admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

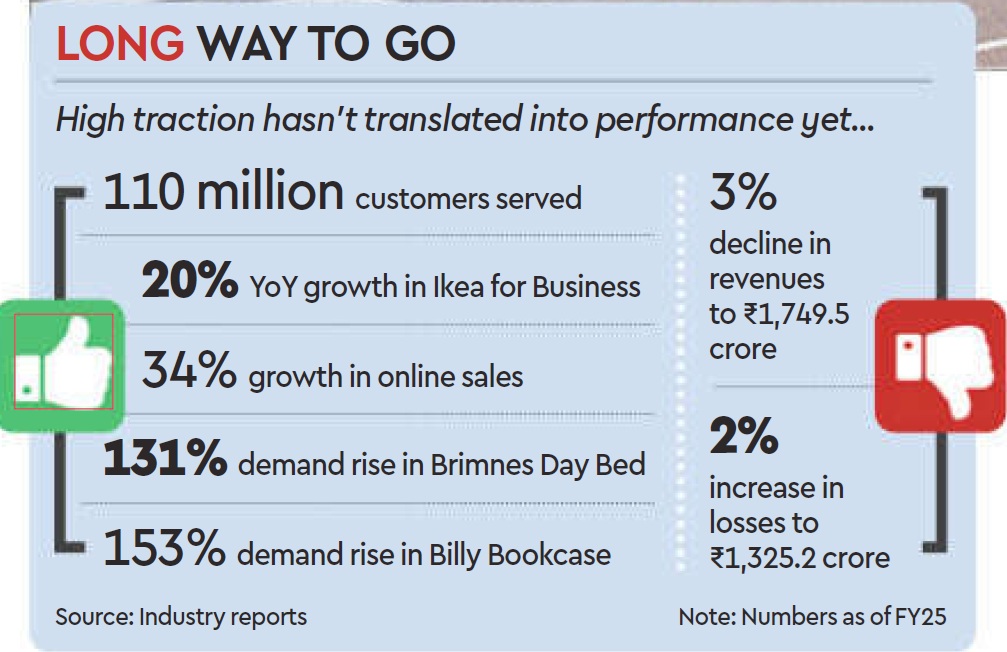

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

May 8, 2024

At the recent Phygital Retail Convention in Mumbai, Devangshu Dutta anchored an engaging “Fireside Chat” with Bhavana Jaiswal of IKEA India and Kapil Makhija of Unicommerce , on retailers engaging with their customers across channels and formats, and the opportunities as well as challenges in managing experiences seamlessly across online and offline interfaces.

Watch the video at this link:

admin

December 20, 2021

Written By Vaishnavi Gupta

The furniture brand’s retail roadmap includes city stores in Delhi, Mumbai and Bengaluru, followed by tier I and II towns

For the Ikea model to succeed, adequate demand-concentration is crucial, which is being currently provided by the bigger cities in India.

After launching two large-format stores in India in a span of three years — one each in Hyderabad and Navi Mumbai — Ikea opened its first small-format store in Worli, Mumbai, to become “more accessible and convenient”. About 90,000 sq ft in size, these ‘city’ stores are already present in markets such as New York, London, Paris, Moscow and Shanghai.

The furniture market in India stood at $17.77 billion in 2020, and is expected to reach $37.72 billion by 2026, growing at a CAGR of 13.37%, according to a Research and Markets report. Godrej Interio, UrbanLadder and Pepperfry are among the big players in this space, all with a significant online presence, too. Godrej Interio has 300 exclusive stores in India, while Pepperfry has more than 110 Studios.

Spread across three floors, Ikea’s first city store has 9,000 products in focus, of which 2,200 are available for takeaway and the rest for home delivery. “We have observed that it is not easy to find large retail locations in cities like Mumbai and Bengaluru. The small store offers convenience and accessibility for consumers to experience Ikea products,” says Per Hornell, area manager and country expansion manager, Ikea India. This launch is in line with the company’s aim to become accessible to 200 million homes in India by 2025, and 500 million homes by 2030.

More launches are being planned: another city store in Mumbai in the spring of 2022 and a large-format store as well as a city store in Bengaluru by the end of 2022. For its retail expansion in Maharashtra, the company plans to invest Rs 6,000 crore by 2030. “We are on track to exceed the investment commitment of Rs 10,500 crore made for India in December last year,” adds Hornell. Delhi, Mumbai and Bengaluru are the three cities on its radar at the moment, which will be followed by tier I and II towns.

