admin

January 31, 2026

Surabhi Prasad, Business Today

Print Edition: 01 Feb, 2026

The last two years—2024 and, more notably, 2025—saw a wave of protests by a new generation of students and young professionals looking for political change, better economic conditions and more climate awareness across countries, including Bangladesh, Nepal, Indonesia and the Maldives.

But beyond these uprisings, Gen Z, the term used to describe those born in late 1990s to the early part of the 2010s and currently aged around 13-29 years, are not only questioning but also bringing forth changes in societal norms and economic behaviour. It’s not just a generation gap!

Gen Z are digital natives. They are tech savvy, have grown up with Internet in their homes, iPads as their support system, social media as a constant companion and take digital payments, online and quick commerce for granted. They tend to be night owls, the real gigsters, at home with artificial intelligence (AI) and machine learning, and with a lingo—cap, salty, suss and tea—that make others scratch their heads.

They also have newer challenges—rising unemployment, an uncertain economic environment, the rise of AI that has put a question mark on the future of work, climate change that is turning more real by the day, and skyrocketing real estate prices that mean a dream home could remain just a dream. Still, they are the rising consumer force who, over the next decade, are poised to become the largest chunk of the labour force and the focus of most companies.

For a country like India that is still young, Gen Z will soon be the economic force to reckon with. A recent report by not-for-profit think tank People Research on India’s Consumer Economy (PRICE) estimates that as of 2025, nearly one in five young individuals globally lives in India. “This is a formidable 420-million strong force, constituting approximately 29% of the nation’s total population, and made up of individuals aged between 15 and 29 as defined by India’s National Youth Policy (2014),” it said.

Labour sociologist Ellina Samantroy, Fellow at the V.V. Giri National Labour Institute, says India’s expanding Gen Z or youth workforce offers a significant opportunity for the country to reap the demographic dividend. As per the recent Periodic Labour Force Survey 2023-24, around 46.5% of the labour force is in the 15-29 age group. “There has been an increase in labour force participation in this age group from 42% during 2021-22. One can see the economic growth potential of this cohort,” she says.

However, with transitions and emerging opportunities in the world of work, it is important to harness the potential of this population cohort with adequate access to education and skilling, she says.

Devangshu Dutta, founder and chief executive of Third Eyesight, a boutique management consulting firm focused on the retail and consumer products ecosystem, says Indian Gen Z consumers are not a uniform cohort.

“A critical issue in India is the coexistence of aspiration and constraint, and India’s Gen Z are shaped by a mix of high digital exposure and wide economic disparity. While they are ambitious and globally aware, their purchasing power varies sharply across segments and locations,” he says.

Further, urban, higher-income Gen Z display global consumption behaviours such as brand experimentation, social commerce and premium aspiration, whereas a large proportion of Gen Z in Tier II, Tier III and rural India is highly value-driven and necessity-led, while drawing their inspiration from global and national sources. He also points out that unlike Millennials, Indian Gen Z are also entering the workforce in a more uncertain economic environment, making price sensitivity, smaller pack sizes and flexible payment options important. “Employment patterns such as informal jobs, gig work and delayed income stability are influencing consumption cycles and brand loyalty,” he says. There is a strong preference for digital discovery, vernacular content and peer-led recommendations, with trust built through community and relevance rather than legacy brand status.

Rising aspirations of Indian households and changes in consumption pattern with a marked move from essentials to more premium products have been well documented, most recently in Household Consumption Expenditure Surveys. But more granular, individual-level data from PRICE shows marked changes in education levels and behaviour of Gen Z and other cohorts such as Millennials (those aged between 30 and 45), Gen X (aged 45-60) and Baby Boomers (60+). A 2024 PRICE ICE 360 Survey of 8,200 respondents (18–70 years) in 25 major cities showed that Gen Z is the most educated cohort, spends the most time browsing the Internet and is more engaged with e-commerce and paid digital services.

