admin

June 8, 2026

Arushi Jain, The Times of India

8 June 2026

Their faces have launched many campaigns and brought crores to the film industry. But can they sell a moisturiser as successfully? India’s beauty market is the hottest growth story globally, estimated to reach $40 billion from $23 billion (2026) and eyeing the fourth-largest spot by 2030 (currently at number seven).

Last month, Estée Lauder announced the buyout of Forest Essentials, one of India’s oldest, Ayurveda-based brands. In 2025, Hindustan Unilever acquired five-year-old skin and hair care brand, Minimalist. A 2025 McKinsey & Company x Business of Fashion survey found that 78% of global beauty executives see India as the most promising growth market. Even celebrities have shown up with chequebooks, but fans are no longer buying at face value.

While Hailey Bieber’s Rhode built a cult following through what she calls an “outside of the box” strategy, Deepika Padukone’s 82°E reported a 30% revenue dip in FY25. Nykaa is in talks to acquire a stake in the brand.

India’s consumer has evolved faster than the brands serving them. They are reading labels now, not just recognising famous faces on packaging. Star power, it turns out, only gets you so far.

Fame gets you in the door. Formulation keeps you there

If a celebrity is the invitation to the party, formulation is what keeps the guest at the after-party. Despite India’s celebrity beauty segment crossing an estimated `5,000 crore in GMV in FY24, scale has not translated into customer retention. The initial spike, familiar to anyone who has tracked a celebrity launch, gives way to an uncomfortable question: what brings a customer back?

“Celebrity isn’t necessarily a sustainable brand asset,” says Devangshu Dutta, CEO of retail consultancy Third Eyesight. “While celebrities can act as interest-creators and trial-generators, repeat purchases are built on functional reasons, not imagery alone.”

Founders echo the same reality from the ground. “Honestly, people come back for what works,” says Aashka Goradia Goble, co-founder of RENÉE Cosmetics. “If a product performs well, feels easy to use, is priced right, and becomes part of someone’s everyday routine, they’ll keep reaching for it.”

Price, too, remains a decisive filter. Sunny Leone, founder of StarStruck, says, “In India, price is the main component.” The journey from first purchase to loyalty is driven by habit, and habit, in beauty, is built on results.

Positioning over popularity

The gap between a viral campaign and a repeat purchase is wider than most A-listers realise. Brand guru Harish Bijoor locates the problem in what he calls the “spinal cord” of a brand: a single, clear positioning that holds the entire business together.

Rihanna’s Fenty is inseparable from its commitment to shade inclusivity. Kylie Jenner’s Kylie Cosmetics was built around one obsession: lips. “It is extremely important to understand what you want to be and focus on just one thing and not on everything,” Bijoor says. That clarity is precisely where most Indian celebrity beauty brands are still finding their footing.

The old playbook: launch a brand online, wrap it in the language of “clean” or “natural,” and wait for a global conglomerate to come calling has run its course. Today, strategic buyers and consumers alike want a brand that can stand on its own. The question is no longer whether a celebrity can generate awareness. It is whether the brand they have built can survive them.

What the labels that last have in common

The brands breaking through are doing so quietly and methodically. In a category where fame can spark interest but not always guarantee repeat purchase, Katrina Kaif’s Kay Beauty, launched with Nykaa in 2019, has emerged as one of celebrity beauty’s more consistent success stories.

The main reason is less about star power and more about strategy. “If you contrast Kay Beauty and 82°E (Deepika Padukone’s brand), Kay Beauty has two distinct advantages,” says Dutta. “Firstly, being priced for a much larger audience, and secondly, having the active participation of Nykaa across channels in terms of merchandising and visibility push for the brand.”

Nykaa is candid about what made the difference. “When we co-created Kay Beauty with Katrina, shade ranges and formulations designed for Indian skin tones and climate were severely limited,” a spokesperson shares, adding that the celebrity association “amplified the brand rather than substituted for it.” The strategy appears to have paid off: Kay Beauty is now a ₹500 crore-plus annualised GMV brand, with new launches contributing 21% of revenue as of Q3 FY26.

Why Indian skin demands more than a famous name

For Indian celebrity brands, the challenge is not just performance; it is perception. “Domestically, we see the mentality for buyers is to look at international brands first based on trust, and then try domestic brands based on lower price value,” says Leone.

