admin

December 23, 2021

Devika Singh, Moneycontrol

December 23, 2021

Male grooming products startup The Man Company, known for its online-first strategy, is looking at offline expansion for its next leg of growth. The company, which operates 28 exclusive brand outlets in the country, plans to launch 60-70 more stores by the end of this fiscal to gain presence across at least 100 locations.

“A lot of growth will come from the offline channel for the next one year at least, especially in Tier II and III cities where launching exclusive stores is a good way to introduce the brand to the consumer as shopping malls are weekend destinations there,” co-founder Hitesh Dhingra told Moneycontrol.

The company, backed by fast-moving consumer goods (FMCG) major Emami which holds a 48.49 percent stake in it, is also looking at introducing its products in more multi-brand outlets. The Man Company is present in 1,200 multi-brand outlets which include lifestyle stores such as Shoppers Stop, Central and Lifestyle as well as hypermarkets, supermarkets and pharmacies. The company plans to be in 2,500 multi-brand outlets by the end of financial year 2022-23.

It currently draws about 70 percent of its sales from online channels including its own direct-to-consumer (D2C) platform and online marketplaces and 30 percent from offline channels. The startup’s strategy is focused on expanding its base in Tier II cities and beyond, which account for 50-55 percent of its sales even on online marketplaces.

“Out of our 28 exclusive brand outlets, only five to six are in top 10 cities and the rest in Tier II and smaller towns. For the new store openings also, we are going to adopt a similar strategy and only 10 percent of the new outlets will be in large cities,” said Dhingra.

The offline way

Several D2C brands have been eyeing the physical retail channel as they try to scale up and tap a wider set of consumers. Brands in the women’s beauty and personal care segment such as Mamaearth, Sugar Cosmetics and Plum Goodness are expanding their presence in the offline retail format. Plum, for instance, is looking to launch 50 exclusive brand outlets in the next two years.

Male grooming startups, too, are following a similar trajectory. For instance, Bombay Shaving Company and Baeardo are launching their products in more and more offline stores.

Devangshu Dutta, chief executive of retail consultancy Third Eyesight, said it makes sense for digitally-native companies that have achieved some brand recognition to launch in offline format for the next phase of growth. Brands in the 1990s for example, he said, who wanted to establish an identity, entered new formats or channels besides the existing ones. Similarly, digitally-native brands need not restrict themselves to online platforms alone, he added.

But he pointed out that these brands will have to address challenges such as ensuring availability of their products in offline channels. “In the online segment, companies can cater to customers with limited stocks. However, in the offline channel, they need to ensure availability of products across stores,” he said.

New categories

Apart from new retail categories, The Man Company has plans to enter categories such as sexual wellness and personal appliances. It has tied up with a marketplace for the launch of personal appliances such as beard trimmers and shavers and the category will be launched exclusively on the platform. The sexual wellness products, too, will be introduced on its D2C platform and later to other marketplaces and offline stores.

“We always launch a product on our platform to test it and get consumer feedback and, based on the response, we introduce the product to the wider market,” said Dhingra.

Launched in 2015, The Man Company caters to the men’s grooming segment and claims to have developed more than 65 stock keeping units. According to Dhingra, the company which competes with Beardo, Bombay Shaving Company and Ustraa will double its sales to Rs 100 crore by the end of this financial year.

Male grooming startups have of late attracted attention from FMCG companies. Marico last year completed the acquisition of Ahmedabad-based Beardo by buying an additional 55 percent stake in the company. It had acquired an initial 45 percent stake in 2019. British consumer goods giant Reckitt Benckiser Group invested Rs 45 crore in Bombay Shaving in February 2021. LetsShave and Ustraa are backed by Wipro Consumer Care.

According to industry estimates, the male grooming market in India was valued at Rs 15,806 crore in 2019 and is expected to cross Rs 36,402 crore by 2025, growing at a compound annual rate of 15-14 percent. Though growth was hit by the pandemic, experts are still bullish about the segment.

