admin

February 18, 2026

Kartikay Kashyap, BrandWagon, Financial Express

18 February 2026

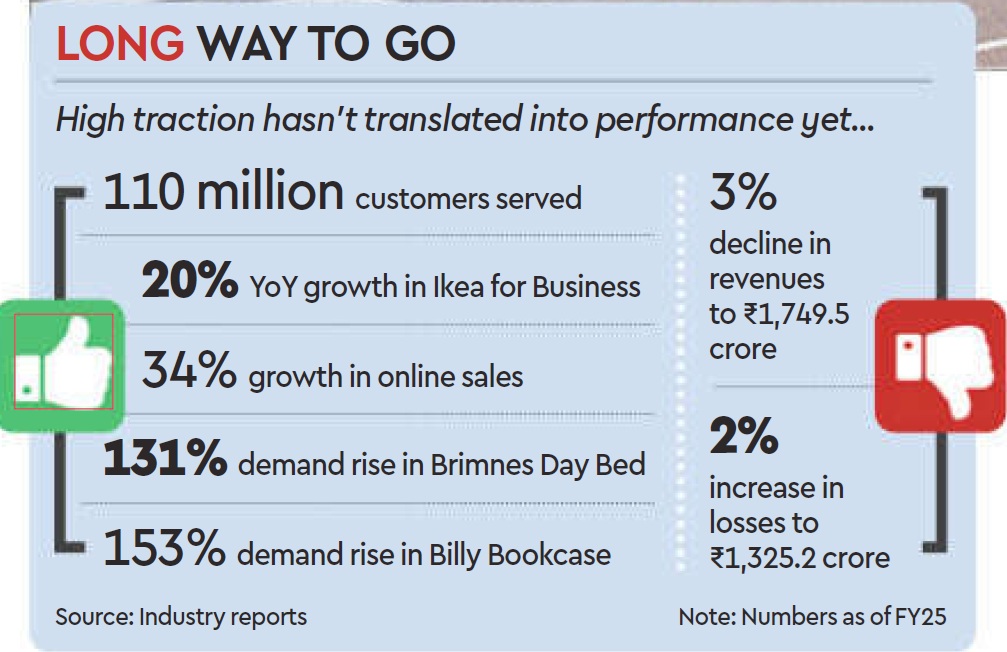

IKEA HAS BEEN around in India for about eight years, with another three years before that spent studying the market. It has developed a range that it deems “locally relevant-like the roti maker, the tava (pan), the belan (rolling pin), and the pressure cooker -which now constitute about 50% of the products it offers in the country. It has shifted its communication strategy to sync with local culture and fit into local spaces and has worked hard to beef up its omnichannel sales model with about 30% of its sales originating online. But profitability has remained elusive for the retailer whose global sales reached approximately €45billion in the 2015 financial year (FY25).

Just for context, the company’s India entity widened its losses by about 29 to 1,325.2 crore in the financial year ending March 31, 2025 (FY25). The revenue also dipped 3 to 1,749.5 crore from 1,809.8 crore in FY25.

So now the brand is taking a leaf out of its China playbook and tweaking its retail formats. Starting last year, it started piloting smaller store sizes ranging from 15,000-20,000 sq ft that are more cost-effective to set up and faster to integrate with its omnichannel model. “The goal is to create a simpler and more efficient shopping experience,” Ingka Group Retail Manager Tolga Oncu had said when the concept was unveiled last August.

Five months on, the furniture retailer is looking to take a step up the ladder – setting up new stores in the 50,000-70,000 sq ft range in the country, which will sit comfortably between its smaller stones (15,000-20,000 sq ft) and big box retail outlets (4 lakh sq ft), Adosh Sharma, country commercial manager at Ikea India told FE recently. Ikea’s broader plan also includes doubling its investments in the country to over 20,000 crore ($2.2 billion) over the next five years and improving local sourcing.

Will all this help the retailer grab a larger share of the highly fragmented furniture and furnishing market in the country? Will the brand achieve profitability in the next two years in keeping with its plans?

Ikea realises copy-pasting its global retail strategy in India is not going to work. That explains its recent moves to tweak store sizes and product design. Over and above the regular 5-M-L strategy, the fourth format the brand is developing comprises no-frills planning and order points, focused on customers who want to design homes or seek complex solutions without distraction.

