admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

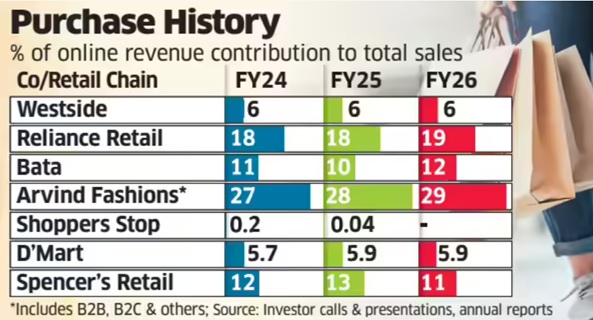

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

September 5, 2025

Shalinee Mishra, Exchange4Media

5 September 2025

Retailers in India are waking up to a hard truth: customer acquisition can no longer ride on advertising alone. Digital ad spends grew by 14-17% in 2024, touching nearly ₹50,000 crore (as per Pitch Madison report) and accounting for 46% of India’s total ad market. But with customer acquisition costs (CAC) rising 30-35% year-on-year and consumer attention fragmented across platforms, the ad-first growth engine is showing strain. What is emerging instead is an ecosystem where content in the form of video, celebrity-led storytelling, or creator-driven engagement is becoming the direct funnel to commerce.

Flipkart for instance is building influencer production hubs and embedding shoppable videos, Myntra has rolled out its video-first Glamstream, and Amazon has long blurred the line between streaming and shopping through Prime Video and Fire TV. From short videos to celebrity gossip, from beauty blogs to shoppable livestreams, e-commerce giants are no longer just marketplaces; they are evolving into media houses and the trend is only growing.

According to Mindshare’s latest Content Trend Report, India’s branded content marketing industry is now worth ₹10,000 crore, growing at nearly 20% annually, with video formats making up almost half of all spends.

India already has over 270 million online shoppers, a number that Bain projects will rise to 350 million by 2027, making it the world’s second largest e-retail user base. That scale is creating fertile ground for shoppable video and live commerce to take off.

Globally, branded content spend is projected to cross $500 bn by 2027. As per PwC estimates, India’s share is still <2% but among the fastest growing.

Video commerce today largely follows two prominent models. The first is driven by social platforms such as YouTube, Instagram, and Facebook, where shoppable posts allow users to move directly from content to purchase. The second is led by e-commerce platforms like Amazon, Myntra, Nykaa, and Flipkart and others which have added video sections to create immersive shopping experiences within their apps.

Within this, live commerce has emerged as a high-potential format. Meesho and Flipkart, for example, are leading the charge with 2-3% conversion rates, generating an estimated $150-200 million in GMV during festive 2024. Events like Flipkart’s Big Billion Days show how timed livestreams can capture active, purchase-ready audiences.

Meanwhile, influencer-led short videos are driving conversion rates as high as 63%, with beauty and personal care (BPC) and food & beverages (F&B) among the top categories benefiting from this shift. Redseer projects India’s live commerce market could touch $4-5 bn GMV by 2027, up from less than $300 mn today. This surge in shoppable video and live commerce is only the surface of a deeper structural change, one where content itself is becoming the moat that protects brands from rising ad costs, fragmented attention, and fickle consumer loyalty.

Beyond ads: Why content has become retail’s strongest defence

Chirag Taneja, co-founder of e-commerce enablement company GoKwik, framed the trend as a fundamental shift in ownership.

“It’s not just about enhancing top-of-funnel reach, it’s about owning demand, connection, and the touchpoint with end shoppers. For years, brands relied on ads to bring traffic. But acquisition costs have been rising, attention is fragmented, and privacy shifts have made targeting difficult. That’s why content is now the moat. When companies acquire content firms, they’re not just buying eyeballs, they’re securing access to communities that trust and engage with that content.”

According to him, content is collapsing the traditional funnel. “One short video or livestream can take a consumer from awareness to purchase in under a minute. That’s why we see D2C brands treating content as a compounding asset, not just an expense,” he added.

Devangshu Dutta, founder and CEO of management consulting firm Third Eyesight, echoed the sentiment.

“Large companies are buying or partnering with content-driven platforms to capture attention beyond transactional touch points. Short video, regional language content, and influencer-driven discovery are embedding commerce within entertainment. If you want to sell more than a commodity, storytelling is critical. Content builds credibility, differentiation, and trust in a cluttered and price-sensitive market.”

