admin

December 23, 2021

Devika Singh, Moneycontrol

December 23, 2021

Male grooming products startup The Man Company, known for its online-first strategy, is looking at offline expansion for its next leg of growth. The company, which operates 28 exclusive brand outlets in the country, plans to launch 60-70 more stores by the end of this fiscal to gain presence across at least 100 locations.

“A lot of growth will come from the offline channel for the next one year at least, especially in Tier II and III cities where launching exclusive stores is a good way to introduce the brand to the consumer as shopping malls are weekend destinations there,” co-founder Hitesh Dhingra told Moneycontrol.

The company, backed by fast-moving consumer goods (FMCG) major Emami which holds a 48.49 percent stake in it, is also looking at introducing its products in more multi-brand outlets. The Man Company is present in 1,200 multi-brand outlets which include lifestyle stores such as Shoppers Stop, Central and Lifestyle as well as hypermarkets, supermarkets and pharmacies. The company plans to be in 2,500 multi-brand outlets by the end of financial year 2022-23.

It currently draws about 70 percent of its sales from online channels including its own direct-to-consumer (D2C) platform and online marketplaces and 30 percent from offline channels. The startup’s strategy is focused on expanding its base in Tier II cities and beyond, which account for 50-55 percent of its sales even on online marketplaces.

“Out of our 28 exclusive brand outlets, only five to six are in top 10 cities and the rest in Tier II and smaller towns. For the new store openings also, we are going to adopt a similar strategy and only 10 percent of the new outlets will be in large cities,” said Dhingra.

The offline way

Several D2C brands have been eyeing the physical retail channel as they try to scale up and tap a wider set of consumers. Brands in the women’s beauty and personal care segment such as Mamaearth, Sugar Cosmetics and Plum Goodness are expanding their presence in the offline retail format. Plum, for instance, is looking to launch 50 exclusive brand outlets in the next two years.

Male grooming startups, too, are following a similar trajectory. For instance, Bombay Shaving Company and Baeardo are launching their products in more and more offline stores.

Devangshu Dutta, chief executive of retail consultancy Third Eyesight, said it makes sense for digitally-native companies that have achieved some brand recognition to launch in offline format for the next phase of growth. Brands in the 1990s for example, he said, who wanted to establish an identity, entered new formats or channels besides the existing ones. Similarly, digitally-native brands need not restrict themselves to online platforms alone, he added.

But he pointed out that these brands will have to address challenges such as ensuring availability of their products in offline channels. “In the online segment, companies can cater to customers with limited stocks. However, in the offline channel, they need to ensure availability of products across stores,” he said.

New categories

Apart from new retail categories, The Man Company has plans to enter categories such as sexual wellness and personal appliances. It has tied up with a marketplace for the launch of personal appliances such as beard trimmers and shavers and the category will be launched exclusively on the platform. The sexual wellness products, too, will be introduced on its D2C platform and later to other marketplaces and offline stores.

“We always launch a product on our platform to test it and get consumer feedback and, based on the response, we introduce the product to the wider market,” said Dhingra.

Launched in 2015, The Man Company caters to the men’s grooming segment and claims to have developed more than 65 stock keeping units. According to Dhingra, the company which competes with Beardo, Bombay Shaving Company and Ustraa will double its sales to Rs 100 crore by the end of this financial year.

Male grooming startups have of late attracted attention from FMCG companies. Marico last year completed the acquisition of Ahmedabad-based Beardo by buying an additional 55 percent stake in the company. It had acquired an initial 45 percent stake in 2019. British consumer goods giant Reckitt Benckiser Group invested Rs 45 crore in Bombay Shaving in February 2021. LetsShave and Ustraa are backed by Wipro Consumer Care.

According to industry estimates, the male grooming market in India was valued at Rs 15,806 crore in 2019 and is expected to cross Rs 36,402 crore by 2025, growing at a compound annual rate of 15-14 percent. Though growth was hit by the pandemic, experts are still bullish about the segment.

