admin

June 12, 2026

Christina Moniz, Financial Express/Brand Wagon

12 June 2026

Legacy luggage brand VIP Industries is shedding some of its old baggage. The company, which manufactures Skybags and Aristocrat along with its flagship VIP range, has gone beyond cringey makeovers solely to attract Gen Z, and has embarked on a transformation journey that leverages its legacy to purvey a fresh range of offerings.

The company is modernising its digital presence and supply chain to catch up with competitors.

Managing director Atul Jain admits that the company has been a bit slow on the e-commerce front. It is reinventing its online store, while also making its products available across other e-commerce channels. “Quick commerce is becoming an important channel since there are several use occasions and segments within the luggage market. For instance, consumers often make last-minute purchases for a weekend trip via quick commerce. School bags and backpacks for kids, also great gifting options, are seeing good demand on these platforms,” he says

The company, which once dominated the ₹16,000 crore organised luggage market in India, saw a bit of a shakeup last year when the Piramal family sold 32% of its stake to a private equity firm. But it continues to be among the top three players in the category with a 29-30% market share. “Luggage plays the role of a traveller’s companion. We are creating designs to fit that role,” says Jain. “For example, our new VIP suitcases have a coffee cup holder and our cabin trolley bag has an easy access compartment for devices like laptops and iPads.”

The transformation goes beyond the product. VIP’s 350 exclusive physical retail touchpoints in the country are being revamped to offer a new customer experience.

Unpacking opportunities

Overits 55 years, VIP has grown from a briefcase brand into Asia’s largest luggage maker, housing labels like Skybags, Aristocrat, and Carlton (premium segment). While VIP is a premium offering targeted at business and travellers, its Aristocrat brand operates in the mass market and the budget-friendly Alfa targets consumers who typically shop in the unbranded segment. Aristocrat and Alfa together contributed upwards of 40% to the company’s revenue in FY25, followed by Skybags (28%) and VIP (20%).

Like many legacy brands, the VIP Industries’ faces the challenge to ia, stay relevant among Gen Z buyers as a plethora of digital-first brands swamp the market. “VIP has lost ground on relevance and desirability to a generation for whom luggage, like sneakers, is an expression of identity. To them, VIP feels like their parents’ brand,” says Nisha Sampath, managing partner, Bright Angles Consulting. D2C players in the category operate in the business of “lifestyle accessories” and not for “luggage” per se, she points out.

With a design-forward approach, incorporating features like compression systems, silent wheels and charging ports, these new-age brands have embedded themselves in travel “culture”, while also being Instagram worthy, say experts.

Jain says Skybags is VIP’s Gen Z focussed brand, which has over 8,20,000 Instagram followers. “We are sharpening our positioning for Skybags in our design, advertising and marketing outreach, especially on social platforms. The brand has a clear differentiation with youthful colours and prints to attract younger consumers,” he adds.

While D2C players have seen notable growth in recent years, they don’t have the kind of trust and brand equity that VIP has cultivated across its brands, nor do they have the scale or revenue that legacy brands have, he says.

Experts believe there is a significant growth opportunity for legacy players given that the unbranded market still accounts for ₹13,000-14,000 crore. The important lever for legacy brands is to clearly demonstrate value beyond price. “The unorganised market competes heavily on affordability, so organised players need to communicate durability, warranty, after-sales service, and consistent quality – areas where they have a strong inherent advantage over unorganised alternatives,” says Praveen Govindu, partner at Deloitte India. He adds that these brands should also invest in advertising and communicate this value to the end consumer.

Not only are the needs different among different consumer groups, competitive pressures are also diverse. “VIP can segment the market more cleanly with its portfolio of brands if it maintains absolute distinction to ensure clear consumer targeting across not just product attributes and pricing, but also communication and channels,” says Devangshu Dutta, CEO, Third Eyesight.

(Published in Financial Express)

admin

June 8, 2026

Arushi Jain, The Times of India

8 June 2026

Their faces have launched many campaigns and brought crores to the film industry. But can they sell a moisturiser as successfully? India’s beauty market is the hottest growth story globally, estimated to reach $40 billion from $23 billion (2026) and eyeing the fourth-largest spot by 2030 (currently at number seven).

