admin

June 12, 2026

Aanya Thakur & Writankar Mukherjee, Economic Times

12 June 2026, Mumbai/Kolkata

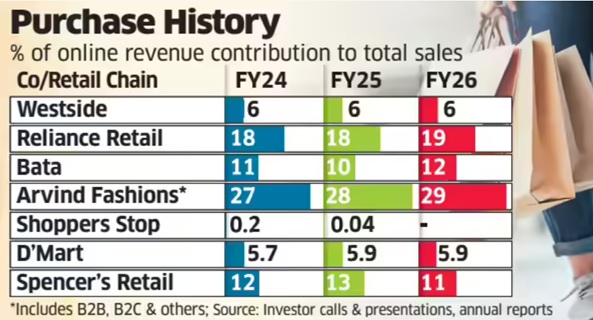

India’s leading retail chains have seen the share of e-commerce in total sales either remain flat or edge up by a sluggish 1-2 percentage points over the past four-five years despite a sustained push towards omnichannel retailing.

An ET analysis of eight major retailers-market leader Reliance Retail, Shoppers Stop, Westside, Arvind Fashions, DMart, Spencer’s Retail, Pantaloons and Bata-showed that the contribution of e-commerce to overall revenue has seen minuscule improvement since 2021-22 even as online sales continue to increase in absolute terms. By contrast, the Covid-19 pandemic spurred explosive growth, with the share of digital sales in total revenue surging three to four times in 2020-21 and 2021-22.

Industry executives attribute the slowdown partly to lower investment levels compared with pure-play digital firms such as Amazon, Flipkart, Swiggy and Blinkit-parent Eternal. Besides, retailers have consistently maintained that they will not pursue online growth at the expense of profitability, keeping prices largely aligned across online and offline channels.

The ET study found Tata-owned Westside’s online contribution stood at 7% in 2021-22 and thereafter remained around 6% till 2025-26. Reliance Retail’s online share ranged between 17% and 19% during the period, while Bata’s remained at 10-12%.

For DMart, e-commerce accounted for 5-6% of sales, while Shoppers Stop’s online arm, Shoppers Stop.Com (India) Ltd, contributed less than 1% to the consolidated revenue between 2021-22 and 2024-25. The company has not disclosed 2025-26 online sales figures yet.

“The DNA of these retailers is rooted in the physical world-infrastructure, processes and systems are not inherently designed for e-commerce, which requires a different operating model,” said Devangshu Dutta, chief executive of consultancy Third Eyesight.

“Most retailers calling themselves omnichannel are effectively multi-channel. Online retail is capital-intensive and hyper-competitive. Given the significant scope for physical store expansion, especially in tier-2 and tier-3 cities, retailers are reluctant to invest aggressively online,” he said.

Even so, Avenue Supermarts, which runs DMart, invested Rs 150 crore in online grocery platform DMart Ready this week, following a Rs 174-crore infusion a year earlier.

By comparison, Eternal infused Rs 2,600 crore into Blinkit in 2025 and another Rs 450 crore in March this year. Similarly, Swiggy approved a Rs 1,000-crore investment in supply-chain subsidiary Scootsy last year as both companies expanded their dark-store networks.

The chief executive of Aditya Birla-owned departmental chain Pantaloons, Sangeeta Tanwani, recently told analysts that online sales accounted for just 3-4% of the business. She said the company had earlier refrained from investing in the channel because profitability remained elusive.

“But over the last year, we called out omnichannel as one of our priorities… The reason why we had paused that business was because we wanted to make sure that we can get the unit economics right and make this business profitable… With all the shifts we have made this year, we feel confident of scaling up this business,” Tanwani said.

Reliance Retail, meanwhile, reported lower earnings before interest, taxes, depreciation and amortisation (EBITDA) margin growth in both the January-March quarter and entire 2025-26 as investments in quick commerce weighed on profitability. Chief financial officer Dinesh Taluja recently told analysts that margins depend on the pace at which online and business-to-business segments grow relative to the core offline business.

