admin

July 9, 2014

B2B event companies don’t often think about consumer spending as something directly relevant to their business. However, consumer trends can allow industry event and exhibition organizers to get an advance view of where the opportunities can lie in the future. In this Keynote address at UFI’s Asia Open Seminar in Bangalore, Devangshu Dutta shares his views about the key consumer trends in India, and the implications for the events and exhibitions industry.

(This presentation was delivered on 6 March 2014 in Bangalore, India.)

admin

January 21, 2013

By Tarang Gautam Saxena & Devangshu Dutta

Since the onset of reopening of India’s economy in the late 1980s, fashion is one consumer sector that has drawn the largest number of global brands and retailers. Notwithstanding the country’s own rich heritage in textiles the market has looked up to the West for inspiration. This may be partly attributable to colonial linkages from earlier times, as well as to the pre-liberalisation years when it was fashionable to have friends and relatives overseas bring back desirable international brands when there were no equivalent Indian counterparts. Even today international fashion brands, particularly those from the USA, Europe or another Western economy, are perceived to be superior in terms of design, product quality and variety.

International brands that have been drawn to India by its large “willing and able to spend” consumer base and the rapidly growing economy have benefitted in attaining quick acceptance in the Indian market and given their high desirability meter, most international brands have positioned themselves at the premium-end of the market, even if that is not the case in the home markets. In addition, Indian companies – manufacturers or retailers – have been more than ready to act as platforms for launching these brands in the market and today there are over 200 international fashion brands in the Indian market for clothing, footwear and accessories alone, and their numbers are still growing.

Global Fashion Brands – Destination India

Europe’s luxury brands have had a long history with India’s princely past, but modern India tickled the interest of international fashion brands in the 1980s when it set on the path of liberalisation. The pioneering companies during this stage were Coats Viyella, Benetton and VF Corporation. At the time the Indian apparel market was still fragmented, with multiple local and regional labels and very few national brands. Ready-to-wear apparel was prevalent primarily for the menswear segment and was the logical target for many international fashion brands (such as Louis Philippe, Arrow, Allen Solly, Lacoste, Adidas and Nike). (Addendum: The rights to Louis Philippe, Van Heusen and Allen Solly in India and a few other markets were sold after several years to the Indian conglomerate, Aditya Birla Group, as part of the Madura Garments business.)

The rapidly growing media sector also helped the international brands in gaining visibility and establishing brand equity in the Indian market more quickly. However, this period did not see a huge rush of international brands into India. West Asia and East Asia (countries such as Japan, South Korea, Taiwan and even Thailand) were seen as more attractive due to higher incomes and better infrastructure. In the mid-1990s there was a brief upward bump in international fashion brands entering the Indian market, but by and large it was a slow and steady upward trend.

The late-1990s marked a significant milestone in the growth of modern retail in India. Higher disposable incomes and the availability of credit significantly enhanced the consumers’ buying power. Growth in good-quality retail real estate and large format department stores also allowed companies to create a more complete brand experience through exclusive brand stores in shopping centres and shop-in-shops in department stores.

By the mid-2000s, however, a very distinct shift became visible. By this time India had demonstrated itself to be an economy that showed a very large, long-term potential and, at least for some brands, the short to mid-term prospects had also begun to look good.![]()

While India was a promising market to many international brands, it was not completely immune to the global economic flu. More than its primary impact on the economy, it sobered the mood in the consumer market. Even the core target group for international brands tightened the purse strings and either down-traded or postponed their purchases.

In 2008, in the midst of economic downturn, scepticism and uncertainty, international fashion brands continued to enter India at nearly the same momentum as the previous year. Many international brands such as Cartier, Giorgio Armani, Kenzo and Prada entered India in 2008, targeting the luxury or premium segment. However, given the high import duties and high real estate costs, the products ended up being priced significantly higher than in other markets. Many brands ended up discounting the goods heavily to promote sales, while a few gave up and closed shop.

The year 2009 saw the true impact of the slowdown as fewer international brands were launched during the year. The brands that launched in 2009 included Beverly Hills Polo Club, Fruit of the Loom, Izod, Polo U.S., Mustang, Tie Rack, Donna Karan/DKNY and Timberland amongst others. Some of these had already been in the pipeline for quite some time and had invested considerable time and effort in understanding the dynamics of the Indian retail market, scouting for appropriate partners, building distribution relationships and tying up for retail space, setting up the supply chain and, most importantly, getting their operational team in place.

2010 was better in comparison: although initially slow, the growth of new international brands entering the Indian market in 2010 bounced back later during the year, and some brands that had exited the Indian market earlier also made a comeback. Amongst the new launches, a highlight of the year was the launch of the most awaited and discussed-about Spanish brand Zara. The first store was launched in Delhi to an absolutely phenomenal response, followed by a store in Mumbai, and a third again in Delhi. The Italian value fashion brand, OVS Industry, was launched in 2010 by Oviesse through a joint-venture with Brandhouse Retail from the SKNL group. While in its first year products were imported from Italy, the company had mentioned that it intended to bring in the merchandise directly from the supply source for speed and cost effectiveness, to achieve aggressive growth over the following five years.

