admin

February 11, 2026

Vaeshnavi Kasthuril, Mint

Bengaluru, 11 February 2026

Sales of winter wear were underwhelming for the second year in a row as an unusually delayed and milder winter disrupted demand for heavy winter wear, particularly in north and west India, executives at two of India’s top clothing retailers said. Initial optimism for a bumper season this year compounded the disappointment for retailers.

While early signs of a La Niña—a weather pattern typically known for bringing freezing temperatures to India—triggered some early buying in the previous quarter, the season remained unusually mild, leaving stores with a surplus of winter clothing. Excess rainfall and cyclonic activity during the festive period in parts of eastern and southern India further weighed on seasonal buying, compounding the pressure on winter sales which are typically front-loaded.

This slump is particularly painful because winter sales are the industry’s largest annual driver. These months coincide with India’s massive wedding season, when spending peaks. Together, they account for roughly 20% of total yearly revenue for apparel companies, according to industry estimates. India’s apparel market was estimated to be worth more than ₹1.9 trillion in FY25, of which 41% was organised, credit ratings firm CareEdge said in January 2026.

V-Mart: margin over volume

Lalit Agarwal, managing director of V-Mart Retail, said, “Northern India saw a delayed or milder winter initially, leading to dispersed demand for heavy winter wear. Winter demand was definitely delayed a little bit—it didn’t get lost, but it was erratic.” He added that while festive demand held up, “demand visibility was uncertain, particularly in winter-led categories, and we consciously chose to protect margins rather than chase volumes.”

V-Mart’s revenue grew a little over 10% year-on-year to ₹1,126.4 crore in Q3 from ₹1,023.7 crore a year earlier and ₹889.05 crore in the third quarter of FY24, but this growth was largely driven by wedding and festive-season clothing, executives at the company said.

Anand Agarwal, chief financial officer of V-Mart Retail, said despite forecasts of a strong, early winter, “peak winters were delayed across North and West India, leading to a lull post-Diwali.” He added, “While the festive period went off reasonably well, winter demand did not pan out as anticipated,” attributing the softer sales to fewer peak winter days and unusually warmer temperatures.

Despite the delayed demand, the company managed to avoid a build-up of unsold inventory during the quarter. “Inventory health remained strong despite the delayed winter, and in some categories we were even short of inventory,” said Anand Agarwal, indicating that the eventual dip in temperatures led to a sudden pick-up in demand in select winter categories rather than excess stock.

Winter-led assortments continue to account for a sizeable share of the company’s quarterly sales, underscoring its sensitivity to weather patterns. “Winter and pre-winter categories accounted for about 40-45% of the overall mix during the quarter, and this share rose to over 60% during peak winter weeks in December,” said Agarwal during the third-quarter earnings call. The higher share of winter wear sales during peak weeks helped cushion margins, even as volumes remained below expectations. Lalit Agarwal said the company refrained from aggressive discounting amid uncertain demand. “Higher full-price sell-through during the winter quarter supported margins, as we did not undertake aggressive discounting,” he said.

Vishal Mega Mart: the late recovery

Gunender Kapur, managing director and chief executive officer of rival Vishal Mega Mart, said delayed winters usually force retailers to push promotions to ensure that they don’t carry forward all that merchandise, because the next opportunity to sell it would be the following year.

Despite this, the company’s performance held up, he said, highlighting that winter sales achieved robust double-digit same-store growth for the entire season and the full quarter, effectively overcoming the sluggish demand during December. Kapur noted that demand for winter clothing increased significantly in January, adding, “Winter merchandise is still selling well, both in our stores and in other stores, we believe.”

Vishal Mega Mart reported revenue growth of about 17% to ₹3,670.3 crore in Q3 FY26 from ₹3,135.9 crore in Q3 FY25 and ₹2,623.5 crore in Q3 FY24, largely on the back of wedding and festive-season demand.

Kapur said the company was unsure whether there would be significant unsold winter merchandise at the end of the season, adding that maintaining pricing discipline helped protect profit margins. “Merchandise that sells in December typically fetches a higher price than January merchandise for winter because sales often begin by late December or early January,” he said. “In our case, there was no problem. We achieved same-store sales growth of over 10%, even with the winter merchandise we purchased for the autumn-winter season.”

