admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

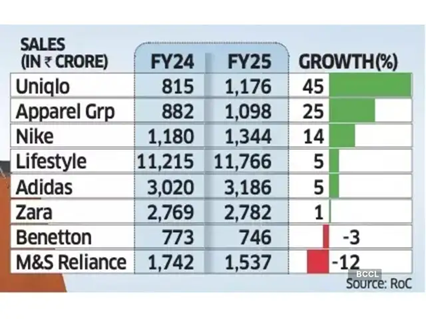

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

December 1, 2025

Priyamvada C, Mint

1 Dec 2025

A wave of investor capital is flowing into India’s laboratory-grown diamond (LGD) segment, as fastscaling brands tap rising consumer adoption in a market now worth well over $300 million. New-age brands have raised multiple rounds of capital on the back of growing market share and improving margins.

Actor Shilpa Shetty-backed Limelight, which is in talks to raise its second round of capital this year, joins the growing list of other small brands such as Onya, Giva, Jewelbox, Lucira Jewellery and Aukera, among others, who have snagged monies in recent months. Limelight has appointed Ambit Capital to raise about $20 million to fund its expansion plans, two people familiar with the matter said.

Confirming the fundraise, the six year-old company’s co-founder Pooja Madhavan said the funds will be used towards store expansion and brand building as it looks to touch 100 stores over the next year. “We are in final talks with growth PE funds and reputed family offices (for the fundraise),” she told Mint.

Other similar fundraises include Onya’s ₹5.5 crore in a pre-seed round led by Zeropearl VC last week, Aukera’s $15 million raise led by Peak XV Partners and Aditya Birla Ventures-backed Giva raised ₹530 crore in an internal round led by Premji Invest, Epiq Capital and Edelweiss Discovery Fund, as it looks to scale up its lab-grown diamond offerings.

Nine pure-play lab grown diamond startups collectively raised a record $26.4 million in 2025, compared with $4.7 million across eight startups last year, data from market intelligence provider Tracxn showed.

The development comes as India’s lab-grown diamond jewellery market, valued at about $300-350 million in 2024, expects to grow at a compound annual growth rate (CAGR) of 15% over the next decade, as per consultancy firm Redseer’s estimates. As the market evolves, several prominent jewellery brands will gradually pivot from exclusively natural/mined diamonds in favour of lab-grown alternatives, alongside high-end jewellers incorporating the lab-growns into their select collections, which will drive sales volumes and act as an affordable entry point for consumers.

This segment has particularly picked pace in the last five years, with millennials and gen Z leading this shift, driven by better value, trendier designs from new-age brands, and growing comfort with lab-grown diamonds as a certified, high-quality product. This category has also widened beyond occasional fashion to gifting, daily wear and increasingly bridal, reflecting sustained consumer confidence and a willingness to treat them as a mainstream jewellery option, Rohan Agarwal, partner at Redseer told Mint in an emailed statement.

He further added that new-age brands have steadily gained market share in the mid-ticket gifting and daily wear segment with many trying to push into premium ranges. While the competitive landscape is still evolving, incumbents have already started responding by launching LGD lines of their own, although the extent to which they can challenge remains to be seen.

Major Indian brands that are considering a foray into this category include Malabar Gold & Diamonds, Senco Gold, which has launched the subbrand Sennes and Tata’s Trent, which launched its brand Pome in Westside stores.

Devangshu Dutta, founder and chief executive officer at Delhi-based consulting firm Third Eyesight, echoed the sentiment. He explained that new-age lab grown diamond players are forcing traditional jewellers to introduce LGD options or risk losing younger customers. “Not just precious jewellery brands, even those that started as fashion jewellery are expanding their range with LGD designs.”

“Down the road, there is potentially scope for consolidation as investors tend to prefer a handful of scaled platforms with strong brand recall and robust economics. So, as the category matures, there may be strategic acquisitions by large jewellery houses and corporates, as well as mergers among funded startups,” he added.

Those startups that can combine in-house manufacturing, design capabilities and data-driven retail expansion would be at an advantage, Dutta said. “Key future growth areas for LGD startups include omnichannel retail presence within India, with offline stores especially in demand-dense locations such as the metros and Tier 1 cities, export markets both with potential cost advantages and brand expansion, and extending into fashion jewellery, everyday wear, coloured lab grown stones and even luxury collaborations that position lab grown as aspirational rather than merely budget friendly.”

(Published in Mint)

admin

November 27, 2025

Viveat Susan Pinto, Financial Express

November 27, 2025

Several of the country’s top retailers, malls and brands have kicked off a shopping extravaganza on the occasion of Black Friday, offering steep discounts across product categories.