2010 indicated a fresh round of optimism as the pace of new brands entering the market picked up, and those already present in the market showing signs that they were adapting their strategies to grow their India business, including lowering prices and entering new segments.

Though the number of new brands entering the Indian shores in 2011 and 2012 may not have matched the numbers in the peak years, both years have been healthy and the list of new brands ready to enter in 2013 already seems promising.

Amongst others, 2011 saw the entry of Australian brands such as Roxy and Quiksilver having tied up with Reliance Brands for distribution. The largest British football club and lifestyle brand Manchester United, signed up with Indus-League Clothing Ltd. to bring the fashion products to India, after having launched café bars in India in 2010 through a franchisee.

2012 brought in luxury brands such as Christian Louboutin, Roberto Cavalli and Thomas Pink, womenswear brands such as Elle, Monsoon and fashion accessories brands such as Claire’s.

Routes to Market – The Evolution

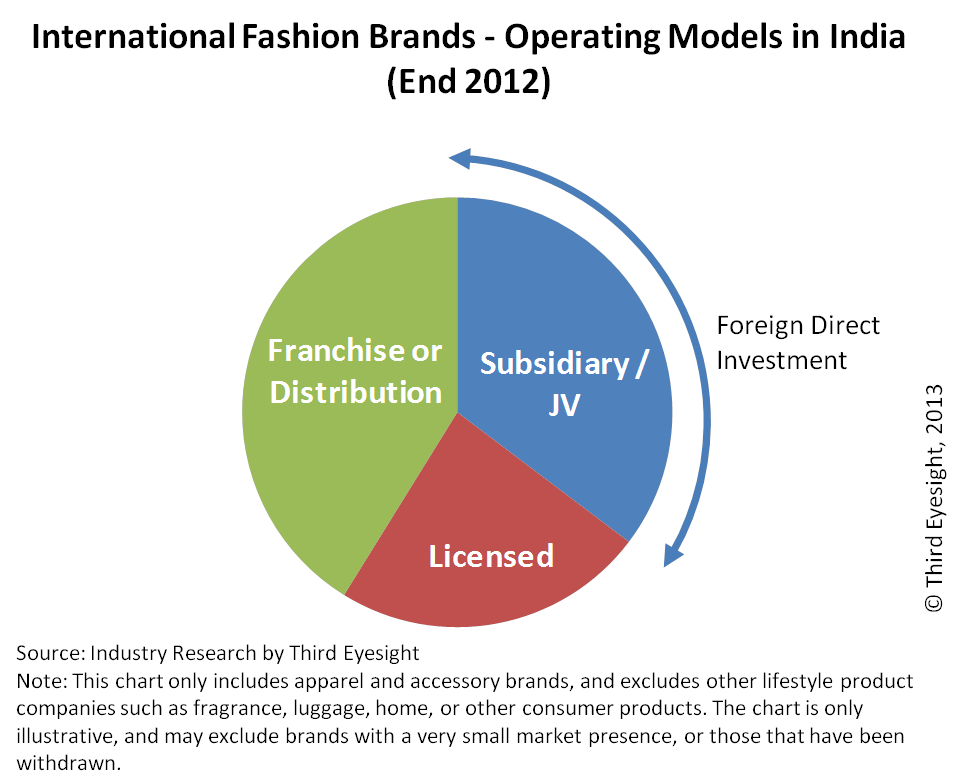

The choice for entry strategy for the fashion brands has evolved over the years. During the initial years licensing was the preferable route for international brands that were testing the market. This shifted to franchising as import duties dropped and brands looked at exerting more control on the product and the supply chain. More recently, brands seem to be opting for some degree of ownership, as they begin to take a long-term view of the market.

In the 1980s and the early 1990s, licensing was a popular entry strategy amongst the global fashion brands, with minimal involvement in the Indian business.

In the mid-1990s a few companies such as Levi Strauss set up wholly owned subsidiaries while others such as Adidas and Reebok entered into majority-owned joint ventures. This helped them to gain a greater control over their Indian operations, sourcing and supply chain, and brand. In the subsequent years import duties for fashion products successively came down making imports a less expensive sourcing option and the realty boom brought in many investors in retail real estate who became franchisees for the international brands. By 2003, franchising became the preferred launch vehicle for an increasing number of international companies, while only a few chose to enter through licensing.

In 2006 the Government of India reopened retail to foreign investment (allowing up to 51 per cent foreign direct investment in single-brand retail). Using this route, many brands have entered India by setting up majority-owned joint ventures, or moving their existing franchise relationships into a joint venture structure. By the end of 2008, more than 40 per cent of the international brands were present through a franchise or distribution relationship, while more than 25 per cent had either a wholly-owned or majority-owned subsidiary. All these structures allowed the brands to have greater control of operations, particularly of the product.

