admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)

admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

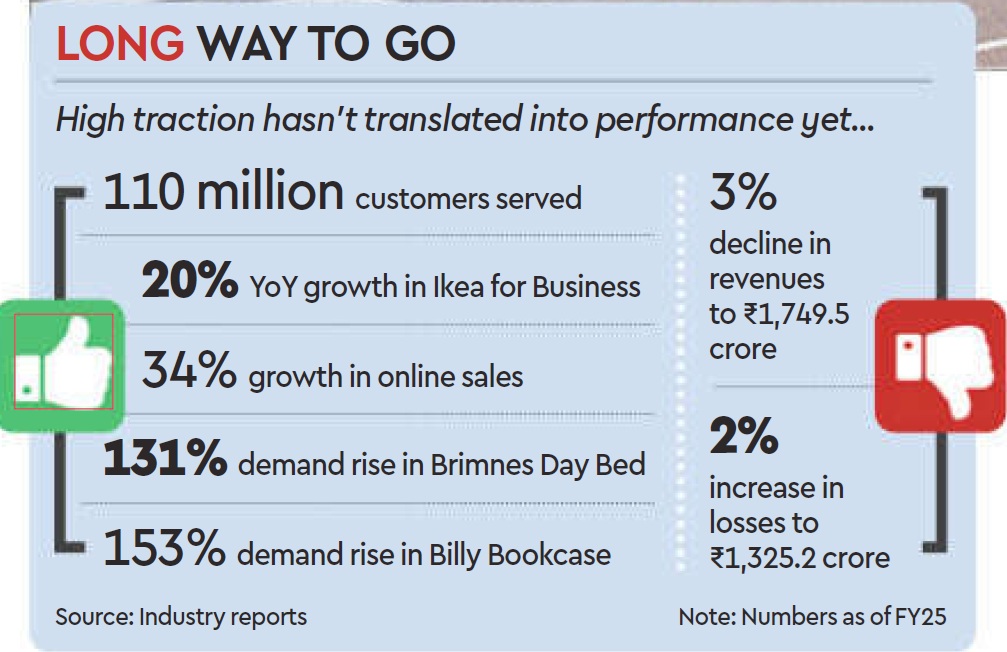

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

February 2, 2026

Sakshi Sadashiv, MINT

Bengaluru, 02 Feb 2026

BRND.ME, a roll-up commerce company, expects to complete its reverse flip (change of headquarters) from Singapore to India by March, clearing a key regulatory hurdle as it prepares to tap Indian public markets with an IPO.

Despite the rise of private labels from quick-commerce giants such as Swiggy Instamart and Zepto, CEO Ananth Narayanan remains confident. He argues that BRND.ME’s core categories—spanning complex, value-added products such as specialized haircare and niche party supplies—possess a level of brand loyalty and complexity that is difficult for generic retail labels to replicate. While private labels are currently displacing national brands in high-frequency, simple categories like dairy and staples, Narayanan believes the company’s core categories remain protected from this encroachment as they drive searches.

Having shifted its strategy from aggressive acquisitions to organic scaling, the company is now doubling down on its four largest brands: MyFitness (peanut butter), Botanic Hearth (haircare), Majestic Pure (aromatherapy), and PartyPropz (celebration supplies).

About 10-15% of BRND.ME’s India business currently comes from quick commerce, a channel the company plans to scale, Narayanan said. The company is the leader in party supplies on quick-commerce platforms, benefiting from impulse-driven demand. “People forget birthdays and anniversaries, so it’s a classic category to build a brand on quick commerce,” he said. The category contributes about ₹200 crore of revenue. The company also leads the peanut butter category through MyFitness, with a 30% market share on all quick commerce platforms and annual revenue of ₹270 crore.

The company’s revenue run rate stands at about $200 million. Male consumers worried about male-pattern baldness now account for about 35% of haircare sales. The company aims for a 10-fold jump in aromatherapy and haircare sales from $6 million to $60 million within four years, led by Majestic Pure and Botanic Hearth.

Drawing on his experience running Myntra, Narayanan said that private labels typically have a ceiling. “Even when we pushed hard on private labels at Myntra, they never went beyond 25-30% of the overall portfolio. That tends to remain the case as the categories we operate in are very hard to displace because we drive searches.”