Indian consumers are also highly specific in what they expect. According to market research firm Mintel, shoppers are increasingly drawn to formulations that are clinically tested and grounded in both science and local familiarity. Products must perform in Mumbai’s humidity and Delhi’s pollution and suit the full spectrum of Indian skin tones.

“Indian consumers love products that do more than one job, last long in our weather, and actually match Indian skin tones,” says Goradia. They are cautious spenders, she adds, but willing to invest when they see real quality and innovation.

Nykaa says this ingredient awareness is now visible across the country, not just metros. “Consumers are reading about niacinamide and retinol, they know what they want from a sunscreen, and are making considered purchase decisions. Brands need to earn their place on merit in every market,” says the spokesperson.

“A brand that addresses these needs well and remains within the customer’s budget succeeds,” says Dutta.

Gen Z will drive 50% of India’s beauty consumption by 2030

By 2030, Gen Z will drive 50% of India’s beauty and personal care consumption, a third of all sales will happen online, and per capita income is forecast to rise 138% in real terms by 2040, according to Euromonitor. Nykaa founder and CEO Falguni Nayar told Bloomberg that comparing India’s beauty routines to South Korea’s famed 14-step regimens is premature, “It is still day zero for beauty consumption in India.”

The global conglomerates have done the math. Estée Lauder, L’Oréal, and Puig are all moving deeper into India, betting on a consumer who is younger, more digitally fluent, and more ingredient-literate than any previous generation. The brands they are acquiring, Forest Essentials, Minimalist, Kama Ayurveda, share a common thread: They are built on something that exists independently of a famous face. “This is an industry that is very crowded and takes a lot of time to grow,” says Leone. “Western brands focus on global distribution and profit and loss. Not just turnover at a loss.” The celebrities who will build something lasting are the ones who understand that the launch is the easiest part. As Bijoor puts it: “Celebrity beauty is not skin deep at all. It is a deep brand science.”

(Published in The Times of India)

admin

May 27, 2026

Writankar Mukherjee and Aanya Thakur, Economic Times

Kolkata/Mumbai, 27 May 2026

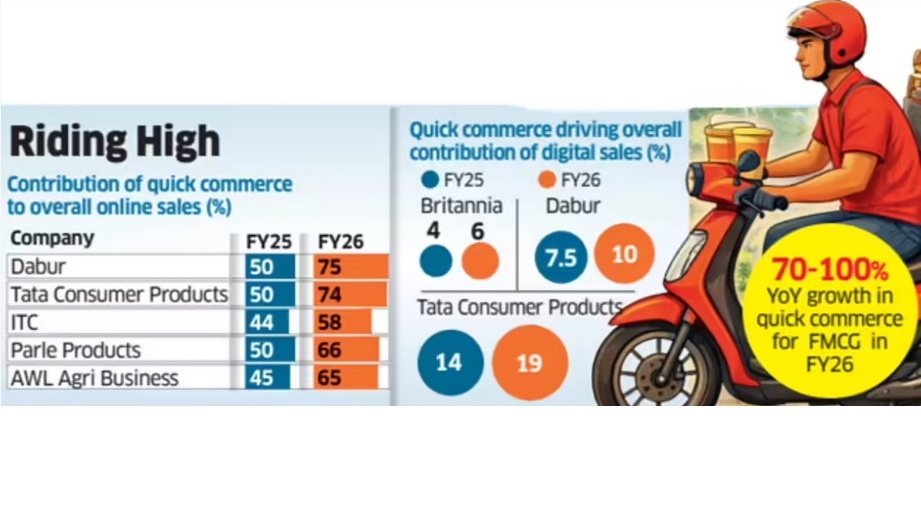

Quick commerce has become the dominant online sales channel for India’s top fast-moving consumer goods (FMCG) companies, with Dabur India and Britannia Industries among others now deriving up to 75% of their digital sales from 10-minute delivery platforms.

Industry executives said quick commerce is reshaping consumer buying habits and increasingly cannibalising sales from all other channels, including ecommerce platforms, modern trade and kirana stores, even as large online marketplaces and retailers expand into the segment.

