admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

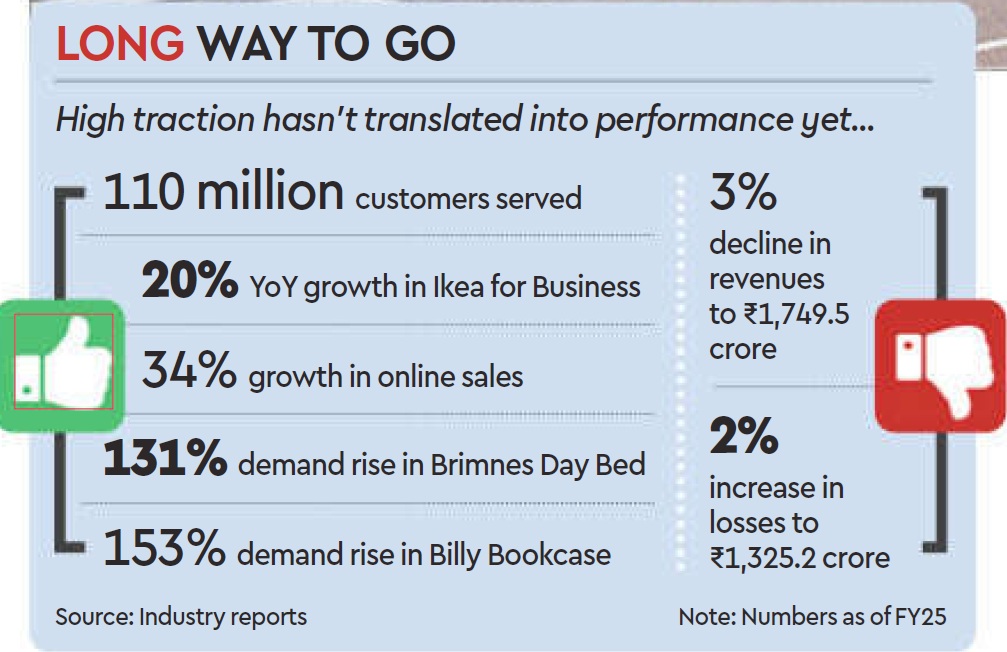

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

December 7, 2025

Gargi Sarkar, Inc42

7 December 2025

The past year has been nothing short of monumental for LensKart — from reporting another operationally profitable quarter in Q2 FY26 to making the public markets leap in November, and crossing a market capitalisation of INR 70,000 Cr despite a muted stock market debut.

A clear shift this year has been Lenskart’s effort to move beyond the image of a ‘basic D2C eyewear’ brand selling prescription glasses and sunglasses. The company is now working to reposition itself as a new-age tech brand.

Further, Lenskart is rethinking where and how its products are manufactured. Currently, around 20–25% of its frames are reportedly manufactured in India. The company is ramping up its domestic production. As a new manufacturing facility in Telangana is a work in progress, Lenskart intends to gradually shift most of its manufacturing operations from China to India.

In many ways, 2025 has been about scaling up for Lenskart, and as it embarks on a fresh journey as a publicly listed company, let’s take stock of the company in 2025 and where it might be headed in 2026.

Lenskart’s Smart Eyewear Bet

Lenskart began its smart eyewear journey last year with the launch of Phonic, its audio glasses. It later deepened its push into the segment by announcing a strategic investment in Ajna Lens, a Mumbai-based deeptech company that develops AI-powered XR glasses. Back then, Peyush Bansal described the move as the “next chapter” in Lenskart’s smart glasses journey.

Cut to December 2025, the company is all set to launch its AI camera smartglasses, B by Lenskart, by the end of this month.

What makes B by Lenskart noteworthy is that it isn’t being marketed as just another pair of smart glasses. The new eyewear features an integrated Sony camera that enables hands-free photo and video capture. The glasses come with a built-in AI assistant powered by Gemini 2.5 Live. They are designed to offer natural, conversational interactions and pack in a range of advanced features — from hands-free UPI payments and live translation to wellness insights and more.