A Western import, the day which symbolises the beginning of the Christmas shopping season in the US, the UK and Europe, gained popularity in India over the past two years as a crucial sale window after Diwali.

Domestic retailers, say experts, are using this period to exhaust existing inventory at steep discounts as they gear up for the winter season.

This year, discounts are up to 60-80% across fashion, lifestyle, electronics and cosmetics, higher than the 50% seen last year. E-tailers such as Ajio have pushed the pedal even harder, offering as much as 85-90% on denims, jackets and select products during the sale this year.

Bigger Deals, Longer Duration

“Retailers in India are building Black Friday as an important off-season peak. The participation of brands is growing, deals are getting bigger and the sale days are more,” Devangshu Dutta, founder and chief executive of Third Eyesight, a Gurugram-based retail consultancy, said. That is visible from the intense promotional activity this year. What began as a flash sale event a couple of years ago has now extended to a week-long sale period this year, experts said.

Pushpa Bector, senior executive director and business head, DLF Retail, said that brands this year are ready with strong offers, driven in part by GST cuts and a stable economic outlook. “Early trends show healthy interest across categories by consumers. We expect a strong double-digit uplift over the Black Friday period, setting us up for a strong close to the year,” she said.

Retailer Strategies

While Black Friday typically falls on the last Friday of November, some retailers such as Flipkart, Croma, Vijay Sales, Nykaa and Tata Cliq have kicked off their Black Friday sales last week itself to build on the excitement. For electronic retailers, said Nilesh Gupta, director, Vijay Sales, Black Friday will extend into Cyber Monday next week (falling on December 1), making it even more relevant for them to focus on the occasion.

“We’ve been building Black Friday as a retail property in the last few of years as it fills the post-Diwali void quite well. Black Friday also extends well into Cyber Monday which comes immediately after. While we started with a few categories in the initial years, we now have offers across all our segments. Discounts are up to 45-50% this year in line with last year,” he said.

Rival Croma is also offering up to 50% discount on products this year, executives said.

“Black Friday has become one of India’s most anticipated shopping moments. At Croma, we are focused on delivering value across categories with steal deals, bundled savings, and limited-time offers,” Croma’s CEO & MD Shibashish Roy said.

Croma will also introduce a special late-night shopping window on November 28 at select stores across India. For two hours—from 10 pm to 11:59 pm —these stores will remain open with exclusive additional discounts on some of the season’s most in-demand products.

Nishank Joshi, chief marketing officer, Nexus Select Malls, said it is elevating the Black Friday experience with bigger assured gifts, giveaways and reward points if consumers upload their bills on their Nexus One apps.

Mayank Lalpuria, director, marketing (north, central & west) at Phoenix Mills, which operates Phoenix malls, said that it was expecting double-digit year-on-year growth and strong footfalls during the Black Friday period.

Tanu Prasad, CEO – Malls, Oberoi Realty, said that the firm was seeing far more planned purchases towards premium products and a rise in family-oriented outings. “We are anticipating an encouraging response at the (Black Friday) weekend resulting in a strong kick-off to the (December) shopping season,” Prasad said.

Direct-to-consumer brands such as Inc.5 footwear and NEWME said that they have rolled out big deals for Black Friday. “We’re looking at a 30x surge in orders across both offline and online for Black Friday,” NEWME Co-founder & CEO Sumit Jasoria said.

“Our customers look forward to Black Friday, and this year, we’re excited to bring fresh new launches, curated edits, and our widest range yet,” Rajesh Kadam, CEO, Inc.5 Footwear, said.

(Published in Financial Express)

admin

November 18, 2025

Chris Kay, Krishn Kaushik and Andrea Rodrigues in Mumbai

Nov 18 2025

Just before dawn, Kashif Sameer joins dozens of couriers zipping across Mumbai to deliver items stocked in a basement of a shopping mall run by Reliance Industries.

“I make between 20 and 30 deliveries in a day,” said the 25-year-old, who had just driven a mile across the chaotic roads of the Indian megacity to drop off groceries ordered 15 minutes earlier. “It is very popular with customers.”

The buzzing activity at the so-called dark store, a mini-warehouse operated by Reliance’s ecommerce platform JioMart, is part of a renewed push by the conglomerate’s chair and Asia’s richest man, Mukesh Ambani, to reassert his company’s position in India’s retail market.