“Smaller stores, which fulfill purpose-led needs will help them to get closer to their customers,” says Devangshu Dutta, founder & CEO, Third Eyesight.

The furniture and home decor segment has been up against slow purchase cycles in India. Smaller sized stores that are closer to residential arras might help step up the frequency of purchases. “Players are moving towards a higher purchase frequency strategy and smaller stores will help lkea cash in on this opportunity,” says Kushal Bhatnagar, associate partner, Redseer Consultant Strategy. He says quick commerce has helped improve the purchase cycle in the home decor space, and that is something Ikea will likely tap going forwand.

Dutta says Ikea has taken a long-term view on India and the investments in the pipeline is an indication of the opportunity that awaits players.

The brand claims it has served close to 110 million customers in FY25 across channels, and online sales are growing 34% compared to the previous fiscal. While furniture contributed the lion’s share of its revenue, the food business contributed 100% and Ikea for Business (tailored solutions for businesses) another 19% to its topline.

(Published in Financial Express)

admin

February 14, 2026

This episode of theUpStreamlife is a freewheeling conversation between Vishal Krishna and Devangshu Dutta, founder of Third Eyesight, with insights into the growth of modern retail and consumption in India, brand building and M&A, the balance of power between brands and retailers/platforms, sustainability vs growth and many other aspects, and is well-suited for founders and teams who want to be building for the long run in India.

admin

February 2, 2026

Sakshi Sadashiv, MINT

Bengaluru, 02 Feb 2026

BRND.ME, a roll-up commerce company, expects to complete its reverse flip (change of headquarters) from Singapore to India by March, clearing a key regulatory hurdle as it prepares to tap Indian public markets with an IPO.

Despite the rise of private labels from quick-commerce giants such as Swiggy Instamart and Zepto, CEO Ananth Narayanan remains confident. He argues that BRND.ME’s core categories—spanning complex, value-added products such as specialized haircare and niche party supplies—possess a level of brand loyalty and complexity that is difficult for generic retail labels to replicate. While private labels are currently displacing national brands in high-frequency, simple categories like dairy and staples, Narayanan believes the company’s core categories remain protected from this encroachment as they drive searches.

Having shifted its strategy from aggressive acquisitions to organic scaling, the company is now doubling down on its four largest brands: MyFitness (peanut butter), Botanic Hearth (haircare), Majestic Pure (aromatherapy), and PartyPropz (celebration supplies).

About 10-15% of BRND.ME’s India business currently comes from quick commerce, a channel the company plans to scale, Narayanan said. The company is the leader in party supplies on quick-commerce platforms, benefiting from impulse-driven demand. “People forget birthdays and anniversaries, so it’s a classic category to build a brand on quick commerce,” he said. The category contributes about ₹200 crore of revenue. The company also leads the peanut butter category through MyFitness, with a 30% market share on all quick commerce platforms and annual revenue of ₹270 crore.

The company’s revenue run rate stands at about $200 million. Male consumers worried about male-pattern baldness now account for about 35% of haircare sales. The company aims for a 10-fold jump in aromatherapy and haircare sales from $6 million to $60 million within four years, led by Majestic Pure and Botanic Hearth.

Drawing on his experience running Myntra, Narayanan said that private labels typically have a ceiling. “Even when we pushed hard on private labels at Myntra, they never went beyond 25-30% of the overall portfolio. That tends to remain the case as the categories we operate in are very hard to displace because we drive searches.”

This dynamic is already visible across several quick-commerce categories. The peanut butter segment is heavily consolidated on Blinkit, with Pintola and MyFitness together accounting for about 73% of sales, according to data from Datum Intelligence. Similar patterns have emerged in other categories. Blinkit’s popcorn segment, for instance, has rapidly consolidated into a duopoly, with 4700BC and Act II controlling 99% of sales.

Private labels muscling in

While Blinkit has consciously avoided launching private-label products on its platform, Swiggy has done so through Noice, and Zepto through Relish and Daily Good. For established brands, these private labels are becoming harder to ignore. Swiggy has scaled Noice aggressively, expanding the portfolio from about 200 to 350 stock keeping units (SKUs) and onboarding more manufacturing partners while moving beyond staples into categories such as beverages and ready-to-cook foods. These products are aimed at delivering significantly higher margins of 35-40%, compared with 10-15% on third-party brands, Mint reported earlier.

