admin

June 12, 2026

Christina Moniz, Financial Express/Brand Wagon

12 June 2026

Legacy luggage brand VIP Industries is shedding some of its old baggage. The company, which manufactures Skybags and Aristocrat along with its flagship VIP range, has gone beyond cringey makeovers solely to attract Gen Z, and has embarked on a transformation journey that leverages its legacy to purvey a fresh range of offerings.

The company is modernising its digital presence and supply chain to catch up with competitors.

Managing director Atul Jain admits that the company has been a bit slow on the e-commerce front. It is reinventing its online store, while also making its products available across other e-commerce channels. “Quick commerce is becoming an important channel since there are several use occasions and segments within the luggage market. For instance, consumers often make last-minute purchases for a weekend trip via quick commerce. School bags and backpacks for kids, also great gifting options, are seeing good demand on these platforms,” he says

The company, which once dominated the ₹16,000 crore organised luggage market in India, saw a bit of a shakeup last year when the Piramal family sold 32% of its stake to a private equity firm. But it continues to be among the top three players in the category with a 29-30% market share. “Luggage plays the role of a traveller’s companion. We are creating designs to fit that role,” says Jain. “For example, our new VIP suitcases have a coffee cup holder and our cabin trolley bag has an easy access compartment for devices like laptops and iPads.”

The transformation goes beyond the product. VIP’s 350 exclusive physical retail touchpoints in the country are being revamped to offer a new customer experience.

Unpacking opportunities

Overits 55 years, VIP has grown from a briefcase brand into Asia’s largest luggage maker, housing labels like Skybags, Aristocrat, and Carlton (premium segment). While VIP is a premium offering targeted at business and travellers, its Aristocrat brand operates in the mass market and the budget-friendly Alfa targets consumers who typically shop in the unbranded segment. Aristocrat and Alfa together contributed upwards of 40% to the company’s revenue in FY25, followed by Skybags (28%) and VIP (20%).

Like many legacy brands, the VIP Industries’ faces the challenge to ia, stay relevant among Gen Z buyers as a plethora of digital-first brands swamp the market. “VIP has lost ground on relevance and desirability to a generation for whom luggage, like sneakers, is an expression of identity. To them, VIP feels like their parents’ brand,” says Nisha Sampath, managing partner, Bright Angles Consulting. D2C players in the category operate in the business of “lifestyle accessories” and not for “luggage” per se, she points out.

With a design-forward approach, incorporating features like compression systems, silent wheels and charging ports, these new-age brands have embedded themselves in travel “culture”, while also being Instagram worthy, say experts.

Jain says Skybags is VIP’s Gen Z focussed brand, which has over 8,20,000 Instagram followers. “We are sharpening our positioning for Skybags in our design, advertising and marketing outreach, especially on social platforms. The brand has a clear differentiation with youthful colours and prints to attract younger consumers,” he adds.

While D2C players have seen notable growth in recent years, they don’t have the kind of trust and brand equity that VIP has cultivated across its brands, nor do they have the scale or revenue that legacy brands have, he says.

Experts believe there is a significant growth opportunity for legacy players given that the unbranded market still accounts for ₹13,000-14,000 crore. The important lever for legacy brands is to clearly demonstrate value beyond price. “The unorganised market competes heavily on affordability, so organised players need to communicate durability, warranty, after-sales service, and consistent quality – areas where they have a strong inherent advantage over unorganised alternatives,” says Praveen Govindu, partner at Deloitte India. He adds that these brands should also invest in advertising and communicate this value to the end consumer.

Not only are the needs different among different consumer groups, competitive pressures are also diverse. “VIP can segment the market more cleanly with its portfolio of brands if it maintains absolute distinction to ensure clear consumer targeting across not just product attributes and pricing, but also communication and channels,” says Devangshu Dutta, CEO, Third Eyesight.

(Published in Financial Express)

admin

January 31, 2026

Surabhi Prasad, Business Today

Print Edition: 01 Feb, 2026

The last two years—2024 and, more notably, 2025—saw a wave of protests by a new generation of students and young professionals looking for political change, better economic conditions and more climate awareness across countries, including Bangladesh, Nepal, Indonesia and the Maldives.

But beyond these uprisings, Gen Z, the term used to describe those born in late 1990s to the early part of the 2010s and currently aged around 13-29 years, are not only questioning but also bringing forth changes in societal norms and economic behaviour. It’s not just a generation gap!