This dynamic is already visible across several quick-commerce categories. The peanut butter segment is heavily consolidated on Blinkit, with Pintola and MyFitness together accounting for about 73% of sales, according to data from Datum Intelligence. Similar patterns have emerged in other categories. Blinkit’s popcorn segment, for instance, has rapidly consolidated into a duopoly, with 4700BC and Act II controlling 99% of sales.

Private labels muscling in

While Blinkit has consciously avoided launching private-label products on its platform, Swiggy has done so through Noice, and Zepto through Relish and Daily Good. For established brands, these private labels are becoming harder to ignore. Swiggy has scaled Noice aggressively, expanding the portfolio from about 200 to 350 stock keeping units (SKUs) and onboarding more manufacturing partners while moving beyond staples into categories such as beverages and ready-to-cook foods. These products are aimed at delivering significantly higher margins of 35-40%, compared with 10-15% on third-party brands, Mint reported earlier.

Private labels now contribute an estimated 6-8% of quick-commerce sales, up from 1-2% two years ago, according to data from 1digitalstack.ai, though penetration in perishables remains limited because of supply-chain complexity and quality concerns. A broader push into fresh categories could lift private-label share to 10-15%. Noice has already captured 3.4% of wafer sales and 1.9% of biscuit sales on the platform within months of its launch, according to 1digitalstack.ai data. The two categories are dominated by Lay’s and Britannia, which have a market share of about 35% each in their respective segments.

Zepto’s private-label push spans multiple everyday categories, including Relish for meat products, Daily Good for staples, Chyll for ice cubes and juices, and Aaha! for snacks, sweets, cereals and batters.

This growing presence creates a structural ‘trap’ for digital-first brands. Devangshu Dutta, chief executive at Third Eyesight, a consultancy firm, said, “Brands that are overly dependent on a single sales platform remain structurally vulnerable to being replaced by the platform’s own private labels, which are designed to capitalise on product opportunities that already have proven demand.” Platforms, he explained, tend to dominate high-frequency purchases, often undercutting brands on both price and visibility.

Persistently high online customer acquisition costs add to the pressure, particularly if the customer relationship is owned by the platform rather than the brand. “This has been one of the significant friction points for all digital-only brands, and weighs especially heavily on companies that have online-heavy portfolios with multiple brands in play,” Dutta added.

(Published in Mint)

admin

January 31, 2026

Surabhi Prasad, Business Today

Print Edition: 01 Feb, 2026

The last two years—2024 and, more notably, 2025—saw a wave of protests by a new generation of students and young professionals looking for political change, better economic conditions and more climate awareness across countries, including Bangladesh, Nepal, Indonesia and the Maldives.

But beyond these uprisings, Gen Z, the term used to describe those born in late 1990s to the early part of the 2010s and currently aged around 13-29 years, are not only questioning but also bringing forth changes in societal norms and economic behaviour. It’s not just a generation gap!

Gen Z are digital natives. They are tech savvy, have grown up with Internet in their homes, iPads as their support system, social media as a constant companion and take digital payments, online and quick commerce for granted. They tend to be night owls, the real gigsters, at home with artificial intelligence (AI) and machine learning, and with a lingo—cap, salty, suss and tea—that make others scratch their heads.

They also have newer challenges—rising unemployment, an uncertain economic environment, the rise of AI that has put a question mark on the future of work, climate change that is turning more real by the day, and skyrocketing real estate prices that mean a dream home could remain just a dream. Still, they are the rising consumer force who, over the next decade, are poised to become the largest chunk of the labour force and the focus of most companies.

For a country like India that is still young, Gen Z will soon be the economic force to reckon with. A recent report by not-for-profit think tank People Research on India’s Consumer Economy (PRICE) estimates that as of 2025, nearly one in five young individuals globally lives in India. “This is a formidable 420-million strong force, constituting approximately 29% of the nation’s total population, and made up of individuals aged between 15 and 29 as defined by India’s National Youth Policy (2014),” it said.

Labour sociologist Ellina Samantroy, Fellow at the V.V. Giri National Labour Institute, says India’s expanding Gen Z or youth workforce offers a significant opportunity for the country to reap the demographic dividend. As per the recent Periodic Labour Force Survey 2023-24, around 46.5% of the labour force is in the 15-29 age group. “There has been an increase in labour force participation in this age group from 42% during 2021-22. One can see the economic growth potential of this cohort,” she says.

