admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

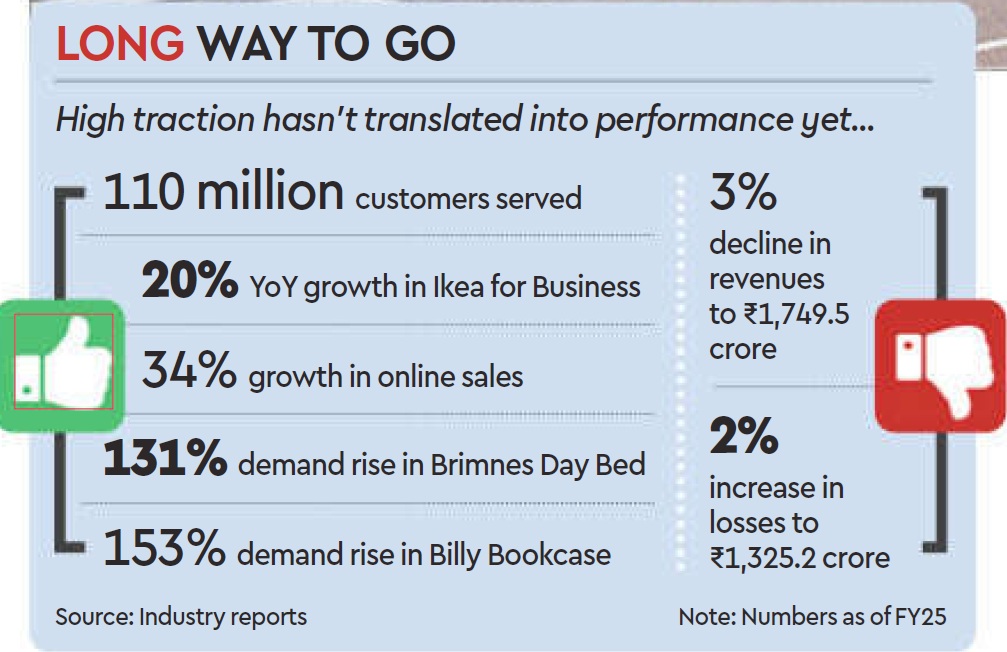

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

May 23, 2025

By Kunal Purohit and Ananya Bhattacharya, Rest of World

Mumbai, India, 23 May 2025

Online retail continues to elude India’s richest man.

The Shein India app, launched by Mukesh Ambani’s Reliance Retail in partnership with the Chinese fast-fashion giant, has struggled to gain traction in a market where Amazon and Walmart have been fighting neck-to-neck for nearly a decade. Downloads for Shein India nosedived from 50,000 a day shortly after its launch in early February to 3,311 in early April, according to AppMagic, a U.S.-based app performance tracker.

In April, when U.S. tariffs hit China, the app saw renewed interest as it was in the news, but experts are unclear on whether this growth is sustainable.

“Unlike earlier times, now … [the] market is saturated with multiple options and offers, and user interest can quickly dwindle,” Yugal Joshi, partner at global research firm Everest Group, told Rest of World.

Kushal Bhatnagar of Indian consulting firm Redseer, however, sees the late-April spike as a healthy sign, given that Reliance has yet to run paid marketing campaigns for Shein.

Reliance Retail declined to respond to Rest of World’s queries about its partnership with Shein.

Reliance launched Shein for India five years after the original Shein app was banned in the country over border tensions with China. But the Shein that has returned is entirely separate from Shein’s global platform: Rather than selling made-in-China clothes and accessories directly to consumers, Shein now operates as a technology partner, while Reliance Retail handles the heavy lifting — from sourcing and manufacturing to distribution. All consumer data is managed by the Indian company.

The partnership is part of Ambani’s broader effort to overhaul his retail business, whose valuation fell to $50 billion in 2025 from $125 billion in 2022. Although the company has made a push into digital platforms like JioMart, Ajio, and most recently Shein India, the bulk of its retail revenue still comes from its 18,000 physical stores.

