admin

May 12, 2026

Anushka Jha & Kausar Madhyia, Afaqs

12 May 2026

On May 10, Prime Minister Narendra Modi, in his address to the nation, made some appeals to the citizens of India. In addition to asking Indians to re-adopt Covid-like practices of working from home and refraining from travel abroad, the prime minister also appealed to the citizenry to stop buying gold for weddings for a year.

The appeals come in response to the global energy crisis and economic instability triggered by the US-Iran war and the consequent West Asia conflict, which makes import-dependent commodities like gold especially vulnerable.

The market reaction was almost immediate. Following the Prime Minister’s appeal, jewellery stocks saw sharp declines on the BSE. According to PTI, Senco Gold fell nearly 11%, Kalyan Jewellers dropped close to 10%, and Titan Company declined around 8%, while Tribhovandas Bhimji Zaveri slipped over 6%.

National interest and gold monetisation

Industry leaders have responded by balancing the Prime Minister’s vision with structural solutions.

“India’s economic strength must always come before individual preferences. Hon’ble Prime Minister’s appeal regarding responsible gold consumption reflects the larger national concern of rising imports and pressure on foreign exchange reserves,” says Rajesh Rokde, chairman of the All India Gem and Jewellery Domestic Council (GJC).

He suggests that a revitalised Gold Monetisation Scheme (GMS) could “mobilise idle household gold” and “convert dormant gold into productive national capital”.

“Nation First. Responsible Gold Ecosystem Next,” he adds.

Avinash Gupta, the vice chairman of GJC, emphasises the emotional and cultural connection of gold to Indian households.

“But today, the nation also faces the challenge of balancing gold demand with economic stability.” He believes the GMS can channel gold into the formal economy, “reducing imports, easing CAD pressure and strengthening India’s financial ecosystem.”

India’s cultural fabric and the market reality

According to a report by MoneyControl, India imports 90% of its gold needs, making the country as one of the largest gold importers globally.

Gold is an integral part of India’s cultural fabric. It is not only a fitting gift for various auspicious occasions but also constitutes one of the most expensive elements of the ‘great Indian weddings’. Additionally, there are specific religious days dedicated solely to the purchase of gold, such as Akshaya Tritiya and Dhanteras.

However, external pressures are already weighing on the market.

Devangshu Dutta, founder of Third Eyesight, a retail management consulting firm, observes: “Jewellery retailers are already suffering from higher raw material costs, and rising gold and silver prices have driven several customers to postpone or reduce their purchases, including on significant dates such as Akshaya Tritiya.”

He notes that while wedding demand may remain strong, discretionary purchases will face a setback. “Companies will need to lean into lighter, more contemporary designs and lower caratage to sustain year-round demand.”

The potential impact of the appeal

Despite rising gold prices, approximately 700 to 800 tonnes of gold are consumed every year by Indian households, weddings, festivals, investment purchases, and rural savings, as per the same Money Control report.

Given the popularity of PM Modi, industry veterans expect a tangible shift in consumer behaviour.

“There will certainly be an impact,” says Arun Iyer, founder and creative partner at Spring Marketing Capital and former chief creative officer at Lowe Lintas, who played a significant role in the creation of Tanishq and several of its iconic advertisements.

“Given that the Prime Minister obviously has a very, very deep influence on our society, I think there will be an impact. People will think twice before buying gold.”

He further notes that while critical purchases will continue, “this quarter is expected to pose some challenges for the jewellery brands”.

Adaptation and brand strategy

According to the India Brand Equity Foundation, India’s gems and jewellery market stood at Rs 7,31,255 crore in January 2025 and is projected to increase to Rs 11,18,390 crore by 2030.

To sustain this growth, players like Suvankar Sen, CEO and MD of Senco Gold Ltd, are focusing on recycling.

“Today, almost 50% of our overall business is driven through recycled gold. This not only helps consumers optimise the value of their existing gold holdings but also contributes towards reducing dependence on fresh gold imports,” he says.

From a brand perspective, Saurabh Parmar, fractional CMO, believes the strategy must shift.