V2 Retail: the outlier

In contrast, V2 Retail recorded strong performance in the third quarter, largely driven by winter wear. Revenue surged nearly 60% year-on-year to ₹929.2 crore in Q3 from ₹590.9 crore a year earlier. This is perhaps because V-Mart and Vishal Mega Mart are more concentrated in north and central India, where winter demand was more uneven this season, while V2 has a stronger presence in eastern and north-eastern markets, including Bihar, Jharkhand, Odisha and Assam.

Managing director Akash Agarwal said the early onset of winter led to a “very good season” for the company. He noted that winter garments typically command a much higher average selling price (ASP) than summer products, which resulted in a visible bump in average bill value during the third quarter, led by higher sales of jackets and sweaters. Agarwal said this high-ASP, high-margin category accounted for the bulk of Q3 sales and was a key driver of the company’s same-store sales growth.

A worsening problem?

Two straight years of sluggish sales because of erratic winters highlight broader challenges around climate change for apparel retailers, which peg their inventory based on weather patterns and demand.

“Seasons have always been inherently unpredictable, and retailers have never been able to forecast with certainty how cold or warm a winter will be or how long it will last,” said Devangshu Dutta, founder of Third Eyesight, a consulting firm. However, he said that the challenge has intensified over the past 15-20 years as apparel businesses have scaled up and expanded their store footprints nationwide, stretching product development and supply chains over several months.

“No matter how hard you work on the plan, your forecast will always be wrong. You will either overshoot or undershoot,” Dutta said, adding that this leaves retailers grappling with either shortages or excess stock. Winterwear, he said, is particularly vulnerable because it has a higher value per unit, a much shorter selling window, and a smaller market, factors which together create a “humongous problem” for retailers.

Data from a World Meteorological Organisation report published on 16 January showed that 2025 was among the three warmest years on record worldwide, continuing a decade-long streak of exceptional heat despite the cooling La Niña phase. This is a clear sign that background warming from greenhouse gases is overwhelming natural variability, the report said. It suggested that climate change will intensify seasonal shifts and extreme weather in the years and decades ahead, making industries tied to seasonal patterns, such as winter apparel, increasingly vulnerable to unpredictable weather swings and weaker cold spells.

(Published in Mint)

admin

January 31, 2026

Surabhi Prasad, Business Today

Print Edition: 01 Feb, 2026

The last two years—2024 and, more notably, 2025—saw a wave of protests by a new generation of students and young professionals looking for political change, better economic conditions and more climate awareness across countries, including Bangladesh, Nepal, Indonesia and the Maldives.

But beyond these uprisings, Gen Z, the term used to describe those born in late 1990s to the early part of the 2010s and currently aged around 13-29 years, are not only questioning but also bringing forth changes in societal norms and economic behaviour. It’s not just a generation gap!

Gen Z are digital natives. They are tech savvy, have grown up with Internet in their homes, iPads as their support system, social media as a constant companion and take digital payments, online and quick commerce for granted. They tend to be night owls, the real gigsters, at home with artificial intelligence (AI) and machine learning, and with a lingo—cap, salty, suss and tea—that make others scratch their heads.

They also have newer challenges—rising unemployment, an uncertain economic environment, the rise of AI that has put a question mark on the future of work, climate change that is turning more real by the day, and skyrocketing real estate prices that mean a dream home could remain just a dream. Still, they are the rising consumer force who, over the next decade, are poised to become the largest chunk of the labour force and the focus of most companies.

For a country like India that is still young, Gen Z will soon be the economic force to reckon with. A recent report by not-for-profit think tank People Research on India’s Consumer Economy (PRICE) estimates that as of 2025, nearly one in five young individuals globally lives in India. “This is a formidable 420-million strong force, constituting approximately 29% of the nation’s total population, and made up of individuals aged between 15 and 29 as defined by India’s National Youth Policy (2014),” it said.

Labour sociologist Ellina Samantroy, Fellow at the V.V. Giri National Labour Institute, says India’s expanding Gen Z or youth workforce offers a significant opportunity for the country to reap the demographic dividend. As per the recent Periodic Labour Force Survey 2023-24, around 46.5% of the labour force is in the 15-29 age group. “There has been an increase in labour force participation in this age group from 42% during 2021-22. One can see the economic growth potential of this cohort,” she says.