Lagging behind Amazon and Walmart-backed Flipkart, which together control nearly 60% of India’s e-commerce market, Reliance has spent years trying to break into the sector. Between 2020 and 2025, Ambani’s group acquired majority stakes in companies spanning digital services, online pharmaceuticals, and quick commerce. But the investments have yet to position Reliance as a serious challenger to Amazon and Flipkart.

Analysts say the Indian behemoth hopes to leverage Shein’s artificial intelligence-powered trendspotting and automated inventory systems to pursue an ambitious goal: capturing a major share of India’s e-commerce market, projected to hit $345 billion by 2030.

According to Kaustav Sengupta, director of insights at VisionNxt, an Indian government-funded initiative that uses AI to forecast fashion trends, such a model is likely to make good use of Reliance’s humongous customer data sets: more than 476 million subscribers for its Jio telecom brand, 300 million users for e-commerce platform JioMart, and 452 million subscribers for its news and entertainment portfolio, consisting of 63 channels, a streaming service, and digital news outlets.

“With these data points, Reliance wants to now sell fashion products, so all it needs is a system where it can feed all these data points,” Sengupta told Rest of World. He said the model would be able to predict best-selling products and suggest the right prices for them.

The original Shein app uses AI-driven models for intelligent warehousing and to spot customer trends before manufacturing a new product. It scales the manufacturing up or tweaks the designs based on the feedback. At any given time, the Shein website has a catalogue of more than 600,000 items. Its Indian iteration does not match up, according to reviews on the Google Play store. Several customer reviews for Reliance’s Shein app are critical of higher prices and reduced options. The app’s rating hovered at 2 out of 5 until February; in May, it climbed to 4.4, but reviews were still a mixed bag.

Reviews of the Indian app highlight the disparity with Shein’s global version, criticizing higher prices and a reduced selection of categories and styles.

As of April 25, Reliance Retail said only 12,000 products were live on Shein India, a stark contrast to the 600,000 items available on Shein’s global platforms. While Shein is reportedly set to debut on the London Stock Exchange this year, Ambani’s years-old promise to take Reliance Retail public remains unfulfilled.

Reliance Retail, which accounts for around 30% of the conglomerate’s overall business, is facing a slowdown in annual growth. Its sales rose just 7.9% in the fiscal year ending March 2025, down from 17.8% the previous year. Meanwhile, shares of rival Tata Group’s retail and fashion arm, Trent, have soared by 133%.

“Reliance would have looked at reviving that momentum and riding on it, while for Shein, adding India back on its portfolio of markets could be a plus point before its proposed public listing,” Devangshu Dutta, founder of Third Eyesight, a brand management consultancy that has worked with various global e-commerce brands including Ikea, told Rest of World.

A Reliance Retail official privy to information about its fast fashion expansion plans told Rest of World the partnership with Shein also hinges on global manufacturing ambitions as the Chinese company is trying to “source its products from other countries like India” to meet the “additional demand that is coming from newer markets.” Reliance Retail has tapped a network of small and midsize Indian manufacturers to locally source products, and its subsidiary Nextgen Fast Fashion Limited is leading the charge. “We need to first scale up our domestic manufacturing, before our partnership starts manufacturing for global markets. Let us see how that goes, first,” the official said, requesting anonymity as he is not authorized to share this information publicly.

India’s Gen Z population is at 377 million and counting, and their spending power is set to surpass $2 trillion by 2035, according to a 2024 report by Boston Consulting Group. Every fast-fashion retailer wants to capture this market, but it “is very new even for Reliance,” Rimjim Deka, founder of Indian fast-fashion platform Littlebox, told Rest of World.

Deka said smaller brands like hers “just see [a trend] and implement it,” which could take a large conglomerate months to do, by which time the trend may have lost relevance.

Reliance’s previous attempts to attract young shoppers with clothing brands like Foundry and Yousta failed to find much success. Anandita Bhuyan, who works in trend forecasting and product creation for fast-fashion clients like H&M and Myntra, told Rest of World the company has struggled to effectively leverage consumer data and target India’s youth.

According to the Reliance Retail official, the company is confident that if “there are 10 existing brands, the 11th brand will also get picked up as long as there is value and there is fashion.”

“Shein already has a recall among the youth. It gives us yet another brand in our portfolio through which we can cater to the youth,” the official said.