Amongst the international brands that entered the Indian market, a few were on their second or even third attempt at the market. For instance, Diesel BV initially signed a joint venture agreement in 2007 with Arvind Mills. However, by the middle of 2008, the relationship ended with mutual consent, as Arvind reduced its emphasis at the time on retailing international brands within the country. Within a few months of ending this relationship, Diesel signed a joint venture with Reliance Brands as the iconic denim brand wanted to take on the Indian market full throttle and the Indian counterpart had indicated that it wanted to rapidly build its portfolio of Indian and foreign brands in the premium to luxury segments across apparel, footwear and lifestyle segments.

Similarly, Miss Sixty entered India in 2007 through a franchisee agreement with Indus Clothing. It switched to a joint venture with Reliance Brands in the same year but the partnership was called off in 2008. Miss Sixty finally entered India through a franchisee agreement with a manufacturer of women’s footwear and accessories.

During the turbulence of 2008 and 2009, a few brands also moved out of the market. Some of them were possibly due to misplaced expectations initially about the size of the market or about the pace of change in consumer buying habits. Others were due to a failure either on the part of the brand or its Indian partners (or both), to fully understand what needed to be done to be successful in the Indian market. Whatever the reason, the principals or their partners in the country decided that the business was under-performing against expectations for the amount of effort and money being invested, and that it was better to pull the plug. Amongst the brands that exited the market during 2008 and 2009 were Gas, Springfield and VNC (Vincci).

In the last few years as the foreign direct investment rules are being softened in particular with regard to the more flexibility in the 30% domestic sourcing and clarification on brand ownership norm there is an increasing preference for international companies to enter the India market with some form of ownership while those that are already in the market are looking to increase their stakes in the business.

Several brands have taken the plunge into investing in the Indian operations and moved more aggressively into the market. Since the year 2009, international brands increasingly opted for joint-ventures as the choice for entry into the market. Even the brands already present started looking to modify the nature of their presence in India in order to exert more control over the retail operations, products, supply chain and marketing. Brands that changed their operating structures and, in some cases partners, include VF (Wrangler, Lee etc.), Lee Cooper, Lee, Louis Vuitton, Gucci, Burberry amongst others. Mothercare, the baby product retailer, which was initially present through a franchise agreement with Shoppers Stop, formed a joint venture with DLF Brands Ltd to enable the expansion through stand-alone stores.

During 2011, Promod changed its franchise arrangement with Major Brands into a joint-venture that is majority-owned by Promod. From its launch in 2005, the brand has opened 9 stores so far. However with the new joint venture in place, the international brand is reported to be looking at opening 40 stores in the next four years with the hope of increasing the contribution of India business to its global revenue to the extent of 15-20% from a mere 3% at present.

After its partnership with Raymond fell through in 2007 and all of its standalone stores were shut down, Gas (Grotto SpA) scouted around for an appropriate partner for India business. Eventually, the brand set up a wholly owned subsidiary in 2010 for wholesale operation while retail stores were franchised. In 2012 the company formed an equal joint venture partnership with Reliance Brands with plans to ramp up India retail presence.

2012 was a defining year marking the government’s decision to allow 100% foreign direct investment in single brand retail business and permitting multi-brand retail in India. Not only has this encouraged new brands to consider the Indian market but many existing brands have started reviewing their existing operating structures and alliances, and have initiated moves towards greater ownership and a stronger foothold in the Indian market. Some of the brands have taken the decision to step into an ownership position in India as they felt that India was too strategic a market to be “delegated” entirely to a partner (whether licensee or franchisee), or that an Indian partner alone might not be able to do justice to the brand in terms of management effort and financial capital.

S. Oliver restructured its India operations in 2012 by exiting its prior relationship with the apparel exporter Orient Craft and tied up with a new partner through a majority joint venture. To gain a larger share in the Indian market the company has repositioning the brand, changed its sourcing strategy, reduced the entry-level prices by 40% while reducing the store size (from 5,000 sq. ft. to 1,200-2,400 sq. ft.). It has also put in place an aggressive expansion strategy for tier II towns. The change in FDI norms towards the end of last year may cause it to review its position further.

Canali has entered into a majority-owned joint-venture with its existing partner Genesis Luxury. The brand had entered in India in 2004 through a distribution agreement. Through this change the international brand plans to grow its presence in India multi-fold by opening 10-15 stores over the next three-four years.

Pavers England is the first international brand to have applied for and been granted the permission to own and operate its retail business in India through a 100 per cent subsidiary owned by a UK based company. Newcomers such as H&M and Loro Piana are reportedly considering the joint venture route.

As we have already mentioned in one of our earlier papers (“Tapping into the India Gold Rush”) we do not expect a dramatic short-term growth in the number of international brands following the retail FDI relaxation in September 2012. However, at that time we did foresee some changes in the operating structures for the single brand ventures already active in the market, as well as entry of new brands that have been holding back so far as they wanted greater control in their India retail business and this seems to be happening already.

In the luxury sector, 51 percent FDI and distribution relationships are likely to continue to be a norm, since it is virtually impossible for most luxury companies to meet the 30 percent domestic sourcing requirement in its true spirit. In many cases, the local partner in a joint venture is a mere placeholder until FDI rules are liberalised further and, unless the business grows significantly, most brands will be content to keep the existing structures in place.