However, with transitions and emerging opportunities in the world of work, it is important to harness the potential of this population cohort with adequate access to education and skilling, she says.

Devangshu Dutta, founder and chief executive of Third Eyesight, a boutique management consulting firm focused on the retail and consumer products ecosystem, says Indian Gen Z consumers are not a uniform cohort.

“A critical issue in India is the coexistence of aspiration and constraint, and India’s Gen Z are shaped by a mix of high digital exposure and wide economic disparity. While they are ambitious and globally aware, their purchasing power varies sharply across segments and locations,” he says.

Further, urban, higher-income Gen Z display global consumption behaviours such as brand experimentation, social commerce and premium aspiration, whereas a large proportion of Gen Z in Tier II, Tier III and rural India is highly value-driven and necessity-led, while drawing their inspiration from global and national sources. He also points out that unlike Millennials, Indian Gen Z are also entering the workforce in a more uncertain economic environment, making price sensitivity, smaller pack sizes and flexible payment options important. “Employment patterns such as informal jobs, gig work and delayed income stability are influencing consumption cycles and brand loyalty,” he says. There is a strong preference for digital discovery, vernacular content and peer-led recommendations, with trust built through community and relevance rather than legacy brand status.

Rising aspirations of Indian households and changes in consumption pattern with a marked move from essentials to more premium products have been well documented, most recently in Household Consumption Expenditure Surveys. But more granular, individual-level data from PRICE shows marked changes in education levels and behaviour of Gen Z and other cohorts such as Millennials (those aged between 30 and 45), Gen X (aged 45-60) and Baby Boomers (60+). A 2024 PRICE ICE 360 Survey of 8,200 respondents (18–70 years) in 25 major cities showed that Gen Z is the most educated cohort, spends the most time browsing the Internet and is more engaged with e-commerce and paid digital services.

Multinational and domestic companies are also now waking up to the Gen Z wave and are realising that they need to review strategies to gain the attention and loyalty of Gen Z as consumers and workers.

“Fashion, beauty and personal care, food and beverages, and mobile and consumer electronics are at the forefront of change in India,” says Dutta. Responding to Gen Z requirements, companies are designing products at accessible price points, expanding entry-level ranges and leveraging sachetisation and subscription models. Brands are investing more in regional languages, local influencers and platforms such as short-video and social commerce channels that resonate with young Indian consumers, he says.

But this process is still at a nascent stage, and many companies and analysts are still trying to assess this generation.

For the 34th Anniversary Issue, we at Business Today decided to decode what Gen Z is truly about, what influences them the most, what they aspire to purchase, what they can afford and what this means for India Inc. Over the course of the last few months, our newsroom saw animated discussions as senior editors sat down with younger colleagues to discuss lifestyle choices, brand loyalties and career ambitions, as we drafted an issue brief and a potential survey.

We then got in touch with PRICE, which worked with us on our survey objectives and tweaked the questionnaire. The result—a first-of-its-kind exercise where PRICE surveyed 4,311 Gen Z respondents, who are now entering the workforce with an income of their own, residing in metros and Tier II cities. The survey covered gender, education, employment status, personal income and household income classes. The main focus was urban, educated Gen-Z who has the income to be a strong consumer.

The research examined consumption behaviour across discretionary and essential categories, savings and credit attitudes, digital influence, brand loyalty, aspirations, and future spending intent.

And the results are indeed, surprising! The survey reveals that traditional consumption models that were built around age-based life stages, linear career progression and early credit adoption no longer hold for Gen Z. “This cohort’s behaviour reflects early exposure to economic shocks, greater career volatility and a redefinition of success away from speed toward resilience,” it underlines.

For businesses, misreading delayed demand as permanent weakness risks underinvestment just as Gen Z approaches its next consumption inflection, it warns. For financial services, premature credit push without trust-building will underperform. For consumer brands, price-led acquisition without quality consistency will fail to convert into lifetime value.

