admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

January 15, 2026

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

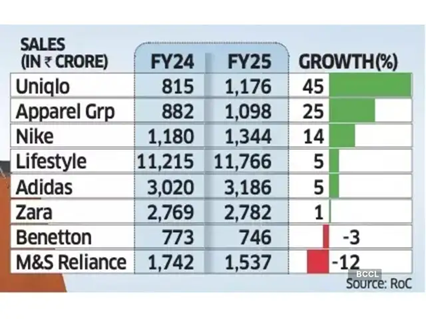

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

January 7, 2026

Writankar Mukherjee & Shabori Das, Economic Times / Brand Equity

7 January 2026

There’s a renewed sparkle in the adage ‘Old is Gold’ at India’s biggest conglomerate Reliance. Banking on Indians’ nostalgia, it is hawking and reviving labels that once defined everyday life, Campa and BPL among them, to set its consumer venture’s cash registers ringing.

What started with sales of Rs. 3,000 crore in FY24, Reliance Industries’ fast-moving consumer goods (FMCG) business quickly accelerated towards Rs. 11,500 crore the following year. With a staggering Rs. 5,400 crore posted in the July to September FY26 quarter alone, the revival story is clearly striking a chord with consumers. But Campa, already the largest contributor to the Reliance Industries’ FMCG business, is only the beginning.

The company is injecting fresh life into acquisition of legacy brands such as Ravalgaon in confectionery and Velvette in personal care. Reliance is applying the same formula to the consumer electronics business, covering televisions, refrigerators and washing machines. Once a staple of Indian households, Kelvinator and BPL are being reintroduced.

Strategy Rings a Bell?

Driving this revival is a strategy Reliance knows well: aggressive pricing that is often 20 to 30% lower than competitors, offering generous trade margins to woo retailers, and a rapid expansion of distribution from its own stores to kiranas and local outlets, alongside local sourcing and an expanding product portfolio.

It’s a playbook that once created waves in the telecom market; this time, however, it comes with a generous dose of nostalgia.

The path ahead though may not be easy. While Campa may have yielded results in a category linked to instant gratification, electronics is a high-ticket, long-term purchase. Marketers are debating whether consumers in their 20s and 30s—spoilt for choice by global brands—would choose a Kelvinator refrigerator, a BPL TV or a Velvette shower gel over LG, Samsung, Dove or Fiama.

Deep Pockets and Retail Muscle

Reliance, experts say, has two advantages— its balance sheet and strong market presence with its own retail stores. “Reliance has the intent to dominate a market in whatever business it enters. Their brands in FMCG and electronics too have a more-than-decent chance of surviving and thriving,” says Devangshu Dutta, founder and chief executive of Third Eyesight, a consultancy in consumer space.

“As long as they have capital and management capability, they may cut their teeth,” he says.

The company is approaching the FMCG and electronics businesses in startup mode, but with deep pockets. As a Reliance executive explains, the strategy is to invest and invest more, gain market share, continue to absorb losses and after achieving scale, drive efficiencies to generate profit.

The path has been carved out. Reliance Consumer Products (RCPL), the FMCG business entity and what started as a unit of Reliance Retail Ventures, is now a direct subsidiary of Reliance Industries. This shift will help the company raise funds independently and eventually launch an initial public offering (IPO), and drive valuation independent of retail. The electronic business may follow suit as it grows in scale.

Reliance did not respond to Brand Equity’s queries.

Electronics: A Tough Play

Industry executives say the electronics foray will not be an easy battle against international brands. Global brands enjoy strong appeal in the Indian market, and companies such as LG, Samsung and Sony have been present for over two decades, cementing their position. Even the newer ones like Haier and Voltas Beko are rapidly gaining market share.

Pulkit Baid, director of the electronics retail chain Great Eastern Retail, says that unlike the cola industry, where two large players (Coca-Cola and PepsiCo) dominate, consumer durables are highly fragmented. “Kelvinator enjoys the brand heritage of an Ambassador car. But we will have to see if the brand is welcomed by Gen Z with the same euphoria as Campa.”

Industry veteran Deba Ghoshal notes that very few legacy brands have been able to withstand the onslaught of new-age brands in consumer electronics. Voltas (from the Tatas) and Godrej are exceptions, he adds.