What makes the move even more significant is Lenskart’s decision to open B by Lenskart to India’s developer ecosystem. By making its AI and camera technology accessible to consumer apps and independent developers, the company is enabling integrations across categories such as food delivery, entertainment, and fitness.

“By opening its AI smartglasses to third-party developers, Lenskart is moving from a one-time product-sale model to a platform ecosystem model. In the long run, this could unlock recurring revenue streams and higher margins,” said a product developer.

Besides, the company is aligning itself with a younger customer cohort, aided by affordability, style, and technology.

“That’s what seems to define their current strategy. Over time, they’ve also brought in elements of innovation like virtual try-ons, and any product, feature, or service that brings novelty and appeals to younger customers has become part of their brand approach,” said Devangshu Dutta, the founder of Third Eyesight.

Next, the timing couldn’t be better for Lenskart to place its bet on smart glasses. An IDC report reveals that despite a slowdown in smartwatch and earwear segments in the second half of 2025, smart glass shipments shot off more than 1,000% over the last year.

However, it’s not going to be smooth sailing from here.

At its core, Lenskart is still a consumer-facing company, and it needs new products to keep its revenue growing. But the competition is already heating up. Jio unveiled its own AI-powered smart glasses, Jio Frames, at Reliance Industries’ 48th annual general meeting. And of course, Meta continues to lead the global smart glasses market.

At this point, smart eyewear is a niche category, which comes with a hefty price tag.

“Unless cost drops dramatically, mass adoption is still a distant dream. As of now, the product will only attract early adopters and tech enthusiasts, rather than the mainstream consumer,” Dutta adds.

Lenskart’s Make In India Push

Lenskart is not only widening its product range but also ramping up its manufacturing. The company currently operates centralised manufacturing facilities in India (Bhiwadi in Rajasthan and Gurugram in Haryana), Singapore, and the UAE. It also has manufacturing operations in China.

Back home, Lenskart has also signed a non-binding MoU with the Government of Telangana for setting up a greenfield manufacturing facility for optical glasses. The proposed investment stands at INR 1,500 Cr and will be supported by certain incentives and assistance from the state government.

The new production facility is expected to strengthen Lenskart’s domestic manufacturing capabilities while reducing its exposure to foreign exchange fluctuations and import-related volatility.

However, the expansion comes with its own set of challenges. While the new manufacturing plant in Telangana is expected to strengthen Lenskart’s vertical integration, it will come with a hefty cost burden.

Profitability Still A Troubling Question

The cost structure is becoming increasingly important for Lenskart. Despite its headline-grabbing profitability, the company is still operating on fairly thin margins.

Lenskart reported a net profit of INR 297 Cr in FY25, a notable turnaround from a loss of INR 10 Cr in FY24. However, market analysts caution that the business’ core operations were unprofitable. It was largely “other income” or investment income that drove the FY25 bottom line.

“Though Lenskart has increased its revenue from INR 3,789 Cr in FY23 to INR 6,651 Cr in FY25, the company’s profitability has largely improved due to a rise in other income. While it reported a PAT of INR 297 Cr in FY25, a closer look shows that the profit was driven significantly by an increase in other income, which jumped to INR 356 Cr in FY25,” SimranJeet Singh Bhatia, senior research analyst for equity at Almondz Group.

The point of concern here is that Lenskart turned operationally profitable only after its market debut. Bhatia believes that at least three to four quarters of consecutive profitability will be needed to prove the company’s underlying strength.

However, making matters worse are the company’s climbing expenses, which stood at INR 1,980.3 Cr in Q2 FY26, up 18.5% YoY.

What Lies Ahead?

The year was equally sour for the eyewear major. While its IPO generated significant buzz and saw strong subscription levels, its market debut turned out to be a muted affair.

At the upper end of its INR 382 to INR 402 IPO price band, the public issue implied a price-to-earnings (P/E) multiple of roughly 235–238 times its FY25 profits, placing it among the most expensive consumer tech listings in India.

On its first day of trading, Lenskart Solutions Ltd. was listed on the NSE at INR 395 per share, a discount of 1.74% to the issue price of INR 402. The stock, however, fell close to 9% shortly thereafter. On the BSE, it debuted at INR 390, marking a discount of nearly 3%.