Last month, Estée Lauder announced the buyout of Forest Essentials, one of India’s oldest, Ayurveda-based brands. In 2025, Hindustan Unilever acquired five-year-old skin and hair care brand, Minimalist. A 2025 McKinsey & Company x Business of Fashion survey found that 78% of global beauty executives see India as the most promising growth market. Even celebrities have shown up with chequebooks, but fans are no longer buying at face value.

While Hailey Bieber’s Rhode built a cult following through what she calls an “outside of the box” strategy, Deepika Padukone’s 82°E reported a 30% revenue dip in FY25. Nykaa is in talks to acquire a stake in the brand.

India’s consumer has evolved faster than the brands serving them. They are reading labels now, not just recognising famous faces on packaging. Star power, it turns out, only gets you so far.

Fame gets you in the door. Formulation keeps you there

If a celebrity is the invitation to the party, formulation is what keeps the guest at the after-party. Despite India’s celebrity beauty segment crossing an estimated `5,000 crore in GMV in FY24, scale has not translated into customer retention. The initial spike, familiar to anyone who has tracked a celebrity launch, gives way to an uncomfortable question: what brings a customer back?

“Celebrity isn’t necessarily a sustainable brand asset,” says Devangshu Dutta, CEO of retail consultancy Third Eyesight. “While celebrities can act as interest-creators and trial-generators, repeat purchases are built on functional reasons, not imagery alone.”

Founders echo the same reality from the ground. “Honestly, people come back for what works,” says Aashka Goradia Goble, co-founder of RENÉE Cosmetics. “If a product performs well, feels easy to use, is priced right, and becomes part of someone’s everyday routine, they’ll keep reaching for it.”

Price, too, remains a decisive filter. Sunny Leone, founder of StarStruck, says, “In India, price is the main component.” The journey from first purchase to loyalty is driven by habit, and habit, in beauty, is built on results.

Positioning over popularity

The gap between a viral campaign and a repeat purchase is wider than most A-listers realise. Brand guru Harish Bijoor locates the problem in what he calls the “spinal cord” of a brand: a single, clear positioning that holds the entire business together.

Rihanna’s Fenty is inseparable from its commitment to shade inclusivity. Kylie Jenner’s Kylie Cosmetics was built around one obsession: lips. “It is extremely important to understand what you want to be and focus on just one thing and not on everything,” Bijoor says. That clarity is precisely where most Indian celebrity beauty brands are still finding their footing.

The old playbook: launch a brand online, wrap it in the language of “clean” or “natural,” and wait for a global conglomerate to come calling has run its course. Today, strategic buyers and consumers alike want a brand that can stand on its own. The question is no longer whether a celebrity can generate awareness. It is whether the brand they have built can survive them.

What the labels that last have in common

The brands breaking through are doing so quietly and methodically. In a category where fame can spark interest but not always guarantee repeat purchase, Katrina Kaif’s Kay Beauty, launched with Nykaa in 2019, has emerged as one of celebrity beauty’s more consistent success stories.

The main reason is less about star power and more about strategy. “If you contrast Kay Beauty and 82°E (Deepika Padukone’s brand), Kay Beauty has two distinct advantages,” says Dutta. “Firstly, being priced for a much larger audience, and secondly, having the active participation of Nykaa across channels in terms of merchandising and visibility push for the brand.”

Nykaa is candid about what made the difference. “When we co-created Kay Beauty with Katrina, shade ranges and formulations designed for Indian skin tones and climate were severely limited,” a spokesperson shares, adding that the celebrity association “amplified the brand rather than substituted for it.” The strategy appears to have paid off: Kay Beauty is now a ₹500 crore-plus annualised GMV brand, with new launches contributing 21% of revenue as of Q3 FY26.

Why Indian skin demands more than a famous name

For Indian celebrity brands, the challenge is not just performance; it is perception. “Domestically, we see the mentality for buyers is to look at international brands first based on trust, and then try domestic brands based on lower price value,” says Leone.

Indian consumers are also highly specific in what they expect. According to market research firm Mintel, shoppers are increasingly drawn to formulations that are clinically tested and grounded in both science and local familiarity. Products must perform in Mumbai’s humidity and Delhi’s pollution and suit the full spectrum of Indian skin tones.

“Indian consumers love products that do more than one job, last long in our weather, and actually match Indian skin tones,” says Goradia. They are cautious spenders, she adds, but willing to invest when they see real quality and innovation.