Multinational and domestic companies are also now waking up to the Gen Z wave and are realising that they need to review strategies to gain the attention and loyalty of Gen Z as consumers and workers.

“Fashion, beauty and personal care, food and beverages, and mobile and consumer electronics are at the forefront of change in India,” says Dutta. Responding to Gen Z requirements, companies are designing products at accessible price points, expanding entry-level ranges and leveraging sachetisation and subscription models. Brands are investing more in regional languages, local influencers and platforms such as short-video and social commerce channels that resonate with young Indian consumers, he says.

But this process is still at a nascent stage, and many companies and analysts are still trying to assess this generation.

For the 34th Anniversary Issue, we at Business Today decided to decode what Gen Z is truly about, what influences them the most, what they aspire to purchase, what they can afford and what this means for India Inc. Over the course of the last few months, our newsroom saw animated discussions as senior editors sat down with younger colleagues to discuss lifestyle choices, brand loyalties and career ambitions, as we drafted an issue brief and a potential survey.

We then got in touch with PRICE, which worked with us on our survey objectives and tweaked the questionnaire. The result—a first-of-its-kind exercise where PRICE surveyed 4,311 Gen Z respondents, who are now entering the workforce with an income of their own, residing in metros and Tier II cities. The survey covered gender, education, employment status, personal income and household income classes. The main focus was urban, educated Gen-Z who has the income to be a strong consumer.

The research examined consumption behaviour across discretionary and essential categories, savings and credit attitudes, digital influence, brand loyalty, aspirations, and future spending intent.

And the results are indeed, surprising! The survey reveals that traditional consumption models that were built around age-based life stages, linear career progression and early credit adoption no longer hold for Gen Z. “This cohort’s behaviour reflects early exposure to economic shocks, greater career volatility and a redefinition of success away from speed toward resilience,” it underlines.

For businesses, misreading delayed demand as permanent weakness risks underinvestment just as Gen Z approaches its next consumption inflection, it warns. For financial services, premature credit push without trust-building will underperform. For consumer brands, price-led acquisition without quality consistency will fail to convert into lifetime value.

Delve into this issue where BT brings to you the in-depth findings of the survey and explains what this means for companies as they vie for a share of this growing consumer segment. Gen Z is not just about rizz and drip, it is giving the main character energy as they come of age.

(Published in Business Today, issue dated 1 February 2026)

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

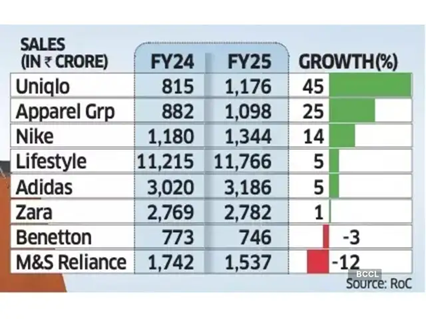

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

December 29, 2025

Yash Bhatia, Impact Magazine

29 December 2025

App, Tap, Pay and Zoom it’s delivered – that is Quick commerce for you. And in India, the narrative has so far been defined by speed, scale, high SKU counts, and the dominance of dark stores. Last week, however, Instamart nudged that model by opening an experiential store in Gurugram, allowing consumers to see and feel select products available on the platform.

The Bengaluru-based company has positioned the outlet not as a conventional retail store, but as a compact experiential format with a sharply curated assortment of around 100–200 SKUs, compared to the 15,000–20,000 SKUs typically housed in a dark store. Spanning roughly 400 sq. ft., the space is about one-tenth the size of a standard 4,000 sq. ft. dark store.

Under this model, sales proceeds are paid directly to sellers. This differs from Instamart’s regular arrangement, where payments are routed through the platform and later settled with sellers after deducting the platform’s share. IMPACT reached out to Instamart for further details, but the company declined to comment.