(Published in Moneycontrol)

Devangshu Dutta

September 28, 2017

In recent decades, the dependence on established medical disciplines has begun to be challenged. There is the oft-quoted dictum that healthcare sector tends to illness rather than health. Another saying goes that some of the food you eat keeps you in good health, but most of what you eat keeps your doctor in good health. With a gap emerging between wellness-seekers and the healthcare sector, so-called “alternative” options are stepping in.

Some of these alternatives actually existed as well-structured and well-documented traditional medical practices for thousands of years before the introduction of more recent Western medical disciplines. This includes India’s Siddha system and Ayurved (literally, “science of life”), which certainly don’t deserve being relegated to an “alternative” footnote. Ayurved is also said to have influenced medicine in China over a millennium ago, through the translation of Indian medical texts into Chinese.

Other than these, there are also more recent inventions riding the “wellness” buzzword. These may draw from the traditional systems and texts, or be built upon new pharmaceutical or nutraceutical formulations. Broader wellness regimens – much like Ayurved and Siddha – blend two or more elements from the following basket: food choices and restrictions, minerals, extracts and supplements, physical exercise and perhaps some form of meditative practices. Wellness, thus, is often characterised by a mix-and-match based on individual choices and conveniences, spiked with celebrity influences.

A key premise driving the wellness sector is that modern medicine depends too heavily on attacking specific issues with single chemicals (drugs) or combinations of single chemicals that are either isolated or synthesised in laboratories, and that it ignores the diversity and complexity of factors contributing to health and well-being. The second major premise for many wellness practitioners (though not all!) is that, provided the right conditions, the body can heal itself. For the consumer the reasons for the surge in demand for traditional wellness solutions include escalating costs of conventional health care, the adverse effects of allopathic drugs, and increasing lifestyle disorders.

After food, wellness has turned into possibly one of the largest consumer industries on the planet. Global pharmaceutical sales are estimated at over US$ 1.1 trillion. In contrast, according to the Global Wellness Institute, the wellness market dwarfs this, estimated at US$ 3.7 trillion (2015). This figure includes a vast range of services such as beauty and anti-ageing, nutrition and weight loss, wellness tourism, fitness and mind-body, preventative and personalized medicine, wellness lifestyle real estate, spa industry, thermal/mineral springs, and workplace wellness. Within this, the so-called “Complementary and Alternative Medicine” is estimated to be about US$200 billion.

There are several reasons why “complementary and alternative medicine” sales are not yet larger. Rooted in economically backward countries such as India, these have been seen as outdated, less effective and even unscientific. In India, the home of Siddha and Ayurved, apart from individual practitioners, several companies such as Baidyanath, Dabur, Himalaya and others were active in the market for decades, but were usually seen as stodgy and products of need, and usually limited to people of the older generations and rural populations. In the West they typically attracted a fringe customer base, or were a last resort for patients who did not find a solution for their specific problem in modern allopathy and hospitals.

However, through the 1970s Ayurved gained in prominence in the West, riding on the New Age movement. Gradually, in recent decades proponents turned to modern production techniques, slick packaging and up-to-date marketing, and even local cultivation in the West of medicinal plants taken from India.

As wellness demonstrated an increasingly profitable vector in the West, Indian entrepreneurs, too, have taken note of this opportunity. Perhaps Shahnaz Husain was one of the earliest movers in the beauty segment, followed by Biotique in the early-1990s that developed a brand driven not just by a specific need but by desire and an approach that was distinctly anti-commodity, the characteristics of any successful brand. Others followed, including FMCG companies such as the multinational giant Unilever. The last decade-and-a-half has also brought the phenomenon called Patanjali, a brand that began with Ayurvedic products and grew into an FMCG and packaged food-empire faster than any other brand before! While a few giants have emerged, the market is still evolving, allowing other brands to develop, whether as standalone names or as extensions of spiritual and holistic healing foundations, such as Sri Sri Tattva, Isha Arogya and others.