“If we slow down online growth, margins will improve. It is a mix as far as the online business continues to grow faster,” he had said.

An industry executive said the online contribution may go up modestly in this financial year due to high investment in scaling up dark stores for quick commerce.

Queries emailed to Reliance Retail did not elicit a response till press time. The company had in December last year appointed former Flipkart executive Jeyandran Venugopal as its new chief executive for the retail business.

(Published in Economic Times)

admin

May 25, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 25 May 2026

Value fashion retailers across the country are likely to face margin pressure in the upcoming quarters as rising crude oil prices are driving up the cost of polyester and other fabrics. Executives at V-Mart Retail Ltd, Vishal Mega Mart Ltd, and Kewal Kiran Clothing Ltd (KKCL) said crude oil-linked inflation has begun to push up yarn and sourcing costs across apparel and general merchandise categories, with the full impact expected to play out over the next few months.

Value fashion retailers face a double whammy: their heavy reliance on polyester and synthetic blends exposes them to crude-linked inflation, while their price-sensitive customer base leaves little room to pass on rising costs without hurting demand.

Apparel contributes about 22.8% of the overall revenue of the country’s largest retailer, DMart, in FY26. Rising polyester and fabric prices could also weigh on this share, which has been declining since FY20.

“We see almost 60% to 70% consumption of polyester yarn or poly-based product lines, which have or will get impacted,” said Lalit Agarwal during the company’s March-quarter earnings call. Agarwal said that yarn prices had already risen sharply in recent weeks. “There is a rise of almost 10% to 15% in the yarn prices, which effectively converts to almost 5% to 7% in the apparel prices,” he said.

“Cost increases are at multiple points. One, of course, is raw material, which is not only fabric, but also polyester buttons, thread, packaging, all of that,” Devangshu Dutta, founder of Third Eyesight, a consulting firm, said. “Because with value, you cannot really pass on the price hikes so readily to the consumer.”

Dutta said that lower- and middle-income consumers were already under financial stress from broader inflationary pressures, “so, they will not be able to absorb price hikes as easily as well.”

Ebitda margins in Q4FY26 are 10.9% for V-Mart Retail, 13.6% for Vishal Mega Mart and 19.1% for Kewal Kiran Clothing.

Double whammy for value segment

Gunender Kapur, CEO of Vishal Mega Mart, during the company’s March-quarter earnings call, said the inflationary impact had started becoming visible towards the end of April and would likely intensify in the coming months.

Despite rising input costs, retailers said they are avoiding broad-based price hikes on entry-level products amid fragile demand conditions in the value segment.

Entry-level products for these retailers range from ₹199 to ₹399, with some going up to ₹1,500.

“We would never tinker with the opening price points and the lower price points in these difficult times, because those are the customers who are the most vulnerable in inflationary situations,” Kapur said.

Hemant Jain, CEO of KKCL, said the company was willing to absorb part of the pressure on profitability to protect revenues and market share.

Jain also said the company had not yet implemented price hikes despite the inflationary environment.

To cushion the impact, companies said they are increasingly relying on cost optimisation, fabric innovation, premium fashion products and deeper expansion into smaller towns to sustain growth.

V-Mart said it was attempting to offset part of the inflation through alternative fabric usage, sourcing efficiencies and tighter inventory planning.

The retailer has also blocked orders in advance and is utilising existing yarn and fabric inventories available with vendors to soften the immediate impact of rising prices.

Vishal Mega Mart’s Kapur said it has revived cost-saving measures from the post-Ukraine cotton inflation cycle, including replacing cartons with gunny bags, removing polybags from some apparel categories, and shipping footwear without outer cartons.

The retailer has also increased the use of computer-aided design systems to reduce fabric waste during cutting.

Premium products, private labels offer buffer

These value retailers are also increasingly depending on premium and higher-fashion assortments, where consumers are relatively less price sensitive, to absorb selective price increases while keeping entry-level products affordable.