Sources close to the development say that Instamart has enabled sellers to open branded experiential stores in and around residential societies as part of a targeted consumer experiment. These are not conventional retail outlets, but compact experiential formats with a highly curated SKU assortment, focused on categories where consumers prefer to assess the products first-hand before purchasing, such as fresh fruits, vegetables, pulses, new product launches, and selected D2C brands. The initiative is largely centred on fresh categories and allows sellers to experiment with Instamart’s branding and service ecosystem.

Devangshu Dutta, Founder, Third Eyesight, a retail consultancy firm, says that physical presence plays a vital role in anchoring trust, particularly in premium products, groceries, and fresh produce. “Experiencing a product or brand physically can significantly enhance perceived value and help create stickiness. For this reason, offline stores continue to remain integral to the consumer products sector,” he explains.

Built on the promise of speed and convenience, quick commerce brands have come under growing scrutiny for quality and hygiene lapses at dark stores. Over the past year, several reports have flagged issues ranging from poor storage conditions and compromised freshness to the sale of expired or damaged products, particularly in food and grocery categories.

In some instances, regulatory inspections have led to licence suspensions after authorities identified hygiene violations at fulfilment centres. “Trust is what builds loyalty, and the shift is clearly moving from minutes to confidence,” says Shankar Shinde, Co-Founder, Aisles and Shelves, a behaviour-led brand consultancy in India. Shinde adds that the emergence of offline formats such as Instamart’s physical store aligns with this transition, particularly in grocery and fresh categories where consumers place a high premium on quality and consistency. “Physical touchpoints help reduce consumer anxiety, especially in a market like India, where shoppers still prefer hand-picked fresh produce such as fruits and vegetables,” he explains.

Against this backdrop, the opening of experiential centres could emerge as one way for quick commerce players to rebuild consumer trust by allowing shoppers to experience products in person before purchasing. IMPACT also reached out to Blinkit and Zepto for their views, but both declined to comment.

Kushal Bhatnagar, Associate Partner, Redseer Strategy Consultants, believes the move is aimed at unlocking incremental growth by tapping into offline-first consumers who are not yet active on quick commerce, while also catering to the offline purchase missions of existing quick commerce users. He notes that quick commerce currently reaches only about 75–80 million annual transacting users as of CY2025, even as over 90% of India’s grocery consumption continues to take place offline.

Beyond expanding reach, Bhatnagar sees offline formats as a way to address deeper trust barriers within the category. He adds that such formats can help deepen consumer confidence, particularly in categories where apprehensions around quality and freshness persist in quick commerce deliveries, concerns that are partly alleviated when consumers can experience products first-hand. Additionally, he points out that this approach benefits brands, especially emerging ones that are largely confined to quick commerce or a limited set of platforms, by giving them greater physical retail visibility without requiring heavy investment in traditional distribution networks.

Viewed through a financial lens, the move also carries implications for how quick commerce platforms justify value. Saurabh Parmar, fractional CMO, believes the initiative signals a shift from promise to performance, with a stronger emphasis on optimisation and a more realistic assessment of long-term value creation. He notes that while quick commerce has expanded into Tier 2 markets and seen growth in user numbers, these metrics alone still fall short of fully justifying current valuations. In this context, an offline presence becomes another lever to strengthen the overall business case.

At the same time, Parmar cautions that offline formats cannot replace the core proposition of quick commerce. He adds that experiential centres enhance brand credibility and make quick commerce feel closer to conventional retail, with the potential to eventually extend into other facets of e-commerce. However, he emphasises that quick commerce must continue to remain the frontline, as the sector’s valuations are fundamentally anchored in its speed-led proposition.

Retail experts, meanwhile, view physical touchpoints as a long-standing mechanism for building trust rather than a structural shift.

Dutta adds that such formats complement existing digital trust mechanisms such as delivery consistency, speed, ratings, and reviews by making brands feel tangible and accountable rather than abstract.

Bhatnagar notes that quick commerce currently has an average monthly transacting user base of around 40 million as of CY2025, leaving significant headroom for growth when compared to India’s overall e-commerce base of nearly 300 million active transacting users.

