admin

June 22, 2026

Sharleen D’souza & Shivani Shinde, Business Standard

Mumbai, 21 June 2026

Online beauty marketplaces Reliance Retail Ventures’ Tira and Nykaa have a common mantra: growing in-house brands. Successful brand acquisitions and margin growth seem to fuel the push.

“With private labels, margins are better. It also helps both companies plug the gap in the market which other brands are not present in,” Devangshu Dutta, chief executive officer (CEO) of Third Eyesight, told Business Standard. Within in-house brands, products need some investment in research and development (R&D), he explained.

Harish Bijoor, brand and business strategy consultant at Harish Bijoor Consults, said that margins are better for platforms with in-house brands.“Typically most companies are getting insular. The idea is to own brands and own the profits from those brands. When you are a marketplace, you put in effort for other brands, this strategy helps marketplaces lock in on profits instead of losing out to other brands, which sell on the platform,” he said.

At the 49th annual general meeting of Reliance Industries (RIL) on Friday, Isha Ambani, executive director of Reliance Retail Ventures Ltd, and non-executive director of RIL, had laid out plans for Tira. “We will scale our own brands to consumers across India and beyond, ensuring Indian beauty prod-

ucts stand proudly alongside the world’s leading global giants.”

Its in-house brands include Puraveda, Pahadi Local, haircare brand Anomaly, which was recently acquired from actress Priyanka Chopra Jonas, and skincare and make-up brand Akind, which it co-created with Mira Rajput Kapoor. Its portfolio also includes Nails Our Way and Dream Immerse Play.

Ambani’s statement had come a day after Nykaa’s management had also hinted at expanding its in-house brands on its investor day on Thursday. The platform, operated by FSN E-Commerce Ventures, outlined an ambitious road map to become an over $5 billion beauty and lifestyle business.

The growth of Nykaa’s “House of Brands” is expected to be significant. The management aims to be the largest house of brands business in India by financial year 2030 (FY30). Management has guided toward a net sale value (NSV) compounded annual growth rate (CAGR) of 30 per cent over FY26-30, taking the NSV from Rs. 1,700 crore in FY26 to Rs. 5,000 crore by FY30.

The “House of Nykaa” GMV grew over 65 per cent in FY26, with an improvement in profitability. In a report on the company’s focus on in-house brands business, Motilal Oswal said, “House of Brands is expected to grow faster than the core marketplace business and become a meaningfully larger contributor to group revenues and profits by FY30. We believe profit contribution is expected to increase disproportionately, given the higher gross margins, stronger pricing control, and lower dependence on third-party brands.”

Nykaa’s platform creates a structural incubation advantage, it said. “Fashion today serves about 300,000 styles across categories, while customer discovery increasingly happens through content, personalisation, and creator-led commerce. This allows the company to identify emerging brands and categories early, before allocating capital behind them,” the report added.

As of the fourth quarter of financial year (FY26), “House of Nykaa” had 12 brands across Beauty and Fashion categories at various growth stages, and two successful acquisitions of Dot & Key and Earth Rhythm. Dot & Key has grown 13 times over the last three years, while Kay Beauty has grown three times over this period, said the company. During the Q4FY26 results, the company had said that the strong performance of “House of Nykaa” had impacted margins positively. P Ganesh, chief financial officer, FSN E-Commerce while explaining the margin growth said, “…with gross margin improving by 132 basis points

in FY26, led by strong performance of House of Nykaa and improved service income across businesses.”

For FY26, “House of Nykaa” delivered a strong Rs. 3,176 crore of GMV. “That’s an about 50 per cent year-on-year increase. Served more than 17 million consumers and expanded distribution beyond online as well to 150,000 GT doors. As a reminder, this unit includes brands across beauty and fashion, seven brands in Beauty and in Fashion five brands, with an increased focus on one in particular, which is Nykd,” said Adwaita Nayar, executive director, cofounder and chief executive officer, “House of Nykaa Brands”, during the fourth quarter results.