Kapur said Vishal Mega Mart’s large private-label portfolio, which contributes over 74% of its revenue, gives it greater flexibility to manage pricing pressure while maintaining discounts against national brands.

KKCL on the other hand, said it would absorb part of the inflationary impact rather than immediately pass on higher costs to consumers.

These retailers are also increasingly leaning on expansion into smaller towns and deeper markets to drive incremental growth as discretionary spending in larger urban centres remains uneven.

Value fashion retailers have underperformed the broader market amid growing concerns over rising input costs and margin pressure. Shares of V-Mart Retail, V2 Retail Ltd, Vishal Mega Mart and Kewal Kiran Clothing have fallen between 4% and 11% on a year-to-date basis, while the benchmark BSE rose 6.1% during the same period.

(Published in MINT)

admin

May 15, 2026

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving “imported inflation” and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below):

1. Dual Impact on Industry and Consumers:

2. Vulnerability of Small Businesses (SMEs):

3. Income vs. Expenditure Strain:

4. Ripple Effect of Crude Oil Beyond Logistics:

5. Shifts in Consumer Spending Patterns & “Shrinkflation”:

The panel noted that while the Reserve Bank of India (RBI) has adequate foreign exchange reserves to defend the rupee temporarily, the definitive solution relies heavily on the cooling down of global geopolitical tensions (such as the Middle East conflict affecting the Strait of Hormuz). Until then, Indian consumers will need careful financial planning and smart spending adjustments to navigate this inflationary phase. [Video below.]

admin

May 9, 2026

Writankar Mukherjee, Economic Times

Kolkata, 9 May 2026

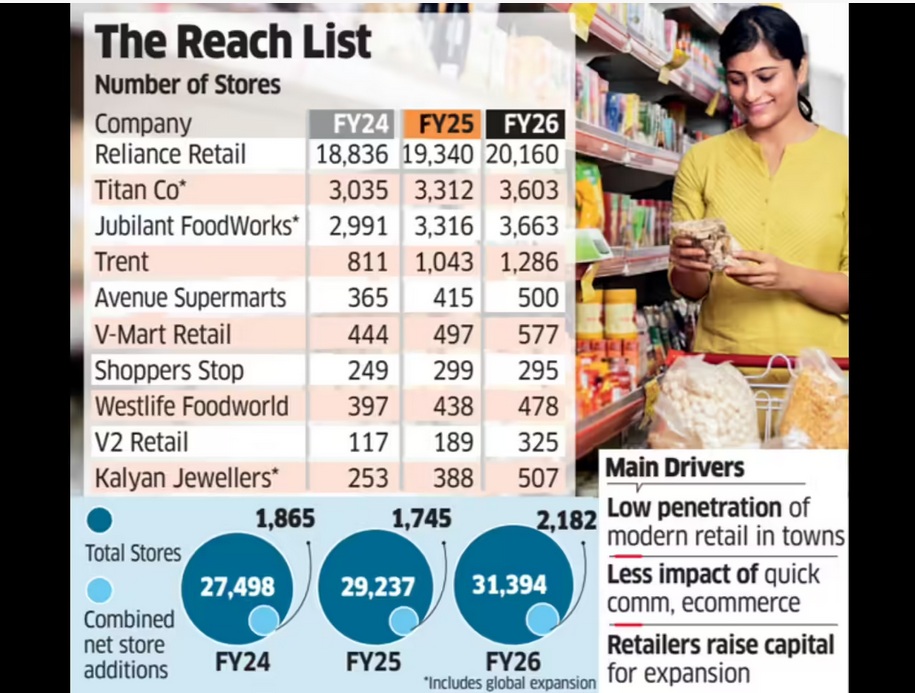

India’s top retail chains including Reliance Retail, DMart, Trent, Titan Company, Jubilant FoodWorks, and V-Mart Retail opened the highest number of stores in three years in FY26, seeking to capitalise on a demand recovery and a clean-up of unviable outlets added during the post-Covid revenge-spending period.