Latest data from companies including ITC Ltd, AWL Agri Business, Tata Consumer Products and Parle Products showed quick commerce accounted for 60-75% of their total online sales in FY26, rising sharply from less than half a year earlier.

For Britannia and Tata Consumer Products, quick commerce now contributes more than 70% of online sales, while the share climbed to 75% for Dabur in the fourth quarter ended March from 50% in the December quarter.

Executives said expanding assortments and demand for instant replenishment are accelerating the shift. “Quick commerce has been gaining ground with several ecommerce companies such as BigBasket, Amazon and Flipkart, as well as retail chains like Reliance Retail, entering the space,” said Mayank Shah, vice-president at leading biscuits maker Parle Products. “Given consumers’ demand for convenience and immediate replenishment, quick commerce has emerged as a strong growth opportunity for them.”

Quick commerce accounted for 65% of online sales of Parle Products and AWL Agri Business last fiscal, compared with 50% and 45%, respectively, in FY25. ITC derived 58% of its online sales from this channel in FY26.

Frequent Purchases

Grocery-shopping are now centred around frequent top-up purchases through the week.

“Quick commerce has facilitated a grocery shopping habit which already existed – more frequent purchases. These companies are now also looking to improve profitability by expanding into higher-margin and impulse-driven categories,” said Devangshu Dutta, founder and CEO of Third Eyesight, a consultancy in consumer space.

While the channel is already significant for FMCG companies in the top 8-10 cities, it is expanding rapidly into smaller towns as operators such as Blinkit, Zepto and Swiggy Instamart widen their footprint.

Premium Push

The channel has also allowed companies to push premium products, executives said.

“While on marketplaces and traditional e-commerce platforms we were heavily skewed towards staples, the shift to q-commerce is helping us premiumise our assortment and sell far more indulgent categories,” Britannia Industries chief commercial officer Vipin Kataria told analysts earlier this month.

The transition has led to a threefold increase in sales of adjacency categories for the biscuits and dairy products maker, he said.

Kataria expects quick commerce’s contribution to the company’s total online sales to rise to 85% from 70% currently.

Most FMCG companies reported 70-100% year-on-year growth in quick commerce sales in FY26, making it the fastest-growing channel for the industry for the past two to three years. Executives expect the trend to continue.

Dabur India global chief executive officer Mohit Malhotra said beverages, foods, personal care and home care are currently the strongest-performing categories in this channel.

Saugata Gupta, managing director of Marico, said quick commerce is likely to be especially dominant in foods, while specialised ecommerce players such as Myntra and Nykaa remain strong in personal care.

The maker of Parachute, Saffola and Livon brands is strengthening its quick commerce supply chain through digitisation, automation and AI-based forecasting, Gupta said.

(Published in Economic Times)

admin

May 25, 2026

Vaeshnavi Kasthuril, MINT

Bengaluru, 25 May 2026

Value fashion retailers across the country are likely to face margin pressure in the upcoming quarters as rising crude oil prices are driving up the cost of polyester and other fabrics. Executives at V-Mart Retail Ltd, Vishal Mega Mart Ltd, and Kewal Kiran Clothing Ltd (KKCL) said crude oil-linked inflation has begun to push up yarn and sourcing costs across apparel and general merchandise categories, with the full impact expected to play out over the next few months.

Value fashion retailers face a double whammy: their heavy reliance on polyester and synthetic blends exposes them to crude-linked inflation, while their price-sensitive customer base leaves little room to pass on rising costs without hurting demand.

Apparel contributes about 22.8% of the overall revenue of the country’s largest retailer, DMart, in FY26. Rising polyester and fabric prices could also weigh on this share, which has been declining since FY20.

“We see almost 60% to 70% consumption of polyester yarn or poly-based product lines, which have or will get impacted,” said Lalit Agarwal during the company’s March-quarter earnings call. Agarwal said that yarn prices had already risen sharply in recent weeks. “There is a rise of almost 10% to 15% in the yarn prices, which effectively converts to almost 5% to 7% in the apparel prices,” he said.

“Cost increases are at multiple points. One, of course, is raw material, which is not only fabric, but also polyester buttons, thread, packaging, all of that,” Devangshu Dutta, founder of Third Eyesight, a consulting firm, said. “Because with value, you cannot really pass on the price hikes so readily to the consumer.”