Flipkart bets big on media and creators

The shift is already reshaping strategy at India’s biggest retailers, and Flipkart has moved fastest. Its move to acquire a majority stake in Pinkvilla, a platform built on entertainment and celebrity news signals a clear push to deepen ties with Gen Z and millennials, a cohort that consumes content first and shops later.

“Our acquisition of a majority stake in Pinkvilla is a critical step in our mission to deepen our engagement with Gen Z. Pinkvilla’s robust content IPs and strong connection with its loyal audience base are assets that will accelerate our efforts to leverage content as a key driver of growth,” said Ravi Iyer, Senior Vice President, Corporate at Flipkart.

Flipkart in the last year has exited investments in companies like Aditya Birla Fashion & Retail, where it sold its 7.5% stake in the owner of Pantaloons, Van Heusen, Louis Philippe and Forever 21, as well as BlackBuck, the trucking marketplace that powers India’s mid-mile logistics.

At the same time, the company has doubled down on content and creators. Its Pinkvilla acquisition gives it access to a platform reaching over 60 million monthly users, while in-house features like Flipkart Feed already clock 5–6 million daily video views, highlighting how commerce and content are converging at scale.

Alongside this, Flipkart has launched Creator Cities in Mumbai, Bengaluru and Gurgaon, production hubs designed for influencers to shoot and scale shoppable content.

It has also introduced Flipkart Feed, a TikTok-style vertical video feature embedded in its app, offering bite-sized, influencer-led, fully shoppable videos. Myntra, its fashion arm, has developed Glamstream, with more than 500 hours of video-first shopping content across music, beauty, travel and weddings, featuring stars like Badshah, Tabu, Zeenat Aman and Vijay Deverakonda.

Flipkart has also partnered with YouTube Shopping, allowing creators with over 10,000 subscribers to tag Flipkart products in videos, Shorts and livestreams, enabling viewers to buy directly while creators earn commissions.

Amazon’s head start in content-commerce convergence Flipkart is not alone. Its biggest rival Amazon has long understood this convergence. Through Prime Video and its original programming slate, Amazon has built an entertainment ecosystem that doubles as a commerce funnel. The shows and films on Prime do not merely entertain; they drive shopping behaviour, influence trends, and lock audiences into Amazon’s larger universe of services. With Fire TV and Alexa integrations, the company has blurred the line between watching and buying, a model others are now racing to replicate.

D2C brands treat content as growth engine

Closer home, the Good Glamm Group, now closed, had pioneered a content-led commerce ecosystem in beauty and personal care. Through acquisitions like ScoopWhoop and MissMalini Entertainment, the group stitched together a portfolio where content platforms brought in audiences, who were then nudged towards its direct-to-consumer brands.

This “editorial-to-checkout” model demonstrated how cultural capital could be translated into purchase pathways. Alibaba has taken the strategy global. With stakes in Youku, a leading video-streaming platform, and Alibaba Pictures, the e-commerce titan integrates entertainment with retail operations. Taobao Live has shown how livestream shopping can dominate consumer behavior, particularly inAsia, creating billion-dollar shopping events entirely dependent on

entertainment-driven discovery.

Shopify, meanwhile, has invested in tools that empower merchants to become content creators themselves. Its partnerships with agencies like Sanity and investments in platforms such as Billo reflect a clear intent to enable retailers to embed storytelling, gamification, and user-generated content into their selling journey. Unlike large marketplaces, Shopify’s vision is not to own the content but to democratize access to it for small and mid-sized businesses.

From content to commerce

This content includes newsletters, creator partnerships, branded podcasts, and niche communities on social media. The idea, as industry experts note, is to treat content as an asset that compounds, not just as a cost.

Unlike ads, content continues to generate discovery and engagement long after it’s published. That’s why more D2C brands are making content central to their growth strategies.

Several big names are experimenting in this space. Durex, Plum, Mother Dairy, and HDFC Bank have launched their own podcasts where celebrities share stories along their brand journey. Founder-led podcasts too are on the rise on YouTube, with voices like Nitin Kamath and Deepinder Goyal drawing large audiences in India.