In the other segments some more relationships could be reconstituted during 2013, taking the international brand at least a step closer to gaining greater control, even if their partners remain the same.

Franchising is still the more common form of route to market for most single brand retail companies although for many international companies an eventual ownership in India business may be desirable. However, licensing should not be excluded from the choice set, especially for companies that are multi-brand retail concepts such as Sephora or those that manage to find a suitable Indian partner that can provide end-to-end support from product sourcing to distribution and retail (for example, the relationship between Elle and Arvind).

Today two thirds of the international fashion brands come from three countries the U.S.A., Italy and the U.K. with nearly 30 per cent originating from the U.S.A. alone.

Is This A Lucky 13?

The theme for the year 2013 is positive for most brands, although still cautious.

Amongst the international brands that one can look forward to shopping in 2013 are “Uniqlo” of Fast Retailing, Japan’s largest apparel retailer, Sweden’s H&M, Emilio Pucci and Billabong. But India is not merely a destination anymore for the international brands to grow their business. The country is also increasingly becoming the innovation-platform or testing ground for new concepts and trends. World Co. a Japanese retailer with more than 3,000 stores in Japan and 200 stores in other parts of Asia is also test-marketing women’s apparel and accessories brands such as Couture Brooch, Opaque.clip, zoc, Tk Mixpie and Hot Beat to gain insights into consumers’ psyche. Italian brand United Colors of Benetton has recently introduced a global retail interior design concept which is present in major European cities but is the first-of-its-kind store in Asia and may well set the trend for the rest of Asia.

Gucci recently opened its largest store in India recently Delhi-NCR after two failed joint ventures. All of its five stores are now run directly by the company and the Indian business also reported to have turned profitable this year.

Brands such as Mango who have chosen the franchise route are tying up with additional partners (e.g. DLF) in the hope of making the Indian business contribute significantly to the overall revenue of the company.

UK-based apparel chain Marks & Spencer is accelerating its expansion in India with plans to add ten stores in the next six to eight months in the country. The company has identified India as one of the key markets to become the world’s most sustainable retailer by 2015. It plans to increase the number of stores in India from 24 currently to over 30 through the 51:49 joint venture with Reliance Retail.

Puma SE, the global sports lifestyle company for athletic shoes, footwear, and other sports-wear aggressively set out to gain 30 per cent of the Indian organised retail sportswear market within a year, from a share of 18-20 per cent in the top four branded sportswear segments in 2011. To this end the company targeted opening nearly 100 more stores during 2012. While the actual numbers are reportedly short of target, the brand has been opening amongst the largest stores during the year.

The confidence in the India opportunity is rising again, with existing global brands expecting the contribution from India business to grow multi-fold in a few years. However, the approach is of careful consideration and brands realise that India is a unique market, different not only from the West but also from other Asian economies such as China. Rather than adopting a “cut-and-paste” approach one needs to seriously consider the appropriate business model for India. Many of the global players have had to create a different positioning from their home markets. Some have significantly corrected pricing and fine-tuned the product offering since they first launched; these include The Body Shop and Marks & Spencer. Others are unearthing new segments to grow into; for instance, Puma and Lacoste are now seriously targeting womenswear as a growth market.

It is not only international brands that are more optimistic. Indian partners are also reviewing their approach. For instance, the Arvind Group that had looked at reducing its emphasis on international fashion brands in 2007-08 has recently acquired the business operations of Planet Retail which operated the franchises of British fashion retailers Debenhams and Next, and American lifestyle brand Nautica in India. The company termed Debenhams’ franchise as a significant acquisition as it provided an entry into the department store segment. Arvind plans to increase the India presence of Debenhams from 2 stores to 8 over the next three years. It also plants to grow the network of Next, the large-format speciality stores, from 3 to 12 in the same period.

As customer footfall and conversions pick up, international brands are also shoring up their foundations for future expansion in terms of better processes and systems, closer understanding of the market, and nurturing talent within their team. Third Eyesight’s study of the market highlights international brands’ concerns with ensuring a consistent brand message, improved organisational capabilities right down to front-line staff, and focussing on unit productivity (per store and per employee).

India shows signs of a healthier business outlook for International brands but the game has just begun and with competition getting tougher, we can expect interesting times ahead.

Devangshu Dutta

January 5, 2010

If we were to look at phrases that have cropped up during the recent recessionary times in the consumer goods sector, “private label” has to be among those at the top of the list.

From clothing to cereals, toothpaste to televisions, there is hardly a category that has not seen retailers trying their hand at creating own labelled products.

The first motivation for most retailers to move into private label is margin. On first analysis, it appears that the branded suppliers are making tons of extra money by being out there in front of the consumer with a specific named product. The retailer finds that creating an alternative product under its own label allows it to capture extra gross margin. Typically the product category picked at the earliest stage of private label development would be one for which several generic or commodity suppliers are available.

At this early stage, the retailer is aiming for a relatively predictable, stable-demand and easily available product whose sales would be driven by the footfall that is already attracted into the store. A powerful bait to attract the customer is the visible reduction in price, as compared to a similar branded product. If the product can be compared like-for-like, customers would certainly convert to private label over time.