After the IPO, Bhatia adds, the biggest concern surrounding Lenskart is the store-level unit economics, particularly because a significant share of the IPO proceeds is being directed toward expanding its company-owned, company-operated store network.

Entering the new year as a public company, Lenskart will have to prove that its scale-up plans are justified and that it has greater control over its balance sheet. 2026 will be a critical juncture for the company, as the next three to four quarters will be closely watched for signs of sustainable growth, improved margins, and stronger operational discipline.

[Edited by Shishir Parasher]

(Published in Inc42)

admin

September 24, 2025

Shabori Das & Sagar Malviya, Economic Times

Bengaluru/Mumbai, 24 September 2025

Chinese fast-fashion platform Shein plans to triple the number of launches in India and shrink its design-to-launch timeline by a third to deepen its push into an increasingly competitive market, a top official said.

The company, which re-entered India through a partnership with Reliance Retail in February this year, said it is overhauling its supply chain to enable faster turnaround times. To achieve this, it has moved away from large-scale manufacturing hubs to smaller production lines with each line focused on creating a single new design daily.

“Our current timelines, measured from ‘thought to site’, stand at 46 days. We are targeting 30 days,” said Vineeth Nair, chief executive of Reliance’s fashion platform Ajio that steers Shein in India. “We currently deliver 320 styles a day – about 10,000 a month – and plan to scale that to over 30,000 styles monthly in the coming months,” he told ET.

Speaking about the speed of manufacturing, Nair said, “We quantify our options in terms of production lines, with each line optimised to deliver one design option per day, rather than factories. Some of our large production units have been repurposed into multiple lines.”

Shein first launched in India in 2018 with its own online shop. However, the app was banned by the Ministry of Electronics and Information Technology (MeitY) along with TikTok, WeChat and over 55 other Chinese apps.

One of the primary issues and controversies surrounding Shein’s India operations was the use of the consumer data by the Chinese apparel retailer.

Under the current partnership model, Reliance Retail is operating Shein under licensing agreement and ensures complete customer data ownership as per the company.

Unlike international markets, Shein India products are made in India.

“It’s still early days – just about three months since we introduced Shein to the India Gen Z,” Nair said. “And we are still in the process of adding multiple products, which we intend to do in the next few months.”

He said the brand is witnessing two million daily average users, dominated by 21-year-old women who account for 62% of the traffic.

Shein, the world’s biggest ecommerce-centred fashion retailer, however, may find it hard to replicate its global success in India, according to Devangshu Dutta, founder of retail consulting firm Third Eyesight.

“Shein’s edge internationally has been its speed of dropping its products, and the width of its product category. The India model is not the same. The India model of fashion is slower, and the product category width is not as large,” he noted. “Hence, the brand will in all probability end up competing with the already established market like Myntra, Zudio and the likes.”

(Published in Economic Times)

admin

September 22, 2025

Christina Moniz, Financial Express

22 September 2025

It is already the largest player among organised fumiture makers with over 15% of the market. With 1,000 stores, it has the widest retail store footprint among organised players. The 102-year-old brand is also the second-largest revenue con-tributor to the parent enterprise.

So why is Interio tinkering with its name, logo and colour attributes?

“We want to move away from being viewed as a functional brand to more of a design-led lifestyle one. We have a wider range of offerings that are more modular and aesthetic,” says Reshu Saraf, head of marketing communications at Interio by Godrej.

As a first step, it has a new logo and name change – from Godrej Interio to Interio by Godrej. The brand has earmarked ₹50 crore towards an integrated campaign across TV, digital, outdoor and in-store branding to promote its new proposition over the next year. Overall, it will invest ₹300 crore in expansion and technology with the goal to more than double revenues to ₹10,000 crore by FY29.

Younger consumers don’t see furniture as utility but as lifestyle, observes Puneet Pandey, strategy head and managing partner, OPEN Strategy & Design. “By moving from ‘solid and sturdy’ to ‘stylish and aesthetic’, the brand earns the right to play at higher price points as well. Design-led positioning will also unlock repeat purchase since people no longer wait a decade to change their furniture based on utility; they want constant upgrades to refresh their living spaces as their tastes evolve,” he notes, adding that Interio needs to make the marketing leap from “catalogue to culture”.