Delve into this issue where BT brings to you the in-depth findings of the survey and explains what this means for companies as they vie for a share of this growing consumer segment. Gen Z is not just about rizz and drip, it is giving the main character energy as they come of age.

(Published in Business Today, issue dated 1 February 2026)

admin

January 28, 2026

What does it actually take to build a fashion brand in India?

This panel (“Beyond the Noise- How D2c Fashion Brands Are Reinventing Retail”) at the 25th Edition of India Fashion Forum focussed on some real answers, in a refreshing, down-to-earth conversation moderated by Devangshu Dutta (Founder, Third Eyesight), with the founders of DeMoza (Agnes Raja George), The Mom Store (Surbhi Bhatia), Miraggio (Mohit Jain), BeyondBound (Tejasvi Madan), and Bari (Sameer Khan Lodhi).

No fluff, no “disrupting the industry” talk. Just founders being honest about what’s worked, what hasn’t, and what they’d do differently. A few things that struck a chord:

• Every single brand started because the founder couldn’t find something they personally wanted: inclusive activewear, affordable handbags that didn’t look cheap, good maternity wear. Sometimes the simplest observation is the best business idea.

• Inventory management came up often. One founder took their inventory cycle from 6 months down to 4. Another re-shuffles stock every 15 days based on what’s selling where. Unglamorous? Yes, but this is what actually keeps a business alive.

• The marketing conversation highlighted a move away from traditional advertising toward things that actually make people feel something. One founder talked about turning a farmhouse into a full “apricot colour” experience for customers. Another shoots content with real customers, not influencers.

• And the most memorable line of the whole discussion came from the most experienced founder in the room sharing a learning: “I won’t open stores fast.” No explanation needed, really.

Building a brand is exciting. Keeping it alive is the harder, quieter work. This panel was a good reminder of that. Worth a watch if you’re building something in this space.

admin

January 15, 2026

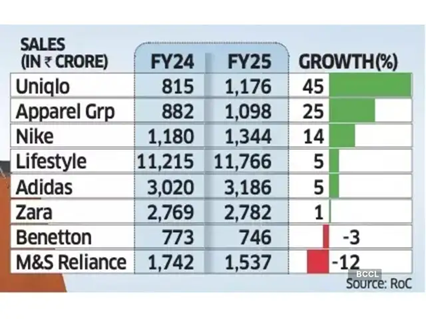

Sagar Malviya, ET Bureau

Mumbai, 15 January 2026

It’s mostly a tale of two halves for top western fashion labels in India after the runaway sales and retail expansion in the years soon after the pandemic.

While Marks & Spencer, Benetton, and Adidas are battling waning demand, Uniqlo and Nike are gaining fresh ground, reflecting wider choices and increasingly discerning buyers in one of the world’s fastest-growing consumer economies.

Spanish brand Zara is facing stagnant growth while it tapered off at Apparel Group, which sells Aldo, and Charles & Keith brands in India. Experts termed the divergent sales performance as a potential structural shift instead of demand slowdown in India’s fashion and lifestyle market.

Devangshu Dutta, founder of retail consulting firm Third Eyesight, said consumers have clearly shifted towards function, even as trend-led brands continue to exist though they tend to be comparatively smaller. Some brands are also finding it harder to set or even follow trends the way they once did.

“This is especially true for Gen Z, which stays closely tuned to global trends and acts as the primary driver of fashion adoption,” said Dutta. “While older consumers may have greater spending power in absolute terms, it is younger shoppers who shape trends and influence product sales.”

Growth slowed across most leading retailers and fast-fashion brands in the country in FY24 as high inflation and stagnant incomes crimped discretionary spending.

While the trend remained the same for many even in FY25, select brands staged a strong rebound. For instance, Nike India’s sales rose 14% in FY25, up from a 4% increase in the previous year, while Uniqlo accelerated growth to 45%, from 31% in FY24.

Revival after Festive Season

Even Lifestyle, India’s biggest department store chain, grew 5% last fiscal, rebounding from a 4% decline in FY24.

Uniqlo said it continues to see steady momentum in India, supported by strong customer response, retail expansion, rising brand awareness, and a strong ecommerce uplift. “India is now among Uniqlo’s fastest-growing markets in Asia and plays a meaningful role in the region’s overall business,” Kenji Inoue, chief financial officer and chief operating officer, Uniqlo India told ET. “The country’s young demographic, growing focus on quality, and increasing appreciation for functional everyday clothing have all contributed to this progress.”