It has added hundreds of dark stores to operate a total of nearly 20,000 physical outlets this year — almost double its pre-pandemic size — as it battles for dominance against Blinkit, Swiggy and Zepto in the country’s ballooning quick-commerce market.

“It’s a question of who runs out of money first,” said Arvind Singhal, chair of retail consultancy The Knowledge Company. “We will see some kind of a shakeout.”

Despite its large network of physical stores, Reliance has yet to corner the domestic consumer market like it did with telecoms a decade ago. It faces entrenched competition from established domestic and international rivals, as well as millions of kiranas, family-run convenience stores.

The sprawling Tata Group operates a wide range of consumer businesses, while global multinationals such as Unilever and Nestlé are important players in India’s household goods market.

Reliance Retail, the division that contains all of the conglomerate’s consumer-facing units, had shed tens of thousands of employees and closed underperforming stores following a bloated build-out during the Covid-19 pandemic and slowing middle-class spending.

But India’s most valuable company, which has a market value of more than $225bn and operates across oil refining, telecoms and entertainment, is expanding its retail reach again.

Reliance Retail’s latest results point to a rebound. In the quarter ending September, the unit reported revenue of about $10bn and profit of $390mn, up 18 and 22 per cent respectively from the previous year.

“Reliance’s scale in retail now is unmatched in India,” said Devangshu Dutta, chief executive of consumer advisory company Third Eyesight, in reference to the breadth of the conglomerate’s business. “This scale is unique in India and rare in global retail.”

Ambani’s retail ambitions are being led by his 34-year-old daughter, Isha. In August, she detailed plans for Reliance’s consumer brands subsidiary, which has a portfolio including Lotus Chocolate and the recently revived nostalgic Indian soft drink Campa Cola, to reach $11.7bn in revenue within five years.

Ultimately, the goal was to “become India’s largest FMCG company with a global presence”, said Isha Ambani during Reliance’s annual meeting.

The company told the Financial Times that it continued to “reinforce its position as India’s largest retailer, expanding its nationwide network”.

While Ambani originally indicated that he wanted to list Reliance Jio Infocomm, the telecoms unit, and Reliance Retail by 2024, people familiar with the company said the retail unit was not ready to go public. The billionaire said the Jio listing could happen in the first half of next year.

“Competitive intensity in every category in the discretionary retail side has picked up very sharply,” said Karan Taurani, executive vice-president at Elara Capital, who does not expect Reliance Retail to float for at least two years. “New competitors, new brands have come in and they are challenging the larger incumbents.”

The Ambanis, who operate as gatekeepers for foreign companies seeking access to India’s massive but challenging business landscape, have sought to cement their position through a spate of partnerships with western retail brands.

Foreign brands including West Elm, Pottery Barn and Superdry have stores in Reliance’s shopping malls in upmarket Mumbai. However, those joint ventures have largely struggled to gain traction with shoppers in India, where the per capita income remains less than $3,000.

The conglomerate’s foreign brands business housing these joint ventures lost Rs2.7bn ($30mn) in the financial year through March 2025, according to the latest available accounts. The Knowledge Company’s Singhal called Reliance’s push to bring international names to India “a vanity project”.

Reliance’s high-profile partnership with fast-fashion retailer Shein has also been underwhelming. The company returned to India this year under Reliance’s wing after being booted out in 2020 when relations between New Delhi and Beijing soured following military clashes along their disputed border.

Shein’s app has been downloaded just 11mn times, according to market intelligence firm Sensor Tower. Its discount prices are largely matched, if not undercut, by many Indian ecommerce and fashion retailers, say analysts.

Reliance is investing heavily in quick commerce, where deliveries are promised in 30 minutes or less. Bank of America estimates the market could reach $128bn by 2030.

The field is at present dominated by Blinkit, Swiggy and Zepto, which together control more than 90 per cent of the quick commerce delivery market and compete with Amazon and Walmart-owned Flipkart. None of the companies are profitable.

The Ambanis are eager to catch up. Over the past six months, Reliance has built about 600 dark stores across cities to plug gaps in its vast store network. By contrast, market leader Blinkit operates about 1,800 dark stores.

In quick commerce, “we have to be there because everybody is”, said a person close to the conglomerate. “It is a long-term strategy.”

On a call with analysts last month, Reliance Retail’s finance chief Dinesh Taluja admitted to delays in entering quick commerce. But he insisted that Reliance offered better prices, more variety and wider reach across smaller Indian cities where it is often the only formal retailer.

“The competition today is mainly in the top 10, 20 cities,” Taluja said. “We are present in almost a thousand cities. Competition will take many years to reach where we already have a head start there.”

