Devangshu Dutta

January 10, 2017

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

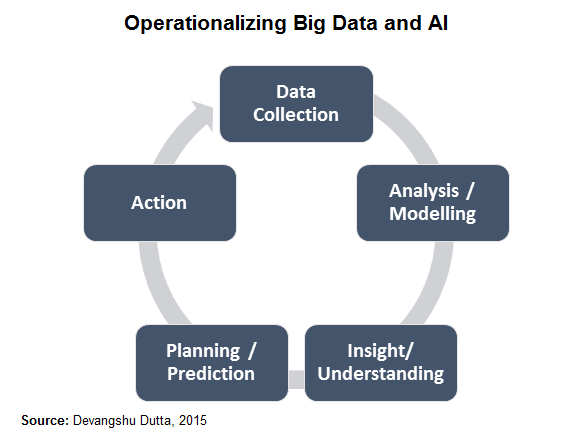

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

November 13, 2008

For all those who have admired the consistency and presentability of produce in western supermarkets, here’s proof that tough times really focus us on substance and force us to look beyond skin-deep beauty.

Even in fruits and vegetables.

British supermarket Sainsbury has challenged European Union guidelines that restrict the sales of fruits by certain physical standards. Sainsbury’s is questioning EU regulations that prevent selling “ugly” fruit and vegetables. Due to EU regulations such as size of cauliflower (minimum 11 cm diameter) and the shape of carrots (requirement that there should be a single root, not multiple), Sainsbury estimates that up to one-fifth of what is produced in British farms cannot be sold in the supermarket. According to Sainsbury’s estimate, not following these regulations can help to reduce prices by up to 40%, and reduce wastage by up to 20%. The retailer is also trying to drum up customer support by running an online poll (94% responses were in favour of Sainsbury’s move, at the time this column was being written).

So less beauty could mean more veggies in the supermarket, and more money in everyone’s pocket including, hopefully, the farmer.

And this may also vindicate anyone who has complained that the beautiful veggies and fruits in western supermarkets taste inferior to their “ugly” counterparts sold on Asian hand-carts. Give us more substance and less style, any day.

Let’s look at some other substantial issues that merchants should consider.

Remember “I can’t get no satisfaction”? That’s what Mick Jagger and his mates in the Rolling Stones hit the world in the face with in 1965, allegedly in response to the rampant commercialism they had seen in the US.

After 43 years – at least judging by the modern supermarket shelves – apparently we still ain’t getting no satisfaction. In fact, the array of choice tends towards “overload”.

A typical developed country supermarket is estimated to carry over 40,000 SKU’s. Can you think of 40,000 types of items (or even 10,000) that you would need from the supermarket for your home?

So here’s the result. During my travels, if I’m in a store that is unfamiliar I could spend over an hour wheeling a trolley around before reaching the checkout. The first 5-10 minutes are focussed on figuring out the aisles based on my list. The next 10 minutes are spent picking what is actually on my list. And the rest of the time before the checkout is usually spent browsing through the thousands of SKU’s and picking stuff that we never knew we needed when the family made the shopping list.

Now, the guys who run the supermarkets are generally a smart bunch – they’ve figured that the more options you put in front of consumers, the more they buy. My cash receipts are proof of that. But, as American professor and author Barry Schwartz (“The Paradox of Choice”) says, the point where the choice becomes counter-productive is already well-past in developed markets.

With such overwhelming choice, consumers get into analysis-paralysis. And even after they finally purchase something out of the enormous range, you get shades of post-purchase dissonance. Only, in this case the dissonance, the dissatisfaction is not related to a bad product, but: “What if there I had made another choice? What if there was a better product than this? What if there was something available for less?”

During these times, it is pertinent to also put this in the context of business costs. There is surely a cost of providing that humongous choice in supermarkets. Have we considered what the saving could be, if the variety was reduced, if the product range was consolidated?

Consider the time (and therefore cost) spent on product mix and pricing decisions – surely merchandising teams have to be larger if you have a larger product mix, since each person can only handle a finite workload. Consider the cost of logistics of handling a widely diversified range. Consider the efficiencies lost in diverse production mix. So, does the consumer really need, really even want all that choice?