According to the Retailers Association of India (RAI), sales growth in organised retail segments such as apparel, footwear, beauty and quick service restaurants (QSR) saw single-digit sales growth last fiscal year but the market has recovered after the festive season with double-digit sales performance.

“Demand has improved, but it isn’t broad-based,” said Kumar Rajagopalan, chief executive at RAI which represents organised retailers. “With more fashion options available, Indian consumers are becoming more selective, and growth is coming to brands that offer a strong value proposition and not the cheapest products, but those where prices are justified by innovation, design and quality.”

In FY25, Apparel Group recorded a 25% sales growth, slowing from a 37% increase a year ago. Inditex Trent, which sells Zara in India, saw flat sales compared with an 8% growth in FY24.

Adidas too saw its revenue growth rate slowing to 5% from 20% in the previous fiscal. Sales of M&S and Benetton fell 12% and 3% each, respectively.

Being the world’s most populous nation, India is an attractive market for apparel brands, especially with youngsters increasingly embracing western-style clothing. However, most international and premium brands have been competing for a relatively narrow slice of the sales pie in large urban centres.

(Published in Economic Times)

admin

January 7, 2026

Writankar Mukherjee & Shabori Das, Economic Times / Brand Equity

7 January 2026

There’s a renewed sparkle in the adage ‘Old is Gold’ at India’s biggest conglomerate Reliance. Banking on Indians’ nostalgia, it is hawking and reviving labels that once defined everyday life, Campa and BPL among them, to set its consumer venture’s cash registers ringing.

What started with sales of Rs. 3,000 crore in FY24, Reliance Industries’ fast-moving consumer goods (FMCG) business quickly accelerated towards Rs. 11,500 crore the following year. With a staggering Rs. 5,400 crore posted in the July to September FY26 quarter alone, the revival story is clearly striking a chord with consumers. But Campa, already the largest contributor to the Reliance Industries’ FMCG business, is only the beginning.

The company is injecting fresh life into acquisition of legacy brands such as Ravalgaon in confectionery and Velvette in personal care. Reliance is applying the same formula to the consumer electronics business, covering televisions, refrigerators and washing machines. Once a staple of Indian households, Kelvinator and BPL are being reintroduced.

Strategy Rings a Bell?

Driving this revival is a strategy Reliance knows well: aggressive pricing that is often 20 to 30% lower than competitors, offering generous trade margins to woo retailers, and a rapid expansion of distribution from its own stores to kiranas and local outlets, alongside local sourcing and an expanding product portfolio.

It’s a playbook that once created waves in the telecom market; this time, however, it comes with a generous dose of nostalgia.

The path ahead though may not be easy. While Campa may have yielded results in a category linked to instant gratification, electronics is a high-ticket, long-term purchase. Marketers are debating whether consumers in their 20s and 30s—spoilt for choice by global brands—would choose a Kelvinator refrigerator, a BPL TV or a Velvette shower gel over LG, Samsung, Dove or Fiama.

Deep Pockets and Retail Muscle

Reliance, experts say, has two advantages— its balance sheet and strong market presence with its own retail stores. “Reliance has the intent to dominate a market in whatever business it enters. Their brands in FMCG and electronics too have a more-than-decent chance of surviving and thriving,” says Devangshu Dutta, founder and chief executive of Third Eyesight, a consultancy in consumer space.

“As long as they have capital and management capability, they may cut their teeth,” he says.

The company is approaching the FMCG and electronics businesses in startup mode, but with deep pockets. As a Reliance executive explains, the strategy is to invest and invest more, gain market share, continue to absorb losses and after achieving scale, drive efficiencies to generate profit.

The path has been carved out. Reliance Consumer Products (RCPL), the FMCG business entity and what started as a unit of Reliance Retail Ventures, is now a direct subsidiary of Reliance Industries. This shift will help the company raise funds independently and eventually launch an initial public offering (IPO), and drive valuation independent of retail. The electronic business may follow suit as it grows in scale.

