admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

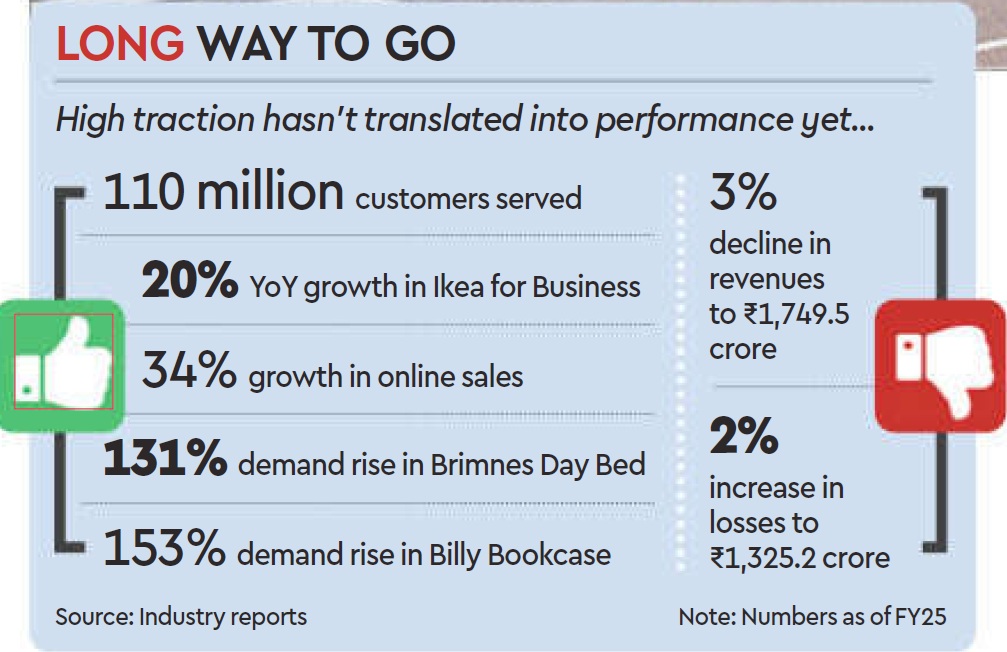

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

December 15, 2025

By Saumyangi Yadav, Entrepreneur India

Dec 15, 2025

India’s D2C ecosystem has grown rapidly over the past five years, but scale remains elusive. While thousands of brands have launched and many have crossed early revenue milestones, only a small fraction manage to break past INR 100 crore in annual revenue. According to a new report by DSG Consumer Partners, based on a survey of over 100 Indian D2C founders and operators, the problem is not demand or product-market fit, it is how brands attempt to scale.

The report shows that around 60–65 per cent of Indian D2C brands remain stuck in the INR 1–50 crore revenue band, with very few reaching the INR 100 crore mark. This stage marks the point where early traction exists, but growth begins to strain unit economics, teams, and operating systems.

Insights from over 100 D2C founders reveal that India’s fastest-growing brands win on fundamentals rather than speed alone. Clear product-market fit, disciplined data tracking, strong unit economics, creative velocity, and an early focus on retention consistently separate scalable brands from those that plateau. Founders also admit that performance marketing mistakes, pricing missteps, and weak creative systems slow growth far more than budget constraints. In a booming D2C landscape, capability gaps in operations, brand-building, and supply-chain depth are widening the divide between breakout brands and those stuck in the performance plateau.

Industry observers argue that this is where many brands mistake rapid online growth for sustainable scale.

As Devangshu Dutta, Founder & CEO, Third Eyesight, explains, “Scaling up online can be very rapid, but is also capital-hungry in terms of CAC. Given the intense competition, the lack of customer stickiness and the power of platforms, there is a constant churn of marketing spend which is a huge bleed for growing brands.”

CAC Inflation is The Real Constraint

One of the clearest findings from the playbook is that acquisition efficiency, rising CAC and unstable ROAS, is the single biggest blocker to growth, cited by more founders than funding or category expansion. Moreover, over 70 per cent of brands rely on Meta as their primary acquisition channel, increasing vulnerability to auction pressure and platform-driven volatility.