(Published in Moneycontrol)

admin

September 28, 2020

Written By Mihir Dalal

(From left to right) Doug McMillon, CEO of Walmart, which owns Flipkart; Mukesh Ambani, chairman and MD of RIL; Jeff Bezos, CEO of Amazon

BENGALURU : Last month, Nimit Jain, an entrepreneur, ordered biscuits, shampoo, toothpaste and other items for his family in Kota. He used JioMart—the new online shopping app by Mukesh Ambani’s Reliance Industries Limited—lured by its low prices and freebies.

JioMart was to deliver the order within two days, but Jain’s family didn’t receive the items on time and JioMart didn’t inform Jain about the delay. The delivery was done four days after he had placed the order, a few hours after Jain had complained to the firm via email and Twitter.

A few products were missing, Jain’s parents informed him. It took time to figure out the missing items because the details of the order weren’t available on the app. Jain had paid online and asked JioMart for a partial refund. Instead of receiving an acknowledgement for his refund request, he received a response for his previous email about the delay in delivery. Five days later, Jain got a refund.

Mumbai-based Jain, a computer science graduate from the Indian Institute of Technology, Madras, usually orders groceries from BigBasket and sometimes from Dunzo. He said that he doesn’t plan to use JioMart again.

“A couple of my friends and relatives (in Mumbai and Kota) have also had similarly bad experiences. It doesn’t look like JioMart is ready for online groceries. Their operations and customer care teams weren’t in sync,” Jain said.

Since JioMart expanded to more than 200 cities this summer, scores of customers like Jain have complained about missing products, delayed deliveries and generally poor service. Still, industry executives say that while its service levels have been inconsistent, JioMart is registering similar order volumes to BigBasket, the largest e-grocer, on the back of aggressive marketing and discounts.

These volumes still comprise a small fraction of the overall business of Amazon India and Walmart-owned Flipkart, the two dominant online retailers. But that’s because JioMart is only selling groceries now; it plans to sell other products like fashion and electronics soon. It’s clear that after many years of talk and hype, Reliance, which owns India’s largest offline retail chain, is finally becoming a serious challenger to Amazon and Flipkart, as well as BigBasket and Grofers.

Still, industry executives, logistics firms, consultants and analysts that Mint spoke with said that Reliance will find it tough to break the dominance of Amazon-Flipkart in e-commerce, similar to how Walmart is struggling to challenge Amazon in digital sales in the US even as its stores continue to prosper. Amazon and Flipkart both have deep pockets, proven expertise in e-commerce, popular brands and good knowledge of the Indian market.

“Reliance has the financial muscle, but Walmart (Flipkart) and Amazon are no pushovers,” said Harminder Sahni, managing director, Wazir Advisors, a consultancy. “Today, most people who want to shop online are happy with Flipkart and Amazon. These companies have achieved significant scale and have very few weaknesses. As a latecomer, it will be very difficult for Reliance to make a big dent in the market.”

Reliance did not respond to an emailed questionnaire seeking comment.

Local internet powerhouse

During the pandemic, Reliance has not only moved fast to make inroads into the e-commerce market, it has also consolidated its leadership in organized offline retail. Last month, Reliance bought most of the businesses of Future Group for about $3.4 billion in a deal that will take its retail footprint to nearly 14,000 stores—by far, the largest in India.

In the past six months, Reliance has raised more than $21 billion for its digital unit Jio Platforms. This month, Reliance kickstarted a separate fund-raising spree for its retail unit, Reliance Retail, bagging about $1.8 billion from private equity firms Silver Lake and KKR, two of the investors in Jio. Several more investment firms, including other shareholders in Jio, are expected to join them.

These moves are part of Reliance’s efforts to transform itself into a 21stcentury digital behemoth. It is positioning itself as India’s answer to Amazon, Facebook, Google, Alibaba and other world-class digital giants, and unlike local startups like Flipkart, Ola and Paytm that have or had similar ambitions, Reliance enjoys some unparalleled advantages.