Reliance did not respond to Brand Equity’s queries.

Electronics: A Tough Play

Industry executives say the electronics foray will not be an easy battle against international brands. Global brands enjoy strong appeal in the Indian market, and companies such as LG, Samsung and Sony have been present for over two decades, cementing their position. Even the newer ones like Haier and Voltas Beko are rapidly gaining market share.

Pulkit Baid, director of the electronics retail chain Great Eastern Retail, says that unlike the cola industry, where two large players (Coca-Cola and PepsiCo) dominate, consumer durables are highly fragmented. “Kelvinator enjoys the brand heritage of an Ambassador car. But we will have to see if the brand is welcomed by Gen Z with the same euphoria as Campa.”

Industry veteran Deba Ghoshal notes that very few legacy brands have been able to withstand the onslaught of new-age brands in consumer electronics. Voltas (from the Tatas) and Godrej are exceptions, he adds.

“Reliance Retail has the strategic foresight to re-establish legacy brands in consumer durables space, instead of chasing a standalone private label business,” adds Ghoshal. “There is a strong opportunity in BPL and Kelvinator, provided they are re-launched with strong value and engaging emotive hooks, and not restricted to being a price warrior. Reliance has the capability; it just needs the right strategy.”

Reliance is readying campaigns for BPL and Kelvinator to connect with the younger consumers. The company is planning to re-launch them beyond Reliance Retail stores—targeting regional retail chains and e-commerce platforms and expanding quickly into smaller towns. With India’s electronics penetration still low—15 to 18% for flat-panel TVs, 40% for refrigerators, 20% for washing machines and less than 10% for air conditioners (ACs)—Reliance has substantial headroom for growth.

Angshuman Bhattacharya, partner and national leader for consumer products and retail at EY India, says Reliance may focus on tier two and three cities. “These markets have been a low priority for the Samsungs and LGs because they want to play in the premium segment where margins are higher. That is where Reliance may expand the market. It requires a lot of capital in terms of inventories and distribution, and Reliance has the ability and potential to do so.”

FMCG: Ball is Rolling

The FMCG push is gaining strong momentum. Reliance plans to double its distribution to three million outlets this fiscal.

Over the next three years, it looks to invest Rs. 40,000 crore to create Asia’s largest integrated food parks and has already invested Rs. 3,000 crore in manufacturing.

Isha Ambani, who spearheads Reliance’s retail and FMCG businesses, drew attention to Campa’s comeback at the company’s AGM in August: “Campa-Cola now holds double-digit market share across many states, breaking a 30-year MNC duopoly of Coca-Cola and PepsiCo. Campa Energy gained two million social media followers in just 90 days.”

Her target is bold: To reach Rs. 1 lakh crore in FMCG revenue within five years and become India’s largest FMCG company with a global presence.

Market watchers say such high ambitions require high investments. Kannan Sitaram, co-founder and partner at venture capital firm Fireside Ventures, said a company like Hindustan Unilever would set aside at least `30-40 crore to launch a brand. “Advertising and marketing alone would take up more than half of that. And when you are re-launching a brand which has not been around for a long while, the spending tends to be 25 to 30% higher in the initial three to four months,” he says.

Yet, analysts believe Reliance is in the consumer brands business for the long term. Bhattacharya says whatever Reliance has learned in this short time is meaningful and serious, something nobody else has managed.

Mover and Shaker

Competitors, including Tata Consumer Products, Dabur and PepsiCo’s largest bottler in India Varun Beverages, have acknowledged the turbulence created by Reliance in the FMCG sector. But the industry hopes low penetration levels will ensure there is room for everyone.

Varun Beverages chairman Ravi Jaipuria did not mince his words in the company’s latest earnings call in October-end: “They (Reliance) have woken all of us up and we are becoming more attentive… it is a very healthy sign for the country because our per capita consumption is so low that in the next five to 10 years, this market may double or triple…there is a huge room, and we see only positives in this.”

The revival of legacy brands and aggressive push into FMCG and consumer electronics indicates that Reliance is preparing for the long haul. In this fight driven by nostalgia, competitive pricing, deep pockets and distribution muscle, the battle for shelf space has just begun.

(Published in Economic Times/Brand Equity)