(Published in Business Standard)

admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

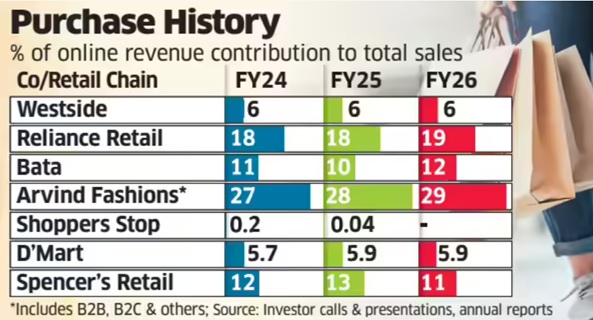

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

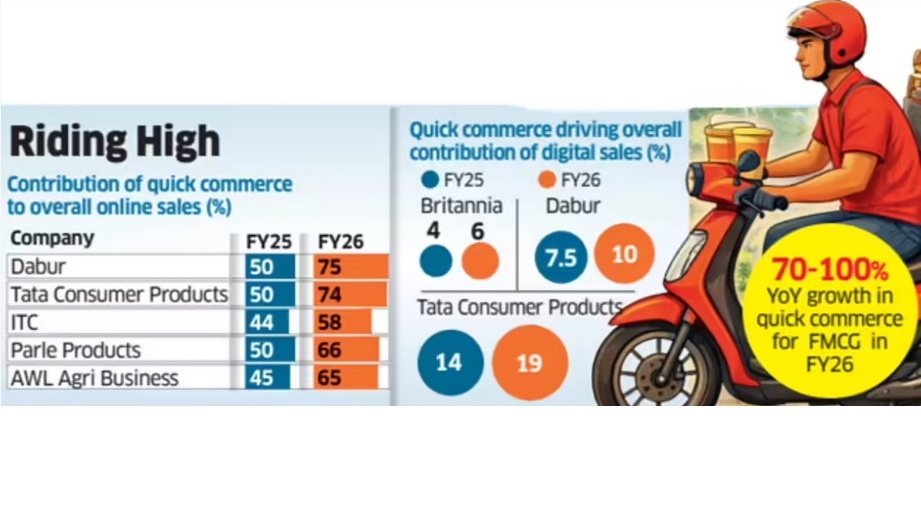

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

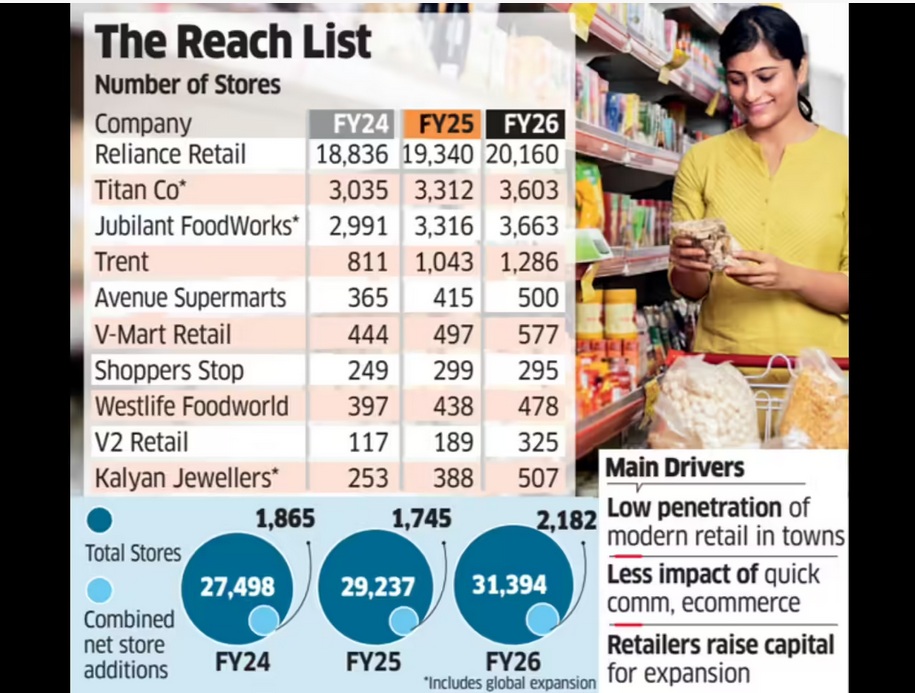

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

March 7, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 7 March 2026

While many consumer goods companies are acquiring direct-to-consumer (D2C) startups, Reliance Consumer Products Ltd (RCPL) is pursuing a different playbook. The consumer arm of billionaire Mukesh Ambani’s Reliance Industries has been steadily buying regional legacy brands with strong local recall. By plugging these brands into Reliance’s vast retail and distribution ecosystem, the company hopes to accelerate its ambition of becoming an FMCG powerhouse.

During the December quarter, RCPL overall gross revenue stood at 5,065 crore, up 60% year-on-year, according to an earnings statement from Reliance Industries. India’s FMCG sector remains dominated by established players such as Hindustan Unilever Ltd, which reported revenue of about 64,138 crore in FY25—highlighting the scale of the opportunity Reliance is targeting as it builds its consumer business.