Gen Z are digital natives. They are tech savvy, have grown up with Internet in their homes, iPads as their support system, social media as a constant companion and take digital payments, online and quick commerce for granted. They tend to be night owls, the real gigsters, at home with artificial intelligence (AI) and machine learning, and with a lingo—cap, salty, suss and tea—that make others scratch their heads.

They also have newer challenges—rising unemployment, an uncertain economic environment, the rise of AI that has put a question mark on the future of work, climate change that is turning more real by the day, and skyrocketing real estate prices that mean a dream home could remain just a dream. Still, they are the rising consumer force who, over the next decade, are poised to become the largest chunk of the labour force and the focus of most companies.

For a country like India that is still young, Gen Z will soon be the economic force to reckon with. A recent report by not-for-profit think tank People Research on India’s Consumer Economy (PRICE) estimates that as of 2025, nearly one in five young individuals globally lives in India. “This is a formidable 420-million strong force, constituting approximately 29% of the nation’s total population, and made up of individuals aged between 15 and 29 as defined by India’s National Youth Policy (2014),” it said.

Labour sociologist Ellina Samantroy, Fellow at the V.V. Giri National Labour Institute, says India’s expanding Gen Z or youth workforce offers a significant opportunity for the country to reap the demographic dividend. As per the recent Periodic Labour Force Survey 2023-24, around 46.5% of the labour force is in the 15-29 age group. “There has been an increase in labour force participation in this age group from 42% during 2021-22. One can see the economic growth potential of this cohort,” she says.

However, with transitions and emerging opportunities in the world of work, it is important to harness the potential of this population cohort with adequate access to education and skilling, she says.

Devangshu Dutta, founder and chief executive of Third Eyesight, a boutique management consulting firm focused on the retail and consumer products ecosystem, says Indian Gen Z consumers are not a uniform cohort.

“A critical issue in India is the coexistence of aspiration and constraint, and India’s Gen Z are shaped by a mix of high digital exposure and wide economic disparity. While they are ambitious and globally aware, their purchasing power varies sharply across segments and locations,” he says.

Further, urban, higher-income Gen Z display global consumption behaviours such as brand experimentation, social commerce and premium aspiration, whereas a large proportion of Gen Z in Tier II, Tier III and rural India is highly value-driven and necessity-led, while drawing their inspiration from global and national sources. He also points out that unlike Millennials, Indian Gen Z are also entering the workforce in a more uncertain economic environment, making price sensitivity, smaller pack sizes and flexible payment options important. “Employment patterns such as informal jobs, gig work and delayed income stability are influencing consumption cycles and brand loyalty,” he says. There is a strong preference for digital discovery, vernacular content and peer-led recommendations, with trust built through community and relevance rather than legacy brand status.

Rising aspirations of Indian households and changes in consumption pattern with a marked move from essentials to more premium products have been well documented, most recently in Household Consumption Expenditure Surveys. But more granular, individual-level data from PRICE shows marked changes in education levels and behaviour of Gen Z and other cohorts such as Millennials (those aged between 30 and 45), Gen X (aged 45-60) and Baby Boomers (60+). A 2024 PRICE ICE 360 Survey of 8,200 respondents (18–70 years) in 25 major cities showed that Gen Z is the most educated cohort, spends the most time browsing the Internet and is more engaged with e-commerce and paid digital services.

Multinational and domestic companies are also now waking up to the Gen Z wave and are realising that they need to review strategies to gain the attention and loyalty of Gen Z as consumers and workers.

“Fashion, beauty and personal care, food and beverages, and mobile and consumer electronics are at the forefront of change in India,” says Dutta. Responding to Gen Z requirements, companies are designing products at accessible price points, expanding entry-level ranges and leveraging sachetisation and subscription models. Brands are investing more in regional languages, local influencers and platforms such as short-video and social commerce channels that resonate with young Indian consumers, he says.

But this process is still at a nascent stage, and many companies and analysts are still trying to assess this generation.

For the 34th Anniversary Issue, we at Business Today decided to decode what Gen Z is truly about, what influences them the most, what they aspire to purchase, what they can afford and what this means for India Inc. Over the course of the last few months, our newsroom saw animated discussions as senior editors sat down with younger colleagues to discuss lifestyle choices, brand loyalties and career ambitions, as we drafted an issue brief and a potential survey.

We then got in touch with PRICE, which worked with us on our survey objectives and tweaked the questionnaire. The result—a first-of-its-kind exercise where PRICE surveyed 4,311 Gen Z respondents, who are now entering the workforce with an income of their own, residing in metros and Tier II cities. The survey covered gender, education, employment status, personal income and household income classes. The main focus was urban, educated Gen-Z who has the income to be a strong consumer.