“Reliance Retail has the strategic foresight to re-establish legacy brands in consumer durables space, instead of chasing a standalone private label business,” adds Ghoshal. “There is a strong opportunity in BPL and Kelvinator, provided they are re-launched with strong value and engaging emotive hooks, and not restricted to being a price warrior. Reliance has the capability; it just needs the right strategy.”

Reliance is readying campaigns for BPL and Kelvinator to connect with the younger consumers. The company is planning to re-launch them beyond Reliance Retail stores—targeting regional retail chains and e-commerce platforms and expanding quickly into smaller towns. With India’s electronics penetration still low—15 to 18% for flat-panel TVs, 40% for refrigerators, 20% for washing machines and less than 10% for air conditioners (ACs)—Reliance has substantial headroom for growth.

Angshuman Bhattacharya, partner and national leader for consumer products and retail at EY India, says Reliance may focus on tier two and three cities. “These markets have been a low priority for the Samsungs and LGs because they want to play in the premium segment where margins are higher. That is where Reliance may expand the market. It requires a lot of capital in terms of inventories and distribution, and Reliance has the ability and potential to do so.”

FMCG: Ball is Rolling

The FMCG push is gaining strong momentum. Reliance plans to double its distribution to three million outlets this fiscal.

Over the next three years, it looks to invest Rs. 40,000 crore to create Asia’s largest integrated food parks and has already invested Rs. 3,000 crore in manufacturing.

Isha Ambani, who spearheads Reliance’s retail and FMCG businesses, drew attention to Campa’s comeback at the company’s AGM in August: “Campa-Cola now holds double-digit market share across many states, breaking a 30-year MNC duopoly of Coca-Cola and PepsiCo. Campa Energy gained two million social media followers in just 90 days.”

Her target is bold: To reach Rs. 1 lakh crore in FMCG revenue within five years and become India’s largest FMCG company with a global presence.

Market watchers say such high ambitions require high investments. Kannan Sitaram, co-founder and partner at venture capital firm Fireside Ventures, said a company like Hindustan Unilever would set aside at least `30-40 crore to launch a brand. “Advertising and marketing alone would take up more than half of that. And when you are re-launching a brand which has not been around for a long while, the spending tends to be 25 to 30% higher in the initial three to four months,” he says.

Yet, analysts believe Reliance is in the consumer brands business for the long term. Bhattacharya says whatever Reliance has learned in this short time is meaningful and serious, something nobody else has managed.

Mover and Shaker

Competitors, including Tata Consumer Products, Dabur and PepsiCo’s largest bottler in India Varun Beverages, have acknowledged the turbulence created by Reliance in the FMCG sector. But the industry hopes low penetration levels will ensure there is room for everyone.

Varun Beverages chairman Ravi Jaipuria did not mince his words in the company’s latest earnings call in October-end: “They (Reliance) have woken all of us up and we are becoming more attentive… it is a very healthy sign for the country because our per capita consumption is so low that in the next five to 10 years, this market may double or triple…there is a huge room, and we see only positives in this.”

The revival of legacy brands and aggressive push into FMCG and consumer electronics indicates that Reliance is preparing for the long haul. In this fight driven by nostalgia, competitive pricing, deep pockets and distribution muscle, the battle for shelf space has just begun.

(Published in Economic Times/Brand Equity)

admin

January 6, 2026

Saumyangi Yadav, Entrepreneur India

Jan 6, 2026

After years of rapid growth and a sharp reset, India’s direct-to-consumer (D2C) sector is expected to settle into a more balanced phase. The period of easy funding, aggressive customer acquisition and scale-at-all-costs expansion is clearly over, experts suggest. Now, what lies ahead in 2026 is a shift towards steadier growth driven by better execution, stronger retention and clearer brand positioning.

According to Bain and Flipkart, India’s e-retail market is projected to reach $170–190 billion in GMV by 2030, driven by a growing online shopper base and evolving commerce models. As adoption deepens across Tier-2 and Tier-3 cities, high-frequency categories such as grocery and lifestyle are expected to drive a larger share of growth, making repeat purchase and habit formation critical for D2C brands.

Against this backdrop, 2026 is shaping up as the year when D2C brands are judged less on ambition and more on outcomes.