Beyond expanding the user base, he adds that experiential stores can also support wallet-share expansion across categories, which remains a key growth lever for the sector. “Non-grocery segments such as beauty and personal care, electronics, and fashion currently contribute about 25% of quick commerce GMV (Gross Merchandise Value), a share that is expected to rise further. Within groceries as well, platforms can drive incremental growth by building greater depth in fresh produce and staples,” Bhatnagar highlights.

From an operational perspective, however, the offline format is viewed more as a supporting layer than a core growth engine. Dutta sees Instamart’s offline presence as an experimental add-on rather than a replacement for its delivery-led model. The operating processes and economics differ significantly from those of quick commerce delivery, positioning physical formats as a complement to the speed proposition rather than an alternative. If the model proves viable and is backed by sufficient resources, it could eventually lead to a parallel scale-up of dark stores and experiential formats across different catchments.

For now, Instamart’s offline foray remains a tightly scoped experiment rather than a strategic pivot. Its significance lies less in square footage and more in what it signals about the evolving priorities of quick commerce. As the category matures, speed alone may no longer be sufficient to secure trust, loyalty, or long-term value. Experiential touchpoints, if deployed selectively, could help platforms bridge the gap between digital convenience and physical reassurance, particularly in categories where quality perception continues to remain fragile.

(Published in IMPACT)

admin

November 4, 2025

Yash Bhatia, IMPACT

4 November 2025

It started with groceries. Quick commerce started delivering milk, bread, and eggs in 10–15 minutes, which seemed revolutionary enough in 2022. Then came the iPhone 14 launch, and suddenly, quick commerce wasn’t just about convenience; it was about spectacle. Overnight, India’s app-based delivery ecosystem became the stage for a new ritual: flagship products arriving at your doorstep faster than you can say ‘checkout.’

And now? Phones aren’t the limit. You can even order motorcycles online. Yes, motorcycles. Royal Enfield has partnered with Flipkart to list its entire 350cc portfolio, which will be delivered to five cities: Bengaluru, Gurugram, Kolkata, Lucknow, and Mumbai.

The lines between e-commerce and quick commerce are becoming increasingly blurred. Flipkart’s Flipkart Minutes and Amazon’s instant delivery options are proof that speed is no longer a differentiator; it’s table stakes. And as platforms race to expand, high-ticket items are joining the frenzy, from electronics and furniture to watches, fitness equipment, and premium kitchen appliances. For platforms, these products are goldmines of margin; the challenge lies in logistics and consumer trust.

According to a report by CareEdge Advisory, India had over 270 million online shoppers in 2024, making it the second-largest e-retail user base globally, while the e-commerce market grew 23.8% in 2024 over the year-ago period, it said. The report also added that Indians ordered Rs 64,000 crore of goods from quick-commerce platforms.

From the consumer standpoint, one of the challenges for consumers to buy high-ticket items from the quick commerce platforms is to get consumer trust, which used to be the case when e-commerce started its operations. Can quick commerce move to high-ticket items? Is quick commerce looking at these items as a branding exercise, or are they looking at them as a serious revenue stream channel?

Chirag Taneja, Founder & CEO, GoKwik – an e-commerce enablement platform, says what began as a branding exercise for D2C brands has now evolved into a credible revenue stream. “In the early days, high-ticket categories on D2C platforms saw limited traction,” he explains. “Trust was still being built, customers were unsure if their orders would even reach them. There were many friction points.”

But that’s no longer the case. According to GoKwik’s network data, high-ticket purchases (above ₹2,500) are no longer outliers, they’re becoming a consistent driver of topline revenue.

Interestingly, most of these premium purchases are powered by credit instruments from no-cost EMIs to instant credit options at checkout. “This reflects a clear shift in mindset,” says Taneja. “Consumers no longer view high-value spending as a financial strain. They see it as a set of manageable, bite-sized payments that help them aspire higher, quicker. It’s not just a financial enabler, it’s a psychological unlock that makes premium consumption feel accessible and routine,” he adds.