Shein was built in China on the back of more than 5,400 micro manufacturers — a scattered and loosely organized network of small and midsize factories.

In January this year, on a visit to China, Deka met with manufacturers working for Shein and Temu. On the outskirts of Guangzhou, Deka saw factories set up in areas that appeared residential, with “women sitting inside houses” making clothes.

“The tech is built in a way that somebody sitting there is able to see that, okay, next 15 days or next one month, how much I should be making … that is the kind of integration they have done,” Deka said.

Deka told Rest of World this model is easier to replicate at a smaller scale. “Me, coming from [the] supply chain industry, I understand that it is much easier for a brand like us because we are at a very smaller scale. We can still go to those people, we can still build it in a very unorganized way and then pull it off,” she said. Her company’s annual net revenue is 750 million Indian rupees ($8.6 million).

“[But] somebody like Reliance, they just cannot go haphazard here. … It has to be always organized,” Deka said.

Shein moved its headquarters to Singapore sometime between late 2021 and early 2022, a strategic departure to distance itself from its Chinese origins and facilitate hassle-free international expansion amid the U.S.-China trade war.

India is part of Shein’s wider strategy to diversify its supply chain — one that also includes a newly leased warehouse near Ho Chi Minh City in Vietnam, and efforts to establish alternative manufacturing hubs in Brazil and Turkey.

But in India, Reliance needs Shein as much as Shein needs Reliance for its global pivot. According to Bloomberg, Reliance Retail is focusing on creating leaner operations to weather a wider consumption slump in the Indian economy.

“It remains to be seen whether the Reliance-Shein combine can deliver on the brand’s promise with a wide range of products, fast and on-trend,” Dutta said. “In the years that Shein has been absent, the Indian market has evolved further, competition has intensified, and past goodwill is not enough to provide sales momentum.”

Kunal Purohit is a freelance journalist based in Mumbai, India.

Ananya Bhattacharya is a reporter for Rest of World covering South Asia’s tech scene. She is based in Mumbai, India.

(Published in Rest of World)

admin

February 23, 2025

Chitra Narayanan, BusinessLine

New Delhi, 23 February 2025

India’s formidable array of craft traditions got full play at the just concluded Bharat Tex 2025, the mega textile trade show in New Delhi that showcased the best of Indian weaves to the world. But if there was one theme that dominated this year’s textile extravaganza, aimed at generating more exports, it was the focus on zero-waste fashions and upcycling. Everywhere the eye could see were standees and gigantic posters pushing the message of conscious consumption and sustainability — be it regenerative cotton, innovative models of textile waste collection, or eco-friendly fibres.

Taking centre stage at one of the halls at Bharat Mandapam, the venue, was a section that showcased age-old traditional arts like rafugari (creative darning or artistic mending), patchwork quilts and toys, and chindi durries (the art of weaving rugs and carpets with waste).

Juxtaposed against these ethnic ways of upcycling waste were the modern works of startups that rose to the textile ministry’s grand innovation challenge to work with discarded materials. From microbial dyes that are non-polluting to flowing fashionable lehengas created out of textile waste, the startups showed that a lot can be done in this area. The ministry had challenges in three more segments — jute, silk and wool.

Some takeaways from a walk-through of the textile trade show:

Closing the loop

The fashion and textile industry generates enormous waste. How to cut down on this was a subject of much deliberation and showcases. There were a lot of good ideas on display, showing that a fair amount of work has been done with fibres (bamboo, banana, flax), as well as creativity and ingenuity in weaves and finished garments.

As Devangshu Dutta, Chief Executive of the consultancy Third Eyesight, points out, due credit must be given for the good work going into generating solutions that will reduce waste, be it textiles that are reprocessed and reused as yarn, or refashioned garments or reloved apparel. But, as he adds, on the other hand we have brands that are constantly looking to grow their business and there is a race to the bottom in terms of price. The relaunch of fast fashion retailer Shein in India is sending conflicting signals. “The basic engine is pumping out more and more products, and that has to be tackled,” he says, pointing to the competing forces at work.

The source of hope, he says, is the fact that the young are a bit more conservative about how they consume and what they consume.