Still, Reliance was facing an uphill battle, warned Elara’s Taurani. “JioMart is making a late entry,” he said, “it will be very tough to disrupt players here.”

(Published in Financial Times, all copyrights owned by FT)

admin

November 13, 2025

Saumyangi Yadav,Entrepreneur

Nov 13, 2025

India’s consumer landscape is undergoing a decisive shift in 2025. While D2C brands that once thrived on digital-only distribution are now aggressively building an offline footprint, legacy FMCG majors are simultaneously acquiring digital-first brands to strengthen their portfolios and tap into new consumer behaviours.

As analysts suggest, these trends signal a maturing phase for India’s D2C ecosystem, one that blends physical retail and strategic consolidation.

Offline Push Accelerates

According to a recent CBRE report, ‘India’s D2C Revolution: The New Retail Order’, D2C brands leased nearly 5.95 lakh sq ft of retail space between January and June 2025, accounting for 18 per cent of all retail leasing during this period, up sharply from 8 per cent in the first half of 2024. Fashion and apparel dominated the expansion, contributing close to 60 per cent of D2C leasing, followed by homeware and furnishings and jewellery at about 12 per cent each, while health and personal care brands accounted for roughly six per cent. The shift is equally visible in the choice of retail formats: 46 per cent of D2C leasing went to high streets, 40 per cent to malls, and the remaining to standalone stores, reflecting the category’s growing focus on visibility, trial and experiential discovery.

Experts suggest that it represents a strategic pivot to blended engagement.

As Devangshu Dutta, CEO of Third Eyesight, notes, “India’s D2C surge is powered by digital-first consumers, tremendous improvement in seamless logistics, and low-cost market entry, supported subsequently by substantial amounts of investor capital chasing those startups that stand out from the competition. Yet, lasting success demands a more holistic view: the divide between online and offline is a business construct, not a consumer reality. The larger chunk of retail sales still happens through physical channels and, for brands that want to be mainstream, an omnichannel presence is absolutely essential.”

This also aligns with the broader market outlook. The India Brand Equity Foundation (IBEF), in its Indian FMCG Industry Analysis (October 2025), estimates the value of India’s D2C market at USD 80 billion in 2024, with expectations of crossing USD 100 billion in 2025. Much of this growth is being led by categories that combine frequent purchase cycles with strong digital discovery, beauty, personal care, and food and beverage segments where consumers are open to experimentation but demand authenticity, transparency, and a compelling product narrative.

“The Gen Z and millennial consumer cohorts value newness but also authenticity and unique product stories, which are best communicated in spaces that are controlled by the brand,” Dutta added, “In the launch and growth phases, this could be the brand’s digital presence including website and social media, but over time this can include pop-up stores, kiosks, shop-in-shops and even exclusive brand stores.”

CBRE’s data reflects this shift clearly, with D2C brands increasingly opting for flexible store formats and high-street locations to maximise traffic and visibility.

M&A Gains Momentum

Parallel to the offline push is a noticeable wave of consolidation. Large FMCG companies are accelerating acquisitions to capture emerging consumer niches and strengthen their digital-native capabilities.

In recent years, Hindustan Unilever has acquired Minimalist; Marico has bought Beardo, Just Herbs, True Elements, and Plix; ITC has taken over Yoga Bar; and Emami has secured full ownership of The Man Company. These deals, reported widely across business media in 2024 and 2025, point to the need for established companies to fast-track entry into high-growth, ingredient-forward, and youth-focused categories without the lead time of in-house incubation.

“Legacy FMCG companies are acquiring D2C brands to rapidly gain access to new consumer segments, product innovation, and digital-native capabilities, including direct engagement and insights. Such deals enable large companies to diversify portfolios, accelerate entry into trending segments by-passing the initial launch risks, and rejuvenate their brands with modern digital marketing expertise,” Dutta explained.

Challenges and Risks

But the acquisitions do not come without risk and challenges, analysts warned.

“However, integrating D2C operations also poses challenges, including cultural differences, the risk of stifling entrepreneurial agility, and the need to harmonise data and omnichannel strategies. The ability to nurture acquired brands without diluting their distinctive appeal will determine acquisition success,” Dutta added.

Yet even as the ecosystem expands, challenges remain. Offline stores add operational complexity, inventory planning, staffing, last-mile logistics, and real-time data integration. Still, the bottom line is that India’s D2C sector is moving into a hybrid era defined by tighter omnichannel integration, sharper product storytelling, and portfolio realignment through acquisitions.

(Published in Entrepreneur)