The research examined consumption behaviour across discretionary and essential categories, savings and credit attitudes, digital influence, brand loyalty, aspirations, and future spending intent.

And the results are indeed, surprising! The survey reveals that traditional consumption models that were built around age-based life stages, linear career progression and early credit adoption no longer hold for Gen Z. “This cohort’s behaviour reflects early exposure to economic shocks, greater career volatility and a redefinition of success away from speed toward resilience,” it underlines.

For businesses, misreading delayed demand as permanent weakness risks underinvestment just as Gen Z approaches its next consumption inflection, it warns. For financial services, premature credit push without trust-building will underperform. For consumer brands, price-led acquisition without quality consistency will fail to convert into lifetime value.

Delve into this issue where BT brings to you the in-depth findings of the survey and explains what this means for companies as they vie for a share of this growing consumer segment. Gen Z is not just about rizz and drip, it is giving the main character energy as they come of age.

(Published in Business Today, issue dated 1 February 2026)

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

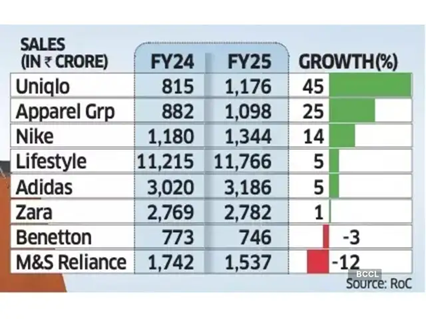

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

December 1, 2025

Priyamvada C, Mint

1 Dec 2025

A wave of investor capital is flowing into India’s laboratory-grown diamond (LGD) segment, as fastscaling brands tap rising consumer adoption in a market now worth well over $300 million. New-age brands have raised multiple rounds of capital on the back of growing market share and improving margins.

Actor Shilpa Shetty-backed Limelight, which is in talks to raise its second round of capital this year, joins the growing list of other small brands such as Onya, Giva, Jewelbox, Lucira Jewellery and Aukera, among others, who have snagged monies in recent months. Limelight has appointed Ambit Capital to raise about $20 million to fund its expansion plans, two people familiar with the matter said.

Confirming the fundraise, the six year-old company’s co-founder Pooja Madhavan said the funds will be used towards store expansion and brand building as it looks to touch 100 stores over the next year. “We are in final talks with growth PE funds and reputed family offices (for the fundraise),” she told Mint.

Other similar fundraises include Onya’s ₹5.5 crore in a pre-seed round led by Zeropearl VC last week, Aukera’s $15 million raise led by Peak XV Partners and Aditya Birla Ventures-backed Giva raised ₹530 crore in an internal round led by Premji Invest, Epiq Capital and Edelweiss Discovery Fund, as it looks to scale up its lab-grown diamond offerings.

Nine pure-play lab grown diamond startups collectively raised a record $26.4 million in 2025, compared with $4.7 million across eight startups last year, data from market intelligence provider Tracxn showed.

The development comes as India’s lab-grown diamond jewellery market, valued at about $300-350 million in 2024, expects to grow at a compound annual growth rate (CAGR) of 15% over the next decade, as per consultancy firm Redseer’s estimates. As the market evolves, several prominent jewellery brands will gradually pivot from exclusively natural/mined diamonds in favour of lab-grown alternatives, alongside high-end jewellers incorporating the lab-growns into their select collections, which will drive sales volumes and act as an affordable entry point for consumers.

This segment has particularly picked pace in the last five years, with millennials and gen Z leading this shift, driven by better value, trendier designs from new-age brands, and growing comfort with lab-grown diamonds as a certified, high-quality product. This category has also widened beyond occasional fashion to gifting, daily wear and increasingly bridal, reflecting sustained consumer confidence and a willingness to treat them as a mainstream jewellery option, Rohan Agarwal, partner at Redseer told Mint in an emailed statement.

He further added that new-age brands have steadily gained market share in the mid-ticket gifting and daily wear segment with many trying to push into premium ranges. While the competitive landscape is still evolving, incumbents have already started responding by launching LGD lines of their own, although the extent to which they can challenge remains to be seen.

Major Indian brands that are considering a foray into this category include Malabar Gold & Diamonds, Senco Gold, which has launched the subbrand Sennes and Tata’s Trent, which launched its brand Pome in Westside stores.

Devangshu Dutta, founder and chief executive officer at Delhi-based consulting firm Third Eyesight, echoed the sentiment. He explained that new-age lab grown diamond players are forcing traditional jewellers to introduce LGD options or risk losing younger customers. “Not just precious jewellery brands, even those that started as fashion jewellery are expanding their range with LGD designs.”