The big question, however, is whether content consumption can effectively be converted into product discovery and purchase pathways. “It’s already happening at scale,” said Taneja. “Content is redefining every aspect of the traditional funnel. In the past, you had awareness at the top, intent in the middle, and purchase at the bottom. Today, one short video or live stream can take a consumer through that entire journey in under a minute.

“From a D2C lens, this convergence is even more critical. D2C brands thrive on agility, the ability to turn trends, storytelling, and community engagement directly into sales. Platforms like Instagram, YouTube, TikTok, and even WhatsApp have embedded shoppable features, which means the content is no longer just ‘top-of-funnel.’ It’s the storefront. But the magic lies in authenticity and design. Consumers don’t want to feel ‘sold to’, they want to feel entertained, inspired, or educated. If the content does that well, conversion becomes a natural byproduct. For example, an athleisure brand showing a workout routine isn’t just demonstrating leggings, it’s giving value. The leggings purchase becomes an easy next step, not a forced pitch.”

The big question: Will content sustain sales at scale?

Taneja further reveals how content is driving sales and long-term growth. “The smartest brands, especially in D2C, have realized that high-quality

content is their most defensible growth engine. Performance marketing will continue to play a role, but the real long-term moat is the kind of content that builds relationships, trust, and recall. Consumers today are spoiled for choice. They don’t buy just products, they buy stories, values, and communities.

“High-quality content allows a brand to consistently show up in ways that feel relevant and credible. And from a business lens, it directly impacts unit economics: it reduces CAC because organic discovery compounds over time, improves LTV because content nurtures loyalty and repeat purchases, and builds resilience because brands with strong content ecosystems are less dependent on fluctuating ad platforms.”

The D2C ecosystem in India is already proving this point. Beauty and personal care brands now run editorial-led platforms alongside commerce, while fashion labels thrive on creator collaborations and storytelling-driven product drops. Their growth is not accidental but built on content strategies that treat every piece not just as a post, but as a business driver.

As an enabler, Taneja adds, the results are visible across platforms. “Brands that invest in content see better conversions on our checkout stack, lower cart drops, and stronger repeat cohorts. Content doesn’t just spark sales it sustains them.”

For all the optimism, the test for content-driven commerce will lie in scale and sustainability. Rising conversions in beauty, fashion, and food show the model works, but questions remain on whether every category can replicate that success, or whether consumers will tire of content-heavy shopping pitches.

(Published in Exchange4Media)

admin

July 28, 2024

Writankar Mukherjee, Economic Times

Kolkata, 28 July 2024

Top retail chains such as Reliance Retail, Shoppers Stop and Spencer’s Retail are facing a prolonged slowdown in consumption, pushing them to exit unprofitable markets, raise debt and control costs.

India’s largest retailer Reliance Retail shuttered 249 stores in the three months ended June. The company is also going slow on expansion, opening 331 new stores in the quarter compared to 470-800 stores opened every quarter in FY22, FY23 and FY24. The closures mean the retail business of Reliance Industries made 82 net new store additions last quarter–the lowest in 15 quarters.

Spencer’s Retail has decided to completely exit North and South India markets by closing 49 stores in the National Capital Region (NCR), Andhra Pradesh and Telangana. The step will erase Rs 490 crore of annual revenue, but the company is hopeful it will improve profitability.

Shoppers Stop chief executive officer Kavindra Mishra told investors last week that it may have to defer a few store openings this fiscal due to regulatory and other issues. The company will also borrow Rs 100 crore for expansion with demand remaining soft.

Meanwhile, V-Mart Retail has closed 22 stores in the first six months of 2024, as per its latest investor presentation.

“Pruning underperforming locations is a natural reaction during times of demand stress,” said Devangshu Dutta, CEO of retail sector consulting firm Third Eyesight.

Pure Economics

“Demand forecasting can never be perfect due to a lag between demand assessment and supply. Retailers now try to do away with underperforming stores at the bottom of the pile quickly. Earlier there were prestige issues in shutting down stores, but now it’s acceptable industry practice and pure economics,” said Third Eyesight’s Dutta.

Analysts say most retailers expanded rapidly after the pandemic, banking on pent-up demand and revenge shopping at the time. With demand turning sluggish, the industry is now being forced to take various steps to sustain operations. At Reliance Retail, net profit rose by a modest 4.6% from a year earlier in the June quarter to Rs 2,549 crore while revenue grew 6.6% to Rs 66,260 crore. It was the slowest pace of revenue growth and came after a 9.8% increase in Q4FY24. Net profit and revenue from operations fell sequentially in the June quarter.