“With strong trust in delivery reliability, smooth returns, and credible brand backing, the ecosystem has bridged the gap that once kept premium shopping offline,” says Taneja.

Devangshu Dutta, Founder of a specialist consulting firm, Third Eyesight, thinks differently and points out that high-value items still make up a small slice of quick commerce sales. “The model thrives on simplicity, a limited product range on the platform’s end, and quick, low-friction decision-making on the consumer’s,” he explains.

That said, Dutta believes quick commerce can still play a strategic role for premium brands. “For high-value products, q-comm can be an excellent lever for driving velocity, testing market response, or amplifying brand visibility. But it should be viewed as one piece of the channel mix, not the primary sales driver.”

From the platform’s perspective, however, listing high-ticket products brings its own upside. “They create excitement, boost average transaction values, and improve realised margins,” Dutta notes. “Consumers are often drawn in by novelty, exclusivity, or status appeal, especially during big launches or limited-time promotions.”

Still, he adds a note of realism: “Premium and high-ticket purchases largely remain planned decisions. Most consumers continue to prefer established offline and e-commerce channels for such buys where trust in authenticity, return policies, and after-sales services still carry greater weight than instant gratification.”

Seshu Kumar Tirumala, Chief Buying and Merchandising Officer, BigBasket, says the company doesn’t look at electronics as a high-ticket item category but rather focuses on building a complete category experience for customers. “For example, if we list an Enfield bike, we’d also want to offer spare parts, servicing options, and extended warranties, because that’s how the category functions,” he explains.

Tirumala adds that BigBasket adopted the same approach when it ventured into mobiles and mobile accessories. “When we launched this category last year, it was a trial. Today, it’s a sizable part of our business,” he says. Currently, electronics and mobile accessories contribute 5–10% of BigBasket’s monthly sales, having grown 250–300% year-on-year since the first iPhone launch on the platform.

While the launch day drives the highest demand for flagship devices like the iPhone, Tirumala notes that the following one to two months see strong accessory sales, from AirPods and headphones to chargers and power banks. “On average, mobiles and accessories account for 7–8% of our total sales, peaking at 10% during the festive season. Overall, this category has grown from zero to 7–8% of our total business in just a year, and we expect it to reach around 25% next year,” he adds.

Currently, the platform offers select models from smartphone brands, including OnePlus, Realme, Redmi, Vivo, and Oppo.

The Bengaluru-based platform is now piloting the delivery of large home appliances across across select city areas in partnership with Croma. If successful, BigBasket plans to expand this model to other cities, further broadening its quick commerce offering beyond everyday essentials.

Taneja points out that the traditional e-commerce model, once driven by discounts and affordability, is now evolving toward experience and access. Over the next few years, two major shifts will shape this transformation: credit-first commerce, where EMIs become the default mode for premium purchases, and aspirational commerce, where consumers view e-commerce as the easiest path to lifestyle upgrades. Consequently, platforms will need to reposition themselves from being “where you save more” to “where you unlock more”, prioritising personalisation, trust, and a seamless shopping experience.

As quick commerce matures, it is no longer just about instant gratification; it’s becoming a bridge between aspiration and accessibility.

Platforms are proving that speed, trust, and seamless experience can coexist with high-value purchases.

(Published in IMPACT)

admin

October 24, 2025

Entrepreneur India

Oct 23, 2025

Indian consumers are increasingly opting for private labels and in-house brands over established ones, and retailers are taking note. According to EY’s ‘Future Consumer Index 2025’, more than half of India’s consumers are now choosing in-house brands over legacy labels.

The report highlights that 52 per cent of Indian consumers have switched to private labels for better value, while 70 per cent believe these in-house brands offer comparable or superior quality. Backed by this shift, retailers from BigBasket to DMart, and quick-commerce players like Zepto and Blinkit, are doubling down on their private label strategies, viewing them as a path to higher margins, stronger brand loyalty, and greater pricing control.