“In a scenario when the head of state says something like this, the brand faces a credibility problem, not a sales problem. The play is to shift from category promotion to category trust, lean on heritage, on long-term value, and on gold’s role in Indian culture.” He advises brands not to appear opportunistic but to signal, ‘We have always been there.'”

Given the popularity of Prime Minister Modi in India, his influence is likely to affect the performance of leading jewellery brands in the next quarter. This may include major players such as Tanishq, Malabar Gold & Diamonds, and Kalyan Jewellers, among others.

(Published in Afaqs)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

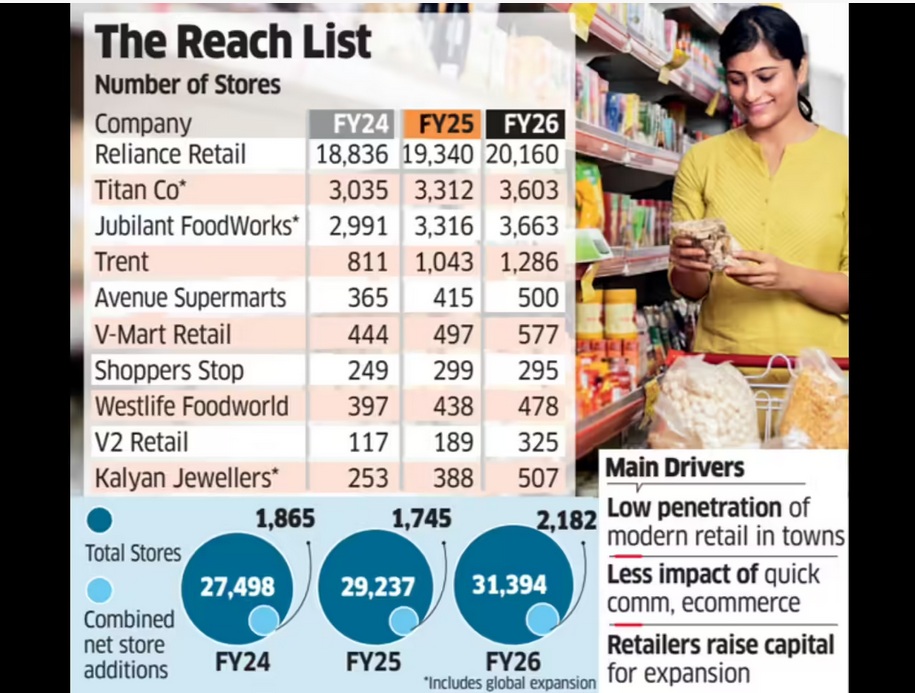

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

March 7, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 7 March 2026

While many consumer goods companies are acquiring direct-to-consumer (D2C) startups, Reliance Consumer Products Ltd (RCPL) is pursuing a different playbook. The consumer arm of billionaire Mukesh Ambani’s Reliance Industries has been steadily buying regional legacy brands with strong local recall. By plugging these brands into Reliance’s vast retail and distribution ecosystem, the company hopes to accelerate its ambition of becoming an FMCG powerhouse.

During the December quarter, RCPL overall gross revenue stood at 5,065 crore, up 60% year-on-year, according to an earnings statement from Reliance Industries. India’s FMCG sector remains dominated by established players such as Hindustan Unilever Ltd, which reported revenue of about 64,138 crore in FY25—highlighting the scale of the opportunity Reliance is targeting as it builds its consumer business.

“What Reliance is doing is cobbling together a portfolio of brands that already have some momentum,” said Arvind Singhal, chairman of The Knowledge Company, a Gurgaon-based management consulting firm.

Which regional brands has Reliance acquired?

Over the past few years, RCPL has assembled a portfolio of regional brands across food, beverages and personal care. One of its latest additions is Chennai-based Southern Health Foods Pvt. Ltd, which sells millet-based foods, health mixes and baby nutrition products under the Manna brand. Reliance acquired the company for about 158 crore, marking its entry into the fast-growing millet and nutrition foods segment.