However, maintaining prices lower than brands can also be counter-productive. In many products, while customers might not be able to discern any qualitative difference, they may suspect that they are not getting a product comparable to one from a national or international brand. And while private label can drive off-take, the price differential can also erode gross margin which was the reason that the retailer may have got into private label in the first place. Over time, such a strategy can prove difficult to sustain, as costs of developing, sourcing and managing private label products move up.

The other strong reason a retailer chooses to have private label is to create a product offering that is differentiated from competitors who also offer brands that are similar or identical to the ones offered by the retailer. Department stores, supermarkets and hypermarkets around the world have all tried this approach – some have been more successful than others. The idea is to provide a customer strong reasons to visit their particular store, rather than any of the comparable competitors.

Of course, when differentiation is the operating factor, the products need more insight and development, and closer handling by the retailer at all stages. A price-driven private label line may be sourced from generic suppliers, but that approach isn’t good enough for a line driven by a differentiation strategy. In this case, costs of product development and management increase for the retailer. However, to compensate, the discount from a comparable national brand is not as high as generic nascent private label. In fact, some retailers have taken their private label to compete head on with national brands – they treat their private labels as respectfully as a national branded supplier would treat its brand.

So what does it take to go from a “copycat” to being a real brand?

Third Eyesight has evolved a Private Label Maturity Model (see the accompanying graphic) that can help retailers think through their approach to private label, whether their product offering is dominated by private label, or whether they have only just begun considering the possibility of including private label in their product range. The model sketches out a maturity path on five parameters that are affected by or influence the strength of a retailer’s private label offering:

In some cases, retailers may have multiple labels, some of which may be quite nascent while others might be highly evolved, clear and comparable to a national brand. This could be by default, because the labels have been launched at different times and have had more or less time to evolve. However, this can also be used as a conscious strategy to target various segments and competitive brands differently, depending on the strength of the competition and their relationship with the consumer.

The interesting thing is that size and scale do not offer any specific advantage to becoming a more sophisticated private label player. Some extremely large retailers continue to follow a discounted-price “me-too” private label strategy where even the packaging and colours of the product are copied from national brands, while much smaller players demonstrate capabilities to understand their specific consumers’ needs to design, source and promote proprietary products that compare with the best brands in the market.

For a moment, let’s also look at private labels from the suppliers’ point of view. As far as we can see, private label seems to be here to stay and grow. Suppliers can treat private labels as a threat, and figure out how to ensure that they retain a certain visibility and relationship with the consumer. On the other hand, interestingly, some suppliers are also looking at private label as an opportunity. They see the growth of private label as inevitable, and would much rather collaborate in the retailer’s private label development efforts. This way they can maintain some kind of influence on the product development, possibly avoid direct head-on conflict with their own star branded products and, if everything else fails, at least grab a share of the market that would have otherwise gone over to generic suppliers.

If you are retailer, I would suggest using the Private Label Maturity Model to clarify where you want to position yourself, and continue to use it as a guide as you develop and deliver your private label offering.

If you are a supplier concerned about private label, my suggestion would be to gauge how developed your customer is and is likely to become, and ensure that you are at least in step, if not a step ahead.

Of course, if you need support, we’ll only be too happy to help! (Contact Third Eyesight to discuss your private label needs.)

Devangshu Dutta

March 13, 2008

Many people I know treat shopping centres or malls as a new phenomenon, a progressive development of recent times or a modern blot on the traditional cityscape (depending on your point of view).

However, Grand Bazaar (Istanbul, Turkey) is the earliest known mall, with the original structures built in 1464, with additions and embellishments later.

In India, if one were to include open arcades, Chandni Chowk in Delhi is reported to have opened around 1650, with its speciality shopping streets. (Of course, more traditional bazaars have been around many thousands of years around the world.)

But even if one were to get more “traditional” about the definition of a mall, possibly India’s first mall was founded in the hottest city in the country then, Kolkata (New Market) in 1874.

In more recent history, Delhi’s municipal pride, the air-conditioned underground Palika Bazar was a novelty in the mid-1980s, while Bangalore’s Brigade Road saw several early pioneers with their shopping arcades in the late 1980s.

Then came the mall-mania beginning with Ansal Plaza in Delhi and Crossroads in Mumbai. Everyone started looking at malls as the new goldmine, being pushed ahead by a “retail boom”.

The early stage of any such gold rush usually has several experiments missing their mark, which is what has happened with the hundreds of mall-experiments that have been launched in the last 7-8 years.

Some of the significant and common issues are starting to be addressed, but many others remain.

Catchment-Based Planning is Needed

The top-most issue in my mind is “oversupply”. While this may sound absurd to many people, given the low figures quoted for modern retail, I am referring to the over-concentration of malls in a small geography. If 8-10 malls open 4-5 million sq. ft. of shopping in a catchment that can only support 1 million sq. ft., everyone knows that some of the malls will fail. But everyone also believes that their mall will succeed (otherwise, they would obviously not have invested in the mall).