“Indian consumers’ growing preference for private labels reflects both short-term price pressures and a longer-term structural evolution in retail,” said Devangshu Dutta, CEO of Third Eyesight, speaking to Entrepreneur India.

Trending globally

The surge isn’t unique to India. A recent report by the Institute of Grocery Distribution (IGD) notes that globally, private labels now account for over 45 per cent of grocery volume and are expanding faster than legacy brands.

In India, this shift is becoming increasingly visible in-store. The EY report found that 74 per cent of consumers have noticed more private label options where they shop, and 70 per cent say these products are now displayed more prominently, often placed at eye level, signalling a strategic retail push.

Commenting on this trend, Angshuman Bhattacharya, Partner and National Leader, Consumer Products and Retail Sector, EY-Parthenon, said, “Consumer behaviour has traditionally evolved in response to changing economic situations, but the current shifts appear to be more permanent. Retailers are confidently launching private labels and allocating prime shelf space to them, while technology is enhancing the shopping experience by providing consumers with limitless options and the ability to compare products.”

From price-fighters to power brands

According to Dutta, private labels are no longer just “copycat” alternatives meant to undercut national brands.

“For retailers, not just in India but globally, lookalike private labels used to be tools at the opening price point to hook the customer, who saw them as credible, affordable alternatives to national brands,” he explained, adding, “However, as retailers have grown, they have gained both scale and expertise to widen and deepen their supply chains.”

Over time, he said, investments in formulation, packaging, and quality consistency have increased consumer trust.

“Private labels now compete on functional benefits rather than only on price, particularly in food staples and apparel, but also in brown goods and white goods, and increasingly in personal care and other FMCG categories,” he added. [Must read: “Private Label Maturity Model”]

Retailers scale up private labels

As demand for in-house brands grows, retailers are scaling up their strategies across sectors.

BigBasket, one of India’s largest online grocery platforms, reported that 35–40 per cent of its FY24 sales came from private labels like Fresho, BB Royal, and Tasties. The company aims to push this share closer to 45 per cent through expansion in frozen foods and ready-to-eat categories.

DMart’s private label arm, Align Retail, has reportedly more than doubled its sales in two years, touching INR 3,322 crore in FY25. The retailer’s in-house brands in staples, apparel, and home essentials have helped boost margins in a highly competitive retail landscape.

Zepto, the quick-commerce player, is taking private labels into the 10-minute delivery domain. Its brand Relish, focused on meats and eggs, has achieved INR 40 crore in monthly sales.

Meanwhile, Reliance Retail has also expanded its portfolio of private labels, including Good Life, Enzo, and Puric, across groceries, personal care, and household products, strengthening its broader FMCG play. In 2024, Reliance Retail’s Tira Beauty also announced the launch of its latest private label brand, Nails Our Way, signifying a major expansion in its beauty offerings.

Capturing a lion’s share in retail

Dutta noted that in India, private labels will remain a core pillar of modern retail strategy rather than a cyclical response to cost pressures.

“Consumers increasingly view retailers as brand owners rather than intermediaries. As private labels mature in branding and innovation, their growth aligns more and more with brand equity development rather than just opportunistic cost-saving,” he said.

From a retailer’s perspective, private labels deliver higher gross margins and greater strategic control, Dutta said. [Must read: “Private Label Maturity Model”]

Another report by the Private Label Manufacturers Association (PLMA), using Circana data, found that in 2024, private-label sales in food and non-edible categories grew faster than bigger brands globally. While figures vary by region and quarter, the pattern remains consistent: private labels are outpacing traditional FMCG growth.

Collectively, these shifts show that private labels are becoming a major revenue driver for retailers in India, and are fast evolving from value alternatives into brands with genuine consumer pull.

(Published in Entrepreneur India)