An absolutely critical driver of this growth in the Indian market now is the generation that has grown up during the last 25-30 years. It is a class that is driven by choice and modern consumerism, but that also wishes to reconnect with its spiritual and cultural roots. This group is aware of global trends but takes pride in home-grown successes. It is comfortable blending global branded sportswear with yoga or using an Indian ayurvedic treatment alongside an international beauty product.

Of course, there is a faddish dimension to the wellness phenomenon, and it is open to exploitation by poor or ineffective products, non-standard and unscientific treatments, entirely outrageous efficacy claims, and price-gouging.

To remain on course and strengthen, the wellness movement will need structured scientific assessment and development at a larger scale, a move that will need both industry and government to work closely together. Traditional texts would need to be recast in modern scientific frameworks, supported by robust testing and validation. Education needs to be strengthened, as does the use of technology.

However the industry and the government move, from the consumer’s point-of-view the juggernaut is now rolling.

(An edited version of this piece was published in Brand Wagon, Financial Express.)

Devangshu Dutta

January 10, 2017

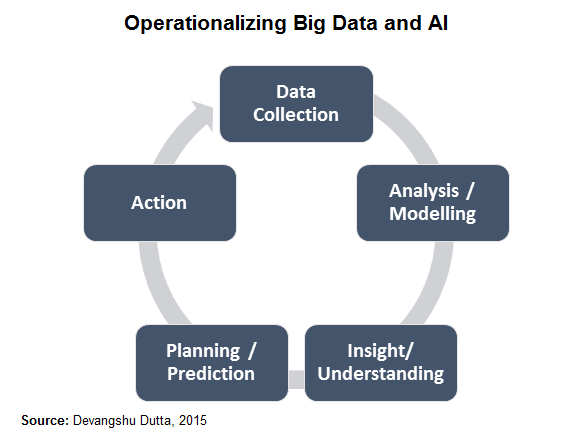

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

January 21, 2016

Aggregator models and hyperlocal delivery, in theory, have some significant advantages over existing business models.

Unlike an inventory-based model, aggregation is asset-light, allowing rapid building of critical mass. A start-up can tap into existing infrastructure, as a bridge between existing retailers and the consumer. By tapping into fleeting consumption opportunities, the aggregator can actually drive new demand to the retailer in the short term.

A hyperlocal delivery business can concentrate on understanding the nuances of a customer group in a small geographic area and spend its management and financial resources to develop a viable presence more intensively.

However, both business models are typically constrained for margins, especially in categories such as food and grocery. As volume builds up, it’s feasible for the aggregator to transition at least part if not the entire business to an inventory-based model for improved fulfilment and better margins. By doing so the aggregator would, therefore, transition itself to being the retailer.

Customer acquisition has become very expensive over the last couple of years, with marketplaces and online retailers having driven up advertising costs – on top of that, customer stickiness is very low, which means that the platform has to spend similar amounts of money to re-acquire a large chunk of customers for each transaction.

The aggregator model also needs intensive recruitment of supply-side relationships. A key metric for an aggregator’s success is the number of local merchants it can mobilise quickly. After the initial intensive recruitment the merchants need to be equipped to use the platform optimally and also need to be able to handle the demand generated.

Most importantly, the acquisitions on both sides – merchants and customers – need to move in step as they are mutually-reinforcing. If done well, this can provide a higher stickiness with the consumer, which is a significant success outcome.

For all the attention paid to the entry and expansion of multinational retailers and nationwide ecommerce growth, retail remains predominantly a local activity. The differences among customers based on where they live or are located currently and the immediacy of their needs continue to drive diversity of shopping habits and the unpredictability of demand. Services and information based products may be delivered remotely, but with physical products local retailers do still have a better chance of servicing the consumer.