A Post-Hype Phase of D2C

Industry observers say the D2C ecosystem has clearly moved beyond its hype-driven phase. Devangshu Dutta, Founder and Chief Executive of retail consultancy Third Eyesight, describes the current moment as one of structural correction rather than contraction.

“India’s D2C ecosystem is in a post-hype phase where growth may be slower but structurally healthier,” Dutta says, adding, “Earlier growth cycles prioritised visibility and sales at the expense of profitability and consistency. Now, success is being measured by repeat rates, contribution margins and the ability to fund growth internally.”

Tighter funding is also driving this shift. With D2C investments slowing and overall capital remaining cautious, brands are now being pushed to show predictability rather than promise. Tracxn data shows Indian D2C startups raised USD 757 million in 2024, significantly lower than previous years, while overall PE-VC investments in India remained flat at USD 33 billion in 2025, according to Venture Intelligence.

As a result, Dutta notes that many D2C companies are rationalising portfolios, tightening inventory cycles and optimising supply chains. Marketing strategies, too, are evolving, with greater emphasis on retention, community-building and owned channels instead of discount-led growth.

Uniqueness Will Define Winners

If capital discipline is one defining force, speed is another. Harish Bijoor, business and brand strategy expert, argues that D2C’s next phase will be shaped by how brands respond to a faster, more fragmented commerce environment.

“The e-commerce revolution led to a more refined orientation of D2C, and that has now given way to a q-commerce revolution that is even faster,” Bijoor says, adding, “The D2C revolution is going to be leveraged by speed. A whole host of players will invest time, energy and innovation into this.”

In Bijoor’s view, traditional e-commerce is now the slowest layer in a spectrum where quick commerce is the fastest, and D2C sits in between. In such a landscape, competing purely on price is no longer sustainable. He believes differentiation will increasingly come from uniqueness and premium positioning rather than ubiquity.

“When you know that you get a particular great-tasting biryani at just one place with no branches, you will go to that place. That uniqueness is what will distinguish D2C commerce in the future,” he says.

Bijoor adds that many D2C brands have been trapped in price wars under the guise of differentiation. He also argued that brands that premiumise and resist excessive omnichannel dilution are more likely to build desirability and long-term value.

Consumers Move Beyond Metros

Structural shifts in demand are reshaping how and where D2C brands grow. India now has one of the world’s largest and most diverse online consumer bases, with growth increasingly driven by Tier-2, Tier-3 and smaller towns rather than metros alone. Internet adoption continues to deepen across rural and semi-urban India, expanding the addressable market well beyond early digital buyers.

This widening base is changing the nature of growth. Consumers are becoming more deliberate in how they spend, weighing value, quality and trust more carefully than before.

As Devangshu Dutta notes, Indian consumers have always been discerning, but rising living costs and economic uncertainty have made them even more thoughtful, pushing brands to earn repeat demand rather than rely on impulse or discount-led purchases.

“Value is not just about discounts,” he says. “It’s a balance of price, performance and trust. For D2C brands, repeat consumption has to be earned through consistent quality, transparent pricing and dependable service.”

High-frequency categories such as grocery, lifestyle and general merchandise are expected to drive much of this expansion. Bain estimates these segments will account for two out of every three e-retail dollars by 2030, reinforcing the importance of habit formation and retention-led models.

Quick Commerce Expands Discovery, Not Profitability

Quick commerce has emerged as a powerful but complex growth lever for D2C brands. The format now accounts for a significant share of India’s e-grocery demand and has scaled into a multi-billion-dollar market, becoming a key discovery channel for food and everyday consumption brands.

However, expansion beyond metros remains challenging. RedSeer data shows non-metro markets contribute just over 20 per cent of quick commerce GMV, even as platforms scale to over 150 cities, with breakeven economics in smaller towns requiring significantly higher throughput.

Praveen Govindu, partner at Deloitte India, cautions that while quick commerce has helped many D2C brands gain discovery, particularly in food and beverage, it is not a sustainable growth engine on its own.

“From a customer acquisition standpoint, quick commerce is not fundamentally different from traditional e-commerce,” Govindu says, adding, “It is an expensive channel, and competition will only intensify. Over the long term, brands cannot rely on burning capital there.”