Retailers like the German chain Aldi raise precisely those questions. Aldi sells about 1,100 SKUs compared to the usual 40,000. And it claims that the typical shopping basket in Aldi’s UK stores is 25% less than competing supermarkets.

Indian retailers, of course, are possibly yet to reach that pain threshold of choice. There are possibly some potentially useful choices that are still missing. But even here, it is well worth taking a hard look at the product offering. With availability levels that can dip as low as 50-60%, it is probably worth asking – what if we dropped XYZ product from our range? Would it really hurt our sales or even our image; or would it help us to focus better on the products that really matter?

If we took our attention away from building such false choices, could the business become more profitable and therefore more sustainable?

The US and European markets are often the source of many a management thought and business model related to consumer products and retail, and of “best practices”.

So, in closing, I should share this question someone asked me recently: “when do you think consumer spending will bounce back in the US?” My first response was, “If only I had a crystal ball”. But the next thought in my mind was what if US consumers actually came to a decision that they had “enough”? What if their excessive consumption was no longer the role model for consumers in emerging economies? What if, instead, the frugal consumers of India and China became the global role model?

What would your business model look like then? Would your corporate be more socially responsible? And would it have a better chance of lasting longer?

For those who are interested in taking this inquiry even further, I can recommend John Naish (“Enough: Breaking Free from the World of More”, 2008), John Lane, Satish Kumar, M. K. Gandhi, Alan Durning (“How Much is Enough?”), or any number of ancient Indian, Chinese, Greek or Roman schools of thought, many of them pigeonholed into “religious” or spiritual categories.

You might also like this video of a talk by Barry Schwartz on Ted.com (below).

Do please share the results of your inquiry with us, too.

Devangshu Dutta

September 14, 2008

You’ve walked into your neighbourhood supermarket with your shopping list. The particular detergent that your spouse had put on the list isn’t on the shelf and the sales associate is not sure whether they have any in stock (maybe you get the standard line: “whatever we have in stock is already on the shelf”).

You’ve forgotten your mobile at home so you can’t call to check whether a substitute brand or different pack size will suffice, so you walk out with the item still on your list.

And into the local kirana store. The brand and pack size that you were looking for isn’t there either, but the shop-owner says that he will have it in stock sometime during the next 3-4 hours, and can send it over to your home. Or, he suggests, you could also buy an alternative brand (or pack size). At the end of that conversation you would have very likely bought the alternative offered, or would have agreed to home-delivery of the item you were seeking. (A study by the Institute of Grocery Distribution in the UK in 2006 discovered that, in case of non-availability, 40% of the customers end up buying the same product somewhere else.)

Some people would be cheering, “Yea, more power to the underdog small retailer”. But the point of this example is not the victory of the local, independent kirana over the chain-store. The point I am illustrating is that the difference in the business models and formats of these two competitors, and the impact of on-shelf availability.

Modern convenience stores and supermarkets, and the format that is being largely adopted by the chain-stores in India, is the western model of self-service. Compared to the kirana-model of “being served”, modern retailers depend on product being available and visible on the shelf. Very clearly, visibility and availability drive sales.

And in the current environment, retailers are or should be looking at squeezing more sales out of their existing stores (see the earlier column – “Priority #1: Same Store Growth”).

On-Shelf Availability is driven by a number of factors – some are within the retailer’s control, while others are not.

On the vendor side, availability is driven by a number of factors. In India, vendors themselves can be small to mid-sized companies, with distribution systems that are poor in terms of information linkages. The supply chain may comprise of several levels of stockists, distributors, and wholesalers, with an inherent and in-built delay in information exchange. In this situation there is always a phase difference between demand (non-availability) and supply.

Other than the phase-difference, the order-fill rates at the vendor’s end can also be poor due to supply constraints. The quantity available in stock for a certain product at a regional or state level can frequently be lower than the requirement, and in such cases the manager, or the distributor, can end up allocating the available stocks.

These causes can lead to availability that is as low as 60-65% on average, even among the popular products. “Good” vendors can have supply rates of 85-90%, but even in these there is a high variance.

However, the interesting thing is that a very high proportion of stock-outs (around 75% according to the 2006 IGD study) can be attributed to problems within the individual store. These include poor in-store disciplines, lack of awareness of the impact of low availability, too much work for the sales associates or the lack of motivation.