What has been missing on the part of local vendors is the ability to use web technologies to provide access to their customers at a time and in a way that is convenient for the customers. Also, importantly, their visibility and the ability to attract customer footfall has been negatively affected by ecommerce in the last 2 years. With penetration of mobile internet across a variety of income segments, conditions are today far more conducive for highly localised and aggregation-oriented services. So a hyperlocal platform that focusses on creating better visibility for small businesses, and connecting them with customers who have a need for their products and services, is an opportunity that is begging to be addressed.

It is likely that each locality will end up having two strong players: a market leader and a follower. For a hyperlocal to fit into either role, it is critical to rapidly create viability in each location it targets, and – in order to build overall scale and continued attractiveness for investors – quickly move on to replicate the model in another location, and then another. They can become potential acquisition targets for larger ecommerce companies, which could acquire to not only take out potential competition but also to imbibe the learnings and capabilities needed to deal with demand microcosms.

High stake bets are being placed on this table – and some being lost with business closures – but the game is far from being played out yet.

Devangshu Dutta

July 22, 2011

The apparel retail sector worldwide thrives on change, on account of fashion as well as season.

In India, for most of the country, weather changes are less extreme, so seasonal change is not a major driver of changeover of wardrobe. Also, more modest incomes reduce the customer’s willingness to buy new clothes frequently.

We believe pricing remains a critical challenge and a barrier to growth. About 5 years ago, Third Eyesight had evaluated the pricing of various brands in the context of the average incomes of their stated target customer group. For a like-to-like comparison with average pricing in Europe, we came to the conclusion that branded merchandise in India should be priced 30-50% lower than it was currently. And this is true not just of international brands that are present in India, but Indian-based companies as well. (In fact, most international brands end up targeting a customer segment in India that is more premium than they would in their home markets.)

Of course, with growing incomes and increasing exposure to fashion trends promoted through various media, larger numbers of Indian consumers are opting to buy more, and more frequently as well. But one only has to look at the share of marked-down product, promotions and end-of-season sales to know that the Indian consumer, by and large, believes that the in-season product is overpriced.

Brands that overestimate the growth possibilities add to the problem by over-ordering – these unjustified expectations are littered across the stores at the end of each season, with big red “Sale” and “Discounted” signs. When it comes to a game of nerves, the Indian consumer has a far stronger ability to hold on to her wallet, than a brand’s ability to hold on to the price line. Most consumers are quite prepared to wait a few extra weeks, rather than buying the product as soon as it hits the shelf.

Part of the problem, at the brands’ end, could be some inflexible costs. The three big productivity issues, in my mind, are: real estate, people and advertising.

Indian retail real estate is definitely among the most expensive in the world, when viewed in the context of sales that can be expected per square foot. Similarly, sales per employee rupee could also be vastly better than they are currently. And lastly, many Indian apparel brands could possibly do better to reallocate at least part of their advertising budget to developing better product and training their sales staff; no amount of loud celebrity endorsement can compensate for disinterested automatons showing bad products at the store.

Technology can certainly be leveraged better at every step of the operation, from design through supply chain, from planogram and merchandise planning to post-sale analytics.

Also, some of the more “modern” operations are, unfortunately, modelled on business processes and merchandise calendars that are more suited to the western retail environment of the 1980s than on best-practice as needed in the Indian retail environment of 2011! The “organised” apparel brands are weighed down by too many reviews, too many batch processes, too little merchant entrepreneurship. There is far too much time and resource wasted at each stage. Decisions are deliberately bottle-necked, under the label of “organisation” and “process-orientation”. The excitement is taken out of fashion; products become “normalised”, safe, boring which the consumer doesn’t really want! Shipments get delayed, missing the peaks of the season. And added cost ends in a price which the customer doesn’t want to pay.

The Indian apparel industry certainly needs a transformation.

Whether this will happen through a rapid shakedown or a more gradual process over the next 10-15 years, whether it will be driven by large international multi-brand retailers when they are allowed to invest directly in the country or by domestic companies, I do believe the industry will see significant shifts in the coming years.