admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

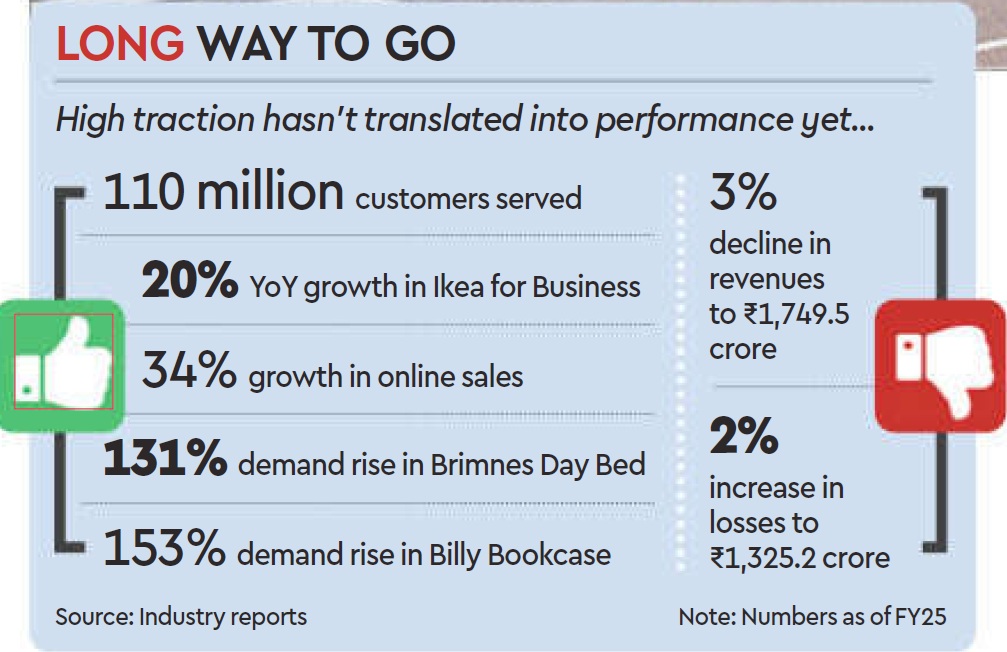

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

October 7, 2024

Writankar Mukherjee, Economic Times

7 October 2024

Reliance Retail has initiated efforts to enter the thriving quick commerce market in a move that is set to escalate competition for Zomato-owned Blinkit, Swiggy Instamart and BigBasket, among others. The country’s largest retailer has started offering quick commerce services in select areas in Navi Mumbai and Bengaluru through its ecommerce platform JioMart since last weekend.

It will initially sell grocery items from its retail stores totalling about 3,000 nationwide, eventually adding value fashion and small electronic products such as smartphones, laptops and speakers, a senior executive said. All orders will be fulfilled from its own network of stores including Reliance Digital and Trends.

The retail arm of Reliance Industries plans to rapidly scale up its quick commerce venture pan-India by this month-end with the aim to deliver most orders in 10-15 minutes and the rest within 30 minutes, the executive said. The company will use its acquired logistics service Grab for the fulfilment.

Reliance, however, doesn’t have any plan to set up dark stores or neighbourhood warehouses, unlike other quick commerce operators, the executive said. Analysts said this may become a challenge in delivering orders within 30 minutes in large cities where traffic is high during peak hours.

To entice customers, Reliance won’t charge any delivery fee, platform fee or surge fee irrespective of the order value, and keep a major focus on untapped smaller cities and towns where quick commerce operators like Blinkit are yet to enter, the executive said. Other platforms have a delivery fee and platform fee.

Reliance plans to offer a wider choice of products of 10,000-12,000 stock keeping units by linking its entire store inventory to the quick commerce business, which too is much more than rivals.

Eventually, the company aims to cover 1,150 cities spanning 5,000 pin codes where it runs grocery stores. The executive said the company would target a bigger share of business from towns and smaller cities hitherto untapped by quick commerce firms.

“Reliance has reworked the way orders are delivered for JioMart. Earlier, orders had a scheduled delivery taking 1-2 days by small trucks who would take multiple orders and deliver them one by one. Now, all grocery orders will be quick commerce where one delivery bike or cycle will deliver one order. Each grocery store will cover a 3 KM radius,” the executive said.

Earlier this year, the company tried to reduce JioMart delivery timings to a few hours or at least the same day under its hyperlocal initiative. It has fine-tuned the process further to 10-30 minute delivery. “This has become a top-of-the-kind requirement in the market right now,” the executive said.

A spokesperson for Reliance Retail didn’t respond to ET’s queries.