Dutta links this directly to the limits of a digital-only mindset. “Limited offline expansion can trap brands in narrow urban digital markets, blocking broader scale,” he said.

This over-reliance on online performance marketing often leads to growth that looks strong on dashboards but weak on cash flow.

Highlighting their report, Pooja Shirali, Vice President, DSG Consumer Partners, said, “Across over 90 consumer brands we’ve partnered with at DSGCP, one truth is clear: brands that master Meta’s ecosystem don’t just grow, they change their entire trajectory through strategic clarity and disciplined execution. The real drivers of scale have less to do with viral moments, and everything to do with the long-term fundamentals that make milestones like the first INR 100 crore predictable, not accidental.”

Why Omnichannel is Unavoidable

The report suggests that brands that scale sustainably are those that reduce overdependence on paid digital acquisition and expand their distribution footprint. However, offline expansion brings its own complexity.

Dutta stresses that omnichannel is not an optional add-on, but a strategic shift. “D2C brands must adopt an omnichannel approach, blending online with offline retail for sustainable and scalable reach. Clearly the channels work very differently and management teams have to be prepared and capitalised for the long haul to tackle acquiring customers with channel-appropriate strategies,” he adds.

This aligns with the DSGCP report’s broader insight that scale breaks down when brands fail to adapt operating models as they grow.

Even within digital channels, performance weakens over time. The playbook finds that 62 per cent of founders report creative fatigue, where repeated creatives fail to sustain ROAS despite higher spends. At the same time, 55 per cent admit to under-investing in CRM and retention, with most brands reporting repeat purchase rates of just 10–30 per cent.

Both the data and expert opinion point to a common theme: brands that cross the INR 100 crore mark are structurally different. They obsess over unit economics, processes, and capital efficiency rather than topline growth alone.

As Dutta puts it, “Scalable brands that cross the growth hump have leadership obsessed with unit economics and omnichannel execution rather than chasing vanity metrics. Cash always was and is king, especially at early stages of growth.”

He adds that execution strength matters as much as strategy. “They are able to grow and steer teams that build and replicate processes fast rather than spending time, effort and money reinventing all the time, and do so without constant CXO intervention.”

As competition intensifies and capital becomes more selective, the next generation of INR 100 crore D2C brands is likely to be defined not by speed, but by the ability to compound cash flows, institutionalise processes, and scale distribution beyond digital platforms.

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

(Published in Entrepreneur India)

admin

November 27, 2025

Viveat Susan Pinto, Financial Express

November 27, 2025

Several of the country’s top retailers, malls and brands have kicked off a shopping extravaganza on the occasion of Black Friday, offering steep discounts across product categories.

A Western import, the day which symbolises the beginning of the Christmas shopping season in the US, the UK and Europe, gained popularity in India over the past two years as a crucial sale window after Diwali.

Domestic retailers, say experts, are using this period to exhaust existing inventory at steep discounts as they gear up for the winter season.

This year, discounts are up to 60-80% across fashion, lifestyle, electronics and cosmetics, higher than the 50% seen last year. E-tailers such as Ajio have pushed the pedal even harder, offering as much as 85-90% on denims, jackets and select products during the sale this year.

Bigger Deals, Longer Duration

“Retailers in India are building Black Friday as an important off-season peak. The participation of brands is growing, deals are getting bigger and the sale days are more,” Devangshu Dutta, founder and chief executive of Third Eyesight, a Gurugram-based retail consultancy, said. That is visible from the intense promotional activity this year. What began as a flash sale event a couple of years ago has now extended to a week-long sale period this year, experts said.

Pushpa Bector, senior executive director and business head, DLF Retail, said that brands this year are ready with strong offers, driven in part by GST cuts and a stable economic outlook. “Early trends show healthy interest across categories by consumers. We expect a strong double-digit uplift over the Black Friday period, setting us up for a strong close to the year,” she said.