Saraf says the brand is also building differentiation with its customer experience. “We’re using digital tools for store walkthroughs and visualisers to help visualise our products in the home. Our product portfolio, which is deeply personalised ane tailored for Indian sensibilities, it is a major differentiator that few other brands offer,” she points out.

E-commerce is also a focus area with the brand looking to increase the revenue share from 15% to 20-22% by 2029. The company is leveraging Al to improve the search functionand sharpen personalisation. Saraf adds the that offline too, the brand will have large format experience centres to help people envision what their rooms could look like, along with mid-size and small-format stores.

Interio also plans to widen its retail store footprint from 1,000 to 1,500 by 2029.

As per industry estimates, the Indian furniture market is set to grow at 11% annually to reach $64.1 billion by 2032 from $30.6 billion in 2025. It is this growth momentum that Interio is looking to cash in on.

Built-in differentiation

Although a significant chunk of Interio’s business comes from its home remodelling services, within the furniture category, it competes with global players like IKEA and digital-first brands like Pepperfry. The challenge for Interio in this market is to embed the design-led positioning in its productsandcus-tomer experience, says Nisha Sam-path, managing partner at Bright Angles Consulting.

One of its biggest advantages is the Godrej brand. “The Godrej brand stands for many values prized in interiors such as quality, trust, reliability and durability with a ‘Made in India’ tag. However, the brand has not been so successful in building an image of cutting-edge design and innovation. These are new values that can make the brand more contemporary,” she remarks.

Devangshu Dutta, CEO of Third Eyesight concurs, pointing out aside from nimble competition, Interio’s key challenges also come from the dual pressures of increasing consumer expectations for rapid delivery and customisation on the one hand, with aggressive price competition on the other.

(Published in Financial Express – Brandwagon)

admin

June 7, 2025

Pooja Yadav, Inc42

7 Jun 2025

SUMMARY: Nearly two decades after its founding, Myntra has made its first international foray with the launch of‘Myntra Global’ in Singapore. Armed with 100+ Indian brands and over 35,000 styles, it is betting big on the 6.5 Lakh-strong Indian diaspora. Shipping directly from India without local warehousing helps avoid upfront costs but could lead to expensive shipping, long delivery times, and tough return logistics.

Nearly two decades after its incorporation in 2007, Myntra announced last month that it marked its first international foray under the new ‘Myntra Global’ banner. The fashion ecommerce marketplace has launched its operations in Singapore.

The Flipkart-owned platform aims to leverage brand loyalty to drive cross-border commerce by tapping into the Indian diaspora of around 6.5 Lakh people in the island nation.

However, while the brand’s intent is clear, the timing and choice of market raise some concerns. For starters, Singapore isn’t going to be an easy market, especially for a newbie like Myntra. This is because the region is filled to the brim with players like Shopee, Shein, Lazada, and Zalora that enjoy a strong brand recognition and stickiness.

Then, experts believe, Singapore-based shoppers are highly selective, constantly seeking great deals and ahead of the rapidly evolving fashion trends. This, among other factors, could make Myntra’s Singapore entry arduous.

So, what makes industry observers say so? Why isn’t Singapore a promising market for Myntra to begin with? What are the stakes at play here — the hits and the misses? Let’s get right into these questions to make sense of Myntra’s Singapore foray.

A Strategic Experiment?

Myntra’s entry into Singapore isn’t just about going global, it’s a strategic experiment to understand how Indian fashion resonates beyond borders.

According to CEO Nandita Sinha, the core of this launch is Myntra’s attempt to test the waters and understand the product-market fit for Indian fashion in an overseas setting.

But why Singapore? Well, the choice was driven by data. Myntra has found that about 10–15% of its web traffic comes from international markets, and Singapore stands out as a concentrated and engaged segment.

