have shifted from ‘buy now’ tactics to ‘stay with me’ strategies. Those days are gone when platforms were giving blanket discounts, now brands are the ones tightening their offers.” Citing an example she mentioned how offline pricing is ₹235, but online it is sold at ₹185, with online adding to top-line rather than bottom-line.

On promo hooks like ‘₹0 delivery’, ‘first-order free’ or ’10-minute delivery’, Agarwal said, “As labour codes, compliance costs, and social-security contributions kick in, platforms will have less room to burn cash on promos that don’t create sustainable value. Consumers care more about convenience than freebies.”

On ad spend shifts, she noted, “Offer-driven campaigns will weaken, while value-driven storytelling will rise. ATL and influencer campaigns will strengthen, and performance marketing will become more strategic. Retail media will become non-negotiable.”

From a brand perspective, Asher pointed out that quick-commerce spends are increasingly evaluated against contribution margin rather than sheer GMV growth. Discounts and zero-fee offers are losing bite as customer acquisition costs rise. First-party data, replenishment journeys, and sharper cohort-based offers are gaining importance, ensuring that incentives remain ROI-focussed rather than mass-oriented. Similarly, speed claims such as “0 delivery” or “10-minute delivery” are becoming less differentiating in top cities, where most players already deliver within 15–20 minutes. Consumers now respond better to reliable ETAs, fair fee structures, and transparent pricing than aggressive speed promises.

Adding her viewpoint, Pooja Dhamdhere, Commerce Lead at Starcom India, said, “Incentives like free delivery or first-order offers are likely to evolve rather than disappear, and platforms will explore strategies such as tiered benefits, curated bundles, or differentiated pricing for specific cohorts.”

According to serial entrepreneur Alok Chawla and Founder at Kiko Live, added that while platforms may continue absorbing delivery costs in the short term, the long-term economics will require charging for ultra-fast or low-value orders. “Once platforms pass the actual delivery costs to consumers, we expect order frequency and small-cart behaviour to change, with many users shifting to larger baskets or neighbourhood retailers offering free delivery,” he noted.

Alternative Consumer-Incentive Models

Devangshu Dutta, founder and chief executive of Third Eyesight, who is an expert in the consumer and modern retail sector, stated, “I think platforms will pass a significant portion of the new 18% GST burden on delivery to end-consumers, either through higher delivery charges or repackaged platform fees. Some of this cost may also be clawed back from restaurant partners and quick-commerce brands via revised commissions, slotting fees or mandatory participation in marketing programmes, especially in categories where the platform has stronger bargaining power. Overall, I expect higher minimum-order thresholds and a tighter margin environment for restaurants and small D2C brands that rely heavily on third-party platforms.”

Analysts highlight strategies such as minimum-order thresholds, where free or lower-fee delivery applies only above a certain cart value, nudging consumers to order larger baskets rather than frequent small-ticket items. Subscription and membership-based models are also gaining prominence, offering benefits like waived or discounted delivery, priority fulfilment, and access to exclusive promotions in exchange for a fixed fee.

Scheduled or batch delivery windows are being used to optimise logistics, reduce cost pressure on ultra-fast last-mile fulfilment, and improve operational efficiency. Meanwhile, curated bundles and value packs, including weekly or monthly combos, allow consumers to plan purchases while enhancing per-unit economics for platforms. These levers also enable brands to maintain margin integrity without over-reliance on short-term discounting.

From a marketing perspective, this shift is prompting agencies and creative-first firms to move toward value-led messaging, premiumisation, and cohort-based targeting. Dhamdhere explained, “Platforms are optimising assortments by surfacing premium SKUs, nudging higher average order values, and using search optimisation to strengthen profitability. Brands are now focusing on aspirational consumers with curated bundles, subscriptions, and value-led propositions, rather than mass discounting. Performance campaigns will continue, but clarity of value and sustainable margin-led offers are becoming key for acquisition and retention.”

2026: Will regulatory pressure force a recalibration?

As 2026 approaches, the combined impact of GST on delivery services and mandatory social-security contributions for gig workers is forcing a fundamental rethink of quick-commerce economics. With blanket discounts, zero delivery fees and ultra-fast delivery no longer viable as mass levers, platforms are shifting toward basket-building, subscriptions, curated bundles and conditional incentives. The growth thesis is evolving from “habit formation at any cost” to protecting contribution margins through reliable ETAs, transparent pricing and premium assortments rather than aggressive subsidies.

Brands are recalibrating alongside this shift. Premiumisation, value-led propositions and sharper cohort-based targeting are taking precedence over broad discounting, and campaigns are increasingly evaluated on ROI, repeat behaviour and lifetime value rather than raw GMV. Tiered memberships, scheduled deliveries and subscription-led conveniences are emerging as key retention tools, while short-form video, influencer ecosystems and retail media help articulate value in a tighter cost environment.

Chawla said platforms will have to move beyond “₹0 delivery”, “first order free” and “10-minute delivery” as core propositions because the delivery cost burn far exceeds margins on small-ticket orders. Many consumers currently place multiple micro-orders a day simply because delivery is free, but once fees come into play, behaviour will likely shift toward clubbing orders or reverting to neighbourhood retailers, who themselves are rapidly digitising through partners like Kiko Live.

In the next phase, he adds, free instant delivery will only be sustainable for larger baskets, whereas scheduled delivery may become the default for free delivery, with paid instant delivery as an optional upgrade. Subscriptions may drive loyalty, but only up to a point, since the heaviest users would consume more deliveries than the subscription fee can realistically subsidise, making it difficult for platforms to make the model profitable.

This points to a clear playbook for 2026. “Free delivery” and mass discounting are expected to fade, giving way to conditional, tier-based formats that reward higher basket values, subscriptions or specific cohorts. Brand platform partnerships will also move toward profitability rather than promotional burn, with campaigns designed to protect margins instead of fuelling discount-led spikes.

Taken together, the signs suggest that 2026 will not mark the end of convenience, but the end of convenience that is subsidised blindly. The real test now is who absorbs this new cost of convenience, platforms, brands, or consumers. And as that battle plays out, another tension is already emerging: whether small and regional advertisers can survive the rising cost of visibility in India’s digital economy.

(published in Exchange4Media)