It is now accepted wisdom among politicians and regulators that India needs a ‘local’ internet powerhouse to counter the dominance of America’s Big Tech and the growing influence of Chinese firms, partly because of sovereignty concerns. Reliance’s mastery in lobbying and its political clout makes the firm best-placed to exploit this urgent establishment need to find a domestic internet powerhouse.

Amazon, Flipkart, Facebook and others face many policy-related restrictions that not only serve as obstacles to them but pave the way for domestic firms led by Reliance to enter the fray. For instance, foreign investment rules prevent Amazon and Flipkart from owning inventory or selling private labels (though critics say that these firms do it anyway using clever legal workarounds), while Reliance has no such constraints. Apart from a supportive policy environment and huge capital resources, on the business front, too, Reliance has an enviable digital distribution network and reservoir of customer data on account of Jio.

But despite these formidable advantages, Reliance has yet to prove that it has the chops to realise its ambitious vision.

The war among Reliance and Flipkart and Amazon and other internet firms is also not restricted to retail, but will extend to other sectors like financial services, content and business-to-business commerce. The technology-centric nature of the battle is more suited to the internet companies than to Reliance. There’s little doubt that Reliance will be a major player in the digital business, but the jury’s out on how much value the firm can corner. Its foray in e-commerce and B2B will provide early answers to this question.

Retail battle

After JioMart began testing its service late last year, media reports said that the company would deliver products to customers from local kirana stores. After Facebook invested in Jio in April in a deal that included a business partnership between JioMart and WhatsApp, Ambani said that JioMart would soon connect some 3 crore kirana stores with their neighbourhood customers.

Many analysts, too, expect the partnership with WhatsApp, the most popular app in India, to be a game-changer. In July, Goldman Sachs estimated that Reliance’s entry will help expand the online grocery market by 20 times to about $29 billion by 2024. Reliance’s partnership with Facebook could help the firm become the leader in e-grocery and garner a market share of more than 50% by 2024, Goldman said.

But Mint learns that Reliance is sourcing a majority of orders on JioMart in many cities through Reliance Retail’s supply chain; only a small number of orders are served through kirana stores. JioMart is signing up a few thousand kirana stores every month, but its expansion is happening at a slower rate than many analysts expect. Two industry executives said that JioMart’s average order value is lower than that of other e-grocers, which means that Reliance is losing larger amounts of money on every order.

According to one e-commerce executive, for BigBasket and Grofers, the delivery cost is about 3-4% of the average order value, which exceeds ₹1000. For Reliance, the delivery cost is presently much higher because its order value is below ₹800. The lower order value is partly because most of JioMart’s 200 city-markets are non-metros. BigBasket and others generate an overwhelming majority of their business from the metros. Reliance is betting on expanding the e-grocery market rather, than taking market share from incumbents, which generate an overwhelming majority of their sales from 10-15 cities. But while Reliance may be able to attract customers in smaller cities initially with discounts, profitability will be tough.

“The economics of serving metros are very different from the rest of India. In the mass market, bill values are much, much lower. Right now, Reliance’s main focus is to scale JioMart, so they aren’t worried about the delivery cost,” the executive cited above said. “But eventually, reality will catch up, and they will have to increase basket sizes because this model isn’t sustainable. Grocery has very thin margins to start with. “

Private label push

One obvious way for Reliance to boost margins is by selling more private label products. In the grocery category, Reliance Retail already generates 14% of its revenues from private labels. People familiar with Reliance’s plans said that the company wants to push its private label products to kirana stores. While there are hundreds of well-known brands in FMCG, the grocery category (products like rice, pulses and flour) is largely unstructured. Reliance plans to sell its private label products both in grocery and FMCG.

Apart from retail, Reliance is also rapidly expanding its B2B business. Its private label products form a key component of its retail and wholesale business plans, the people cited above said.