Private labels now contribute an estimated 6-8% of quick-commerce sales, up from 1-2% two years ago, according to data from 1digitalstack.ai, though penetration in perishables remains limited because of supply-chain complexity and quality concerns. A broader push into fresh categories could lift private-label share to 10-15%. Noice has already captured 3.4% of wafer sales and 1.9% of biscuit sales on the platform within months of its launch, according to 1digitalstack.ai data. The two categories are dominated by Lay’s and Britannia, which have a market share of about 35% each in their respective segments.

Zepto’s private-label push spans multiple everyday categories, including Relish for meat products, Daily Good for staples, Chyll for ice cubes and juices, and Aaha! for snacks, sweets, cereals and batters.

This growing presence creates a structural ‘trap’ for digital-first brands. Devangshu Dutta, chief executive at Third Eyesight, a consultancy firm, said, “Brands that are overly dependent on a single sales platform remain structurally vulnerable to being replaced by the platform’s own private labels, which are designed to capitalise on product opportunities that already have proven demand.” Platforms, he explained, tend to dominate high-frequency purchases, often undercutting brands on both price and visibility.

Persistently high online customer acquisition costs add to the pressure, particularly if the customer relationship is owned by the platform rather than the brand. “This has been one of the significant friction points for all digital-only brands, and weighs especially heavily on companies that have online-heavy portfolios with multiple brands in play,” Dutta added.

(Published in Mint)

admin

January 30, 2026

Vashnavi Kasthuril, MINT

Mumbai, 30 January 2026

Reliance Consumer Products Ltd (RCPL) plans to enter the bottled iced tea market this coming summer with the relaunch of “Brew House”, three people close to the development told Mint. The people added that the brand—for which the company received approval on 23 July 2025, according to the commerce ministry records—is expected to be relaunched within the next two months. The oil-to-retail conglomerate acquired the brand in 2024 for an undisclosed amount.

The iced teas will be launched in two flavours, lemon and peach, for an entry price of ₹20 for a 200ml bottle, according to two of the three people. “The product was initially supposed to be launched for ₹10 for a 200ml bottle, but after the goods and services (GST) recast, the ready-to-drink segment falls under the ~40% GST bracket, so the company decided to start with ₹20 instead,” said one of the three people, all of whom spoke on the condition of anonymity. RCPL did not immediately respond to Mint’s emailed queries. However, multiple distributors also confirmed to Mint that “Brew House” will launch within the next two months.

FMCG ambitions

Apart from relaunching Brew House, RCPL is also evaluating launching other niche-category drinks. RCPL is also working on several new concepts, such as kombucha, prebiotic sodas, and ayurvedic drinks. RCPL now has the focus and capability to build a specialized route to market for these kinds of offerings. RCPL’s larger ambition is to be a full-scale fast-moving consumer goods (FMCG) company, spanning categories across home care, food, beverages, and snacks, said the second person.

In August 2025, RCPL, the packaged consumer goods arm of Reliance Industries Ltd, acquired a majority stake in a joint venture with Naturedge Beverages Pvt. Ltd, the Mumbai-based company behind the herbal functional drink Shunya. Shunya offers zero-sugar, zero-calorie herbal beverages infused with Indian super-herbs such as ashwagandha, brahmi, khus, kokum, and green tea across India.

“When Reliance acquires a brand, one can be sure of product innovations, and you will see the same here,” said the third person. To be sure, the company has expanded its beverage portfolio to include a diverse range of beverages across mass and value segments, ranging from carbonated soft drinks under the Campa brand to packaged drinking water, sodas, mixers, energy and sports drinks, and traditional Indian refreshments such as nimbu pani, fruit beverages, and milkshakes. RCPL is also present in packaged foods through brands such as SIL, which sells noodles and other staples.

Brew House was launched in May 2017 by Siddhartha Jain under Positive Food Ventures Pvt. Ltd in Gurugram as a premium ready-to-drink iced tea brand positioned as a healthier alternative to carbonated and sugar-heavy beverages. It differentiated itself through real, whole-leaf brewing, lower sugar content and the absence of preservatives. Targeting urban, health-conscious consumers, the brand initially built distribution through cafés, hotels, restaurants, multiplexes and airports before expanding into modern trade and online channels. Its portfolio included flavours such as lemon and peach, sold in 300-350ml glass or premium PET bottles priced at ₹40-80. Singapore-based Food Empire Group later acquired a majority-stake to scale operations, before RCPL acquired the brand in 2024 for an undisclosed amount.