Nykaa says this ingredient awareness is now visible across the country, not just metros. “Consumers are reading about niacinamide and retinol, they know what they want from a sunscreen, and are making considered purchase decisions. Brands need to earn their place on merit in every market,” says the spokesperson.

“A brand that addresses these needs well and remains within the customer’s budget succeeds,” says Dutta.

Gen Z will drive 50% of India’s beauty consumption by 2030

By 2030, Gen Z will drive 50% of India’s beauty and personal care consumption, a third of all sales will happen online, and per capita income is forecast to rise 138% in real terms by 2040, according to Euromonitor. Nykaa founder and CEO Falguni Nayar told Bloomberg that comparing India’s beauty routines to South Korea’s famed 14-step regimens is premature, “It is still day zero for beauty consumption in India.”

The global conglomerates have done the math. Estée Lauder, L’Oréal, and Puig are all moving deeper into India, betting on a consumer who is younger, more digitally fluent, and more ingredient-literate than any previous generation. The brands they are acquiring, Forest Essentials, Minimalist, Kama Ayurveda, share a common thread: They are built on something that exists independently of a famous face. “This is an industry that is very crowded and takes a lot of time to grow,” says Leone. “Western brands focus on global distribution and profit and loss. Not just turnover at a loss.” The celebrities who will build something lasting are the ones who understand that the launch is the easiest part. As Bijoor puts it: “Celebrity beauty is not skin deep at all. It is a deep brand science.”

(Published in The Times of India)

admin

May 15, 2026

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving “imported inflation” and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below):

1. Dual Impact on Industry and Consumers:

2. Vulnerability of Small Businesses (SMEs):

3. Income vs. Expenditure Strain:

4. Ripple Effect of Crude Oil Beyond Logistics:

5. Shifts in Consumer Spending Patterns & “Shrinkflation”:

The panel noted that while the Reserve Bank of India (RBI) has adequate foreign exchange reserves to defend the rupee temporarily, the definitive solution relies heavily on the cooling down of global geopolitical tensions (such as the Middle East conflict affecting the Strait of Hormuz). Until then, Indian consumers will need careful financial planning and smart spending adjustments to navigate this inflationary phase. [Video below.]

admin

March 1, 2026

Apoorva Mittal, Economic Times

1 March 2026

Resshmi Nair, 31, had grown used to the dotted red bumps on her arms. Her dermatologist diagnosed it as keratosis pilaris aka strawberry skin. It is a harmless skin condition that often affects legs and arms but Nair, a Mumbai-based marketing consultant, wanted it gone. She slathered lotions and salves but to no avail. Then she chanced upon an Instagram reel which showed an oil-based in-shower spray that promised to take care of her problem. “It was very tempting as it resonated with a personal concern,” she says. She is now on her third bottle. The bumps haven’t disappeared entirely, but they have become smaller, she says.

Like Nair, there are many who seek solutions tailormade for their beauty bugbears. Consumers who once searched for moisturisers and shampoos now look for niche products for hair and skin. They want to repair skin barrier, tame baby hairs and minimise facial pores.

A new generation of Indian beauty and personal care (BPC) brands are both listening to them and leading them. Focused products, they realise, could help them stand out in a crowded sector dominated by FMCG giants. While problems like acne, frizzy hair and rough skin have always been around, experts say the commercial importance of solving them narrowly and packaging that specificity as a brand strategy have become more intense of late.

India’s direct-to-consumer (D2C) beauty and personal care market—which is heavily invested in micro-problem targeting—is estimated to be $4.5 billion in FY2025, according to consulting firm Redseer. The new-age brands could account for 25-35% of total BPC spends by 2030. “Three major factors have contributed to this: one, the rise of digital medium for both commerce and marketing, which created a segue for new brands to launch and scale; two, younger consumers (Gen Z and young millennials) have become ingredient literate and look for results over broad promises; and three, competitive intensity in the market is pressing brands to position as per the right niches,” says Kushal Bhatnagar, associate partner, Redseer.

The shift is measurable on beauty retailer Nykaa’s platform. “Consumer vocabulary is far more evolved,” says a company spokesperson. Searches driven by specic concerns or ingredients are growing faster than broad category items. While foundational concerns like acne and brightening remain relevant, the platform is seeing strong growth in queries around pigmentation, barrier repair, pore care and specic hair issues. “This fragmentation is actually a sign of a more informed and aware consumer base,” the spokesperson adds.