Omnichannel Enters Its Toughest Phase Yet

As digital acquisition costs rise, India’s ad market is projected to grow nearly 8 per cent in 2025 to Rs 1.37 lakh crore, with digital accounting for almost half of the spends, brands are being pushed to diversify distribution. Yet omnichannel presence alone is no longer enough.

“Many brands talk about omnichannel, personalisation and seamless journeys, but in practice these efforts are still disjointed. In 2026, the focus will shift from intent to execution,” Govindu says.

RedSeer projects India’s retail market to cross USD 2 trillion by 2030, with nearly 90 per cent of consumption still happening offline. For D2C brands, this makes offline expansion unavoidable, but success will depend on consistent execution across pricing, inventory, service and communication.

Consumers, Govindu notes, do not consciously differentiate between online, offline or social platforms. “They simply want a consistent experience,” he says. “Even small inconsistencies can erode trust.”

AI-Led Discovery and Experience

Perhaps the most transformative force shaping 2026 will be the evolution of buying journeys themselves. Govindu sees the rise of AI-led and agentic commerce as a major inflection point.

“Conversational platforms and AI-driven assistants will increasingly influence discovery, purchase, fulfilment and post-sales experiences. What earlier happened across multiple touchpoints is now beginning to happen in one place,” he says.

This convergence amplifies the importance of content-led discovery, owned data and deep consumer understanding. Brands that can unify storytelling, commerce and service into a coherent narrative are more likely to build loyalty in an environment where switching costs are low and alternatives are abundant.

Whether growth comes through D2C websites, marketplaces, quick commerce or offline stores, experts agree that the real differentiator will be a brand’s ability to build durable consumer relationships. As investors shift focus from short-term metrics to long-term value creation like retention, margins and brand strength, the next phase of India’s D2C story is less about rapid expansion and more about refinement.

(Published in Entrepreneur India)

Saumyangi is a Senior Correspondent at Entrepreneur India with over three years of experience in journalism. She has reported on education, social, and civic issues, and currently covers the D2C and consumer brand space.

admin

December 29, 2025

Yash Bhatia, Impact Magazine

29 December 2025

App, Tap, Pay and Zoom it’s delivered – that is Quick commerce for you. And in India, the narrative has so far been defined by speed, scale, high SKU counts, and the dominance of dark stores. Last week, however, Instamart nudged that model by opening an experiential store in Gurugram, allowing consumers to see and feel select products available on the platform.

The Bengaluru-based company has positioned the outlet not as a conventional retail store, but as a compact experiential format with a sharply curated assortment of around 100–200 SKUs, compared to the 15,000–20,000 SKUs typically housed in a dark store. Spanning roughly 400 sq. ft., the space is about one-tenth the size of a standard 4,000 sq. ft. dark store.

Under this model, sales proceeds are paid directly to sellers. This differs from Instamart’s regular arrangement, where payments are routed through the platform and later settled with sellers after deducting the platform’s share. IMPACT reached out to Instamart for further details, but the company declined to comment.

Sources close to the development say that Instamart has enabled sellers to open branded experiential stores in and around residential societies as part of a targeted consumer experiment. These are not conventional retail outlets, but compact experiential formats with a highly curated SKU assortment, focused on categories where consumers prefer to assess the products first-hand before purchasing, such as fresh fruits, vegetables, pulses, new product launches, and selected D2C brands. The initiative is largely centred on fresh categories and allows sellers to experiment with Instamart’s branding and service ecosystem.

Devangshu Dutta, Founder, Third Eyesight, a retail consultancy firm, says that physical presence plays a vital role in anchoring trust, particularly in premium products, groceries, and fresh produce. “Experiencing a product or brand physically can significantly enhance perceived value and help create stickiness. For this reason, offline stores continue to remain integral to the consumer products sector,” he explains.

Built on the promise of speed and convenience, quick commerce brands have come under growing scrutiny for quality and hygiene lapses at dark stores. Over the past year, several reports have flagged issues ranging from poor storage conditions and compromised freshness to the sale of expired or damaged products, particularly in food and grocery categories.