“The relaunch has been a bit slow. It’s available in small batches at Reliance Retail stores for now, but the company’s waiting for the right product, price point, and strategy before scaling it up. Over 2025, the focus has been on building distribution through larger beverage categories and investing in back-end capabilities, including automatic brewing equipment,” said the third person. RCPL has focused on building distribution through larger categories first. It’s difficult for a small, standalone brand to create reach, but a broad portfolio allows scale. Once that foundation is in place, the company can create a separate vertical for niche beverages like iced tea, the person added.

The niche drinks market

The ready-to-drink (RTD) iced tea category in India has long been shaped by major multinational brands and legacy beverage players, though it has remained a relatively niche segment compared with carbonated drinks. Hindustan Unilever Limited and PepsiCo first introduced Lipton Ice Tea in the country in the early 2000s through a joint venture, but the product was pulled back after an initial launch as consumers at the time were not widely ready for iced tea. It was later reintroduced in select markets with PET bottle formats in flavours such as lemon and green tea variants in 2011.

Coca-Cola and Nestle’s joint venture, Nestea, also experimented with bottled lemon RTD iced tea in the early 2010s, initially available in 400ml packs at around ₹25, before its broader rollout was scaled back while the JV evaluated consumer feedback. Aside from multinational brands, Indian companies such as Wagh Bakri have sold iced tea products, including peach-flavour premix packs, retailing around ₹95-100 for 250gm sizes online, though these are often powder mixes rather than RTD bottles.

Currently, Lipton’s bottled RTD iced tea is available in 350ml packs online at roughly ₹60, while powdered iced tea mixes such as Nestle’s 400gm pouches are priced at ₹200-230. In contrast, RCPL’s relaunch of Brew House will be brought to market in 200ml PET bottles at ₹20, undercutting these legacy players and signalling an aggressive pricing strategy.

To be sure, RCPL used a similar strategic playbook when it relaunched Campa Cola, one of India’s once-iconic soft drink brands. Campa, first introduced in the 1970s and marketed with the slogan “The Great Indian Taste”, was a household name in the pre-liberalization era but faded in the 1990s after global giants Coca-Cola and PepsiCo entered the market. Reliance acquired the brand from Pure Drinks Group in 2022 for around ₹22 crore and formally relaunched it in 2023 with variants such as Campa Cola, Campa Lemon, and Campa Orange, initially through its own retail channels and then nationwide.

Reliance’s move into iced tea aligns with its broader FMCG and retail strategy of identifying categories with long-term growth potential, according to Devangshu Dutta, founder of Third Eyesight and co-founder of PVC Partners. While iced tea remains a niche within India’s overall beverage market, Dutta said it is seeing steady, organic growth, driven by the rise of cafe culture, increased eating out, and younger consumers’ demand for non-alcoholic alternatives. “Whether it’s consumed as a standalone iced tea or used as part of a cocktail or some kind of concoction, it’s a category that’s seeing increasing interest,” he said.

Reliance’s key advantage, Dutta added, lies in its distribution muscle and captive shelf space across its retail network, which allows it to scale new products more effectively than smaller, standalone brands. “Anything they put on those shelves and price well becomes an opportunity for growth,” he said, adding that the entry of a large player like Reliance is likely to expand the overall market rather than intensify competition.

(Published in Mint)

admin

January 17, 2026

Prachi Srivastava, Hindustan Times

January 16, 2026

We keep telling ourselves that 2026 will be the year of budgeting. So, we’ve cut back on weekend brunch, paused Zara hauls, are collecting every coupon code we can, and are furiously spinning the wheel of luck on every site’s pop-up box. One thing that’s making it a little easier: Mini-sized luxury.

We’ve been here before. India’s sachet and sample-size products have been so successful, they’re studied in business school. We’ve lived through the beauty-box-subscription revolution (we still have the empty pouches somewhere). We’ve sprung for discovery kits on Nykaa and Tira (those 7ml doses will never make a difference, but still…). But luxury in small sizes? In this economy, when we’re budgeting and still craving pick-me-ups, it’s an idea whose time has come.