Earlier, RCPL bought a majority stake in Udhaiyam Agro Foods Pvt. Ltd, a Tamil Nadu-based staples brand known for pulses, flours, spices and ready-to-cook mixes. Revenue at Shri Lakshmi Agro Foods Pvt. Ltd, which sells products under the Udhaiyam brand, rose about 5% year-on-year to 668.2 crore in FY24, according to Tracxn data.

Reliance has also acquired Delhi-based Sii, a legacy condiments maker known for jams, sauces and cooking pastes as well as Velvette, the historic personal care label that pioneered shampoo sachets in India in the 1980s.

In beverages, RCPL revived Campa Cola, acquired from the Pure Drinks Group, as a mass-market challenger in the carbonated drinks segment. It has also partnered Hajpuri & Sons to distribute regional drinks such as Sosyo, Kashmira and Ginlim, and tied up with Sri Lanka’s Elephant House to manufacture and distribute its beverages in India.

What do regional brands gain from partnering with Reliance?

Regional brands that partner with or are acquired by Reliance gain access to scale that is often difficult to achieve independently. Many local brands enjoy strong loyalty in their home markets but face constraints such as limited capital, weaker supply chains and restricted distribution networks.

Under the Reliance umbrella, these brands gain access to the group’s nationwide retail and distribution ecosystem, which includes millions of kirana stores as well as large-format retail chains operated by Reliance Retail. This enables them to expand beyond their regional strongholds far faster than they could independently.

Reliance can also improve manufacturing and supply-chain efficiencies, helping these brands scale production, strengthen sourcing and reduce logistics costs. In addition, stronger marketing capabilities and financial backing allow brands to invest in packaging, advertising and product innovation—helping them evolve from local favourites into national brands.

Why is Reliance pursuing this strategy?

For Reliance Consumer Products Ltd, acquiring regional brands offers a faster and potentially less risky way to expand in India’s vast FMCG market. These brands already have loyal customers, established products and existing manufacturing. By plugging them into Reliance Retail’s distribution network, the company can rapidly expand their reach across the country.

The strategy also allows Reliance to quickly build a diverse portfolio across staples, beverages and personal care—strengthening its ability to compete with established FMCG giants such as Hindustan Unilever and ITC.

How are rival FMCG companies expanding instead?

Most traditional FMCG companies are pursuing a different strategy by acquiring or investing in digital-first D2C brands. These startups often operate in fast-growing segments such as premium skincare, clean beauty and health-focused foods, helping established companies tap younger, digitally savvy consumers.

• Hindustan Unilever recently acquired skincare startup Minimalist, a fast-growing digital-first brand known for its ingredient-focused beauty products.

• Dabur India has also entered the space by acquiring premium beauty brand RAS Luxury Skincare through its 500-crore venture capital arm.

• Marico has taken a similar approach, investing in digital-first brands such as Beardo and Just Herbs to strengthen its presence in grooming and natural beauty.

Such deals allow established companies to quickly enter emerging premium categories.

What challenges could Reliance face in scaling regional brands?

Scaling regional brands nationally can be more complex than expanding digital-first startups. Many regional brands are built around specific local tastes, price sensitivities and cultural preferences that may not translate easily across markets. “India is very diverse, and consumer preferences vary significantly across regions,” said Singhal of The Knowledge Company.

Another challenge is that many regional brands lack the infrastructure to scale independently. “For many regional brands, the first real scaling often comes from the acquirer’s distribution rather than from the brand itself,” said Devangshu Dutta, founder of consulting firm Third Eyesight.

In contrast, many D2C brands are designed from the outset for a national or digital audience, making them easier to scale online. However, these startups often rely heavily on marketing spends and online channels, which can make profitability and large-scale expansion challenging.

For RCPL, the key test will be retaining the regional authenticity of these brands while using the nationwide distribution strength of Reliance Retail to expand them beyond their core markets.