The private label push, however, is making large FMCG companies like Hindustan Unilever, Marico and Dabur, which sell competing products, wary of working with Reliance’s B2B arm.

Like Flipkart and Amazon, which are also expanding their B2B businesses, Reliance’s grand vision over time is to have an integrated ecosystem of wholesale and retail in which it connects consumer goods makers with kirana stores and retailers, supplies a large number of private label products across many categories to retailers and end-customers, and becomes the biggest omnichannel retail firm in the country. But realising this vision will require Reliance to work seamlessly with millions of kirana stores, thousands of brands, modern retailers (all of which will see the firm as a rival to an extent)—and provide exceptional service in a profitable manner to retail customers.

Analysts and industry executives said that Reliance has a higher probability of finding success in categories like fashion (in which it already runs a portal called Ajio) and grocery that are mostly unorganised and have a shortage of established brands. In these categories, Reliance faces fewer barriers from existing players and has a better chance of pushing its private labels in both the wholesale and retail markets. But in categories like electronics and FMCG, which are dominated by entrenched brands, kirana stores and e-commerce firms, Reliance may struggle to scale as fast.

For instance, Flipkart and Amazon dominate online sales of electronics and fashion, which together comprise more than 75% of all e-commerce. To win significant share in electronics, Reliance will have to spend enormous amounts on discounts, marketing and offering favourable terms to brands . But, in fashion, Reliance can tap its low-priced private labels to lure customers without resorting to value destruction.

“The market is too varied for one player to be big in all categories,” an investment banker said. “Reliance will have to carefully choose its battles. There’s a risk that it may spread itself too thin, so it’s wise for them to have started with grocery.”

Meanwhile, while Google and Facebook have together invested more than $10 billion in Reliance, both companies are continuing to expand their own businesses in India. Google and Facebook have ambitions to enter e-commerce and expand in other sectors like payments and content. What this means is that while Google and Facebook will end up collaborating with Reliance in some areas, they will also compete with the firm in others, joining Flipkart and Amazon in the war of the digital conglomerates.

Flipkart and Amazon have already stepped up their lobbying efforts with the emergence of Reliance as a threat. Because of the pandemic that has made e-commerce indispensable, there has been a thaw in the government’s attitude towards the US e-commerce firms. A more antagonistic attitude may return when the pandemic passes.

Eventually, though, the war will be decided by customers. Here, experts are divided on whether Reliance will emerge as the winner. “Reliance still has to do a lot more on getting the customer experience in place, but given the strides they’ve made, it is well-placed to compete in the digital space,” said Devangshu Dutta, head of retail consultancy firm Third Eyesight.

Source: livemint

Devangshu Dutta

September 28, 2017

In recent decades, the dependence on established medical disciplines has begun to be challenged. There is the oft-quoted dictum that healthcare sector tends to illness rather than health. Another saying goes that some of the food you eat keeps you in good health, but most of what you eat keeps your doctor in good health. With a gap emerging between wellness-seekers and the healthcare sector, so-called “alternative” options are stepping in.

Some of these alternatives actually existed as well-structured and well-documented traditional medical practices for thousands of years before the introduction of more recent Western medical disciplines. This includes India’s Siddha system and Ayurved (literally, “science of life”), which certainly don’t deserve being relegated to an “alternative” footnote. Ayurved is also said to have influenced medicine in China over a millennium ago, through the translation of Indian medical texts into Chinese.

Other than these, there are also more recent inventions riding the “wellness” buzzword. These may draw from the traditional systems and texts, or be built upon new pharmaceutical or nutraceutical formulations. Broader wellness regimens – much like Ayurved and Siddha – blend two or more elements from the following basket: food choices and restrictions, minerals, extracts and supplements, physical exercise and perhaps some form of meditative practices. Wellness, thus, is often characterised by a mix-and-match based on individual choices and conveniences, spiked with celebrity influences.