According to Statista (2024), approximately 6.5 Lakh Indians reside in Singapore, with around 3 Lakh Persons of Indian Origin (PIOs). Sinha pointed out, “While analysing our data and exploring potential market opportunities, we discovered that nearly 30,000 of these users are visiting our platform every month.”

This organic interest gave the company confidence to make Singapore its first stop under the Myntra Global banner. The platform has gone live in Singapore with 35,000+ styles, which it now plans to scale up to 1 Lakh in the near future.

However, what’s interesting is that Myntra is betting big on desi styles and brands to cater to the Indian diaspora in Singapore. The platform has launched a curated lineup of over 100 Indian brands, including popular names like Aurelia, Global Desi, AND, Libas, Rustorange, Mochi, W, The Label Life, House of Pataudi, Chumbak, Anouk, Bombay Dyeing, and Rare Rabbit.

Whether it’s ethnic wear, fusion fashion, or home décor, the idea is to spotlight Indian design and craftsmanship. Not to mention, Myntra sees significant potential for cultural occasions such as festivals, weddings and special celebrations.

As per Devangshu Dutta, the founder and chief executive of Third Eyesight, Singapore is an ideal market for Myntra’s international test run due to several reasons. For one, it is a digitally advanced, high-income market with a significant Indian diaspora that is familiar with the brands Myntra offers.

“This makes it a natural nucleus for testing an out-of-India offering,” Dutta said, adding that Singapore’s relatively small size makes it easier to manage the complexities of merchandising across different segments, potentially making it a more efficient testing ground.

Moreover, if the business succeeds, Singapore could serve as a strategic launchpad for Myntra to expand into other Southeast Asian markets. However, for now, Myntra’s Singapore launch is less about scale and more about learning.

Ankur Bisen, senior partner and head at Technopak Advisors, said that Myntra’s recent expansion makes strong strategic sense. This is because it is no longer an Indian company, and expanding to Singapore and Southeast Asia offers significant scale and growth opportunities.

“Unlike a purely Indian company, Myntra can explore multiple markets simultaneously and is not restricted to focussing solely on India,” Bisen said.

However, not everything is rainbows and sunshine, as Myntra’s success will only hinge on pricing, local adaptation, and understanding the distinct preferences of the Indian diaspora in Singapore that may be different from Indian buyers. In simple terms, one size may not fit all.

Then, shipping delays and high logistics costs could dilute the value proposition, especially in a market like Singapore where consumers are used to fast and affordable service.

Imperative to mention that Myntra currently has no plans to set up a warehouse in Singapore. Myntra CEO Sinha mentioned that products would be shipped directly from India, where the inventory will be maintained by the brands themselves.

“Myntra Global was not intended to be a localised service tailored to the Singapore market or any other international location. Instead, the focus would remain on serving global consumers from India, with no immediate plans for physical expansion or local warehousing.”

What Could Go Wrong?

Expanding into a new market is always a risky affair. Some potential pitfalls for Myntra could be logistics complexities, return management, and supply chain localisation.

Yash Dholakia, partner, Sauce.vc, too, pointed out that execution risks extend beyond pricing and scale to include logistics, returns, and supply chain.

Dholakia added that Singapore is a different ballgame altogether, as its distinct retail landscape is not an easy feat. “The fashion industry’s fast-changing nature calls for a sharp understanding of Singapore’s diverse, millennial consumers, who have unique cultural preferences and social media-driven buying habits.”

Moreover, many second- or third-generation PIOs see themselves mainly as Singaporean and have different cultural and fashion preferences.

Therefore, assumptions that what works in India will work for this class of consumers may lead to failure.

To hedge this, Myntra will have to take a fully local approach, which will include setting up independent teams on the ground to understand and address these local differences, rather than just copying and pasting its India playbook.

Moreover, from a branding and market reach perspective, targeting just the 10–15% Indian diaspora in Singapore restricts Myntra’s audience significantly. The fashion market in the city-state is already competitive, with several efficient players offering fast and affordable options.

“Myntra’s edge would primarily be Indian ethnic wear, which restricts its ability to emerge as a broad-market contender,” Dholakia said.

Per Dutta, relying heavily on the Indian diaspora may provide a strong initial boost, but this may not sustain for too long.