What happens to the malls that fail? Depending on the design of the building, many of them can be repurposed into office space – another area where a lot of investment is still needed. So in the end, actually, most people win, one way or the other. Yet, there will be some losers. Does anyone “plan” on being one?

The second key issue in my mind has been that mall developers have been thinking as “property developers” rather than retail space managers. The successful shopping centre operators worldwide (now also in India), are actually as concerned about what and who is occupying that space as a retailer would be. They are concerned about the composition of the catchment, the shopping patterns, the volume of sales, the shopping experience. Therefore, the tenant mixes as well as adjacencies are factored into the earliest stages of planning the shopping centres.

In fact, if I were to identify the most critical operational problem for many of the malls, it is the lack of relevance to catchment and, therefore, the low conversion of footfall into sales for the tenants other than the food-courts. Customer flow planning within the mall is another factor that can make a tremendous impact on the success and failure of the tenant stores.

Once you start looking at these factors during the planning of a mall, another obvious aspect that jumps out is “differentiation”. Currently, there is little to choose from between malls (other than possibly the anchor store). However, with more clarity in terms of the target audience, the potential strategies for differentiation also become clearer. The visitors also become segmented accordingly, and there is a natural benefit to the tenants occupying the mall.

If, as a mall operator, you want to be in business for long, and also develop other properties in the future, the success of your tenants is probably the most critical driving factor for your business.

Integration into the Urbanscape

When we gauge malls from the perspective of integrating within the urban landscape, there are obviously some glaring errors being made. Instead of aesthetic design that reflects the heritage and culture of the location and its surroundings, or some other inspirational source for the architect, most malls that have come up are concrete and glass boxes.

Beyond the looks, some of the malls are a victim of their own success. They attract more crowds during the peak than they have planned for. Not only does the parking prove to be inadequate, there is no holding capacity for cars entering or exiting the mall. The result is a traffic nightmare – not just for general public, but even for the visitors to the mall. Someone who has spent 45 minutes stuck in a jam waiting to get into the parking of a mall will certainly not be in the best frame of mind to buy merchandise at the stores occupying the mall.

Some of the problems lie outside the mall-developer’s control – for instance land costs are a major driver of the cost of the project (and, therefore, the lease costs to the tenants), and land is a commodity which is independent. Real estate is available within the cities as brown-field sites (former industrial locations), but the regulations are convoluted and the strings are in the hands of too many different departments of the government (city, state and central). This needs joint creative thinking on the part of developers, the government and the public, if our cities are to develop in a more sane fashion than they have in the past.

Similarly, land deals are still not clean enough for foreign investors to be comfortable participating in many developments. This obviously is holding back a tremendous source of capital and domain expertise that could contribute to the growth of this sector.

Many other operational issues exist – manpower, systems, health & safety – some of them can be managed or controlled by the mall developers, and it is a question of time (and of their gaining experience). Other issues are more in the domain of the government, and need a visionary push to make “urban renewal” a true mission.

New Life for the Cities

In my opinion, one of the most interesting areas which would be in the joint interest of almost all parties (that I can think of) is the possibility of revitalizing the high streets and community markets, and reinventing them as the true centres of shopping.

Many of our markets are rotting (a strong word, but let me say it anyway). The individual stores are owned by individual owners who are not all equally capable of maintaining the same look and feel throughout. The infrastructure in and around the markets are owned or managed by several different agencies. To make matters worse, there is often no cohesiveness and no synergy in the interests of most of the members of the market association. None of these individually have the power or the mandate to recreate the shopping centre. But what if they could get together and take the help of a re-developer?

If an example is needed, New Delhi’s Connaught Place provides the example of one stage of redevelopment. Connaught Place had lost its pre-eminent position as a shopping centre, due to the spread of Delhi’s population and the new local markets that had come up. Further disruption was caused by the construction by Delhi Metro. But DMRC has reconstructed an “improved” centre, and the Metro connectivity has made the customers come back into CP, as it is affectionately known in Delhi.

There are clearly many such opportunities around India’s cities. These need to be looked at as a commercial opportunity for all concerned (revenue for the redeveloper, better sales for the store owners / tenants, more tax revenue for the government from additional sales and consumption). But it is also a broader social opportunity to breathe a new life into our cities, and to make them proud beacons of a growing India.

It would be a mission that would truly prove the worth of shopping centre developers, urban planners, regulators and the retailers themselves.

Any takers?

Devangshu Dutta

January 18, 2008

The entertainment business suggests that nostalgia is a very powerful driver of profit.

It is quite clear that retro is “in”. The movie business worldwide is full of sequels, prequels, re-releases and remakes. The music business is ringing up the cash registers with remixes and jukebox compilations. Star Wars and Sholay still have a fan following. ABBA has leaped across three decades, Hindi film songs from 30-60 years ago have been given a skin-uplift by American hip-hop artists, while Pink Floyd is hot with Indian teens along with Akon and Rihanna.