“What Reliance is doing is cobbling together a portfolio of brands that already have some momentum,” said Arvind Singhal, chairman of The Knowledge Company, a Gurgaon-based management consulting firm.

Which regional brands has Reliance acquired?

Over the past few years, RCPL has assembled a portfolio of regional brands across food, beverages and personal care. One of its latest additions is Chennai-based Southern Health Foods Pvt. Ltd, which sells millet-based foods, health mixes and baby nutrition products under the Manna brand. Reliance acquired the company for about 158 crore, marking its entry into the fast-growing millet and nutrition foods segment.

Earlier, RCPL bought a majority stake in Udhaiyam Agro Foods Pvt. Ltd, a Tamil Nadu-based staples brand known for pulses, flours, spices and ready-to-cook mixes. Revenue at Shri Lakshmi Agro Foods Pvt. Ltd, which sells products under the Udhaiyam brand, rose about 5% year-on-year to 668.2 crore in FY24, according to Tracxn data.

Reliance has also acquired Delhi-based Sii, a legacy condiments maker known for jams, sauces and cooking pastes as well as Velvette, the historic personal care label that pioneered shampoo sachets in India in the 1980s.

In beverages, RCPL revived Campa Cola, acquired from the Pure Drinks Group, as a mass-market challenger in the carbonated drinks segment. It has also partnered Hajpuri & Sons to distribute regional drinks such as Sosyo, Kashmira and Ginlim, and tied up with Sri Lanka’s Elephant House to manufacture and distribute its beverages in India.

What do regional brands gain from partnering with Reliance?

Regional brands that partner with or are acquired by Reliance gain access to scale that is often difficult to achieve independently. Many local brands enjoy strong loyalty in their home markets but face constraints such as limited capital, weaker supply chains and restricted distribution networks.

Under the Reliance umbrella, these brands gain access to the group’s nationwide retail and distribution ecosystem, which includes millions of kirana stores as well as large-format retail chains operated by Reliance Retail. This enables them to expand beyond their regional strongholds far faster than they could independently.

Reliance can also improve manufacturing and supply-chain efficiencies, helping these brands scale production, strengthen sourcing and reduce logistics costs. In addition, stronger marketing capabilities and financial backing allow brands to invest in packaging, advertising and product innovation—helping them evolve from local favourites into national brands.

Why is Reliance pursuing this strategy?

For Reliance Consumer Products Ltd, acquiring regional brands offers a faster and potentially less risky way to expand in India’s vast FMCG market. These brands already have loyal customers, established products and existing manufacturing. By plugging them into Reliance Retail’s distribution network, the company can rapidly expand their reach across the country.

The strategy also allows Reliance to quickly build a diverse portfolio across staples, beverages and personal care—strengthening its ability to compete with established FMCG giants such as Hindustan Unilever and ITC.

How are rival FMCG companies expanding instead?

Most traditional FMCG companies are pursuing a different strategy by acquiring or investing in digital-first D2C brands. These startups often operate in fast-growing segments such as premium skincare, clean beauty and health-focused foods, helping established companies tap younger, digitally savvy consumers.

• Hindustan Unilever recently acquired skincare startup Minimalist, a fast-growing digital-first brand known for its ingredient-focused beauty products.

• Dabur India has also entered the space by acquiring premium beauty brand RAS Luxury Skincare through its 500-crore venture capital arm.

• Marico has taken a similar approach, investing in digital-first brands such as Beardo and Just Herbs to strengthen its presence in grooming and natural beauty.

Such deals allow established companies to quickly enter emerging premium categories.

What challenges could Reliance face in scaling regional brands?

Scaling regional brands nationally can be more complex than expanding digital-first startups. Many regional brands are built around specific local tastes, price sensitivities and cultural preferences that may not translate easily across markets. “India is very diverse, and consumer preferences vary significantly across regions,” said Singhal of The Knowledge Company.

Another challenge is that many regional brands lack the infrastructure to scale independently. “For many regional brands, the first real scaling often comes from the acquirer’s distribution rather than from the brand itself,” said Devangshu Dutta, founder of consulting firm Third Eyesight.

In contrast, many D2C brands are designed from the outset for a national or digital audience, making them easier to scale online. However, these startups often rely heavily on marketing spends and online channels, which can make profitability and large-scale expansion challenging.

For RCPL, the key test will be retaining the regional authenticity of these brands while using the nationwide distribution strength of Reliance Retail to expand them beyond their core markets.

(Published in Mint)