ZOOMING IN

For young D2C brands, this behavioural shift has opened a narrow but potent entry point. Instead of launching another shampoo or moisturiser, they launch a product targeting a single problem and market it in an easily demonstrable short-video format. In the current beauty landscape, the market has shifted from general solutions to hyper-targeted efficacy.

Moxie Beauty, founded by Nikita Khanna in 2023, illustrates the playbook. Khanna, who previously worked at McKinsey, began with a focus on wavy and frizzy hair, a segment she herself belongs to. But it was one particular styling product, the flyaway hair stick, that went viral, propelling the brand into visibility. She says, “The wavy hair routine required us to educate people, which took time. But one can understand the flyaway wand in five seconds.” And it targeted what she calls a “widely held pain point”. That helped Moxie cut through crowded feeds and end up on consumer shelves. “Being synonymous with a category helps,” she says. “When people want a wax stick or flyaway stick, they search for our brand.”

That shift—from paying for visibility to being searched for directly—is critical in a market where customer acquisition costs (CAC) can be punishingly high. For many D2C brands, launching a sharply defined product is a way to reduce discovery friction and lower early-stage CAC. But a brand cannot be built or scaled on gimmicks, says Khanna. “If you solve only for what will look good in a video and will go viral, you won’t be able to scale. And if it’s a gimmick, people won’t repeat the purchase,” she adds.

Divanshee Jindal, cofounder of the brand The Solved Skin, says companies have to get the “product-communication fit” right. Her brand’s liquid pimple patch, which is designed to mask acne under makeup, is quickly emerging as its hero product. “People get excited when a product feels relatable and authentic,” says Jindal. “A new, convenient format that solves a real pain point makes consumers willing to try a new brand. But if it’s a standard product, say, a salicylic acid face wash, they will often default to a brand they already trust.”

SMALL IS BEAUTIFUL

The idea is to start small but evolve. Moxie, for instance, has moved beyond textured hair into solving broader “Indian hair problems” like damage repair and anti-dandruff that has brought in male consumers as well. “Curly or wavy hair was a huge, underserved problem,” says Khanna. “But the thought was always to solve other problems as well.” Moxie, which recently raised $15 million in a funding round led by Bessemer Venture Partners, says it has crossed Rs. 100 crore in annual recurring revenue on its two-year mark, and is seeing roughly 50% consumers coming back in six months across platforms. However, it says profitability is harder to crack because of intense competition from new brands and changing channel mix.

Mani Singhal, MD of the consulting firm Alvarez & Marsal, points out that most successful D2C brands started out with a sharply defined hero product. “Earlier it was natural vs chemical or price disruption; today it’s much more about efficacy proof, ingredient transparency, visible results and credible

storytelling,” she says.

From the manufacturer’s side, Nishit Dedhia of Kain Cosmeceuticals, a cosmetics manufacturing company, says, “It is easier today for brands to target special concerns. That specificity helps them build a differentiated product earlier on.” Most brands, he explains, x a major problem such as acne, dryness, pigmentation and then layer in a niche twist. Strawberry skin, once not a mainstream concern, is now a category. “People didn’t know the term. Once you give it a name, they identify with it,” he adds.

Dedhia describes the portfolio strategy as 8-2 or 9-1 where eight or nine products are general, incremental variations of core needs, while one or two are “category-building products” that require significant consumer education or product communication but create their own search demand. “That is the only way you get out of the vicious cycle of paying for visibility,” he says. “When people search for your brand directly, CAC comes down.”

Devangshu Dutta, founder of management consulting firm Third Eyesight, says micro-problem framing is “co-created” by consumers and companies. “The fragmentation is real, but the language used to describe it is heavily brand-driven,” he says. Terms like “strawberry skin” or “glass skin” correlate with influencer campaigns but label pre-existing dissatisfactions that mass products did not address sharply.

However, sometimes, in the race to differentiation, brands go for outlandish ideas. Dedhia says brands increasingly approach manufacturers with amusing asks in the quest to stand out. For instance, beard fillers packaged like mascara or plumpers for face and neck.