As copyright restrictions are removed from the works of authors long-gone, the market gets flooded with several reprints of their most popular writings. Of course, we know that classic literature survives not just a few years but even thousands of years. Examples include the still widely-read 2,500-year-old Indian epic Ramayana by Valmiki, the Greek philosophers’ works that continue to be popular after two millennia and the Norse legends that have been told and re-told for over a thousand years. Spiritual and religious leaders’ writings are also recycled into the guaranteed market of their followers and possible converts for a long time after their passing away.

On the other hand, the basic premise of today’s fashion and lifestyle businesses is that silhouettes, colours and design-cues will become (or be made) obsolete within a few weeks or a few months, and will be replaced with new ones. This principle is true not just of clothing and footwear, but is applied to home furnishings, furniture, white goods, electronics, mobile phones and even cars. In fact, the fashion business (as it exists) would find it impossible to survive if customers around the world chose only classics which could be used for as long as the product lasted in usable form.

What Fashionability Means for Brands

Other than individual styles or products falling out of favour, as fashions move and as the market changes, it is evident that some brands also become less acceptable, are seen as “outdated” and may also die out as they lose their customer base.

Of course, that some brands become classics is quite apparent, especially in the luxury segment where brands such as Bulgari have survived several generations of consumers, and continue to thrive.

However, the past is of relevance to the fashion sector because, other than planned or forced obsolescence, the fashion business has also long worked on another principle – that trends are cyclical.

Skirts go up and down, ties change their width, and the colour palette moves through evolution across the years. A style formula that was popular in the summer of a year in the 1970s might be just right in another summer in the first decade of the 21st century.

So, the question that comes up is whether the same logic that is applicable to individual products, styles and trends, could also be applied to brands.

The answer to whether apparently weak, dead or dying brands could be brought back to life is provided by brands such as Burberry’s, Lee Cooper and Hush Puppies. Sometimes innovative consumers create the opportunity – as with Hush Puppies in the 1980s – while in other cases (such as Burberry’s, Volkswagen’s Beetle, or Harley Davidson), vision, concerted effort and resources can make the brand attractive again.

The question then is not whether brands can be relaunched – they can. The more important question for brand owners is: should a brand be relaunched. And using the logic of the fashion business, rather than being left to linger and then dying a painful death, could brands be consciously phased-out and later brought back into the market as the trends change?

The Brand Portfolio – Diversifying Opportunities and Risks

These questions are particularly important for large companies, or in times when market growth rates are slow, or when the market is fragmented. Organic growth can be difficult in all these scenarios, and companies begin to look at developing “portfolios” by acquiring other businesses and brands, or by launching multiple brands of their own.

The car industry worldwide has lived with brand portfolio management for long. Even as companies have merged with and acquired each other, the various marques have been retained and sometimes even dead ones have been revived. The companies generally focus the brands in their portfolio on distinct customer segments and needs (such as Ford’s ownership of “Ford”, “Volvo” and “Jaguar”, or General Motors with its multiple brands), and then further play with models and product variants within those. When things go right portfolio strategies can be quite profitable, but the mistakes are especially expensive. Sensible and sensitive management of the portfolio is absolutely critical.

In the fashion and lifestyle sector, the players who already follow a portfolio strategy are as diverse as the luxury group LVMH, mainstream fashion groups like Liz Claiborne (with brands in its portfolio including Liz Claiborne, Mexx, Juicy Couture, Lucky Brand Jeans) and LimitedBrands (Limited, Victoria’s Secret, La Senza etc.), retailers such as Marks & Spencer (with its original St. Michael’s brand having given way to “Your M&S”, and also Per Una) and Chico’s (Chico’s, White House | Black Market, and Soma Intimates) who wish to capture new customer segments or re-capture lost customers. Some of these companies have launched new brands, some have relaunched their own brands, and some have even acquired competing brands.

The issue is also relevant to the Indian market, whether we consider Reliance’s revival of Vimal, the new brand ambassador for Mayur Suitings, or the PE-funded take over of Weekender. As the market begins evolving into significantly large differentiated segments, branding opportunities grow, and so will activity related to existing or old brands being resurrected and refreshed. An additional twist is provided by Indian corporate groups such as Reliance, Future (Pantaloons) and Arvind that are looking to partner international and Indian brands, or grow private labels to gain additional sales and margin.

The issue also concerns those companies whose management is attached to one or more brands owned by them which may not have been performing well in the recent past, but due to historical or sentimental reasons the management may not like to close down or sell them.

It is equally critical for potential buyers who would like to take over and turn brands around into sustainable profits. This is a real possibility in this era of private-equity funds and leveraged buyouts, where a company or a financial investor might find it cheaper and more profitable to take over an existing brand and turn it around, rather than building a new brand. This is already happening in the Indian market. More interestingly, Indian companies have also already acquired businesses in the USA and Europe, and the potential revival or relaunch of brands is certainly relevant for these companies as well.

When to Recycle and Reuse

Relaunch or acquisition of an existing active or dormant brand can be an attractive option when building a portfolio, or when a company is getting into a new market.

For the company, acquiring an existing brand is often a lower cost way to reach the customers, and also faster to roll-out the business. The company may assess that the brand already has an existing share of positive customer awareness that is active or dormant, and that the effort and resources (including money) needed to build a business from that awareness will be much less than that to create a new brand.