Retailer Strategies

While Black Friday typically falls on the last Friday of November, some retailers such as Flipkart, Croma, Vijay Sales, Nykaa and Tata Cliq have kicked off their Black Friday sales last week itself to build on the excitement. For electronic retailers, said Nilesh Gupta, director, Vijay Sales, Black Friday will extend into Cyber Monday next week (falling on December 1), making it even more relevant for them to focus on the occasion.

“We’ve been building Black Friday as a retail property in the last few of years as it fills the post-Diwali void quite well. Black Friday also extends well into Cyber Monday which comes immediately after. While we started with a few categories in the initial years, we now have offers across all our segments. Discounts are up to 45-50% this year in line with last year,” he said.

Rival Croma is also offering up to 50% discount on products this year, executives said.

“Black Friday has become one of India’s most anticipated shopping moments. At Croma, we are focused on delivering value across categories with steal deals, bundled savings, and limited-time offers,” Croma’s CEO & MD Shibashish Roy said.

Croma will also introduce a special late-night shopping window on November 28 at select stores across India. For two hours—from 10 pm to 11:59 pm —these stores will remain open with exclusive additional discounts on some of the season’s most in-demand products.

Nishank Joshi, chief marketing officer, Nexus Select Malls, said it is elevating the Black Friday experience with bigger assured gifts, giveaways and reward points if consumers upload their bills on their Nexus One apps.

Mayank Lalpuria, director, marketing (north, central & west) at Phoenix Mills, which operates Phoenix malls, said that it was expecting double-digit year-on-year growth and strong footfalls during the Black Friday period.

Tanu Prasad, CEO – Malls, Oberoi Realty, said that the firm was seeing far more planned purchases towards premium products and a rise in family-oriented outings. “We are anticipating an encouraging response at the (Black Friday) weekend resulting in a strong kick-off to the (December) shopping season,” Prasad said.

Direct-to-consumer brands such as Inc.5 footwear and NEWME said that they have rolled out big deals for Black Friday. “We’re looking at a 30x surge in orders across both offline and online for Black Friday,” NEWME Co-founder & CEO Sumit Jasoria said.

“Our customers look forward to Black Friday, and this year, we’re excited to bring fresh new launches, curated edits, and our widest range yet,” Rajesh Kadam, CEO, Inc.5 Footwear, said.

(Published in Financial Express)

admin

November 4, 2025

Yash Bhatia, IMPACT

4 November 2025

It started with groceries. Quick commerce started delivering milk, bread, and eggs in 10–15 minutes, which seemed revolutionary enough in 2022. Then came the iPhone 14 launch, and suddenly, quick commerce wasn’t just about convenience; it was about spectacle. Overnight, India’s app-based delivery ecosystem became the stage for a new ritual: flagship products arriving at your doorstep faster than you can say ‘checkout.’

And now? Phones aren’t the limit. You can even order motorcycles online. Yes, motorcycles. Royal Enfield has partnered with Flipkart to list its entire 350cc portfolio, which will be delivered to five cities: Bengaluru, Gurugram, Kolkata, Lucknow, and Mumbai.

The lines between e-commerce and quick commerce are becoming increasingly blurred. Flipkart’s Flipkart Minutes and Amazon’s instant delivery options are proof that speed is no longer a differentiator; it’s table stakes. And as platforms race to expand, high-ticket items are joining the frenzy, from electronics and furniture to watches, fitness equipment, and premium kitchen appliances. For platforms, these products are goldmines of margin; the challenge lies in logistics and consumer trust.

According to a report by CareEdge Advisory, India had over 270 million online shoppers in 2024, making it the second-largest e-retail user base globally, while the e-commerce market grew 23.8% in 2024 over the year-ago period, it said. The report also added that Indians ordered Rs 64,000 crore of goods from quick-commerce platforms.

From the consumer standpoint, one of the challenges for consumers to buy high-ticket items from the quick commerce platforms is to get consumer trust, which used to be the case when e-commerce started its operations. Can quick commerce move to high-ticket items? Is quick commerce looking at these items as a branding exercise, or are they looking at them as a serious revenue stream channel?