(For instance, 35% of sales executives in British study did not plan to pursue retail selling as a long-term career. In a study carried out by Third Eyesight a few months ago, with retail was being seen as a “growth industry”, that figure in India was about 55% and was closely correlated with the frontline attrition rates being witnessed by Indian retailers.)

One of the critical factors in how on-shelf availability is handled is the very different perception various people have of its importance. The store manager or a sales executive may directly correlate lack of availability with lost sales (and lost incentives), while a category merchant may not find it as critical since he or she may be able to balance the margins through the mix of product and the aggregation of sales across stores. The first critical element to be fixed is to have a common view on the importance of availability communicated across the retail organisation.

The second important element is highlighting the visibility of stock within the store – isn’t it surprising that despite the small size of back-office space, how stock that is showing “on the system” can be so invisible?! The product may be stacked in inaccessible boxes, or may have just been kept in the wrong location.

On busy days and during busy hours, merchandise can arrive at the store and simply “disappear” off the radar for a few hours, since the staff may not have had the time to take the stock into the store’s inventory. It sits in the shipping boxes waiting for stock intake, which may well happen after the peak selling hours have passed.

Sometimes the availability issue comes up because the product is very popular, and it becomes virtually impossible to maintain a high availability during the critical selling windows – a typical example may be health and beauty products or popular snacks, where the aggregate availability may be high during the week, but abysmally low during the peaks. A key feature of these categories is also the large number of SKUs, which can be cause for substitutions in the supply chain, and therefore poor availability of a particular SKU.

On the other hand, fresh produce and dairy may show poor availability if daily reports are configured for end-of-day rather than beginning-of-day stock-checks, since fresh vegetables, fruit, fish and dairy may actually be taken into the store during the early hours in the morning.

Many people believe that the best way to tackle these issues is through information technology.

However, IT is only a tool that can enable a business if the processes are robust and people are attuned to a common objective.

The correct sequence, as for many other aspects of business, is to tackle the people issue first. Awareness and common understand can only happen through consistent communication and widespread training. (The 2007 study by IGD (UK) on this issue highlighted the fact that 61% of the sales associates had not received any formal training, while 23% had no communication about on-shelf availability.)

This communication needs to be not just within the organisation, but across the retailer and vendor relationship. This process is, unfortunately, not enabled by the very tactical and adversarial nature of the buyer-supplier relationship. Retail buyers don’t easily share point-of-sale information with vendors due to a variety of real and perceived barriers – confidentiality, power-issues, competitive pressures.

Fortunately, although it is still early days, chain-stores and vendors in India are already beginning to work together. Very often the exercise is actually being led by the larger, multi-national vendors who have been exposed to the concepts of Efficient Consumer Response (ECR) and Collaborative Planning, Forecasting & Replenishment (CPFR) – concepts that have been around for about 15 years.

However, these frameworks require a significant amount of joint business planning as well as point-of-sale visibility being provided to the vendor, and both of those aspects are still weak in the Indian modern retail ecosystem. Such degree of high transparency will only come in with further maturation of the retail businesses and the vendor relationships. Some of the modern retailers are already able to see consistent availability of over 90% through these efforts, and as word spreads, hopefully so will the practice.

Creating a culture of transparency and communicating the desired levels of availability is the foundation on which robust processes can be built for checking and reporting availability, which then can be enabled through technology. The correct sequence, therefore, is People-Process-Technology, and not the other way round.

In closing, let me show the other side of the coin (after all, this column is titled “Devil’s Advocate”!). The additional sales from better availability are very seductive, and can be very profitable, but up to a point. After a certain level, the law of diminishing returns takes over as the cost of maintaining high availability exceeds the additional margin. Particularly in perishables the possibility of product expiry and spoilage is quite high. Of course, during festive occasions there may be no option but to ensure high availability of perishables such as gift packs of snacks and packaged foods, even at the risk of spoilage or expiry.

Having said that, on the whole, modern retailers in India and their vendors do need to focus on on-shelf availability as a key area for increasing the productivity of the existing stores. For many stores, there is significant room an increase in sales. With real estate and operating overheads remaining high, every extra rupee of sales squeezed out of the current square footage will contribute directly to the bottom-line, a fact that Indian retailers cannot ignore today.