However, with transitions and emerging opportunities in the world of work, it is important to harness the potential of this population cohort with adequate access to education and skilling, she says.

Devangshu Dutta, founder and chief executive of Third Eyesight, a boutique management consulting firm focused on the retail and consumer products ecosystem, says Indian Gen Z consumers are not a uniform cohort.

“A critical issue in India is the coexistence of aspiration and constraint, and India’s Gen Z are shaped by a mix of high digital exposure and wide economic disparity. While they are ambitious and globally aware, their purchasing power varies sharply across segments and locations,” he says.

Further, urban, higher-income Gen Z display global consumption behaviours such as brand experimentation, social commerce and premium aspiration, whereas a large proportion of Gen Z in Tier II, Tier III and rural India is highly value-driven and necessity-led, while drawing their inspiration from global and national sources. He also points out that unlike Millennials, Indian Gen Z are also entering the workforce in a more uncertain economic environment, making price sensitivity, smaller pack sizes and flexible payment options important. “Employment patterns such as informal jobs, gig work and delayed income stability are influencing consumption cycles and brand loyalty,” he says. There is a strong preference for digital discovery, vernacular content and peer-led recommendations, with trust built through community and relevance rather than legacy brand status.

Rising aspirations of Indian households and changes in consumption pattern with a marked move from essentials to more premium products have been well documented, most recently in Household Consumption Expenditure Surveys. But more granular, individual-level data from PRICE shows marked changes in education levels and behaviour of Gen Z and other cohorts such as Millennials (those aged between 30 and 45), Gen X (aged 45-60) and Baby Boomers (60+). A 2024 PRICE ICE 360 Survey of 8,200 respondents (18–70 years) in 25 major cities showed that Gen Z is the most educated cohort, spends the most time browsing the Internet and is more engaged with e-commerce and paid digital services.

Multinational and domestic companies are also now waking up to the Gen Z wave and are realising that they need to review strategies to gain the attention and loyalty of Gen Z as consumers and workers.

“Fashion, beauty and personal care, food and beverages, and mobile and consumer electronics are at the forefront of change in India,” says Dutta. Responding to Gen Z requirements, companies are designing products at accessible price points, expanding entry-level ranges and leveraging sachetisation and subscription models. Brands are investing more in regional languages, local influencers and platforms such as short-video and social commerce channels that resonate with young Indian consumers, he says.

But this process is still at a nascent stage, and many companies and analysts are still trying to assess this generation.

For the 34th Anniversary Issue, we at Business Today decided to decode what Gen Z is truly about, what influences them the most, what they aspire to purchase, what they can afford and what this means for India Inc. Over the course of the last few months, our newsroom saw animated discussions as senior editors sat down with younger colleagues to discuss lifestyle choices, brand loyalties and career ambitions, as we drafted an issue brief and a potential survey.

We then got in touch with PRICE, which worked with us on our survey objectives and tweaked the questionnaire. The result—a first-of-its-kind exercise where PRICE surveyed 4,311 Gen Z respondents, who are now entering the workforce with an income of their own, residing in metros and Tier II cities. The survey covered gender, education, employment status, personal income and household income classes. The main focus was urban, educated Gen-Z who has the income to be a strong consumer.

The research examined consumption behaviour across discretionary and essential categories, savings and credit attitudes, digital influence, brand loyalty, aspirations, and future spending intent.

And the results are indeed, surprising! The survey reveals that traditional consumption models that were built around age-based life stages, linear career progression and early credit adoption no longer hold for Gen Z. “This cohort’s behaviour reflects early exposure to economic shocks, greater career volatility and a redefinition of success away from speed toward resilience,” it underlines.

For businesses, misreading delayed demand as permanent weakness risks underinvestment just as Gen Z approaches its next consumption inflection, it warns. For financial services, premature credit push without trust-building will underperform. For consumer brands, price-led acquisition without quality consistency will fail to convert into lifetime value.

Delve into this issue where BT brings to you the in-depth findings of the survey and explains what this means for companies as they vie for a share of this growing consumer segment. Gen Z is not just about rizz and drip, it is giving the main character energy as they come of age.

(Published in Business Today, issue dated 1 February 2026)