A key premise driving the wellness sector is that modern medicine depends too heavily on attacking specific issues with single chemicals (drugs) or combinations of single chemicals that are either isolated or synthesised in laboratories, and that it ignores the diversity and complexity of factors contributing to health and well-being. The second major premise for many wellness practitioners (though not all!) is that, provided the right conditions, the body can heal itself. For the consumer the reasons for the surge in demand for traditional wellness solutions include escalating costs of conventional health care, the adverse effects of allopathic drugs, and increasing lifestyle disorders.

After food, wellness has turned into possibly one of the largest consumer industries on the planet. Global pharmaceutical sales are estimated at over US$ 1.1 trillion. In contrast, according to the Global Wellness Institute, the wellness market dwarfs this, estimated at US$ 3.7 trillion (2015). This figure includes a vast range of services such as beauty and anti-ageing, nutrition and weight loss, wellness tourism, fitness and mind-body, preventative and personalized medicine, wellness lifestyle real estate, spa industry, thermal/mineral springs, and workplace wellness. Within this, the so-called “Complementary and Alternative Medicine” is estimated to be about US$200 billion.

There are several reasons why “complementary and alternative medicine” sales are not yet larger. Rooted in economically backward countries such as India, these have been seen as outdated, less effective and even unscientific. In India, the home of Siddha and Ayurved, apart from individual practitioners, several companies such as Baidyanath, Dabur, Himalaya and others were active in the market for decades, but were usually seen as stodgy and products of need, and usually limited to people of the older generations and rural populations. In the West they typically attracted a fringe customer base, or were a last resort for patients who did not find a solution for their specific problem in modern allopathy and hospitals.

However, through the 1970s Ayurved gained in prominence in the West, riding on the New Age movement. Gradually, in recent decades proponents turned to modern production techniques, slick packaging and up-to-date marketing, and even local cultivation in the West of medicinal plants taken from India.

As wellness demonstrated an increasingly profitable vector in the West, Indian entrepreneurs, too, have taken note of this opportunity. Perhaps Shahnaz Husain was one of the earliest movers in the beauty segment, followed by Biotique in the early-1990s that developed a brand driven not just by a specific need but by desire and an approach that was distinctly anti-commodity, the characteristics of any successful brand. Others followed, including FMCG companies such as the multinational giant Unilever. The last decade-and-a-half has also brought the phenomenon called Patanjali, a brand that began with Ayurvedic products and grew into an FMCG and packaged food-empire faster than any other brand before! While a few giants have emerged, the market is still evolving, allowing other brands to develop, whether as standalone names or as extensions of spiritual and holistic healing foundations, such as Sri Sri Tattva, Isha Arogya and others.

An absolutely critical driver of this growth in the Indian market now is the generation that has grown up during the last 25-30 years. It is a class that is driven by choice and modern consumerism, but that also wishes to reconnect with its spiritual and cultural roots. This group is aware of global trends but takes pride in home-grown successes. It is comfortable blending global branded sportswear with yoga or using an Indian ayurvedic treatment alongside an international beauty product.

Of course, there is a faddish dimension to the wellness phenomenon, and it is open to exploitation by poor or ineffective products, non-standard and unscientific treatments, entirely outrageous efficacy claims, and price-gouging.

To remain on course and strengthen, the wellness movement will need structured scientific assessment and development at a larger scale, a move that will need both industry and government to work closely together. Traditional texts would need to be recast in modern scientific frameworks, supported by robust testing and validation. Education needs to be strengthened, as does the use of technology.

However the industry and the government move, from the consumer’s point-of-view the juggernaut is now rolling.

(An edited version of this piece was published in Brand Wagon, Financial Express.)