Devangshu Dutta, chief executive at consulting firm Third Eyesight, said Reliance can ultimately use a blended approach of quick commerce deliveries in areas near its stores and scheduled deliveries a bit far away.

“Since they are in a market share acquisition mode in quick commerce, charging no transaction fees and offering higher discounts on products is a given. There is significant scope for deep-pocketed players like Reliance to strengthen presence in quick commerce. They have aggressively backed other experiments in the retail business once they worked, and may do it again,” said Dutta.

For fast-moving consumer goods companies, quick commerce is the fastest growing channel, accounting for 30-35% of total online sales.

(Published in Economic Times)

admin

August 10, 2024

Faizan Haidar, Economic Times

10 Aug 2024, New Delhi

Japanese apparel major Uniqlo’s sales growth in India slipped by more than half to a still-strong 32% last fiscal year while its net profit expanded by 25%.

The Indian unit of Asia’s biggest clothing brand posted a net profit of ₹85.1 crore for the year ended March 2024 with net revenues of ₹824 crore, according to its latest filing with the Registrar of Companies (RoC). Uniqlo India had posted a profit of ₹68.1 crore with sales of ₹625 crore in the previous year. Its on-year revenue growth was 69% in FY23 and 64% in FY22.

Uniqlo opened its first door in the country in September 2019, but lockdowns and other constraints during the Covid-19 pandemic delayed its store expansion plans. At present, it has about 13 outlets in the country. Overall retail sales growth rate across segments such as apparel, footwear and quick service restaurants (QSR) fell year-on-year every month in FY24, reflecting comparatively weaker consumer sentiment.

Last fiscal’s comparatively slower 4-7% growth rate sustained this year as well, with May and June seeing a 3% and 5% rise each, Retailers Association of India (RAI) recently said after a survey of top 100 retailers.

“The market was sluggish for the industry as a whole last year, and that will reflect in practice every brand P&L, whether Indian or international,” said Devangshu Dutta, chief executive of retail sector consultancy Third Eyesight. “However, any brand that is committed to the Indian market as a strategic market for its future growth will take the ups and downs in its stride,” he said.

“Uniqlo’s expansion plans now include store sizes that would be smaller both in the cities it is already present in and in newer cities, which should help it tap into the demand at operating costs that are appropriate to each location,” Dutta said. Inditex Trent, Spanish fast-fashion major Zara’s joint venture with Tata that runs 23 stores in the country, saw its revenue rise 8% to ₹2,775 crore last fiscal, significantly down from 40% growth a year earlier, according to Trent’s annual report. Its net profit fell 8% on year to ₹244 crore.

Over the past decade, global brands Zara and H&M have become market leaders in the fast fashion segment in India.

Uniqlo has said India is one of the most priority markets where consumers are increasingly shifting from ‘fast fashion’ to long-lasting essentials and functional wear. As the world’s second most-populated country, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing.

Uniqlo is globally popular for functional basics like T-shirts, jeans and woollen wear, unlike fast-fashion rivals which are associated with designs that move quickly from the catwalk to the showroom.

(Published in Economic Times)

admin

August 28, 2023

Viveat Susan Pinto, Financial Express

August 28, 2023

Coffee Day Global, which operates the Cafe Coffee Day (CCD) chain, has been given a temporary relief against bankruptcy proceedings initiated by lender IndusInd Bank last month. The Chennai bench of the National Company Law Tribunal (NCLAT) last week halted admission of IndusInd Bank’s plea against Coffee Day Global, a subsidiary of the listed Coffee Day Enterprises (CDEL), by the NCLT Bengaluru, till September 20.

What this means for CCD is that it get some more time at a time when it has swung into the black after struggling for the last few years, since the tragic demise of its founder VG Siddhartha in 2019. Coffee Day Global posted a net profit of Rs 24.57 crore for the June quarter of 2023-24 (FY24) versus a net loss of Rs 11.73 crore reported in the same period last year.

Revenue from operations stood at Rs 223.20 crore in the quarter under review, a growth of nearly 18% versus the year-ago period, CDEL results for Coffee Day Global showed.

More importantly, CCD outlets are down to 467 in the June quarter of FY24 from a peak of 1,752 stores in FY19, indicating that the company is shutting down unprofitable operations as it looks to manage its debt and other expenses. Group debt is down to Rs 1,711 crore, according to its latest annual report for FY23, versus Rs 7,214 crore reported in FY19.

“While the coffee retail market in India is growing, in CCD‘s case the need to downsize has to do with internal issues. Sometimes a smaller footprint just helps to manage operations better especially when you are dealing with larger problems such as a debt overhang,” says Devangshu Dutta, chief executive officer of retail consultancy Third Eyesight.