Sandip Ghose, CEO of MP Birla Group, which has one of the oldest jute companies in India, was among the visitors at Bharat Tex. “As an industry insider, what I found good at Bharat Tex was that quite a bit of research seems to be on, both for finished fabric and for weaving. There was a lot of work on making jute look aesthetic. There were some vanity projects like tea leaves packed in jute bags. But the challenge is in two areas — commercialisation, and scaling up of these ideas,” he says.

He rues that the jute sector has not taken advantage of the production-linked incentive scheme at a time when the world is looking for eco-friendly and biodegradable textiles. “A tripartite partnership between the Centre (Niti Aayog and textile ministry), State government, and industry would address the issue of industry’s dependence on subsidies, labour issues and exports,” he says, adding that if India is looking at textiles as a major export area, jute is an option that has been missed.

Spinning into luxury

A clear trend evident from a tour of some of the apparel and home textile pavilions is the move towards premiumisation, similar to what is visible in other sectors, noticeably FMCG.

Talking to the manufacturers, especially those focused on the domestic market, the story one heard was that consumption had slowed in the mass segment, but was reassuringly strong in the premium segment.

Several players were also moving into the luxury and uber luxury segments. Both myTrident and Welspun had striking luxury collections.

Another trend visible in the home textiles section was the use of celebrity designers — myTrident’s eye-catching collection by resort-wear designers Shivan-Narresh; and Welspun’s beautiful sets from Kate Shand and Payal Singhal.

“When the economy suffers, it is the poor and middle class who cut down. There is no pressure to reduce consumption at the upper levels, and companies will try to tap into demand that is recession-proof,” says Dutta, explaining the push towards luxury by textile manufacturers.

New trade routes?

Export houses seemed reasonably happy with the buyer interest. Some mentioned that it was interesting to see buyers from Russia at the fair. However, for those supplying to US entities and Western Europe, the buyer interest from Russia may not translate into deals, given the risk of sanctions they could face.

To sum up, it was a fairly good showcase of India’s textile prowess to the world, but whether it will ring in more export orders is debatable as many of the problems and challenges the sector faces were swept under the carpet.

(Published in BusinessLine)

admin

January 5, 2024

Sagar Malviya, Economic Times

January 5, 2024

Top global apparel and fast fashion brands appear to have struck a strong chord with young customers, racking up sales growth of anywhere between 40% and 60% in FY23, bucking the trend in a market where the overall demand for discretionary products slowed down.

For instance, Swedish fashion retailer H&M and rival Zara reported a 40% increase in its topline while Japanese brand Uniqlo saw a 60% jump in sales. American denim maker Levi Strauss and British brand Marks & Spencer posted a 54% increase, latest filings with the Registrar of Companies showed. Dubai-based department store Lifestyle International, too, saw a 46% jump in revenues on a large base. These brands garnered combined annual revenues of nearly $2.6 billion, more than double compared to FY21 when it was $1.1 billion all put together.

“With consumers getting brand conscious, global brands have a natural advantage. There is a distinct aspirational momentum for international brands that carries them through. Also they can sustain having unsold inventory and discounting better than smaller peers,” said Devangshu Dutta, founder of Third Eyesight, a strategy consulting firm. “Also, these brands have not yet reached saturation point in terms of network and hence can invest further to widen their reach.”

The revenue surge was also led by brands’ shifting focus on ecommerce, which now accounts for more than a quarter of their sales, even as they face intensify competition from both local and global rivals in an increasingly crowded market where web-commerce firms continue to offer steep discounts. Over the past two years, sales growth for most retailers have been price-led, reversing the historic trend when volumes or actual demand drove a bulk of the sales.

The fashion retail segment has been struggling with a demand slowdown since January last year due to inflationary headwinds. The overall retail growth slowed down to 6% in both March and April, increasing marginally to 9% in August and September before falling slightly to 7% in October and November, according to the Retailers Association of India.

“Spends are shifting to experience, holidays and big ticket purchases such as cars. Stronger retailers which had the right product to price proposition works for consumers who are not necessarily looking at brands from global and local lens. What helped our sales was product rationalisation, renovation of stores as well as our value proposition,” said Manish Kapoor, managing director at Pepe Jeans that clocked 54% growth to Rs560 crore in FY23. “The current fiscal has been muted and we expect election spending and improved sentiment to drive recovery next fiscal.