PRODUCE & PERISH

The problem is that the mortality rate of skincare brands is very high in India. Dedhia estimates that around 60% companies shut down in three years. Many brands burn through capital chasing ads and trends without building repeat customers or a community.

“For a brand to cross over from being a curiosity-driven purchase to being part of a regimen needs a minimum 25-30% of customers showing up as repeats after three months, while truly successful brands reach higher repeat numbers,” says Dutta.

Subscriptions are an even stronger test. “Generic formulations, me-too products and influencer spends can get you first users, but repeats will happen only from the user getting demonstrated value,” says Dutta.

But growth does not equal stability. CAC typically starts low for niche products, rises during scaling-up and stabilises only if organic demand takes over, says Bhatnagar of Redseer. Quick commerce accelerates discovery but compresses margins due to the high commission rates on these platforms, promotional expectations and lower average order values.

Singhal, who says a consolidation phase is underway, adds: “Niche entry can work extremely well if the problem is frequent enough and the solution is demonstrably effective.” Durable brands deliver consistent performance, build adjacencies beyond the first niche and maintain disciplined unit economics.

“If repeat rates don’t stabilise, economics becomes very challenging, very quickly.”

PERSONALISATION AHEAD

For Aparna Saxena, founder of Delhi-based beauty brand Antinorm, the next decade will be defined by even greater personalisation. Her brand has multifunctional products that are timesaving. Saxena says she surveyed about 250 women above 25 years of age and found that five-step routines typically do

not last after two months. Antinorm’s architecture rests on multifunctionality, like a leave-in cream that doubles as heat protectant and promises a “presentable” hair look without a blow-dry. Its most popular product is a spray that cleanses and moisturises, which they dub as “instant shower” or “facial in a flash”.

She says the brand, which launched in July last year, will close next fiscal with about Rs. 25 crore in revenue. Repeat rates are currently under 25% “because the denominator is expanding rapidly”, she adds. “Between 2020 and 2025, customers moved away from incumbents and got used to having options and trying newer brands,” she says. “Now they have routines in place. The next five years will be defined by more and more personalisation and micro-problem solving.” The beauty is about to go really skin deep.

(Published in Economic Times)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

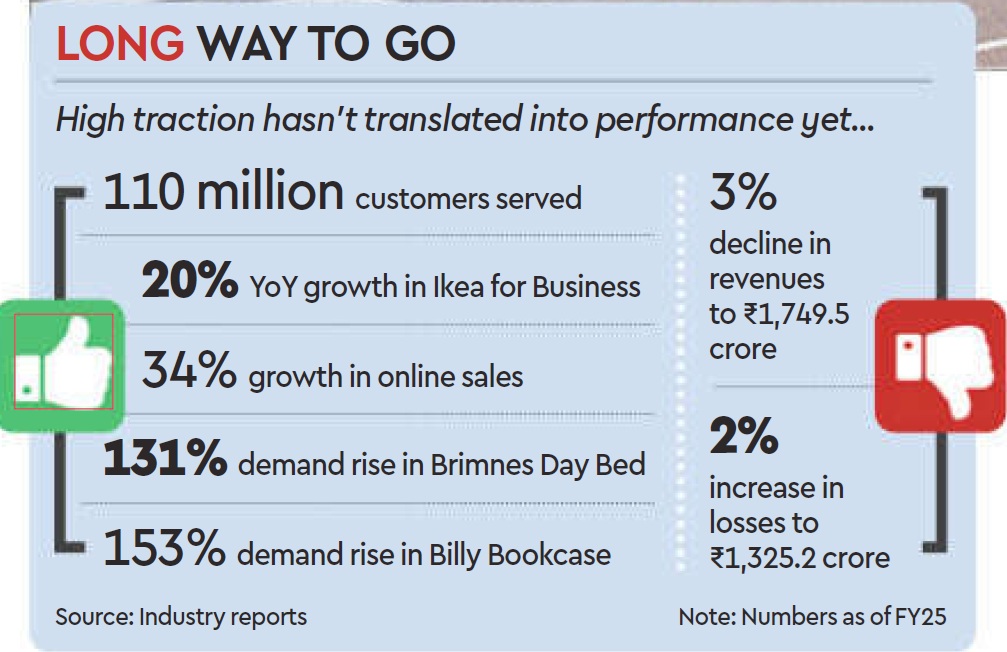

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)