The risk of failure may also be lower for a relaunched brand than for a new brand.

This is because the softer aspects, the hidden psychological and emotional hooks, are already pre-designed. This provides a ready platform from which to re-launch and grow the brand.

From the customer’s point of view, there is the confidence from previous experience and usage, and possibly also nostalgia and comfort of the ‘known’.

‘Age’ or vintage is respectable and trustworthy. This is especially powerful during volatile times or in rapidly changing environments when there is uncertainty about what lies in the future, and makes an existing brand a powerful vehicle for sustaining and growing the business.

On the Downside

However, when handling brands it is also wise to keep in mind the cautionary note that mutual funds issue: “past performance is no indicator of the future”.

In re-launching active or dormant brands, there is also a downside risk. While the brand may have been strong and relevant in its last avatar, it may be totally out of place in the current market scenario. The competitive landscape would have shifted, consumers would have changed – new consumers entering the market, old consumers evolving or moving out – and the economic scenario itself may now be unfriendly to the brand.

Also, the “awareness” or “share of mind” may only be a perception in the mind of the person who is looking to re-launch the brand, and the consumer may actually not care about the brand at all. There are instances where the management of the company has been so caught up in their own perception of the brand that they have not bothered to carry out first-hand research with the target segment to check whether there is actually an unaided recall, or at worst, aided-recall of the brand. They are imagining potential strengths, when the brand has none.

It is also possible that, during its last stint in the market, the brand may have gathered negative connotations – consumers may remember it for poor products or wrong pricing, the trade may remember it for late deliveries, vendors may remember it for delayed payments…the list goes on. In such a scenario, it may be a relaunch may be a disaster.

So how does one know whether to resurrect a brand, or to reincarnate it in another form, and when to just let it die? The answers to that lie in answering the question: what is a brand? And then, what is this brand?

A Critical Question: What is a Brand?

Even in these enlightened marketing times, many people believe that the brand is the name. They believe that once you advertise a name widely and loudly enough, a brand can be created. Nothing could be further from the truth. High-decibel advertising only informs customers of the name, it cannot create a brand.

If we put ourselves in the customer’s shoes, a brand is an image, comprising of a bundle of promises on the company’s part and expectations on the customer’s part, which have been met. When promises are delivered, when expectations are met, the brand develops an attribute that it is defined by.

The promise may be of edgy design (think Apple), and the customer expects that – when the brand delivers on the promise and meets the expectation the brand image gets re-affirmed and strengthened. However, these attributes are not always necessarily all “positive” in the traditional sense. For instance, a company’s promise may be to be low-cost and low-service (think Ikea, or “low-cost airlines”), and the customer may expect that and be happy with that when the company delivers on that promise. The promise may be products with a conscience (think The Body Shop), which may strike a chord with the consumer.

What that brand actually stands for can only be created experientially. Creating this image, creation of the brand, is a complex and step-by-step process that takes place over time and over many transactions. Repetition of the same kind of experience strengthens the brand.

The brand touches everything that defines the customer’s experience – the product design and packaging, the retail store it is sold in, the service it is sold with, the after-sales interaction – all have a role to play in the creation of the brand.

For instance, to some it may sound silly that market research or how supply chain practices can help define a brand, but that is exactly how the state of affairs is for Zara. Changeovers and new fashions being quickly available are what that brand is about, and it would be impossible for Zara to deliver on that promise without leading edge supply chains, or a wide variety of trend research.

Similarly, it may sound clichéd that your salesperson defines the brand to the consumer, but even with the best products, extensive advertising, and swanky stores, for service-oriented retailers everything would fall apart if the salesperson is not up to the mark. This is indeed a sad reality faced by so many of the so-called premium and luxury brands.

Of course, brand images can be changed or updated, but the new image also needs to be reinforced through repeated action, a process just like the first time the brand was created.

Reviving a Brand: the New-Old Seesaw

Given that a brand is created over multiple interactions and repetitive delivery of certain attributes, it is only natural that the older the brand, the more potential advantage it would have over a new brand. Just the sheer time it would have spent in the market would give an old brand an edge.

An old brand can appear to be proven, experienced and secure, while a new brand could be seen as untested, raw and risky. An old brand may have had a positive relationship with the consumer, but may have been dormant due to strategic or operational reasons. In this case, reviving the brand is clearly a good idea. There is already an existing awareness of an older brand, which can act as a ready platform for launching the same or a new set of products or services. Often, there may be a connection with the consumer’s past positive experience of the brand.

On the other hand, a new brand may appear to be fresh, more up-to-date and relevant, and vigorous, compared to an old one that may be seen as outdated and tired. Certainly, if nostalgia had been all that brands needed to thrive, then old brands would never die and it would be difficult to create new brands.

Clearly, there is no single answer to whether it is a good idea to re-launch an existing or old brand. If you are considering whether it would be a good idea to revive an old brand, or to acquire and turn an existing brand around, ask yourself this:

If the answer is “No” to any of these questions, then one needs to think again. However, if the answers are all “Yes”, then a resuscitation is just what the doctor might have ordered.