Dutta said that lower- and middle-income consumers were already under financial stress from broader inflationary pressures, “so, they will not be able to absorb price hikes as easily as well.”

Ebitda margins in Q4FY26 are 10.9% for V-Mart Retail, 13.6% for Vishal Mega Mart and 19.1% for Kewal Kiran Clothing.

Double whammy for value segment

Gunender Kapur, CEO of Vishal Mega Mart, during the company’s March-quarter earnings call, said the inflationary impact had started becoming visible towards the end of April and would likely intensify in the coming months.

Despite rising input costs, retailers said they are avoiding broad-based price hikes on entry-level products amid fragile demand conditions in the value segment.

Entry-level products for these retailers range from ₹199 to ₹399, with some going up to ₹1,500.

“We would never tinker with the opening price points and the lower price points in these difficult times, because those are the customers who are the most vulnerable in inflationary situations,” Kapur said.

Hemant Jain, CEO of KKCL, said the company was willing to absorb part of the pressure on profitability to protect revenues and market share.

Jain also said the company had not yet implemented price hikes despite the inflationary environment.

To cushion the impact, companies said they are increasingly relying on cost optimisation, fabric innovation, premium fashion products and deeper expansion into smaller towns to sustain growth.

V-Mart said it was attempting to offset part of the inflation through alternative fabric usage, sourcing efficiencies and tighter inventory planning.

The retailer has also blocked orders in advance and is utilising existing yarn and fabric inventories available with vendors to soften the immediate impact of rising prices.

Vishal Mega Mart’s Kapur said it has revived cost-saving measures from the post-Ukraine cotton inflation cycle, including replacing cartons with gunny bags, removing polybags from some apparel categories, and shipping footwear without outer cartons.

The retailer has also increased the use of computer-aided design systems to reduce fabric waste during cutting.

Premium products, private labels offer buffer

These value retailers are also increasingly depending on premium and higher-fashion assortments, where consumers are relatively less price sensitive, to absorb selective price increases while keeping entry-level products affordable.

Kapur said Vishal Mega Mart’s large private-label portfolio, which contributes over 74% of its revenue, gives it greater flexibility to manage pricing pressure while maintaining discounts against national brands.

KKCL on the other hand, said it would absorb part of the inflationary impact rather than immediately pass on higher costs to consumers.

These retailers are also increasingly leaning on expansion into smaller towns and deeper markets to drive incremental growth as discretionary spending in larger urban centres remains uneven.

Value fashion retailers have underperformed the broader market amid growing concerns over rising input costs and margin pressure. Shares of V-Mart Retail, V2 Retail Ltd, Vishal Mega Mart and Kewal Kiran Clothing have fallen between 4% and 11% on a year-to-date basis, while the benchmark BSE rose 6.1% during the same period.

(Published in MINT)

admin

May 15, 2026

The ET Now Swadesh panel discussion focussed on the dual challenge facing the Indian economy: a weakening rupee and rising crude oil prices, which together are driving “imported inflation” and straining household budgets. Devangshu Dutta (Founder, Third Eyesight) put forth the following key points during the discussion (the video link is under the text summary below):

1. Dual Impact on Industry and Consumers:

2. Vulnerability of Small Businesses (SMEs):

3. Income vs. Expenditure Strain:

4. Ripple Effect of Crude Oil Beyond Logistics:

5. Shifts in Consumer Spending Patterns & “Shrinkflation”:

The panel noted that while the Reserve Bank of India (RBI) has adequate foreign exchange reserves to defend the rupee temporarily, the definitive solution relies heavily on the cooling down of global geopolitical tensions (such as the Middle East conflict affecting the Strait of Hormuz). Until then, Indian consumers will need careful financial planning and smart spending adjustments to navigate this inflationary phase. [Video below.]

admin

May 12, 2026

Anushka Jha & Kausar Madhyia, Afaqs

12 May 2026

On May 10, Prime Minister Narendra Modi, in his address to the nation, made some appeals to the citizens of India. In addition to asking Indians to re-adopt Covid-like practices of working from home and refraining from travel abroad, the prime minister also appealed to the citizenry to stop buying gold for weddings for a year.