Everyone’s doing fun-size now: There’s one-day-use SPF as a handbag charm, tiny tubes of mascara, three-spritz niche perfumes. There are advent calendars – 30-day boxed sets for December, promising big savings. But also tasting jars of chilli-oil, one-hour-burn micro candles, single-wash detergent pods, even a single-cup insulated flask for your morning brew.

They all have starring roles in What’s in My Bag videos and GRWM reels. “Mini-product content sees higher engagement because it’s visually satisfying,” says beauty influencer Preiti Bhamra (@PreitiBhamra). “The contrast of a big hand holding a tiny product instantly catches attention.” Minis are deliberately packaged in the same style as a full-sized product, for better brand recognition. They photograph better too. Plus, think of how many more treats can fit on a shelf or a handbag, if they’re a smaller size.

Thinking small

Minis used to be linked to the Lipstick Index. The uptick in small-luxury purchases has, for decades been a recession indicator – ostensibly because when finances feel uncertain, consumers tend to avoid big purchases and turn to smaller indulgences for an emotional boost. That’s no longer true. Small is now a category unto itself.

On top beauty sites, you can filter products by mini size (not Travel Size as they were once called). Korean and Japanese brands deliberately market “ampoule” sizes for single-dose products. Platforms such as Smytten sell only sample sizes. Gemz, a mass-market brand that hasn’t launched in India yet, is aimed directly at GenZ (as the name suggests). It sells bath products in single-use packs. Hang them on the shower rod, open one, add water, lather, rinse, repeat.

Retail and luxury analyst Devangshu Dutta notes that minis are just low-risk experiments in luxury. It “encourages consumers to try premium categories they might otherwise postpone”. Think about it: A full-size Maison Francis Kurkdjian perfume may cost more than a month of Uber rides, but its mini discovery set under ₹5,000 feels like reasonable adulting. A Jo Malone candle is basically an EMI for your nose — but the 35g version? Suddenly doable.

“Across beauty, fragrance, personal care and gourmet foods, minis help brands acquire new customers faster,” Dutta adds. “They rotate better on shelves, get tried more often, and build quicker loyalty.”

I feel so used

We don’t buy minis only because they’re practical. We buy them because they hit our emotional pressure points. Clinical psychologist Dr Prerna Kohli says that when life feels overwhelming, “a small treat feels manageable.” A tiny lipstick becomes a quick hit of “at least this feels good,” even when nothing else is going right.

“There’s also a cultural twist,” Kohli adds. Indians grow up on the idea of delayed pleasure — work first, reward later. Tiny luxuries flip that script. They’re permission to feel good now. “Choosing something beautiful reminds you that you still matter, without waiting for a milestone.” Women, particularly working women and caregivers, hesitate to invest in themselves. But a tiny serum? That feels “allowed.” Less money, less guilt, and far fewer explanations.

Tiny treats thrive in the kitchen, as young professionals find them easier to experiment with, than brimming jars of an unfamiliar flavour. Food creator Natasha Gandhi (@NatashaaGandhi) says that tasting sets, mini variety packs and weekend-use portions have been doing well in the gourmet and artisanal category as diners seek restaurant-style flavours at home, but don’t want to cook the same thing over and over. In smaller kitchens and cluttered pantries, they also feel practical. They sit “at the sweet spot of ambition, convenience and low commitment.”

Too tiny to thrill

Not all minis deliver value. A 7ml sunscreen sachet isn’t enough for a user to determine if it truly suits their skin. A one-meal condiment delivers flavour, not familiarity. Single-use homecare creates packaging waste, adds to clutter, and cost-per-use can quietly climb. Luxury shampoo and conditioner minis are largely “overrated,” says Bhamra — often more indulgent illusion than practical trial.

The real red flag appears when the buying shifts from enjoyment to emotional avoidance. “It becomes unhealthy when shopping is used to numb uncomfortable emotions,” cautions Kohli. The usual symptoms apply: Shopping in secret, adding to cart the same time every day, week or month – indicating shopping during cyclical low periods, overjustification for a purchase. “Enjoyment is fine. Distraction always circles back.”

Perhaps in an age of overwhelm, the new luxury isn’t about owning more, but about feeling steadier. “Sometimes people simply enjoy beautiful things in small forms,” says Kohli. “We’re allowed to like something just because it makes us smile.”