(Published in Mint)

admin

March 1, 2026

Apoorva Mittal, Economic Times

1 March 2026

Resshmi Nair, 31, had grown used to the dotted red bumps on her arms. Her dermatologist diagnosed it as keratosis pilaris aka strawberry skin. It is a harmless skin condition that often affects legs and arms but Nair, a Mumbai-based marketing consultant, wanted it gone. She slathered lotions and salves but to no avail. Then she chanced upon an Instagram reel which showed an oil-based in-shower spray that promised to take care of her problem. “It was very tempting as it resonated with a personal concern,” she says. She is now on her third bottle. The bumps haven’t disappeared entirely, but they have become smaller, she says.

Like Nair, there are many who seek solutions tailormade for their beauty bugbears. Consumers who once searched for moisturisers and shampoos now look for niche products for hair and skin. They want to repair skin barrier, tame baby hairs and minimise facial pores.

A new generation of Indian beauty and personal care (BPC) brands are both listening to them and leading them. Focused products, they realise, could help them stand out in a crowded sector dominated by FMCG giants. While problems like acne, frizzy hair and rough skin have always been around, experts say the commercial importance of solving them narrowly and packaging that specificity as a brand strategy have become more intense of late.

India’s direct-to-consumer (D2C) beauty and personal care market—which is heavily invested in micro-problem targeting—is estimated to be $4.5 billion in FY2025, according to consulting firm Redseer. The new-age brands could account for 25-35% of total BPC spends by 2030. “Three major factors have contributed to this: one, the rise of digital medium for both commerce and marketing, which created a segue for new brands to launch and scale; two, younger consumers (Gen Z and young millennials) have become ingredient literate and look for results over broad promises; and three, competitive intensity in the market is pressing brands to position as per the right niches,” says Kushal Bhatnagar, associate partner, Redseer.

The shift is measurable on beauty retailer Nykaa’s platform. “Consumer vocabulary is far more evolved,” says a company spokesperson. Searches driven by specic concerns or ingredients are growing faster than broad category items. While foundational concerns like acne and brightening remain relevant, the platform is seeing strong growth in queries around pigmentation, barrier repair, pore care and specic hair issues. “This fragmentation is actually a sign of a more informed and aware consumer base,” the spokesperson adds.

ZOOMING IN

For young D2C brands, this behavioural shift has opened a narrow but potent entry point. Instead of launching another shampoo or moisturiser, they launch a product targeting a single problem and market it in an easily demonstrable short-video format. In the current beauty landscape, the market has shifted from general solutions to hyper-targeted efficacy.

Moxie Beauty, founded by Nikita Khanna in 2023, illustrates the playbook. Khanna, who previously worked at McKinsey, began with a focus on wavy and frizzy hair, a segment she herself belongs to. But it was one particular styling product, the flyaway hair stick, that went viral, propelling the brand into visibility. She says, “The wavy hair routine required us to educate people, which took time. But one can understand the flyaway wand in five seconds.” And it targeted what she calls a “widely held pain point”. That helped Moxie cut through crowded feeds and end up on consumer shelves. “Being synonymous with a category helps,” she says. “When people want a wax stick or flyaway stick, they search for our brand.”

That shift—from paying for visibility to being searched for directly—is critical in a market where customer acquisition costs (CAC) can be punishingly high. For many D2C brands, launching a sharply defined product is a way to reduce discovery friction and lower early-stage CAC. But a brand cannot be built or scaled on gimmicks, says Khanna. “If you solve only for what will look good in a video and will go viral, you won’t be able to scale. And if it’s a gimmick, people won’t repeat the purchase,” she adds.

Divanshee Jindal, cofounder of the brand The Solved Skin, says companies have to get the “product-communication fit” right. Her brand’s liquid pimple patch, which is designed to mask acne under makeup, is quickly emerging as its hero product. “People get excited when a product feels relatable and authentic,” says Jindal. “A new, convenient format that solves a real pain point makes consumers willing to try a new brand. But if it’s a standard product, say, a salicylic acid face wash, they will often default to a brand they already trust.”

SMALL IS BEAUTIFUL

The idea is to start small but evolve. Moxie, for instance, has moved beyond textured hair into solving broader “Indian hair problems” like damage repair and anti-dandruff that has brought in male consumers as well. “Curly or wavy hair was a huge, underserved problem,” says Khanna. “But the thought was always to solve other problems as well.” Moxie, which recently raised $15 million in a funding round led by Bessemer Venture Partners, says it has crossed Rs. 100 crore in annual recurring revenue on its two-year mark, and is seeing roughly 50% consumers coming back in six months across platforms. However, it says profitability is harder to crack because of intense competition from new brands and changing channel mix.