Entry into smaller towns and cities where many consumers continue to prefer shopping at physical stores over online is also influencing the expansion plans.

An ET study of the 10 largest listed retailers showed they added 25% more stores in the last fiscal year compared to FY25. Additions are on a net basis after accounting for loss-making outlet closures.

Collectively, the retailers added 2,182 stores in FY26, equivalent to six new stores a day on a net basis. In comparison, they added 1,745 stores in FY25 and 1,865 in FY24.

Retailers attributed the store expansion spree to improving consumer sentiment, helped further by cuts in income tax and goods and services tax (GST) rates last fiscal, along with low penetration of organised retail in smaller towns and cities. Together, the ten retailers had 31,394 stores operational as of March 2026.

Expansion Set to Continue

V-Mart Retail chief executive officer Lalit Agarwal said the ongoing shift from unorganised to organised retail is fuelling this expansion as several companies are meeting their sales growth expectations. “Many retailers have also raised capital, which they are deploying to grow topline,” he said, adding that the “growth phase will continue in the current fiscal as well.”

Companies surveyed by ET also include Shoppers Stop, Westlife Foodworld, V2 Retail and Kalyan Jewellers. Together, the ten retailers had 31,394 stores operational as of March 2026. Their combined store count grew 7% in FY26, ahead of a 6% expansion in the year before.

Reliance Retail alone added 820 net stores last fiscal, rebounding from a slowdown in FY25 when it shut several unviable outlets that were opened immediately post Covid, impacting overall industry growth rates. The country’s largest retailer had added 504 net stores in FY25, 796 in FY24, and 2,844 in FY23.

Similarly, Tata-owned Titan added 532 stores in FY23, but expansion moderated to 280-290 stores annually in FY25 and FY26.

India’s retail industry saw hyper expansion in late FY22 and FY23 as retailers sought to tap a boom in post-pandemic revenge shopping.

“Retail expansion now is more organic and measured as compared to the post Covid phase when there was a huge backlog of demand and over expansion,” said Devangshu Dutta, founder and CEO at Third Eyesight, a consultancy in consumer space.

(Published in Economic Times)

admin

February 27, 2026

Samar Srivastava, Forbes India

Feb 27, 2026

India’s young consumers are discovering the next big beauty serum, protein bar or sneaker brand not in a mall, but on Instagram reels, YouTube shorts and quick-commerce apps that promise 10-minute delivery. What began as a trickle of digital-first labels a decade ago has now become a full-blown wave. Direct-to-consumer (D2C) brands—built online, fuelled by social media and venture capital—have reshaped India’s consumer landscape and forced legacy companies to rethink everything from marketing to distribution.

India today has more than 800 active D2C brands across beauty, personal care, fashion, food, home and electronics, according to industry estimates and consulting reports. The Indian D2C market is estimated at $12–15 billion in 2025, up from under $5 billion in 2020, and growing at 25–30 percent annually. The pandemic accelerated online adoption, but the structural drivers—cheap data, digital payments and over 750 million internet users—were already in place.

Unlike traditional FMCG brands that relied on distributors and kirana stores, D2C brands such as Mamaearth, boAt, Licious and Sugar Cosmetics built their early traction online. Customer acquisition happened through performance marketing; feedback loops were immediate; product iterations were rapid.

Importantly, these brands are discovered online—but as they scale, consumers buy them both online and offline, increasingly through quick-commerce platforms such as Blinkit, Zepto and Swiggy Instamart, as well as modern trade and general trade stores. The omnichannel play is now central to their growth strategy.

According to Anil Kumar, founder and chief executive of Redseer Strategy Consultants, the ecosystem is maturing in measurable ways. Brands are taking lesser time to reach ₹100 crore or ₹500 crore revenue benchmarks and, once there, mortality rates are coming down. There is also an acceptance that if a brand is not profitable in a 3–5 year timeframe, that needs to be corrected. “There is a lot of emphasis on growing profitably and not just through GMV,” he says.