Spencer’s Retail CEO Anuj Singh told analysts on Thursday the 49 stores it is closing make up nearly 22% of revenue, but also Rs 56 crore of losses at the regional Ebitda level in North and South India. “They were a drag on the balance sheet. We will now focus on Uttar Pradesh and the East where there is a sizable consumption opportunity with a 250 million population,” he added.

Singh said the store rationalisation exercise and about 35% headcount reduction at corporate offices will reduce overheads from 8% operating cost to 6.3% of total sales. “We now expect to achieve Ebitda breakeven by March 2025 which will give us the option to raise capital,” he said.

Mishra at Shoppers Stop said demand remained subdued last quarter due to fewer wedding dates, long election season with polling dates on weekend, heatwaves, and high level of cumulative inflation. All these factors combined hit growth and volume recovery, except in value fashion and beauty.

More stores shut than opened

In fact, the sustained demand slowdown saw chains like Pantaloons, Spencer’s Retail and Nature’s Basket close more stores than they opened last fiscal. Retailers like V-Mart Retail, W, Aurelia and Titan Eye+ had a higher rate of store closures than openings in the March quarter.

(Published in Economic Times)

Devangshu Dutta

July 14, 2008

In early-June Big Bazaar (part of Future Group) was reported to have broken off its relationship with Cadbury’s. About 2-3 weeks later the two were reportedly back together. The alleged differences and the apparent solutions have been reported widely, as also the feeling that some issues remain unresolved.

If that reads like something you would find in a celebrity tabloid, you’re probably right. The relationship between brands and large retailers is truly one of the “love-hate” kind. And this case is no different from many other such relationships in various markets around the world. In fact, the Future Group itself is reported to have had similar run-ins with PepsiCo’s FritoLay and GlaxoSmithKline in the past.

I won’t dwell on the various allegations and clarifications about commercial structures and differential pricing in this particular case, since the view from outside isn’t really clear. But it is certainly worth noting that this case is not unique, and thinking about what the future (no pun intended) might hold for brands in markets such as India.

There is no doubt that brands love the scale that large retailers provide them, with the quick access to a large footprint in the market, and the high visibility. On the other hand, as a vendor, they hate the negotiating edge that this scale gives the large retailer. Brand generally rule fragmented retail environments such as India. Large retailers, on the other hand, squeeze out more margins in the form of bulk discounts, placement fees and the like. There’s more: special promotions, differential merchandising and delivery needs…the list of demands seems endless.

On the other side, retailers love brands for the footfall they bring. The brand typically creates a “need to buy” on the consumer’s part, and invests in creating a distinctive proposition which is valuable in a cluttered market. In many cases the brand would have also advertised where it is available. This is all good stuff for the retailer, who then essentially has to make sure that the brand is available and visible in-store to the customer to convert the walk-ins into sales. However, what retailers don’t like is the fact that brands will generally charge a premium of 10-50% over a comparable generic product. In some cases the premium may be so high that the brand product’s price itself is multiples of a generic product’s price.

The retailer-brand partnership is a very powerful one, even from early days. Many consumer brands and branded companies have scaled up significantly with the growth of their retail customers. The US market due to its sheer size and its evolution offers numerous examples including companies such as Levi Strauss, Hanes, Fruit of the Loom and Proctor & Gamble that grew on the back of discounters such as Wal-Mart and K-Mart as well as retailers such as JC Penney, Macy’s and Sears. Similar examples appear from other countries where the modernisation and consolidation of retail have happened over decades along with economic development.

An established brand provides the new retailer credibility, even as the retailer provides the brand new shelf-space. Or the other way around: even a new brand provides value to an established retailer by identifying the market need, developing the product, managing sourcing & production, and establishing the consumer’s interest in the product, while it is the established retailer who provides the much-needed credibility and presence to the new brand.

For most, this remained a happy relationship for a long time even as the retail environment grew and evolved. Retailers focussed on creating shelf-space and managing it, while the brands focussed on creating products and desirability.

However, economic shocks various times and the rise of low-cost imports raised questions in retailers’ minds about the value added by the brand compared to the margin they supposedly made on the higher prices. At the same time, better communication and travel infrastructure as well as falling costs made it easier for retailers to consider approaching factories directly.