The appeals come in response to the global energy crisis and economic instability triggered by the US-Iran war and the consequent West Asia conflict, which makes import-dependent commodities like gold especially vulnerable.

The market reaction was almost immediate. Following the Prime Minister’s appeal, jewellery stocks saw sharp declines on the BSE. According to PTI, Senco Gold fell nearly 11%, Kalyan Jewellers dropped close to 10%, and Titan Company declined around 8%, while Tribhovandas Bhimji Zaveri slipped over 6%.

National interest and gold monetisation

Industry leaders have responded by balancing the Prime Minister’s vision with structural solutions.

“India’s economic strength must always come before individual preferences. Hon’ble Prime Minister’s appeal regarding responsible gold consumption reflects the larger national concern of rising imports and pressure on foreign exchange reserves,” says Rajesh Rokde, chairman of the All India Gem and Jewellery Domestic Council (GJC).

He suggests that a revitalised Gold Monetisation Scheme (GMS) could “mobilise idle household gold” and “convert dormant gold into productive national capital”.

“Nation First. Responsible Gold Ecosystem Next,” he adds.

Avinash Gupta, the vice chairman of GJC, emphasises the emotional and cultural connection of gold to Indian households.

“But today, the nation also faces the challenge of balancing gold demand with economic stability.” He believes the GMS can channel gold into the formal economy, “reducing imports, easing CAD pressure and strengthening India’s financial ecosystem.”

India’s cultural fabric and the market reality

According to a report by MoneyControl, India imports 90% of its gold needs, making the country as one of the largest gold importers globally.

Gold is an integral part of India’s cultural fabric. It is not only a fitting gift for various auspicious occasions but also constitutes one of the most expensive elements of the ‘great Indian weddings’. Additionally, there are specific religious days dedicated solely to the purchase of gold, such as Akshaya Tritiya and Dhanteras.

However, external pressures are already weighing on the market.

Devangshu Dutta, founder of Third Eyesight, a retail management consulting firm, observes: “Jewellery retailers are already suffering from higher raw material costs, and rising gold and silver prices have driven several customers to postpone or reduce their purchases, including on significant dates such as Akshaya Tritiya.”

He notes that while wedding demand may remain strong, discretionary purchases will face a setback. “Companies will need to lean into lighter, more contemporary designs and lower caratage to sustain year-round demand.”

The potential impact of the appeal

Despite rising gold prices, approximately 700 to 800 tonnes of gold are consumed every year by Indian households, weddings, festivals, investment purchases, and rural savings, as per the same Money Control report.

Given the popularity of PM Modi, industry veterans expect a tangible shift in consumer behaviour.

“There will certainly be an impact,” says Arun Iyer, founder and creative partner at Spring Marketing Capital and former chief creative officer at Lowe Lintas, who played a significant role in the creation of Tanishq and several of its iconic advertisements.

“Given that the Prime Minister obviously has a very, very deep influence on our society, I think there will be an impact. People will think twice before buying gold.”

He further notes that while critical purchases will continue, “this quarter is expected to pose some challenges for the jewellery brands”.

Adaptation and brand strategy

According to the India Brand Equity Foundation, India’s gems and jewellery market stood at Rs 7,31,255 crore in January 2025 and is projected to increase to Rs 11,18,390 crore by 2030.

To sustain this growth, players like Suvankar Sen, CEO and MD of Senco Gold Ltd, are focusing on recycling.

“Today, almost 50% of our overall business is driven through recycled gold. This not only helps consumers optimise the value of their existing gold holdings but also contributes towards reducing dependence on fresh gold imports,” he says.

From a brand perspective, Saurabh Parmar, fractional CMO, believes the strategy must shift.

“In a scenario when the head of state says something like this, the brand faces a credibility problem, not a sales problem. The play is to shift from category promotion to category trust, lean on heritage, on long-term value, and on gold’s role in Indian culture.” He advises brands not to appear opportunistic but to signal, ‘We have always been there.'”

Given the popularity of Prime Minister Modi in India, his influence is likely to affect the performance of leading jewellery brands in the next quarter. This may include major players such as Tanishq, Malabar Gold & Diamonds, and Kalyan Jewellers, among others.

(Published in Afaqs)