Devangshu Dutta

January 10, 2017

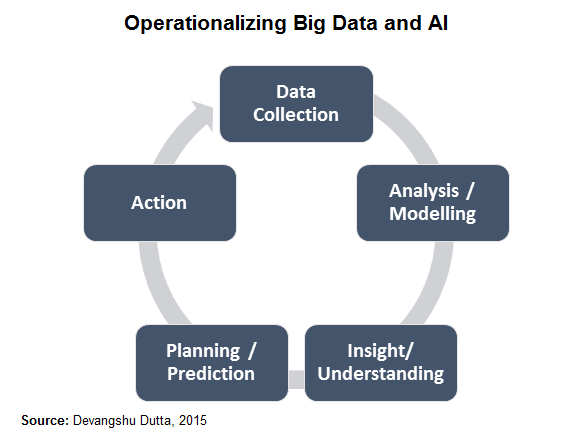

In this piece I’ll just focus on one aspect of technology – artificial intelligence or AI – that is likely to shape many aspects of the retail business and the consumer’s experience over the coming years.

To be able to see the scope of its potential all-pervasive impact we need to go beyond our expectations of humanoid robots. We also need to understand that artificial intelligence works on a cycle of several mutually supportive elements that enable learning and adaptation. The terms “big data” and “analytics” have been bandied about a lot, but have had limited impact so far in the retail business because it usually only touches the first two, at most three, of the necessary elements.

“Big data” models still depend on individuals in the business taking decisions and acting based on what is recommended or suggested by the analytics outputs, and these tend to be weak links which break the learning-adaptation chain. Of course, each of these elements can also have AI built in, for refinement over time.

Certainly retailers with a digital (web or mobile) presence are in a better position to use and benefit from AI, but that is no excuse for others to “roll over and die”. I’ll list just a few aspects of the business already being impacted and others that are likely to be in the future.

On the consumer-side, AI can deliver a far higher degree of personalisation of the experience than has been feasible in the last few decades. While I’ve described different aspects, now see them as layers one built on the other, and imagine the shopping experience you might have as a consumer. If the scenario seems as if it might be from a sci-fi movie, just give it a few years. After all, moving staircases and remote viewing were also fantasy once.

On the business end it potentially offers both flexibility and efficiency, rather than one at the cost of the other. But we’ll have to tackle that area in a separate piece.

(Also published in the Business Standard.)

Devangshu Dutta

December 29, 2016

In 2016, brick-and-mortar modern retailers seemed to have begun recovering their confidence, and cautiously investing in expansion. However, currency shortage has significantly dampened demand at the end of the year. The hangover would continue into the first half of 2017, and consumers could be muted overall on discretionary purchases, including fashion, mobile upgrades and out-of-home dining.

On the other hand, while digital transactions introduce a note of caution (friction) in the consumer’s purchase decision, for e-tailers they do reduce complexity, cash-handling costs and potential returns which could provide significant unexpected wins.

I’ve written about this for years, and don’t tire of reiterating: the retail sector must recognise that shopping is a unified activity for the consumer; physical stores and non-store environments are alternative but complementary channels. Brands can and must use whatever channel mix works for them, and brick-and-mortar retailers need to invest in creating an integrated growth blueprint towards “unified commerce”.

On their part, while e-commerce companies are constrained by FDI policy, they will need to invest more in developing “old economy” strengths – strong product differentiation and distinguishable brands. Fashion, accessories, home decor and other lifestyle products are strong drivers of gross margin for all multi-product retailers, and e-commerce players struggling on the path to profit would focus on these even more, as well as on private labels. They also need to have management teams that are able to cast their minds 3-5 years into the future, while keeping close watch on immediate cash flows. Capital is available, but turning risk-averse. All businesses need to focus on up-skilling their teams, retaining good people, improving processes and adopting technology. In recent years, growth in the retail sector seems to have been driven by a “spray-and-pray” approach, not necessarily management sophistication. Spending like there’s no tomorrow is a sure way to no tomorrow.

In short, 2017 could be the year where the entire retail sector grows up – a lot. We hope.

(This piece was published in The Hindu – Businessline on 29 December 2016).