In some instances, regulatory inspections have led to licence suspensions after authorities identified hygiene violations at fulfilment centres. “Trust is what builds loyalty, and the shift is clearly moving from minutes to confidence,” says Shankar Shinde, Co-Founder, Aisles and Shelves, a behaviour-led brand consultancy in India. Shinde adds that the emergence of offline formats such as Instamart’s physical store aligns with this transition, particularly in grocery and fresh categories where consumers place a high premium on quality and consistency. “Physical touchpoints help reduce consumer anxiety, especially in a market like India, where shoppers still prefer hand-picked fresh produce such as fruits and vegetables,” he explains.

Against this backdrop, the opening of experiential centres could emerge as one way for quick commerce players to rebuild consumer trust by allowing shoppers to experience products in person before purchasing. IMPACT also reached out to Blinkit and Zepto for their views, but both declined to comment.

Kushal Bhatnagar, Associate Partner, Redseer Strategy Consultants, believes the move is aimed at unlocking incremental growth by tapping into offline-first consumers who are not yet active on quick commerce, while also catering to the offline purchase missions of existing quick commerce users. He notes that quick commerce currently reaches only about 75–80 million annual transacting users as of CY2025, even as over 90% of India’s grocery consumption continues to take place offline.

Beyond expanding reach, Bhatnagar sees offline formats as a way to address deeper trust barriers within the category. He adds that such formats can help deepen consumer confidence, particularly in categories where apprehensions around quality and freshness persist in quick commerce deliveries, concerns that are partly alleviated when consumers can experience products first-hand. Additionally, he points out that this approach benefits brands, especially emerging ones that are largely confined to quick commerce or a limited set of platforms, by giving them greater physical retail visibility without requiring heavy investment in traditional distribution networks.

Viewed through a financial lens, the move also carries implications for how quick commerce platforms justify value. Saurabh Parmar, fractional CMO, believes the initiative signals a shift from promise to performance, with a stronger emphasis on optimisation and a more realistic assessment of long-term value creation. He notes that while quick commerce has expanded into Tier 2 markets and seen growth in user numbers, these metrics alone still fall short of fully justifying current valuations. In this context, an offline presence becomes another lever to strengthen the overall business case.

At the same time, Parmar cautions that offline formats cannot replace the core proposition of quick commerce. He adds that experiential centres enhance brand credibility and make quick commerce feel closer to conventional retail, with the potential to eventually extend into other facets of e-commerce. However, he emphasises that quick commerce must continue to remain the frontline, as the sector’s valuations are fundamentally anchored in its speed-led proposition.

Retail experts, meanwhile, view physical touchpoints as a long-standing mechanism for building trust rather than a structural shift.

Dutta adds that such formats complement existing digital trust mechanisms such as delivery consistency, speed, ratings, and reviews by making brands feel tangible and accountable rather than abstract.

Bhatnagar notes that quick commerce currently has an average monthly transacting user base of around 40 million as of CY2025, leaving significant headroom for growth when compared to India’s overall e-commerce base of nearly 300 million active transacting users.

Beyond expanding the user base, he adds that experiential stores can also support wallet-share expansion across categories, which remains a key growth lever for the sector. “Non-grocery segments such as beauty and personal care, electronics, and fashion currently contribute about 25% of quick commerce GMV (Gross Merchandise Value), a share that is expected to rise further. Within groceries as well, platforms can drive incremental growth by building greater depth in fresh produce and staples,” Bhatnagar highlights.

From an operational perspective, however, the offline format is viewed more as a supporting layer than a core growth engine. Dutta sees Instamart’s offline presence as an experimental add-on rather than a replacement for its delivery-led model. The operating processes and economics differ significantly from those of quick commerce delivery, positioning physical formats as a complement to the speed proposition rather than an alternative. If the model proves viable and is backed by sufficient resources, it could eventually lead to a parallel scale-up of dark stores and experiential formats across different catchments.

For now, Instamart’s offline foray remains a tightly scoped experiment rather than a strategic pivot. Its significance lies less in square footage and more in what it signals about the evolving priorities of quick commerce. As the category matures, speed alone may no longer be sufficient to secure trust, loyalty, or long-term value. Experiential touchpoints, if deployed selectively, could help platforms bridge the gap between digital convenience and physical reassurance, particularly in categories where quality perception continues to remain fragile.

(Published in IMPACT)