Big Cheques, Bigger Exits

The D2C boom would not have been possible without capital. Between 2014 and 2022, Indian D2C startups raised over $5 billion in venture and growth funding. Peak years like 2021 alone saw more than $1.2 billion invested in the segment. Beauty, personal care and fashion accounted for nearly 50 percent of total inflows, followed by food and beverages.

Some brands scaled independently; others found strategic buyers. Among the most prominent exits:

> Hindustan Unilever acquired a majority stake in Minimalist, reportedly valuing the actives-led skincare brand at over ₹3,000 crore. For Hindustan Unilever, the annual run rate from sales of its D2C portfolio is estimated at around ₹1,000 crore, underscoring how material digital-first brands have become to its growth strategy.

> ITC Limited bought Yoga Bar for about ₹175 crore in 2023 to strengthen its health foods portfolio.

> Emami acquired a majority stake in The Man Company, expanding its digital-first play.

> Tata Consumer Products acquired Soulfull as part of its health and wellness strategy.

> Marico invested in brands such as Beardo and True Elements.

Private equity has also entered aggressively at the growth stage. ChrysCapital invested in The Man Company; L Catterton backed Sugar Cosmetics; General Atlantic invested in boAt; and Sequoia Capital India (now Peak XV Partners) was an early backer of multiple consumer brands.

Valuations were often steep. boAt was valued at over $1.2 billion at its peak. Mamaearth’s parent, Honasa Consumer, listed in 2023 at a valuation of around ₹10,000 crore. Across categories, brands crossing ₹500 crore in annual revenue began attracting buyout interest, with deal sizes ranging from ₹150 crore to over ₹3,000 crore depending on scale and profitability.

Yet exits have not always been smooth. “While it takes 7-8 years to build a brand most funds that invest in them have a timeline of 3-5 years before they need an exit,” says Devangshu Dutta, founder of Third Eyesight, a retail consultancy. This timing mismatch can create pressure—pushing brands to scale aggressively, sometimes at the cost of margins.

Integration Pains and the Profitability Pivot

For large FMCG companies, buying D2C brands offers speed: Access to younger consumers, premium positioning and digital marketing expertise. But integration brings challenges.

Founder-led organisations operate with rapid decision cycles, test-and-learn marketing and flat hierarchies. Large corporations often work with layered approvals, structured brand calendars and rigid cost controls. Cultural friction can lead to talent exits if autonomy is curtailed too quickly.

Margins are another sticking point. In the early growth phase, many D2C brands spent 30–40 percent of revenue on digital advertising. Rising customer acquisition costs post-2021, combined with higher logistics expenses, squeezed contribution margins. As brands entered offline retail, distributor and retailer margins of 20–35 percent further compressed profitability.

Large acquirers, used to EBITDA margins of 18–25 percent in mature FMCG portfolios, often discovered that digital-first brands operated at low single-digit margins—or were loss-making at scale. Rationalising ad spends, optimising supply chains and pruning SKUs became essential.

The funding slowdown between 2022 and 2024 triggered a reset. Marketing spends were cut by as much as 25–40 percent across several startups. Growth moderated from 80–100 percent annually during peak years to 25–40 percent for more mature brands—but unit economics improved.

Quick-commerce has emerged as a structural growth lever. For categories such as personal care, snacking and health foods, these platforms now account for 10–25 percent of urban revenues for scaled brands, improving inventory turns and reducing dependence on paid digital acquisition.

The next phase of India’s D2C journey will be less about blitz scaling and more about disciplined brand building—balancing growth, profitability and exit timelines. What began as a disruption is now part of the mainstream consumer playbook. And as capital becomes more selective, only brands that combine strong gross margins, repeat purchase rates above 35–40 percent and sustainable EBITDA pathways will endure.

(Published in Forbes India)