Mani Singhal, MD of the consulting firm Alvarez & Marsal, points out that most successful D2C brands started out with a sharply defined hero product. “Earlier it was natural vs chemical or price disruption; today it’s much more about efficacy proof, ingredient transparency, visible results and credible

storytelling,” she says.

From the manufacturer’s side, Nishit Dedhia of Kain Cosmeceuticals, a cosmetics manufacturing company, says, “It is easier today for brands to target special concerns. That specificity helps them build a differentiated product earlier on.” Most brands, he explains, x a major problem such as acne, dryness, pigmentation and then layer in a niche twist. Strawberry skin, once not a mainstream concern, is now a category. “People didn’t know the term. Once you give it a name, they identify with it,” he adds.

Dedhia describes the portfolio strategy as 8-2 or 9-1 where eight or nine products are general, incremental variations of core needs, while one or two are “category-building products” that require significant consumer education or product communication but create their own search demand. “That is the only way you get out of the vicious cycle of paying for visibility,” he says. “When people search for your brand directly, CAC comes down.”

Devangshu Dutta, founder of management consulting firm Third Eyesight, says micro-problem framing is “co-created” by consumers and companies. “The fragmentation is real, but the language used to describe it is heavily brand-driven,” he says. Terms like “strawberry skin” or “glass skin” correlate with influencer campaigns but label pre-existing dissatisfactions that mass products did not address sharply.

However, sometimes, in the race to differentiation, brands go for outlandish ideas. Dedhia says brands increasingly approach manufacturers with amusing asks in the quest to stand out. For instance, beard fillers packaged like mascara or plumpers for face and neck.

PRODUCE & PERISH

The problem is that the mortality rate of skincare brands is very high in India. Dedhia estimates that around 60% companies shut down in three years. Many brands burn through capital chasing ads and trends without building repeat customers or a community.

“For a brand to cross over from being a curiosity-driven purchase to being part of a regimen needs a minimum 25-30% of customers showing up as repeats after three months, while truly successful brands reach higher repeat numbers,” says Dutta.

Subscriptions are an even stronger test. “Generic formulations, me-too products and influencer spends can get you first users, but repeats will happen only from the user getting demonstrated value,” says Dutta.

But growth does not equal stability. CAC typically starts low for niche products, rises during scaling-up and stabilises only if organic demand takes over, says Bhatnagar of Redseer. Quick commerce accelerates discovery but compresses margins due to the high commission rates on these platforms, promotional expectations and lower average order values.

Singhal, who says a consolidation phase is underway, adds: “Niche entry can work extremely well if the problem is frequent enough and the solution is demonstrably effective.” Durable brands deliver consistent performance, build adjacencies beyond the first niche and maintain disciplined unit economics.

“If repeat rates don’t stabilise, economics becomes very challenging, very quickly.”

PERSONALISATION AHEAD

For Aparna Saxena, founder of Delhi-based beauty brand Antinorm, the next decade will be defined by even greater personalisation. Her brand has multifunctional products that are timesaving. Saxena says she surveyed about 250 women above 25 years of age and found that five-step routines typically do

not last after two months. Antinorm’s architecture rests on multifunctionality, like a leave-in cream that doubles as heat protectant and promises a “presentable” hair look without a blow-dry. Its most popular product is a spray that cleanses and moisturises, which they dub as “instant shower” or “facial in a flash”.

She says the brand, which launched in July last year, will close next fiscal with about Rs. 25 crore in revenue. Repeat rates are currently under 25% “because the denominator is expanding rapidly”, she adds. “Between 2020 and 2025, customers moved away from incumbents and got used to having options and trying newer brands,” she says. “Now they have routines in place. The next five years will be defined by more and more personalisation and micro-problem solving.” The beauty is about to go really skin deep.

(Published in Economic Times)

admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)