“Down the road, there is potentially scope for consolidation as investors tend to prefer a handful of scaled platforms with strong brand recall and robust economics. So, as the category matures, there may be strategic acquisitions by large jewellery houses and corporates, as well as mergers among funded startups,” he added.

Those startups that can combine in-house manufacturing, design capabilities and data-driven retail expansion would be at an advantage, Dutta said. “Key future growth areas for LGD startups include omnichannel retail presence within India, with offline stores especially in demand-dense locations such as the metros and Tier 1 cities, export markets both with potential cost advantages and brand expansion, and extending into fashion jewellery, everyday wear, coloured lab grown stones and even luxury collaborations that position lab grown as aspirational rather than merely budget friendly.”

(Published in Mint)

admin

September 17, 2025

Sowmya Ramasubramanian, Mint

17 September 2025

Snapdeal, run by AceVector, is relying on strong growth in fashion and apparel to strengthen its position in the competitive e-commerce space, especially during the high-stakes festive season when customer loyalty is low. According to CEO Achint Setia, the company has seen its fashion and lifestyle categories triple in growth this year, though exact figures remain undisclosed.

“Fashion has been a standout category this year and, in fact, has been possibly the fastest-growing one so far. Overall, lifestyle [including fashion, home decor, and kitchen] already accounts for 90% of our business today, and fashion is a major driving force,” Setia told Mint in an interview.

Setia was appointed to the role in January, replacing Himanshu Chakrawarti, who led Snapdeal and its subsidiary Stellaro Brands for three years. Setia has over two decades of experience across marketing and strategy roles in firms like Myntra, Viacom18 Media, and Zalora Group.

While the festival season is a key period for all consumer-facing brands and platforms, this year is important for Snapdeal as it is currently waiting for the Securities and Exchange Board of India (Sebi) clearance to list in the public markets.

“Approval from Sebi before the end of the financial year is crucial for Snapdeal. If they don’t get it, or if they have to refile, they’ll need to update their IPO documents with a full year of financial data. This means the festive season performance will be key in shaping investor sentiment, especially in a volatile market,” said a senior e-commerce executive, asking not to be named.

The firm filed its draft papers for an IPO reportedly to raise ₹500 crore through the confidential route in July, which allows it to withhold public disclosure of IPO details until later stages. Setia declined to comment on the progress of the filing.

Despite its early entry, Snapdeal is yet to make a mark among the top e-commerce players in the country by both market share and volume of transactions. For context, industry estimates show Flipkart as the market leader with 48% share, followed by Meesho and Amazon. The Indian e-commerce market is projected to grow at a compound annual growth rate (CAGR) of 21% and reach $325 billion dollars in 2030 as per an October 2024 report by Deloitte.

Founded in 2010 by Kunal Bahl and Rohit Bansal, Snapdeal was initially launched as a daily deals platform and later pivoted to a full-fledged marketplace in 2011. Over the years it raised more than $1.8 billion in funding from Softbank, Alibaba group, Foxconn and Blackrock among others. However, intense competition and the absence of a distinct growth strategy have gradually eroded Snapdeal’s momentum in the e-commerce space.

Snapdeal largely caters to cities outside metropolitan areas where value retail has picked up in recent years. Within this, fashion remains the top growth driver-with more than 80% of orders placed priced below 1599 and 80% of them com-ing from small town India, accord-ing to CEO Setia. “For us, it’s about the value-conscious mindset that could be sitting out of anywhere,” he noted.

Over the last few months, Snapdeal has invested substantially in in-house festive campaigns, as well as technology and tools for returns forecasting and logistics. According to Setia, it has also expanded its seller portfolio, adding more from key clusters like Tirupur, Surat, Ludhiana, and Agra.

According to a September 2024 report by market research firm Centrum, the mass-market fashion segment accounts for 56% of India’s total apparel market.

However, offline continues to account for more than half the sales, with Tata’s Trent, D-Mart, and Vishal Mega Mart offering a sufficient selection of price-conscious consumers in smaller towns.

While small-town India offers a wide online shopping-savvy market waiting to be captured, Meesho has raced past Snapdeal in those geographies, especially in value commerce.

“For a very long time, Snapdeal has been positioned as an e-commerce platform for Bharat, but it doesn’t necessarily hold a strong position. Meesho, Flipkart and Amazon have expanded their presence in these markets over the years, which means competition is so much more now,” said Devangshu Dutta, founder and chief executive officer at consulting firm Third Eyesight.

(Published in Mint)