Furthermore, Ingka Centres, part of Ingka Group that includes Ikea Retail, is coming up with its first shopping centre in Gurugram (followed by Noida), which will be integrated with an Ikea store.

In India, unlike its organised furniture market competitors, Ikea doesn’t have a pan-India online presence yet. It has been following a “cluster-based expansion strategy” for its online offering, but the company insists this is not a limitation. “At present, 30% of our overall India sales come from online channels,” Hornell informs. Through its e-commerce website and mobile shopping app, the company currently operates in Hyderabad, Mumbai, Pune, Bengaluru, Surat, Ahmedabad and Vadodara.

On the other hand, players like Godrej Interio and Pepperfry have big plans to tap new markets. The former aims to add 50 exclusive stores each year, while Pepperfry aims to achieve the 200 Studios mark by March 2022. In September this year, Pepperfry forayed into the customised furniture segment with the Pepperfry Modular offering, which focusses on modular kitchens, wardrobes and entertainment units.

Good start?

This is a good time for Ikea to establish its presence in the Indian market, says Alagu Balaraman, CEO, Augmented SCM. “Earlier, people used to rely on carpenters for furnishing their homes; now, they prefer to buy ready-made furniture. The market is moving towards acceptability, making plenty of headroom for growth for these companies,” he says.

Ikea’s cautious expansion approach in a market like India where several local dynamics are at play, is tactful, analysts say. Devangshu Dutta, founder, Third Eyesight, says, “In the past, Western businesses have made the mistake of simply copy-pasting formats and strategies in emerging markets from their more developed markets.” He believes there is “nothing wrong” in being incremental while growing footprint. “There’s no sense in carpet-bombing the market with stores, when many may end up being loss-making or sub-optimal,” he adds.

Getting the product mix and pricing right would be key in realising the full potential of this market. Balaraman says Ikea will have to balance its global portfolio with what it is doing locally, and make sure it is profitable.

For the Ikea model to succeed, adequate demand-concentration is crucial, which is being currently provided by the bigger cities in India. Given its global popularity, the furniture giant, analysts say, is poised to see traction in the metros and tier I cities.

Source: financialexpress

admin

January 6, 2019

Written By Editor

Ikea wants to sell you more than furniture – it wants to sell sustainable living, and that includes what you need to grow your own food.

Ikea is reported to be developing a new line of products with British industrial designer Tom Dixon, to be formally announced in May 2019 and released in stores in 2021.

The retailer has already introduced a hydroponic system to grow lettuce on your kitchen countertop, and the company’s innovation lab, Space10, experimented with a flatpack urban farm to fit in your backyard.

The collaboration with Tom Dixon would possibly to make it easier to grow plants in small spaces in city homes and to maximize the amount of food production in the smallest possible space.

With this, Ikea is jumping on to the trend of products focused on people farming in an urban environment.

Source: billionfarmers

Devangshu Dutta

October 23, 2009

Trade, of course, has been global for millennia, so it seemed hardly unusual for retailers in the US, and in Europe to begin sourcing from distant countries in Asia where certain items were more readily available or significantly cheaper. Imports have also been encouraged as a political and developmental vehicle to aid friendly countries.

So, on the sourcing-end, large retailers have been comfortably operating beyond international borders for several decades even while the stores-end of their business was entirely domestic.

For most large modern retailers however, after the post-Second World War economic boom their core markets have grown relatively slowly (and rather predictably). While the sheer size of the US market kept American retailers busy domestically, planning and legal restrictions in terms of store size, locations, market share etc. limited manoeuvrability for retailers in Europe.

Among the current major retailers, the early retail explorer, Carrefour set out into neighbouring Spain in 1973 and then into distant Brazil in 1975. Soon after, Dutch retailer Ahold landed in the USA in 1977.

However, it took the opening up of East European economies in the 1990s to really prime the pump for growth of international retail. Suddenly, many more millions of consumers became available to European retailers close to their existing markets – both geographically and culturally – and western European retailers jumped at the opportunity.

At the same time, China seemed to have become steadily more open over the previous decade and in the early-1990s India looked accessible again. Some of the Latin American markets were also steaming up.

And, obviously, the prospect of 3-4 billion new consumers in emerging or developing markets was clearly not going to be ignored. In 2001, post dot-com, another inspiring idea hit the business world that was desperately looking for hope – the golden BRICs – the four countries focussed upon by Goldman Sachs as the biggest economies of the future: Brazil, Russia, India and China.