As the world’s second most-populated country, India is an attractive market for aspirational apparel brands as rising disposable incomes cause the consuming base of the pyramid to broaden further. “The Indian economy is on course to be among the top economies in the world. The key factors driving the India consumption story include a large proportion of young population, rising urbanization, growing affluence, increasing discretionary spending and deeper penetration of digital,” said Levi Strauss in its latest annual report.

Last year Levi’s said India is now the largest market for them within Asia and sixth largest globally while M&S said it is opening a store every month in India, already its largest international market outside home in terms of store network.

(Published in Economic Times)

admin

June 29, 2023

Dia Rekhi & Faizan Haidar, Economic Times

New Delhi, June 29, 2023

Fast Retailing, the parent company of Uniqlo, is looking to set up a significant manufacturing presence in India through about 20 ‘production partners’, multiple people aware of the development told ET.

One of the world’s most valuable clothing retailers, Uniqlo already has a cluster of production partners in India and is looking to expand this network through a significantly large investment, they said without sharing any estimated amount.

“The investment amount will be significant because Uniqlo is serious about India and views it as an important market,” one of the persons said. “Unlike the existing facilities in India, which cater more towards exports, the production partners that Uniqlo will bring to India will be specifically meant for the domestic market.”

One of the company’s production partners that ET spoke to confirmed that their current mandate is to produce only for exports.

Uniqlo, which is Asia’s biggest clothing brand, had said India is one of the top priority markets for them where consumers are increasingly shifting from ‘fast-fashion’ to long-lasting essentials and functional wear.

The company’s ambitions for India are considerable with its CEO Tadashi Yanai indicating that he wants Uniqlo to become the “best-selling retailer in India”.

The Japanese brand opened its first door in September 2019, but stringent lockdown measures announced to contain the outbreak of the pandemic in March 2020 delayed the expansion plan.

The brand is now planning to enter Mumbai and Bangalore. It has already opened stores in Lucknow and Chandigarh after Delhi.

Uniqlo does not own any factories. Instead, it outsources production of almost all its products to factories outside Japan.

As per a report titled ‘The Uniqlo case: fast retailing recipe for attaining market leadership position in casual clothing’, this model allows Uniqlo to keep its breakeven point low and improve return on investment.

“As we expand our global sales, we continue to grow our partner factory network in countries like Vietnam, Bangladesh, Indonesia, and India,” the company has stated on its website.

As per its list of garment factories, as on March 1, 2023, Uniqlo has 227 factories in China, 54 in Vietnam, 33 in Bangladesh, 13 in Indonesia, and 16 factories in India and Japan among several other locations.

As the world’s second most-populated country, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing.

Over the past decade, global brands Zara and H&M became market leaders in the fast fashion segment in India.

“For global brands, India should be one of the most logical sourcing hubs given its large vertically integrated manufacturing sector on the one hand and the large, growing domestic market driving demand on the other hand,” Devangshu Dutta, founder of retail consulting firm Third Eyesight, told ET. “However, its weight in the sourcing baskets has historically been low due to several reasons, in spite of China being visible for decades to the management teams of brands and retailers as a concentrated sourcing risk,” he said.

Uniqlo’s existing production partners in the country include Shahi Exports, Brandix Lanka, Tangerine Design, Maral Overseas, Shingora Textiles, Silver Spark Apparel, SM Lulla Industries Worldwide and Penguin Apparels.

As per Fast Retailing’s first-half results, the company said its revenue was 1.4672 trillion yen, or around $10.2 billion, and that its operating profit had risen to 220.2 billion yen ($1.53 billion), bolstered by strong performances from operations in several regions, including India where it said it generated significant increases in both revenue and profit.

With regard to Uniqlo International, in particular, it said revenue stood at 755.2 billion yen ($5.25 billion), while operating profit was 122.6 billion yen ($852.93 million).

The company said regions like India “reported significant revenue and profit gains as they enter a full-fledged growth phase”.

(Published in Economic Times)