CCD’s financial health is critical for CDEL, which derives close to 94% of its group turnover from the coffee retail business, according to its FY23 annual report. In FY22, the contribution of the coffee retail business to group turnover was 85%. Losses of Coffee Day Global in FY23 narrowed to Rs 69.62 crore from Rs 112.48 crore in FY22. In FY19, the company had a net profit of Rs 10 crore.

Apart from cafes, CCD also has kiosks and vending machines installed in corporate offices, institutions and business hubs. While the number of kiosks has fallen over the last few years and is at around 265 now from a peak of 537 in FY19, the number of vending machines have been growing after briefly slowing down over the last few years. From a peak of 58,697 crore in FY20, it is now at 50,870 in number, the company’s latest results show.

CCD is also expected to fight the insolvency proceedings against it aggressively, according to industry sources. IndusInd Bank has claimed that Coffee Day Global defaulted on a loan of Rs 94 crore, which occurred on February 28, 2020. The company has disputed this in court.

(Published in Financial Express)

admin

February 21, 2016

![]() Shinmin

Bali, Financial Express

Shinmin

Bali, Financial Express

![]() Mumbai,

21 February 2016

Mumbai,

21 February 2016

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

Having

created quite a stir at the time of their launch, hyperlocal companies

are now witnessing a dampened mood. While several have folded

up operations in some cities, others have downsized staff, tweaked

the services they offer and even made alterations to their business

models. A recent example is Grofers shutting down operations in

Bhopal, Bhubaneswar, Coimbatore, Kochi, Ludhiana, Mysuru, Nashik,

Rajkot and Visakhapatnam.

TinyOwl last year was in the news for a poorly-handled downsizing

operation in Pune, with a dramatic hostage situation involving

its co-founder Gaurav Choudhary. PepperTap also recently shut

down operations in six cities.

Ironically, giants like Amazon have not only aggressively entered

the hyperlocal space, they are building on it. Amazon is currently

offering the service in Bengaluru, Amazon Now, after running a

pilot project, Kirana Now, in 2015.

The investor sentiment in India is also on a decline, as was

reported earlier this year. Investments by venture capitalists

have dropped from $2.12 billion (October-December 2014) to $1.15

billion (October-December 2015), according to a report by CB Insights

and KPMG International. This leaves an even shorter window of

opportunity for players to retain investor interest.

Albinder Dhindsa, co-founder, Grofers, states that differing

levels of technology literacy among the majority of merchants

and consumer adaptation to the online platform are concern areas

for the company. In 2016, the company is looking to bring over

one lakh merchants aboard and ensure that turnaround time stays

under an hour. Grofers delivers more than 35,000 orders per day

on average. In Q4 2015, the firm acquired teams of SpoonJoy and

Townrush to bring dynamic learning to the table.

For Swiggy’s co-founder Nandan Reddy, the focus is currently

to grow the market, while catering to a wide demographic of consumers.

He admits that in the early stages, the brand had trouble educating

even its partners. Furthermore, operating a delivery fleet in

an on-demand service offering sub-40 minute deliveries is a challenging

task, given that there are at least 15 points of failure in an

average order. Swiggy currently owns a delivery fleet of 3,800

delivery executives. The brand’s repeat consumers contribute

to over 80% of orders.

Debadutta Upadhyaya, co-founder, Timesaverz, says some of the

major challenges in a hyperlocal market are optimum resource utilisation

and matching locations, price points, and other specific requirements

to customer needs. Timesaverz currently has a service range spread

across 40 categories, aided by a network of over 2,500 service

partners across five metros. Its revenue model is commission based,

where 80% of earnings from consumers are shared with service partners.

Vinod Murali, MD, Innoven Capital, points out that as the hyperlocal

industry is in its nascent stages, it needs a fair amount of time

to grow. “One aspect to keep in mind is that a large sized

equity cheque does not imply that a company has achieved operational

maturity or robust business metrics, especially in this segment,”

he notes.

Given the recent consolidation in this category, the survivors

have the opportunity and time to focus on improving unit economics

and demonstrate that their businesses are viable and valuable.

Devangshu Dutta, CEO, Third Eyesight, is of the opinion that

hyperlocals make the mistake of borrowing business models and

terminologies from Silicon Valley, without adequately understanding

the real context of the Indian market. “Is there an existing

or even potential demand for the service claimed to be provided?

Or are you just going to introduce an intermediary and an additional

link in the chain, with additional costs and unnecessary administration

involved?” he asks.

(Published in Financial Express)