Enter private label, the “other” in the love-hate triangle.

Over the last couple of decades, department stores, hypermarkets, grocery stores and even discounters have worked seriously on private label. The opening premise was that you could entice the customer with a lower price (sharing some of the margin earned by direct sourcing), and as long as you gave a comparable product the consumer was happy. Many Indian retailers followed a similar route when they began exploring private label.

The strategy has had a varied degree of success, much of it to do with how the private label has been handled (indifferently in most cases). Recognising this flaw, many retailers around the world have attempted to improve their handling of their private label product development and also presenting it also in a manner (including advertising) similar to a national or an international brand. Some of these retailers’ own labels are now serious brands in their own right even though they are restricted to only one retail chain.

The difference between a “label” and a “brand” is the inherent promise that a brand has built into the name, the repeated experience that the customer has had with the brand that reinforces this promise, and the relationship that develops between the consumer and the brand. All of this requires structuring, nurturing and careful management, and it costs time, effort and money. When the economy and individual incomes are growing, consumers are willing to shell out a little extra for a brand and all that it stands for.

However, brands get into trouble if income and spending perceptions turn downwards, and comparable products are available. The 10+ per cent premium between branded and generic begins to look like an important saving to the customer. Or conversely, due to the growing market more suppliers for the same product appear that the retailer can use as a foil to the branded market leader. With falling import barriers, more diverse contract manufacturing becomes available for sourcing private label merchandise. The scenario becomes particularly grim if the relationship between the brand and the consumer is not old enough to have become lasting – in this case, replacement of the brand with an alternative or a retailer’s own label is truly feasible.

The Indian market, at this time, shows all of the above ingredients. Inflation is making consumers reconsider how and where they spend their money. The growth of the market over the last few years has attracted several companies with alternative products and brands e.g. ITC as a challenger to biscuit-cookie major Britannia as well as to Pepsi’s potato chip brand Lays. Retailers such as the Future Group, Shopper’s Stop and Reliance have actively incorporated imports into their sourcing strategy. In many cases, the brands that most want to be on the modern retailer’s shelves are new to the market, and don’t yet have a strong imprint on the consumer’s mind.

However, at the same time, retailers themselves are still developing the systems and disciplines to manage their relatively new businesses. They are more than fully occupied with rising real estate costs, and managing the front end. If a brand can handle the product and supply side for a reasonable margin, they are more than happy to ride with the brand.

There is place for the branded suppliers in the market, and for them even to lead the market. Even as retailers grow, branded suppliers won’t lie down or die quietly. Many of them (such as Hindustan Unilever) are also actively engaging with smaller retailers, to help them improve their business processes and competitiveness. On the other hand, they are also reconciled to the inevitable growth of modern retailers, and are developing “key account management” functions, parallel distribution processes etc. to cater to the large retailers differently from the rest of the market.

So will brands survive, or will it be the retailer with the muscle of the storefront relegate them to a small portion of the market?

As long as the competitive pressures and economic cycles remain, the relationship between retailers and their branded suppliers will inherently be a tug-of-war for margin.

In either case, whether individual brands or retailers win or lose in the short term, the consumer will hopefully be a beneficiary in terms of better product, more variety and some sanity in terms of prices.

Devangshu Dutta

February 2, 2008

Creating an entrepreneurial ecosystem is absolutely critical to a healthy and vigorous society and economy.

Creating a “democratic” entrepreneurial ecosystem is even more critical to sustaining that health. A democratic entrepreneurial system is like all other democracies – inclusive and widespread – and vital to improving the baseline quality of life.

As we’ve pointed out elsewhere, retailing is not just a fundamentally entrepreneurial business, it also offers up a platform for the birth and growth of other entrepreneurial businesses.

Obviously, big retailers offer a change for companies to scale up faster, once they meet the performance criteria set by the retailers.

The interesting thing is that small retailers offer an even more interesting growth opportunity since, as their own business grows, they grow their supply partners as well.

Countless companies and brands have been launched on the back of the likes of Wal-Mart, Carrefour, Tesco, Marks & Spencer, and in India retailers such as Pantaloon’s and Spencer’s (and even some of the early modern retailers in India that don’t exist anymore).

In view of this, it is wonderful to see 2-9 February 2008 being celebrated as Entrepreneurship Week (on the National Entrepreneurship Network’s website) and also its powerfully worded pledge.