As incomes grew in these “developing” or “emerging markets”, the hypothesis was that consumer would want products and services similar to those in the more developed markets, creating the opportunity for retailers to cross borders. In the last 15 years or so, retail internationalization (and gradually “globalization”) has become an increasingly acceptable theme – in conceptual thinking, in retail boardrooms, in white papers, and finally in trade and mainstream media. The world has witnessed a network of retail subsidiaries, joint-ventures, franchise and other relationships spreading across continents.

Certainly, through the 1990s and 2000s, growing tele-connectivity, fashion, portable TV programming concepts, movies and print media seemed to give the impression that consumers around the world are becoming more similar, and can be reached by common formats and brands. Led by the FMCG companies on the one hand and fashion brands on the other, insights, concepts, products, formats, advertising campaigns are routinely extended across countries. (Unilever’s TV commercial for Close-Up in West Asia is a great example of this – an Anglo-Dutch company’s international brand of toothpaste, Indian models in Thailand, an Arabic voiceover and a Hindi song (“Paas Aao” – “Come Closer”) by Sona Mohapatra – surely you don’t get more global than that?)

But wait! Is the picture really as clear as that?

In 2006 Wal-Mart pulled the plug on its €2 billion German business that was a combination of German chains that it had acquired. In Russia it still has only a development presence since 2005, though it is reported to be looking at opening 10-15 stores in the following three years. According to Newsweek, Wal-Mart’s 13 year old Chinese business – even after an acquisition that is still to be approved – will have fewer stores than it would have opened in the US just in 2009. In the past it has struggled in Japan and Brazil.

In June 2009, Carrefour opened its first 86,000 sq. ft. hypermarket in Moscow, and a second one soon after that. In September, the company affirmed that the BRIC markets were its highest priority for international growth. However, in October it announced that it was pulling out of Russia. Within 4 months of the first store, Russia has gone from a market with “outstanding long term potential” to being a market to exit. In previous years the company has moved out of Japan, South Korea and Mexico. The Economist reports that significant Carrefour’s shareholders are forcing it to look at selling its Chinese business as well – obviously a move that would be politically very sensitive in China. The same shareholders are also reported to be urging a sale of its Latin American business. For now, the official statement from the company maintains an ongoing interest in all these markets.

Ikea has decided to freeze further investments in Russia, and has decided not to enter India until the Indian government allows 100 per cent foreign ownership of retail operations. It entered China in 1998, and has only 7 stores so far.

Even as Carrefour and Ikea announce plans to pull out of Russia, Russian retailers have pulled out from Ukraine, while Metro is cautious in its outlook about that country. French retailer Auchan has opened three stores in Ukraine since 2007, while the German retailer Rewe has opened all of nine since 2000.

Could the juggernaut of global retail be slowing, stopping or even – shock! – reversing? Are the BRICs and emerging markets falling out of favour?

Before we jump to conclusions, as they say in the television world: please don’t adjust your sets. As the French author Karr wrote: “plus ça change, plus c’est la même chose” (the more things change, the more they are the same).

It is a fact that, no matter how international or global a company becomes, when it gets to the business of retail, it needs to be intensely local. While elements of the business – concepts, products, people, money – can travel across borders, it is extremely difficult to take across an intact retail mix and expect to address a significant portion of the population in the new country. And given how important scale is to mass retailers, lack of localization would be a significant hurdle.

A company sourcing products from a developing country can fully expect his suppliers to adapt to his practices and customs. On the other hand, the same company entering that country as a retailer needs to do exactly that – adapt to the customers – rather than expecting them to fall in line because the “best practice” manual dictates certain processes or because central merchandising found some deals that were great for the home market which are totally irrelevant in the new market.

However, there are encouraging signs that retailers looking to grow internationally understand this more and more. Tesco, for one, has been following a localized approach in Thailand and South Korea, while Carrefour, Ikea, Wal-Mart have all steadily modified their approach in China and other markets. Wal-Mart’s cautious steps in India, including the stores opened by its joint-venture partner Bharti, are a complete contrast to the aggressive “plans” that were being reported in the press 2006-onwards. Recently Wal-Mart’s international chief C. Douglas McMillon was quoted by BusinessWeek as saying “we know you can’t run the world from one place”.

For the larger international retailers this means that, the benefits from international scale would be limited by the amount of localization that they carry out in their operations. For smaller and local competitors that are based in an emerging market this means a fighting chance to remain in business and even remain market leaders.

Lastly, as far as all the dark clouds gathered over international retailing and all the retreats being announced – stay tuned – this weather will change, too.