A Launchpad For D2C Brands

This is not the first time Myntra has tried to enter an international market. In 2020, Myntra partnered with UAE-based platforms, noon and Namshi, to enter the Middle East with a few Indian brands.

However, its current expansion into Singapore looks more ambitious with a cavalry of over 100+ Indian brands.

To strengthen its footprint in Singapore, Myntra is offering free shipping across a wide range of categories, including women’s fashion, kidswear, and home essentials.

Myntra is offering products across a wide range of price buckets. In the women’s tops category, prices start as low as INR 350 with brands like Tokyo Talkies, and go up to INR 4,800 with brands like Berrylush, DressBerry, and Vishudh. Western dresses also extend up to INR 7,100. In ethnic wear, kurtas range from INR 833 to over INR 3,800, while sarees are priced between INR 1,200 and INR 18,000.

“In terms of pricing, it’s ultimately the brands themselves that determine their price positioning on the platform. As they begin listing and transacting with consumers, they will decide how they want to price their products,” said Sinha.

In addition, what could work in its favour is the opportunity to give the global audience a taste of fast-growing Indian D2C brands.

Many Indian internet-first brands haven’t had the chance to engage with global consumers before, but this expansion lets them showcase their products directly to the Indian diaspora in Singapore.

Besides, the expansion will allow Indian brands to understand new consumer preferences, optimise their product mix for cross-border demand, and grow their presence beyond India.

This pilot could indeed spark broader cross-border opportunities for Indian D2C brands. But it demands localised marketing, deep consumer understanding, and a willingness to adapt to regional preferences.

For brands used to making for Indian buyers, this could be a steep but rewarding learning curve. If executed well, it offers them not just an entry into Singapore but a scalable template for global expansion.

The Cross-Border Gamble

Myntra’s global play comes at a time when the ecommerce platform posted a net profit of INR 30.9 Cr in FY24 versus a loss of INR 782.4 Cr in FY23. This turnaround came on the back of a 15% increase in its operational revenue and tighter cost control.

The platform generates revenue through a mix of transaction fees from sellers, logistics services, advertising, and its private labels. To move towards profitability, Myntra brought down its total expenses to INR 5,123 Cr in FY24 from INR 5,290.1 Cr in FY23.

However, its recent entry into Singapore may bring new financial challenges, even as Myntra has opted not to set up a warehouse in Singapore. It would rather ship products from India through third-party logistics providers.

So, is the fashion major being penny-wise and pound-foolish?

Probably. While this asset-light model avoids upfront capital expenditure, it introduces risks such as longer delivery times, higher logistics costs, customs delays and complicated return processes that could sour customer sentiment. For a platform that just turned profitable, these are crucial levers that could strain margins.

Further, even though Myntra is not offering exchange and returns currently, once it does, it could complicate things further.

This is because shipping a 2 Kg fashion parcel from India to Singapore costs an estimated INR 2,800 to INR 3,500, inclusive of air freight, GST, and last-mile delivery. Reverse logistics could add another INR 1,200 to INR 2,000 per item, pushing the total cost per cross-border order significantly higher.

According to Dibyanshu Tripathi, cofounder and CEO of Hexalog, a logistics company, cross-border logistics could significantly impact Myntra’s profitability as it expands into Southeast Asia.

“Sustaining margins will be challenging with high per-order shipping costs, return expenses, and longer delivery timelines that may affect customer satisfaction. Without localised infrastructure or cost efficiencies, profitability in new markets may be hard to maintain despite revenue growth,” Tripathi said.

In contrast, players such as Lenskart and Nike have structured their global expansions with supply chain control at the core.

All in all, Myntra’s Singapore foray is a bold experiment aimed at testing global appetite for Indian fashion, especially among the diaspora.

While the move offers promising opportunities for Indian D2C brands and cross-border growth, it’s also fraught with challenges. For one, with a lack of local infrastructure, high shipping costs and a diaspora divided between two cultures, sustaining this expansion may prove tough. Can Myntra turn its Singapore pitch into a lasting global success story?

(Published on Inc42)