Chirag Taneja, Founder & CEO, GoKwik – an e-commerce enablement platform, says what began as a branding exercise for D2C brands has now evolved into a credible revenue stream. “In the early days, high-ticket categories on D2C platforms saw limited traction,” he explains. “Trust was still being built, customers were unsure if their orders would even reach them. There were many friction points.”

But that’s no longer the case. According to GoKwik’s network data, high-ticket purchases (above ₹2,500) are no longer outliers, they’re becoming a consistent driver of topline revenue.

Interestingly, most of these premium purchases are powered by credit instruments from no-cost EMIs to instant credit options at checkout. “This reflects a clear shift in mindset,” says Taneja. “Consumers no longer view high-value spending as a financial strain. They see it as a set of manageable, bite-sized payments that help them aspire higher, quicker. It’s not just a financial enabler, it’s a psychological unlock that makes premium consumption feel accessible and routine,” he adds.

“With strong trust in delivery reliability, smooth returns, and credible brand backing, the ecosystem has bridged the gap that once kept premium shopping offline,” says Taneja.

Devangshu Dutta, Founder of a specialist consulting firm, Third Eyesight, thinks differently and points out that high-value items still make up a small slice of quick commerce sales. “The model thrives on simplicity, a limited product range on the platform’s end, and quick, low-friction decision-making on the consumer’s,” he explains.

That said, Dutta believes quick commerce can still play a strategic role for premium brands. “For high-value products, q-comm can be an excellent lever for driving velocity, testing market response, or amplifying brand visibility. But it should be viewed as one piece of the channel mix, not the primary sales driver.”

From the platform’s perspective, however, listing high-ticket products brings its own upside. “They create excitement, boost average transaction values, and improve realised margins,” Dutta notes. “Consumers are often drawn in by novelty, exclusivity, or status appeal, especially during big launches or limited-time promotions.”

Still, he adds a note of realism: “Premium and high-ticket purchases largely remain planned decisions. Most consumers continue to prefer established offline and e-commerce channels for such buys where trust in authenticity, return policies, and after-sales services still carry greater weight than instant gratification.”

Seshu Kumar Tirumala, Chief Buying and Merchandising Officer, BigBasket, says the company doesn’t look at electronics as a high-ticket item category but rather focuses on building a complete category experience for customers. “For example, if we list an Enfield bike, we’d also want to offer spare parts, servicing options, and extended warranties, because that’s how the category functions,” he explains.

Tirumala adds that BigBasket adopted the same approach when it ventured into mobiles and mobile accessories. “When we launched this category last year, it was a trial. Today, it’s a sizable part of our business,” he says. Currently, electronics and mobile accessories contribute 5–10% of BigBasket’s monthly sales, having grown 250–300% year-on-year since the first iPhone launch on the platform.

While the launch day drives the highest demand for flagship devices like the iPhone, Tirumala notes that the following one to two months see strong accessory sales, from AirPods and headphones to chargers and power banks. “On average, mobiles and accessories account for 7–8% of our total sales, peaking at 10% during the festive season. Overall, this category has grown from zero to 7–8% of our total business in just a year, and we expect it to reach around 25% next year,” he adds.

Currently, the platform offers select models from smartphone brands, including OnePlus, Realme, Redmi, Vivo, and Oppo.

The Bengaluru-based platform is now piloting the delivery of large home appliances across across select city areas in partnership with Croma. If successful, BigBasket plans to expand this model to other cities, further broadening its quick commerce offering beyond everyday essentials.

Taneja points out that the traditional e-commerce model, once driven by discounts and affordability, is now evolving toward experience and access. Over the next few years, two major shifts will shape this transformation: credit-first commerce, where EMIs become the default mode for premium purchases, and aspirational commerce, where consumers view e-commerce as the easiest path to lifestyle upgrades. Consequently, platforms will need to reposition themselves from being “where you save more” to “where you unlock more”, prioritising personalisation, trust, and a seamless shopping experience.

As quick commerce matures, it is no longer just about instant gratification; it’s becoming a bridge between aspiration and accessibility.

Platforms are proving that speed, trust, and seamless experience can coexist with high-value purchases.

(Published in IMPACT)